- Healthcare Services

- Neurosurgery Market

Neurosurgery Market Size, Share, and Growth Forecast 2026 - 2033

Neurosurgery Market by Product (Neuro Interventional Devices: Neurovascular Embolization Devices, Neurovascular Coiling Assist Devices, Neurovascular Thrombectomy Devices, Microguidewires, Microcatheters, Others; Neuroendoscopes; Radiosurgery Systems: Linear Accelerator, GammaKnife; Dura Substitutes; Neurosurgical Ablation Devices; Neurosurgery Instruments), Indication (Peripheral Nerve Disorders, Brain Tumours, Traumatic Brain Injuries (TBI), Cerebrovascular Disorders, Epilepsy, Brain Hemorrhages or Stroke, Others), End-user, and Regional Analysis, 2026 - 2033

Neurosurgery Market Share and Trends Analysis

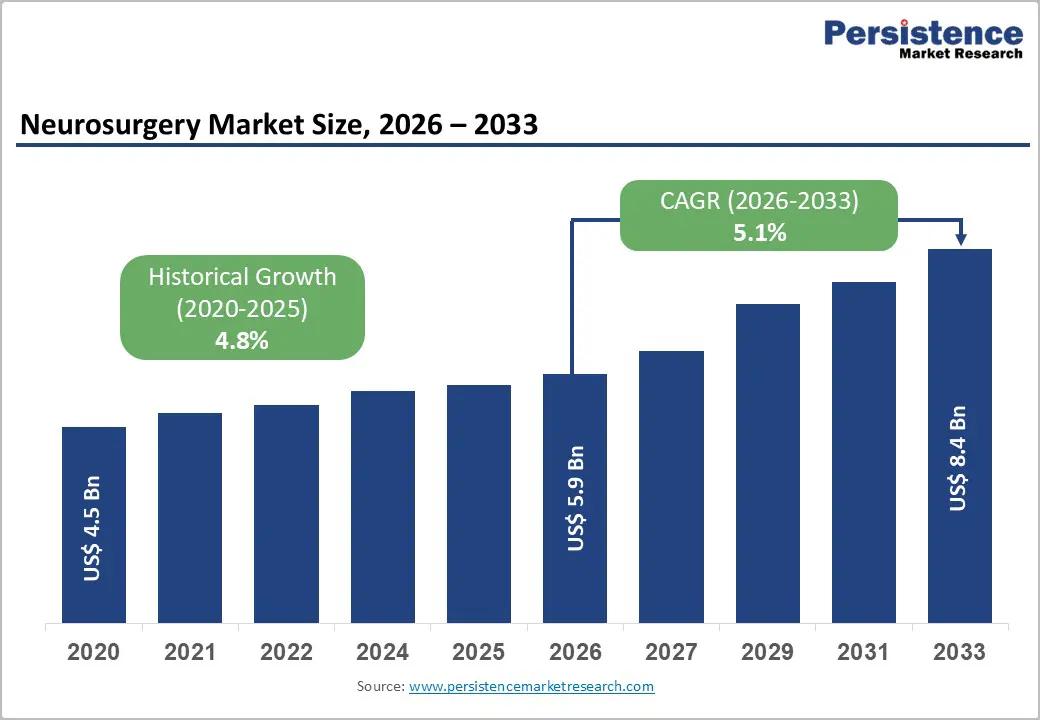

The global neurosurgery market size is expected to be valued at US$ 5.9 billion in 2026 and projected to reach US$ 8.4 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033. This is driven by the rise in global burden of neurological conditions, including traumatic brain injury, stroke, brain tumors, and epilepsy, combined with rapid innovation in minimally invasive neurosurgical techniques, neuro-interventional devices, and stereotactic radiosurgery systems. The World Health Organization (WHO) estimates that neurological disorders affect over 1 billion people worldwide, making them a leading cause of disabilities across the globe.

Expanding access to neurosurgical care in the Asia Pacific, growing adoption of robot-assisted neurosurgery, and strong device innovation pipelines from leaders, including Medtronic, Stryker, and Brainlab AG are collectively sustaining the market's upward trajectory through the 2033 forecast period.

Key Industry Highlights

- Leading Region: North America leads the global Neurosurgery market with approximately 38% revenue share in 2025, driven by 150+ Joint Commission-certified Comprehensive Stroke Centers, AANS-accredited neurosurgery training, and strong FDA commercialization pathways for neurosurgical devices.

