- Food Ingredients & Additives

- Plant-Based Flavor Market

Plant-Based Flavor Market Size, Share, and Growth Forecast, 2025 - 2032

Plant-Based Flavor Market By Source (Fruits & Vegetables, Herbs & Spices, Others), Form (Liquid, Powder, Others), Application, and Regional Analysis for 2025 - 2032

Plant-Based Flavor Market Size and Trends Analysis

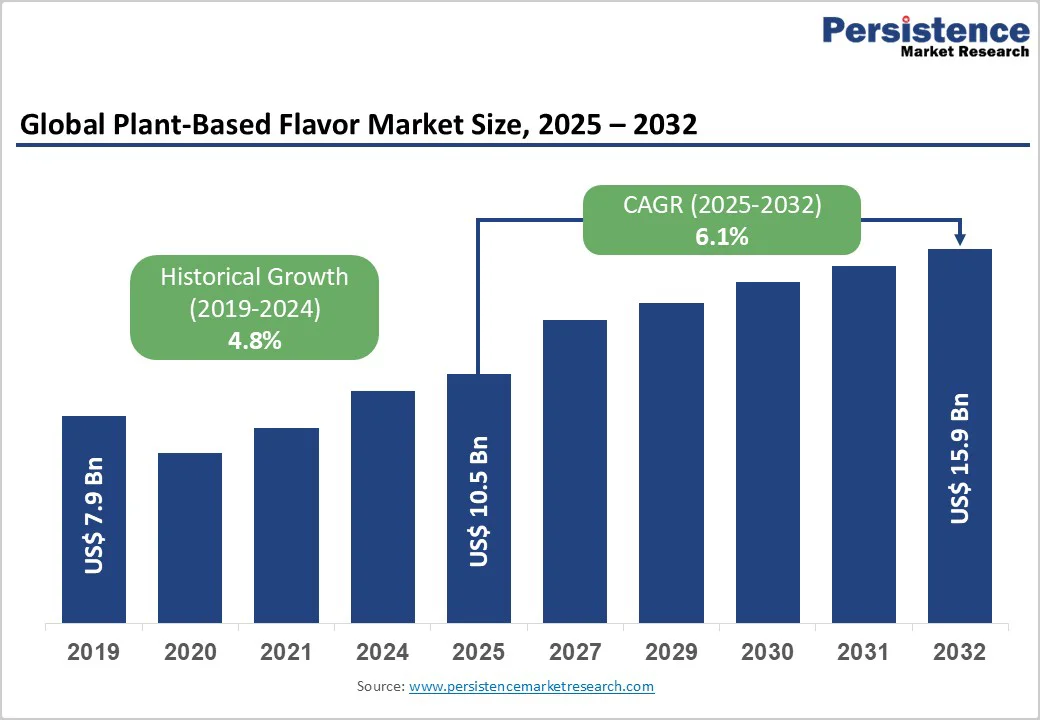

The global plant-based flavor market size is likely to be valued at US$10.5 Billion in 2025 and is expected to reach US$15.9 Billion by 2032, growing at a CAGR of approximately 6.1% during the forecast period from 2025 to 2032, driven by the rising consumer shift toward plant-derived ingredients, clean-label products, and vegan formulations in food, beverages, and nutraceuticals. Increasing investments in natural flavor extraction technologies and the growing penetration of sustainable food manufacturing are reinforcing long-term growth. The adoption of botanical flavors in alternative dairy, plant-based meat, and functional beverages is strengthening global demand.

