- Power Generation, Transmission, & Distribution

- Power T&D Equipment Market

Power T&D Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Power T&D Equipment Market by Equipment Type (Transformers: Power Transformers, Distribution Transformers; Switchgear: Circuit Breakers, Fuses, Distribution Control Panels, Others; Cables & Lines: Conductors; Insulators & Fittings; Meters & Control Devices; Substation Equipment; Others), Voltage Level (Low Voltage, Medium Voltage, High Voltage), End-User (Utilities, Industrial, Commercial & Infrastructure, Residential), and Regional Analysis for 2026 - 2033

Power T&D Equipment Market Size and Trend Analysis

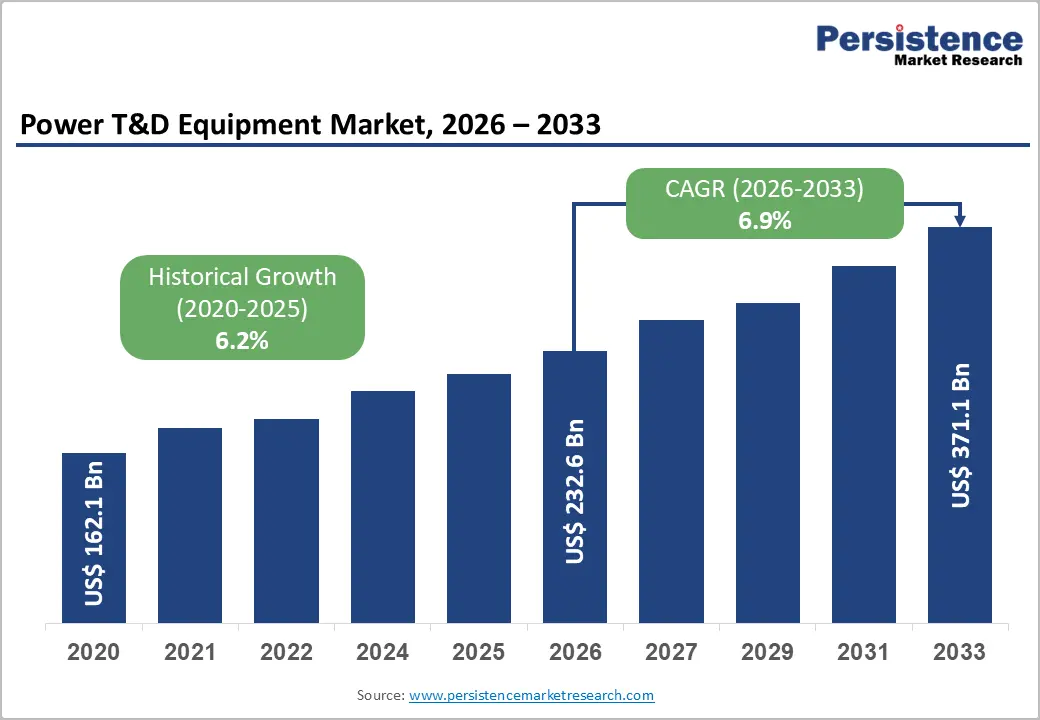

The global power T&D equipment market size is valued at US$ 232.6 billion in 2026 and is projected to reach US$ 371.1 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033.

This robust expansion is driven by an unprecedented global wave of grid modernization investment, the accelerating integration of renewable energy sources that demand upgraded transmission and distribution infrastructure, and the critical need to replace aging power equipment in developed economies while simultaneously building new grid capacity in rapidly electrifying emerging markets.