- Fast-Growing Market: Asia Pacific is the fast-growing neurosurgery region during the forecast period anchored by China's ~3 million annual strokes (Chinese Stroke Association), India's Ayushman Bharat capacity expansion, Japan's mature device market, and growing Southeast Asian tertiary neurosurgery infrastructure.

- Dominant Product Segment: Neuro interventional devices lead the product category with approximately 36% market share in 2025, driven by clinical adoption of mechanical thrombectomy systems Penumbra, Medtronic Solitaire, Stryker Trevo, backed by landmark stroke trial evidence demonstrating 3-fold outcome improvements.

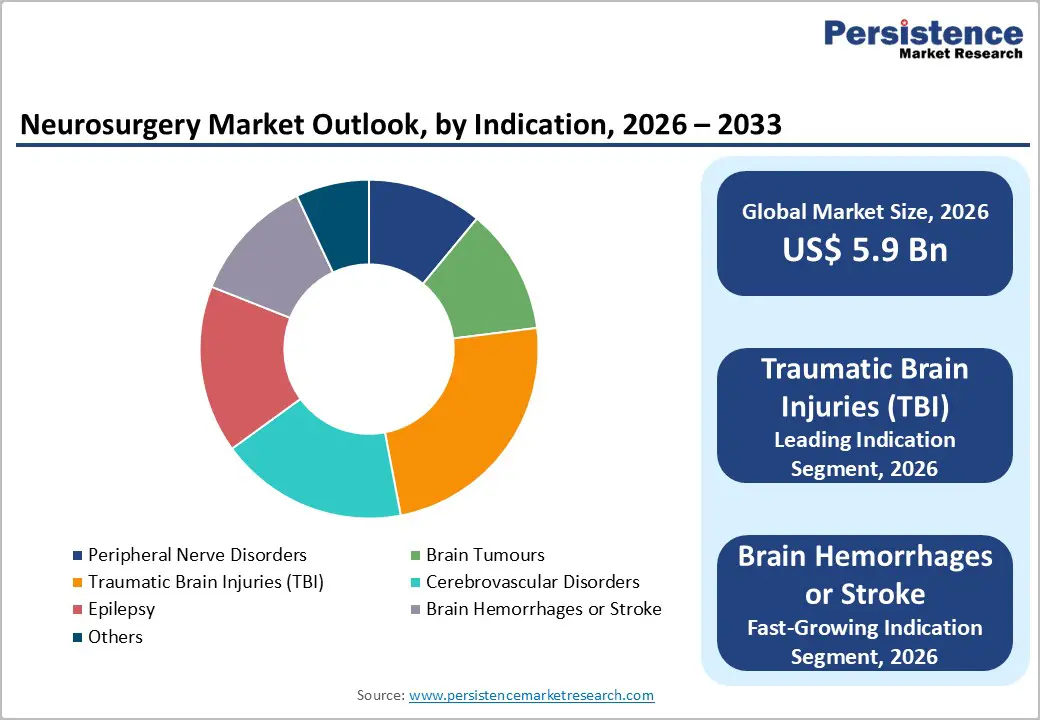

- Fast-Growing Product: Brain Hemorrhages or Stroke is the fastest growing indication during 2026 - 2033, fueled by the WHO-reported 13.7 million new strokes annually, expanding thrombectomy center networks globally, and next-generation neurovascular devices receiving FDA/CE clearances.

- Key Opportunity: Asia Pacific's underserved stroke intervention landscape with China's 3 million annual strokes and thrombectomy adoption still at early stages combined with Healthy China 2030 and Ayushman Bharat infrastructure programs, represents the highest-volume growth opportunity in the neurosurgery device market through 2033.

Market Dynamics

Drivers - Rising Global Incidence of Neurological Disorders and Traumatic Brain Injuries

The escalating global burden of neurological diseases is the most structural driver of the neurosurgery market. The Global Burden of Disease (GBD) Study estimates that neurological disorders collectively accounted for 9 million deaths and over 276 million DALYs (disability-adjusted life years) in 2019. Traumatic brain injury (TBI) alone affects an estimated 69 million people globally each year, according to a landmark meta-analysis published in Neurosurgical Focus. Cerebrovascular disease, including ischemic stroke, affects 13.7 million people annually, according to WHO data.