Key Industry Highlights

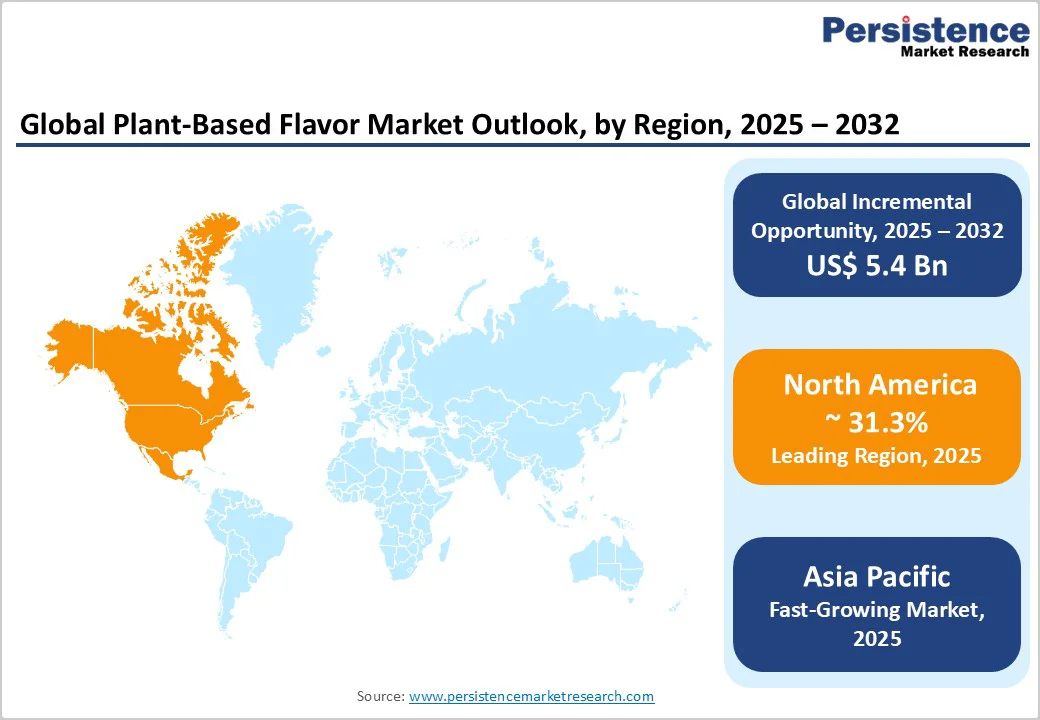

- Leading Region: North America holds a dominant 31.3% share of global revenue in 2025, supported by strong adoption of plant-based foods, advanced flavor extraction technologies, and high consumer trust in clean-label ingredients.

- Fastest-growing Region: Asia Pacific, driven by rapid urbanization, expanding middle-class populations, and increasing demand for natural and sustainable food flavors.

- Investment Plans: Major investments focus on flavor fermentation facilities, bio-based extraction R&D, and AI-driven flavor formulation, with expansion projects in California, Singapore, and India aimed at improving scalability and cost efficiency.

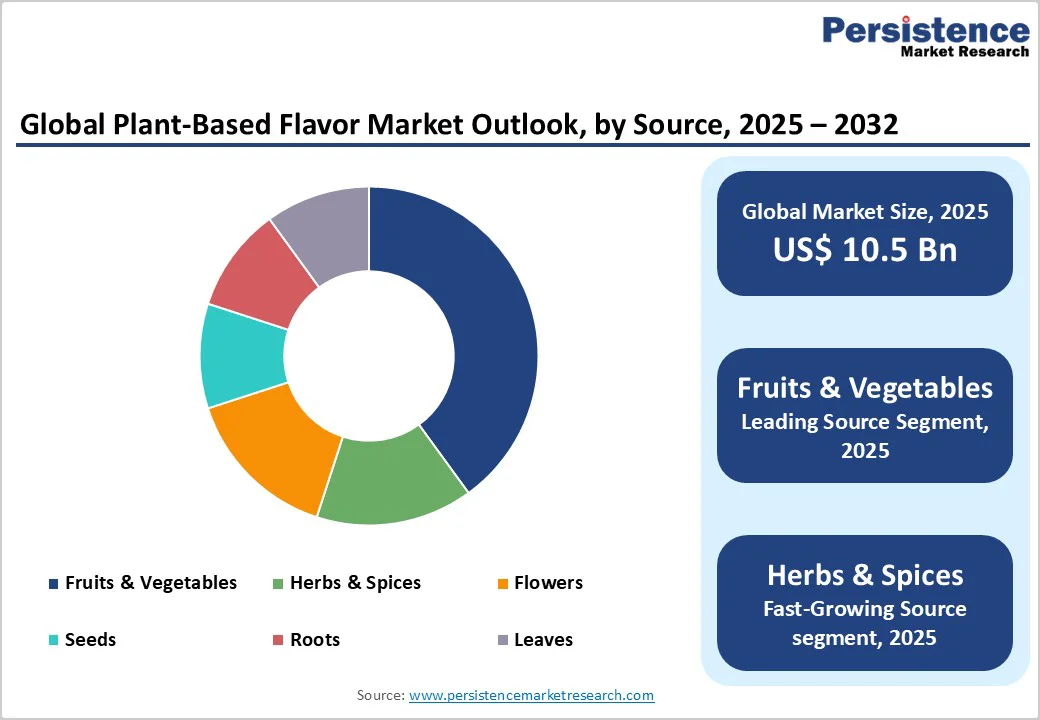

- Dominant Source: Fruits & vegetables hold 40.7% share in 2025, with citrus, apple, berry, and tropical fruit profiles leading demand in beverages, confectionery, and bakery sectors.