Key Industry Highlights:

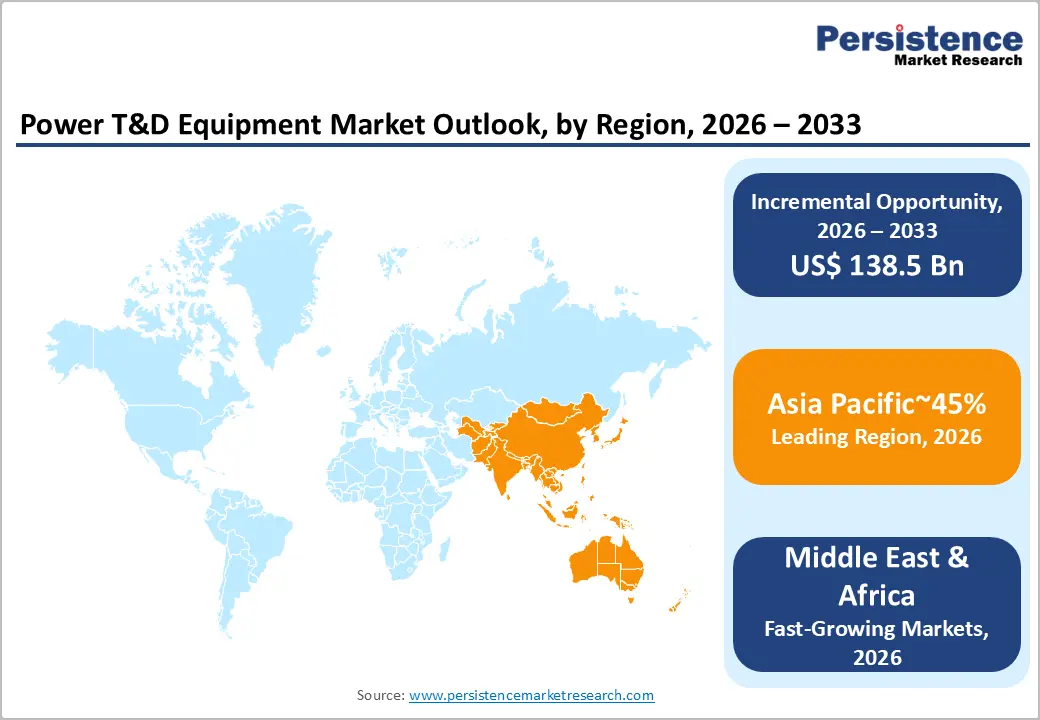

- Leading Region: Asia Pacific leads the global Power T&D Equipment market with approximately 45% of global market share, anchored by China's State Grid's investment, India's INR 3.03 trillion RDSS distribution modernization program, and rapidly electrifying Southeast Asian economies generating sustained new grid build demand.

- Fastest Growing Region: North America is the fastest-growing T&D equipment region, driven by the U.S. IIJA's US$ 65 billion clean energy grid allocation, Bank of America Institute's projection of 2.5% CAGR U.S. electrical demand growth through 2035 from data centers, EVs, and building electrification, and NREL's projection that transformer capacity requirements could increase 260% by 2050.