Each of these conditions generates significant neurosurgical device and instrumentation demand from thrombectomy systems to ICP monitors, creating a large, structurally growing addressable market that compels sustained investment in neurosurgical infrastructure and technology globally.

Technological Advancement in Minimally Invasive Neurosurgery and Radiosurgery

The rapid adoption of minimally invasive neurosurgical techniques and advanced stereotactic radiosurgery is materially expanding the procedural volume and commercial scope of the neurosurgery market. Medtronic's StealthStation neuronavigation system, Stryker's Q Guidance System, and Brainlab's Curve platform are enabling surgeons to perform complex cranial and spinal procedures with sub-millimeter precision. Elekta's Leksell Gamma Knife and Varian's TrueBeam LINAC systems have transformed the treatment of brain metastases, arteriovenous malformations, and trigeminal neuralgia without open surgery.

The American Association of Neurological Surgeons (AANS) reports growing adoption of endoscopic and robotic-assisted procedures among board-certified neurosurgeons globally, reducing patient morbidity, shortening hospital stays, and expanding the eligible surgical population-all factors that increase neurosurgical device utilization volumes.

Restraints - Severe Shortage of Trained Neurosurgeons Globally

A critical structural constraint on the neurosurgery market is the global shortage of trained neurosurgeons, particularly in low- and middle-income countries. The World Federation of Neurosurgical Societies (WFNS) estimates that there is a global deficit of over 23,000 neurosurgeons relative to current population-based needs, with the Sub-Saharan Africa region having fewer than 1 neurosurgeon per 10 million people in many countries. This workforce gap severely limits the deployment and utilization of neurosurgical devices and systems in high-burden regions, leaving a large volume of necessary procedures unperformed annually.

High Capital Investment Required for Advanced Neurosurgical Systems

Advanced neurosurgical platforms, including stereotactic radiosurgery systems, neuronavigation suites, and robotic surgical systems, require substantial upfront capital investment. A Leksell Gamma Knife (Elekta) installation costs approximately US$ 3-5 million, while comprehensive neuronavigation and intraoperative imaging setups can exceed US$ 1-2 million per operating room. These cost thresholds are prohibitive for smaller hospitals and healthcare systems in the Asia Pacific, Latin America, and Africa, limiting technology adoption and constraining procedural growth in high-incidence but under-resourced markets.

Opportunities - Stroke and Brain Hemorrhage Segment: Fastest Growing Indication Driven by Thrombectomy Innovation

Brain Hemorrhages or Stroke represents the fastest growing indication segment in the neurosurgery market, driven by the clinical revolution in mechanical thrombectomy for large vessel occlusion (LVO) ischemic stroke. Penumbra Inc.'s aspiration thrombectomy systems, Stryker's Trevo ProVue stent retriever, and Medtronic's Solitaire device have transformed acute ischemic stroke management, with landmark MR CLEAN, ESCAPE, and SWIFT PRIME trials demonstrating up to 3-fold improvement in functional outcomes versus IV thrombolysis alone.

The WHO reports 13.7 million new strokes annually. As thrombectomy-capable stroke centers expand, particularly in Asia Pacific and Eastern Europe, neurovascular interventional device demand will accelerate significantly through 2033.

Asia Pacific Infrastructure Investment and Neurosurgery Capacity Expansion

Asia Pacific represents the fastest-growing regional neurosurgery market, with government-led healthcare infrastructure investments across China, India, Japan, South Korea, and Southeast Asia creating the conditions for rapid neurosurgical device adoption. China's Healthy China 2030 plan and India's Ayushman Bharat program are funding expansion of tertiary care hospital capacity, including neurosurgery departments and stroke intervention centers.

China alone has approximately 3 million strokes annually according to the Chinese Stroke Association, with thrombectomy adoption still at early stages relative to incidence. Japan's PMDA and South Korea's MFDS have established efficient regulatory pathways for neurosurgical device approvals. Manufacturers with locally adapted products, service networks, and training programs in these markets are positioned to capture substantial incremental revenue through the forecast period.

Category-wise Analysis

Product Insights

The Neuro Interventional Devices segment leads the Neurosurgery market by product category, accounting for approximately 36% of total product revenue in 2025. This leadership is driven by the dramatic clinical adoption of endovascular neurovascular procedures including mechanical thrombectomy, coil embolization for aneurysms, and flow diversion for complex vascular lesions which have supplanted open surgical approaches for many cerebrovascular conditions.