- Leading Application: Beverages capture roughly 39.2% of global demand in 2025, making beverages the single largest application for plant-based flavors, driven by flavored waters, plant-based milks, RTD teas, and functional drinks.

| Key Insights | Details |

|---|---|

| Plant-Based Flavor Market Size (2025E) | US$10.5 Bn |

| Market Value Forecast (2032F) | US$15.9 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Global Demand for Clean-Label and Natural Ingredients

The surging consumer preference for clean-label formulations has substantially influenced flavor manufacturing. According to industry food surveys, over 65% of global consumers now prefer products with transparent, natural ingredients. This behavioral shift has accelerated the substitution of synthetic flavoring agents with plant-derived alternatives such as vanilla, mint, citrus, and herbal extracts. Companies in the F&B sector are investing in natural sourcing and biotechnological flavor extraction to ensure purity and traceability, thereby driving growth across beverage and snack segments.

Expansion of the Plant-Based Food and Beverage Industry

The broader plant-based food sector, valued at over US$45 Billion in 2024, is creating large-scale opportunities for natural flavor manufacturers. Demand for flavor modulation in meat alternatives, dairy substitutes, and ready-to-eat meals is growing steadily. Manufacturers are leveraging botanical flavor systems to replicate authentic taste and mouthfeel. This trend is reinforced by increasing vegan and flexitarian populations, particularly in North America and Europe, enhancing revenue potential for flavor developers.

Technological Advancements in Extraction and Fermentation

Advancements in extraction technologies such as supercritical CO? extraction, enzymatic processing, and natural fermentation have revolutionized the purity and yield of plant-based flavor compounds. Biotechnological innovation allows sustainable production of high-impact flavors such as vanillin and steviol glycosides without reliance on chemical synthesis. These methods reduce waste, energy consumption, and environmental impact, aligning with the sustainability goals of multinational food companies and supporting long-term market scalability.

Barrier Analysis - High Production and Raw Material Costs

The cost structure of plant-based flavor production remains higher than that of synthetic counterparts due to raw material volatility, low extraction yields, and complex processing steps. Natural sources such as vanilla beans or citrus peel exhibit yield inconsistencies depending on climatic conditions, affecting supply stability. This price imbalance limits adoption in mass-market products and pressures margins for smaller manufacturers.

Limited Shelf Life and Formulation Challenges

Plant-derived flavors often face stability issues when exposed to high temperatures or light, leading to degradation during food processing or extended storage. Maintaining sensory quality without chemical stabilizers poses challenges in high-volume manufacturing. These formulation barriers restrict usage in specific applications such as baked goods and frozen foods, slowing down widespread adoption.

Opportunity Analysis - Expansion into Functional Food and Nutraceutical Applications

The increasing convergence of flavor science and nutrition presents a strong growth frontier. Plant-based flavors derived from herbs, spices, and botanicals are being integrated into dietary supplements and functional beverages for enhanced taste and perceived health benefits. This emerging application segment is expected to generate over US$1.2 Billion in new opportunities by 2032, driven by growing consumer emphasis on wellness-oriented products.

Growing Potential in Emerging Economies

Asia-Pacific and Latin America are becoming high-growth hubs due to evolving consumer tastes and rapid retail penetration. Urban populations with higher disposable income are shifting toward sustainable food consumption. The rising adoption of plant-based dairy alternatives and snacks in countries such as India, China, and Brazil provides a fertile market for flavor manufacturers. Localization of sourcing and production is expected to reduce costs and increase competitiveness.

Regulatory Push Toward Natural Additives

Global food regulatory agencies are tightening restrictions on artificial flavoring agents and encouraging natural alternatives. Compliance with safety and labeling standards promotes transparency and consumer confidence. This regulatory shift, combined with the demand for sustainable sourcing, positions plant-based flavors as a long-term substitute for synthetic compounds across mainstream categories.