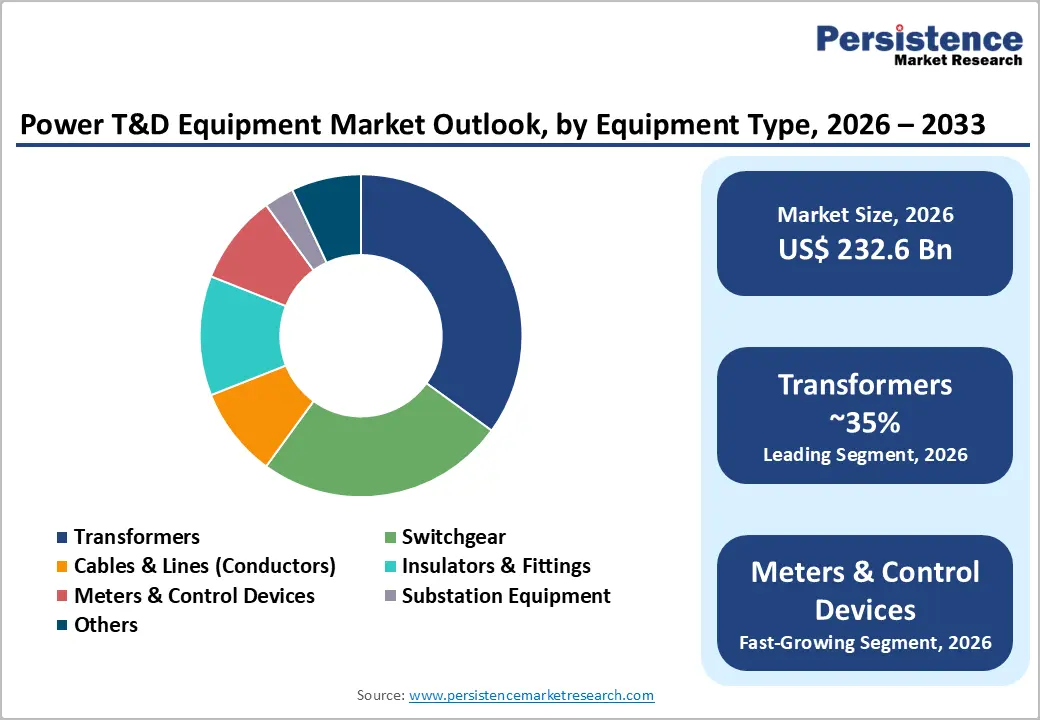

- Dominant Equipment Segment: Transformers dominate with approximately 35% of global Power T&D Equipment revenue, driven by their fundamental operational role in every grid voltage level, NREL's projection of 260% capacity increase requirements by 2050, and massive replacement demand as aging units across North America and Europe reach end-of-life service.

- Fastest Growing Segment: Smart grid and digital substation equipment within meters & control devices and substation equipment is the fastest-growing sub-segment, with the smart transformers market alone projected to grow from US$ 2.96 Bn in 2024 to US$ 7.36 Bn by 2033, as utilities invest in IEC 61850-based digital substations and IoT-enabled intelligent assets for real-time grid monitoring and optimization.

- Key Market Opportunity: HVDC transmission infrastructure for renewable energy corridor development, with the EU requiring 50,000+ km of new lines by 2030 and BOEM leasing over 20 million acres for U.S. offshore wind, creates a multi-decade pipeline for specialist HVDC converter, transformer, and switchgear systems commanding unit values of US$ 400-600 million per converter station.

DRO Analysis

Drivers - Massive Global Grid Modernization Investment Driven by Renewable Energy Integration and Electrification

The global energy transition is generating the largest single wave of grid infrastructure investment in history, as transmission and distribution networks built for centralized fossil fuel power generation must be fundamentally upgraded to accommodate decentralized, variable renewable generation from solar and wind farms, bi-directional power flows from distributed energy resources, and surging electricity demand from EV charging, data centers, and industrial electrification.

The International Energy Agency (IEA) estimates that global electricity grids need over US$ 600 billion in annual investment through 2030 to meet net-zero targets, with transmission and distribution equipment representing the core capital expenditure category.

Hitachi Energy, the world's largest transformer manufacturer, signed a landmark deal worth up to US$ 700 million with German utility E.ON in July 2025 for power and distribution transformers to modernize Germany's grid infrastructure, announced alongside the new German government's €500 billion infrastructure fund with a major energy focus. The U.S. Infrastructure Investment and Jobs Act (IIJA) has allocated US$ 65 billion specifically for clean energy transmission and grid modernization, while India's Revamped Distribution Sector Scheme (RDSS) has committed INR 3.03 trillion (approximately US$ 36 billion) to distribution network upgrades. These coordinated global public-sector investment commitments are creating a structurally elevated and multi-year demand pipeline for transformers, switchgear, cables, and substation equipment.

Aging Grid Infrastructure Replacement Creating Non-Deferrable Equipment Demand Globally

The existing power transmission and distribution infrastructure across North America, Europe, and Japan is approaching or has exceeded its designed operational lifespan, making large-scale equipment replacement a non-discretionary capital expenditure obligation for utilities regardless of economic cycle conditions. In the United States, the DOE acknowledges that the nation's electrical grid cannot currently meet expected future demand while maintaining affordable energy, with a significant proportion of installed transformers and switchgear in service for over 40 years, well beyond typical design lifetimes of 25-30 years.

The American Society of Civil Engineers (ASCE) has repeatedly awarded U.S. energy infrastructure a D+ grade in its Infrastructure Report Cards, highlighting the critical and urgent investment requirement. In Europe, the European Network of Transmission System Operators for Electricity (ENTSO-E) has identified over 50,000 km of new and refurbished transmission lines needed by 2030 under its Ten-Year Network Development Plan (TYNDP).

Restraints - Global Power Transformer Supply Chain Bottlenecks and Long Lead Times

The global power transformer market, the highest-value single equipment category in the T&D segment, is facing acute supply chain constraints, with lead times for large power transformers (100 MVA and above) extending to 80-100 weeks in 2024-2025 compared to historical norms of 40-52 weeks. This shortage reflects constrained global manufacturing capacity, concentrated in a small number of specialist manufacturers, combined with surging concurrent demand from utilities in the U.S., Europe, and Asia Pacific.

The NREL and CIGRÉ have both flagged transformer supply constraints as a significant bottleneck for achieving renewable energy integration and grid modernization timelines, with utilities reporting that equipment delivery delays are pushing back grid upgrade project completion schedules by 12-24 months in some cases.

Skilled Labor Shortage and Installation Workforce Constraints Delaying Grid Projects

The accelerating pace of grid expansion and upgrade projects globally is revealing a structural shortage of qualified electrical engineers, substation technicians, high-voltage cable installation crews, and field service specialists capable of commissioning new T&D equipment. The U.S. Bureau of Labor Statistics (BLS) has projected that demand for electrical engineers and power line workers will grow faster than the average across all occupations through 2032, while current education and apprenticeship pipelines are not generating sufficient talent at the pace required.

This workforce gap is constraining the ability of utilities and contractors to execute T&D equipment installation projects on schedule, creating a ceiling effect on the rate at which new equipment orders can be translated into commissioned infrastructure, indirectly limiting the effective deployment rate of power T&D equipment spending.

Opportunities - Smart Grid and Digital Substation Technology: Transforming T&D Equipment into Intelligent Assets

The progressive deployment of smart grid technologies, encompassing digital substations, smart transformers, grid-edge sensors, advanced metering infrastructure (AMI), and AI-powered distribution management systems, is creating a powerful commercial opportunity for T&D equipment manufacturers to transition from commodity hardware suppliers to premium intelligent system providers. Hitachi Energy unveiled its PASS M00-Wind dual-breaker switchgear at the 8th China International Import Expo in 2025, designed for high-capacity wind turbines and supporting the expansion of next-generation offshore wind farms, exemplifying the product innovation trajectory across digital and intelligent T&D equipment platforms.

The IEA has confirmed that digital grid technologies, enabled by IoT sensors, communication protocols, and software analytics, can reduce distribution losses by up to 15% and improve grid capacity utilization by 10-20%. Equipment manufacturers including ABB, Siemens Energy, Schneider Electric, and Hitachi Energy are investing heavily in digital twin platforms, IEC 61850-based communication protocols, and AI-driven predictive maintenance capabilities that fundamentally differentiate intelligent T&D products from conventional equipment and command significant pricing premiums.

Offshore Wind and HVDC Transmission Infrastructure: A High-Value Equipment Frontier

The global offshore wind energy expansion, combined with the need to transmit renewable energy from generation hubs to distant demand centers using High Voltage Direct Current (HVDC) technology, is creating a distinct and high-value segment of T&D equipment demand that rewards manufacturers with specialized high-power, high-voltage engineering capabilities. The European Union's offshore wind target of 120 GW by 2030 requires hundreds of offshore wind substation platforms equipped with specialized transformers, switchgear, and power electronics capable of operating in harsh marine environments, a technically demanding and premium-priced equipment category.

Hitachi Energy's OceaniQ™ portfolio, covering fixed, floating, and subsea offshore wind applications, and the successful commissioning of its 66 kV HiDry dry-type transformer at the Huaneng Shandong Offshore Wind Farm in 2025 demonstrate the growing commercial maturity of purpose-engineered offshore T&D equipment.

The U.S. Bureau of Ocean Energy Management (BOEM) has leased over 20 million acres of offshore areas for wind development, each requiring substantial offshore substation and cable infrastructure investment. HVDC converter stations, costing US$ 400-600 million each, represent the highest unit-value single equipment purchase in the power sector, with global HVDC project pipelines in Europe, China, and India generating multi-billion-dollar procurement programs for specialist T&D equipment suppliers with HVDC capabilities.