Category-wise Analysis

Source Insights

The fruits and vegetables segment leads the global market, accounting for over 40.7% of the total share in 2025. Its dominance stems from strong consumer demand for refreshing, familiar, and naturally sweet flavor profiles. Popular fruit-based flavors such as citrus, apple, berry, mango, and pineapple remain key across beverages, confectionery, and bakery applications. Advancements in extraction methods, including cold-pressing and CO? supercritical extraction, have improved flavor stability and aromatic retention, enabling large-scale production. Beverage brands are expanding offerings with tropical flavors such as dragon fruit, passion fruit, and yuzu, while vegetable-derived options such as beetroot, cucumber, and carrot are gaining traction in smoothies, soups, and plant-based snacks.

The herbs and spices segment is the fastest-growing, supported by the rising popularity of aromatic and health-driven flavoring. Ingredients such as basil, ginger, turmeric, cinnamon, and mint are increasingly used in sauces, condiments, and functional drinks for their wellness benefits, particularly anti-inflammatory and antioxidant properties. In Europe and Asia, producers are launching herbal teas, spiced coffees, and immunity beverages infused with ginger, lemongrass, and turmeric. Innovative regional spice blends, such as masala chai and chili-lime seasoning, are broadening appeal across global cuisines, driving rapid segment expansion.

Application Insights

The beverage segment leads the global market, accounting for nearly 39.2% of the total demand in 2025. Fruit-based and herbal infusions dominate this category, particularly in carbonated drinks, flavored waters, ready-to-drink teas, and plant-based milks. Beverage producers are emphasizing natural flavor authenticity to attract health-conscious millennials and Gen Z consumers who increasingly avoid artificial additives. The surge in functional beverages, such as energy drinks with natural caffeine sources, including guarana and green tea, and electrolyte-rich options such as coconut or aloe vera water, has intensified demand for plant-derived flavor solutions. Brands are also crafting sophisticated botanical blends, including lavender-lemon, hibiscus-berry, and cucumber-mint, to offer unique sensory experiences. Expanding retail distribution and the premiumization of wellness beverages continue to sustain this segment’s market leadership.

The dairy alternatives and plant-based meat segment represents the fastest-growing category. Flavor innovation is crucial to replicating authentic dairy and meat profiles while improving sensory appeal. Plant-based modulators help mask earthy or beany notes in protein bases such as soy, pea, and lentil, enhancing creamy or savory characteristics. Producers of oat milk, almond yogurt, and coconut ice cream are adding fruit and caramel notes, while plant-based meat brands use natural smoke, spice, and umami extracts to achieve realistic flavor depth, fueling rapid market expansion.

Regional Insights

North America Plant-Based Flavor Market Trends - Biotechnology-Driven Innovation and Regulatory Transparency Fuel Growth

North America maintains a commanding position, contributing over 31.3% of the global revenue in 2025. The U.S. remains the largest national market, supported by the widespread adoption of plant-based food and beverage alternatives, a mature retail distribution infrastructure, and strong consumer preference for clean-label and sustainable flavor ingredients. The regional market benefits from increasing investments in biotechnology-driven flavor extraction, including the use of precision fermentation and bio-conversion technologies to replicate natural taste profiles at scale.

Regulatory agencies such as the U.S. Food and Drug Administration (FDA) continue to emphasize the use of natural and transparent labeling, which has reinforced consumer confidence and encouraged innovation across the value chain. Companies are prioritizing R&D initiatives to enhance flavor intensity and stability while maintaining natural authenticity. A notable recent development includes the expansion of flavor fermentation facilities in California and Texas, focusing on scalable production of natural vanillin and fruit-based notes through microbial processes.

Strategic collaborations between food manufacturers and biotech startups, for instance, partnerships to develop non-GMO, enzyme-derived natural sweet flavors, illustrate the region’s forward momentum. This convergence of technology, regulation, and consumer demand has positioned North America as a global leader in sustainable flavor innovation.

Europe Plant-Based Flavor Market Trends -Sustainability, Circular Production, and AI-Led Flavor Innovation

Europe represents the second-largest regional market, accounting for around 28% of the global revenue share in 2025. Countries, including Germany, France, the U.K., and Spain, are at the forefront of flavor innovation, driven by stringent regulatory frameworks, eco-conscious consumer preferences, and a strong focus on sustainability goals under the EU Green Deal. The market is significantly shaped by policies emphasizing natural additives, non-GMO certification, and traceable supply chains. This has fostered the expansion of botanical and floral flavor profiles in the bakery, dairy, and premium confectionery sectors.