Category-wise Analysis

Equipment Type Insights

Transformers constitute the dominant equipment type segment, accounting for approximately 35% of total global Power T&D Equipment market revenue. Transformers are the most fundamental and highest unit-value component in every transmission and distribution network, enabling efficient voltage step-up and step-down operations that make long-distance bulk power transmission and localized distribution economically feasible.

Their revenue dominance reflects both the sheer ubiquity of transformer deployment across the grid hierarchy, from Extra High Voltage (EHV) power transformers at transmission substations to pole-mounted distribution transformers at every residential and commercial street, and the sustained global demand for transformer replacements, capacity upgrades, and new installations driven by renewable integration and grid expansion.

The NREL projects that U.S. transformer capacity requirements could increase by 260% by 2050, underscoring the extraordinary scale of transformer demand ahead. Leading manufacturers Hitachi Energy, ABB, Siemens Energy, and Hyosung Heavy Industries collectively serve the global transformer market with products spanning the full capacity and voltage range from distribution to ultra-high voltage applications.

Voltage Level Insights

High Voltage is the leading voltage level segment, commanding approximately 45% of total global Power T&D Equipment market revenue. High-voltage equipment, encompassing high-voltage transformers (66 kV and above), high-voltage circuit breakers, gas-insulated switchgear (GIS), and HVDC converter systems, commands market revenue leadership due to its high unit value, the strategic importance of transmission-level infrastructure in national grid architectures, and the accelerating global investment in long-distance high-capacity power transmission corridors required to connect remote renewable energy generation zones to urban load centers.

In China, the State Grid Corporation of China (SGCC) is the world's largest single investor in high-voltage and ultra-high-voltage (UHV) transmission infrastructure, having invested in a global-scale network of UHV AC and DC transmission lines that required specialized high-voltage equipment from domestic manufacturers including NR Electric Co., Ltd. and international suppliers.

End-user Insights

Utilities dominate the end-user segment, accounting for approximately 52% of total global power T&D Equipment market revenue. Electric utilities, encompassing transmission system operators (TSOs), distribution network operators (DNOs), and vertically integrated power companies, are by far the largest and most consistent buyers of power T&D equipment globally, as grid infrastructure ownership, operation, and capital renewal is their core business function. Utility procurement of power T&D equipment is driven by regulated asset base expansion and replacement cycles, government-mandated reliability standards, renewable integration compliance requirements, and long-term network development plans.

The U.S. Energy Information Administration (EIA) confirmed that U.S. electric utilities collectively invested over US$ 130 billion in transmission and distribution infrastructure in 2023, one of the highest annual T&D capex levels ever recorded in the United States. China's State Grid Corporation of China (SGCC) and India's state-owned distribution companies (DISCOMs) investing under the RDSS scheme represent the world's two largest utility-sector T&D equipment procurement programs, with combined annual investment running into tens of billions of dollars.

Regional Insights

North America Power T&D Equipment Trends & Insights

The United States is the largest single-country market for power T&D equipment in North America, driven by the most significant grid modernization investment cycle in the country's modern history, catalyzed by the U.S. Infrastructure Investment and Jobs Act's (IIJA) US$ 65 billion clean energy grid allocation, the Inflation Reduction Act's incentives for clean energy infrastructure, and the DOE's Grid Deployment Office initiatives targeting transmission expansion and resilience.

Bank of America Institute's July 2025 analysis confirms that U.S. electrical demand is projected to grow at 2.5% CAGR through 2035, driven by data center construction, building electrification, industrial demand, and EV adoption, each of which requires new and upgraded T&D infrastructure investment.

Florida power & light's smart grid technology, demonstrating the ability to prevent 900,000 outages during hurricanes, and Duke Energy's self-healing technology, preventing 300 million minutes of downtime, exemplify the measurable ROI driving smart T&D equipment adoption.

Canada complements the North American market through large-scale hydroelectric transmission upgrades and inter-provincial grid interconnection investments. General Electric Company, Eaton Corporation, and Schneider Electric maintain major North American T&D equipment manufacturing and service footprints, while Hitachi Energy has announced significant capacity investments to serve growing North American demand.

The U.S. Federal Energy Regulatory Commission (FERC) Order 1000 and the FERC Order 2023 for interconnection reform are streamlining grid expansion approvals, clearing regulatory bottlenecks that had constrained transmission investment. North America is expected to be the fastest-growing region for T&D equipment investment through 2033, reflecting both the scale of deferred infrastructure replacement and new renewable integration requirements.

Europe Power T&D Equipment Trends & Insights

Europe is undergoing its most consequential power grid transformation in decades, driven by the European Green Deal's clean energy transition mandate, the REPowerEU program's urgent diversification away from Russian gas toward domestic renewable generation, and the ENTSO-E's requirement for over 50,000 km of new and upgraded transmission lines by 2030 under the Ten-Year Network Development Plan (TYNDP).

Germany is the continent's largest single T&D equipment market, reflecting both the scale of its power infrastructure and its ambitious Energiewende energy transition program, with the new German government's €500 billion infrastructure fund including a major energy component. Hitachi Energy's landmark US$ 700 million deal with E.ON for power and distribution transformers in Germany, announced in July 2025, is the most prominent single demonstration of European grid investment momentum translating into T&D equipment procurement.

The United Kingdom's National Grid and transmission operators in France (RTE), Spain (Red Eléctrica), and Italy (Terna) are all executing multi-billion-euro grid investment programs driven by offshore wind integration, cross-border interconnector expansion, and aging asset replacement.

The EU's Internal Electricity Market Regulation and Network Codes provide regulatory harmonization for cross-border grid operation and investment standards, while the European Commission's revised Electricity Market Design framework is accelerating investment approval and cost recovery for grid infrastructure projects. European T&D equipment manufacturers, including ABB, Siemens Energy, and Schneider Electric, hold structural advantages in serving European utility customers through their regulatory expertise, localized manufacturing, and deep technical service networks.

Asia Pacific Power T&D Equipment Trends & Insights

Asia Pacific is the world's dominant Power T&D Equipment region, commanding approximately 45% of global market volume, driven by the world's largest single national power infrastructure programs in China and India, the rapid electrification of Southeast Asian economies, and Japan's grid modernization and offshore wind development initiatives.

China's State Grid Corporation (SGCC), the world's largest utility by assets, continues to invest on a scale unmatched globally, with its Ultra High Voltage (UHV) transmission network comprising over 40,000 km of UHV lines transmitting renewable power from the country's western generation hubs to eastern demand centers. China's 14th Five-Year Plan specifically targets US$ 480 billion in power grid investment through 2025, while the 15th Five-Year Plan (commencing 2026) is expected to sustain comparable grid investment levels aligned with carbon neutrality targets.

India is the Asia Pacific's fastest-growing T&D equipment market, with the Revamped Distribution Sector Scheme (RDSS) committing INR 3.03 trillion (~US$ 36 billion) to distribution network modernization and loss reduction across the country's DISCOM ecosystem. Hitachi Energy announced US$ 250 million in India-specific investments in October 2024, including the expansion of large power transformer factory capacity and upgraded testing capabilities, directly responding to accelerating domestic grid investment.

Bharat Heavy Electricals Limited (BHEL) and CG Power and Industrial Solutions serve as the country's leading domestic T&D equipment manufacturers, benefiting from government Make in India policies that mandate local content in public utility procurement. Southeast Asian nations, including Vietnam, Indonesia, Philippines, and Thailand are investing in new generation capacity and grid expansion to serve growing industrial and residential demand, creating multi-year procurement pipelines for T&D equipment from both domestic and international suppliers.

Competitive Landscape

The global power T&D equipment industry is moderately consolidated at the premium tier, with a small number of globally integrated electrical equipment conglomerates, Hitachi Energy, Siemens Energy, ABB, Schneider Electric, and GE, commanding dominant shares in high-voltage and digital T&D equipment. Mid-market competition is increasingly intense, with Korean (Hyosung, Hyundai Electric), Japanese (Mitsubishi Electric, Toshiba, Nissin Electric), and Chinese (NR Electric) manufacturers competing aggressively on price-to-performance in emerging markets.