Major regional producers are investing in circular production systems and carbon-neutral manufacturing, aligning with Europe’s environmental sustainability objectives. For example, several flavor producers in France and the Netherlands recently launched upcycled fruit extract lines, utilizing surplus agricultural produce to minimize waste. European flavor houses are also increasingly collaborating with local farming cooperatives to ensure ethical sourcing and transparent ingredient origin.

The rising integration of AI-driven sensory analytics to predict consumer taste trends and optimize flavor formulation reflects another layer of innovation. With its blend of regulatory discipline and sustainable technology adoption, Europe continues to serve as a hub for flavor research and a key exporter of advanced formulations to North America and Asia Pacific.

Asia Pacific Plant-Based Flavor Market Trends - Rapid Expansion through Localization and Sustainable Manufacturing

Asia Pacific is the fastest-growing region driven by urbanization, rising disposable incomes, and shifting dietary preferences in key economies such as China, India, Japan, and ASEAN countries. A growing number of consumers are turning toward plant-based dairy, snacks, and beverages, influenced by both health awareness and environmental sustainability concerns. Local manufacturers are scaling natural flavor extraction and fermentation technologies to meet the surging demand for authentic, clean-label ingredients.

Governments across the region are implementing policies to encourage sustainable and locally sourced food production. For instance, India’s Production-Linked Incentive (PLI) scheme has indirectly supported the food processing sector, encouraging domestic flavor innovation. In China, the expansion of flavor R&D centers by major global firms, such as those in Shanghai and Guangzhou, has accelerated product localization.

A recent example includes new natural citrus and spice flavor plants launched in Singapore and Malaysia to cater to the regional beverage and snack industries. Joint ventures between multinational corporations and local enterprises are improving cost efficiency, technology transfer, and supply resilience. With an expanding millennial and Gen Z consumer base prioritizing natural ingredients, Asia Pacific is expected to contribute the largest share of incremental market revenue through 2032.

Competitive Landscape

The global plant-based flavor market remains moderately consolidated, with leading players accounting for an estimated 45–50% of total revenue. Large multinational firms dominate through diversified portfolios and global supply networks, while regional specialists focus on niche botanical and herbal extracts. Competition is based on product innovation, quality certification, and sustainable sourcing. Increasing partnerships with food manufacturers are enhancing vertical integration and reducing supply chain risks.

Market leaders are pursuing strategies centered on innovation, sustainable sourcing, and regional diversification. Companies are integrating advanced bioprocessing technologies and focusing on traceability to meet regulatory standards and strengthen consumer confidence. Cost optimization through localized supply chains remains a key competitive differentiator.

Key Industry Developments

- In June 2025, Sensient Flavors & Extracts announced the launch of BioSymphony, a portfolio of natural flavors created through biotransformation of plant ingredients, aiming to expand its clean-label and sustainable offering.

- In June 2025, Givaudan S.A. revealed its participation in a major technology conference to showcase digital advances in flavor development and ‘story-smelling’ experiences, underscoring its investment in next-gen flavor innovation.

- In March 2025, flavor houses published new reports on AI-powered precision fermentation and machine-learning platforms enabling replication of complex flavor molecules such as cultivated saffron and plant-derived umami enhancers, signalling a technological leap in flavor sourcing.

Companies Covered in Plant-Based Flavor Market

- Givaudan SA

- Symrise AG

- Kerry Group plc

- International Flavors & Fragrances Inc. (IFF)

- Takasago International Corporation

- Sensient Technologies Corporation

- Firmenich SA

- Mane SA

- Döhler GmbH

- ADM (Archer Daniels Midland Company)

- Tate & Lyle PLC

- Robertet Group

- T. Hasegawa Co., Ltd.

- Blue California

- Bell Flavors & Fragrances

- Flavorchem Corporation

- Synergy Flavors Inc.

- Huabao International Holdings Limited

- McCormick & Company, Inc.

- Planteneers GmbH

Frequently Asked Questions

The plant-based flavor market size is valued at US$10.5 Billion in 2025.

By 2032, the plant-based flavor market is projected to reach US$15.9 Billion.

Key trends include flavor fermentation technologies, CO₂ extraction methods, and rising demand for botanical and herbal infusions in beverages and snacks.

The fruits and vegetables segment leads by source, accounting for over 40.7% of market share in 2025, while beverages dominate by application with about 39.2% share due to growing demand for fruit-based and herbal drinks.

The plant-based flavor market is expected to grow at a CAGR of 6.1% from 2025 to 2032.

Major companies include Givaudan SA, Symrise AG, Kerry Group plc, International Flavors & Fragrances Inc., and Takasago International Corporation.