Key competitive differentiators include digital substation and smart grid integration capability, HVDC system engineering expertise, green and SF6-free switchgear development, and comprehensive global service networks. Emerging competitive models include outcome-based grid performance contracts, digital twin-as-a-service offerings, and modular prefabricated substation solutions that accelerate deployment timelines.

Key Developments:

- In July 2025, Hitachi Energy signed a landmark deal worth up to US$ 700 million with German utility E.ON to supply power and distribution transformers for critical grid infrastructure modernization in Germany, announced alongside the new German government's €500 billion infrastructure fund focused on energy.

- In November 2025, Hitachi Energy unveiled the PASS M00-Wind dual-breaker switchgear and successfully commissioned its 66 kV HiDry dry-type transformer at the Huaneng Shandong Offshore Wind Farm in China, reinforcing its technology leadership in offshore wind T&D equipment.

- In October 2024, Hitachi Energy announced investments of approximately US$ 250 million (INR 2,000 crore) in India to expand large power transformer production capacity, upgrade specialty transformer testing capabilities, and boost traction transformer output for Indian railway modernization.

Companies Covered in Power T&D Equipment Market

- Hitachi Energy Ltd.

- Siemens Energy AG

- General Electric Company

- Schneider Electric SE

- ABB Ltd.

- Eaton Corporation plc

- Mitsubishi Electric Corporation

- Toshiba Energy Systems & Solutions Corporation

- Hyosung Heavy Industries

- CG Power and Industrial Solutions Ltd.

- Bharat Heavy Electricals Limited (BHEL)

- NR Electric Co., Ltd.

- Nissin Electric Co., Ltd.

- Hyundai Electric & Energy Systems

- WEG S.A.

Frequently Asked Questions

The global Power T&D Equipment market is valued at US$ 232.6 Bn in 2026 and is projected to reach US$ 371.1 Bn by 2033, growing at a CAGR of 6.9% during the forecast period. This growth is anchored by the IEA's estimate of over US$ 600 billion in annual grid investment needed globally through 2030 and the U.S. IIJA's US$ 65 billion clean energy grid allocation driving North America's fastest-growing T&D equipment investment cycle.

The two primary drivers are: (1) global grid modernization investment driven by renewable energy integration and the IEA's confirmation of over US$ 600 billion in annual grid investment needed by 2030, with Hitachi Energy's US$ 700 million E.ON deal in Germany (July 2025) exemplifying this acceleration; and (2) aging infrastructure replacement, with the NREL projecting U.S. transformer capacity requirements increasing by 260% by 2050 and ENTSO-E requiring 50,000+ km of new European transmission lines by 2030.

Transformers (Power and Distribution combined) lead the Equipment Type category with approximately 35% of global market revenue, driven by their non-negotiable operational role at every voltage level of the grid hierarchy, from Extra High Voltage transmission substations to distribution-level pole-mounted units.

Asia Pacific leads the global Power T&D Equipment market with approximately 41-45% of global share, driven by China's State Grid Corporation (SGCC) investing US$ 480 billion in grid infrastructure under the 14th Five-Year Plan, including the world's most extensive Ultra High Voltage (UHV) transmission network, and India's Revamped Distribution Sector Scheme (RDSS) committing INR 3.03 trillion (~US$ 36 billion) to distribution network modernization.

The most significant opportunity is HVDC transmission infrastructure for renewable energy corridors, with the EU requiring 50,000+ km of new transmission lines by 2030 under ENTSO-E's TYNDP and BOEM leasing over 20 million acres for U.S. offshore wind, generating multi-decade demand for specialist HVDC converter systems and offshore substation equipment valued at US$ 400-600 million per converter station, accessible only to manufacturers with certified HVDC engineering capability.

The global Power T&D Equipment market is led by Hitachi Energy Ltd., ABB Ltd., Siemens Energy AG, Schneider Electric SE, GE (GE Vernova), Eaton Corporation, Mitsubishi Electric Corporation, Toshiba Energy Systems, Hyosung Heavy Industries, CG Power and Industrial Solutions, BHEL, NR Electric Co., Hyundai Electric & Energy Systems, Nissin Electric, and WEG S.A., among others.