The Society of NeuroInterventional Surgery (SNIS) reports consistent double-digit growth in endovascular procedure volumes across U.S. comprehensive stroke centers. Devices from Penumbra Inc., Medtronic (Solitaire/Pipeline), Stryker (Trevo/Neuroform), and Terumo are globally deployed, supported by strong clinical evidence bases and standardized interventional neurology training pathways that sustain procedural volume growth.

Indication Analysis

The Traumatic Brain Injury (TBI) indication leads the Neurosurgery market, accounting for approximately 24% of indication-based revenue in 2025. TBI drives disproportionate neurosurgical device consumption due to the acuity and complexity of intervention required, including craniotomy, ICP monitoring, ventricular drainage, and decompressive craniectomy, combined with its high global incidence. A meta-analysis published in Neurosurgical Focus estimates 69 million TBI cases annually worldwide, with approximately 5.5 million requiring acute hospital admission and surgical management. Road traffic accidents, the leading cause of TBI globally, are disproportionately prevalent in the Asia Pacific and Africa, creating sustained device demand in these rapidly developing healthcare markets.

End-user Insights

The Hospitals segment leads the Neurosurgery market by end-user, representing approximately 58% of end-user revenue in 2025. Hospitals, particularly Level I and Level II trauma centers, comprehensive stroke centers, and tertiary academic medical centers, are the primary settings for neurosurgical procedures globally due to the complexity and acuity of neurosurgical cases, which require multidisciplinary teams, specialized neuro-ICU facilities, intraoperative imaging, and advanced anesthesia support.

The Joint Commission in the U.S. certifies over 150 Comprehensive Stroke Centers nationally, each requiring the full spectrum of neurovascular interventional equipment. As neurosurgical subspecialization increases globally, hospitals will continue to concentrate procedure volume and device procurement, sustaining their dominant end-user position.

Regional Insights

North America Neurosurgery Market Trends and Insights

North America leads the global Neurosurgery market with approximately 38% of total revenue in 2026, supported by the highest global density of comprehensive stroke centers, advanced neurosurgical training programs accredited by the AANS, and robust FDA 510(k) and PMA regulatory pathways enabling rapid neurosurgical device commercialization. The region's extensive medical device reimbursement infrastructure under Medicare and commercial insurance sustains high procedural volumes for thrombectomy, radiosurgery, and tumor resection.

U.S. Neurosurgery Market Size

The U.S. accounts for approximately 87% of North America's neurosurgery market revenue. The AANS reports over 3,500 board-certified neurosurgeons practicing in the U.S., supported by 150+ Joint Commission-certified comprehensive stroke centers. Medtronic, Stryker, Penumbra, and Integra LifeSciences are headquartered or principally sell in the U.S., concentrating commercial innovation and device revenue.

Europe Neurosurgery Market Trends and Insights

Europe is the second-largest neurosurgery market, supported by national health system funding for neurosurgical procedures and CE-marking regulatory frameworks that allow efficient device commercialization across EU member states. The European Association of Neurosurgical Societies (EANS) promotes training standardization across the continent. Germany, France, and the U.K. lead regional device adoption, driven by high neurovascular procedure volumes and established radiosurgery center networks.

Germany Neurosurgery Market Size

Germany accounts for approximately 23% of European neurosurgery revenue, supported by the country's GKV statutory insurance coverage for neurosurgical procedures and a dense hospital network of over 1,900 hospitals with neurosurgery departments. Brainlab AG headquartered in Munich, and B. Braun Melsungen AG maintain strong domestic commercial positions, and Germany's high neurosurgical procedure volumes make it Europe's largest single-country neurosurgery device market.

U.K. Neurosurgery Market Size

The U.K. represents approximately 17% of European neurosurgery revenue. The NHS England Neurosurgery Network coordinates neurosurgical service provision across specialist centers, and NICE guidelines govern device adoption for intracranial procedures. Elekta's Leksell Gamma Knife units are installed across multiple NHS and private radiosurgery centers, and U.K. neurovascular intervention volumes have grown substantially following national thrombectomy network establishment.

Asia Pacific Neurosurgery Market Trends and Insights

Asia Pacific is the fastest-growing neurosurgery market, expected to register the highest CAGR during 2026 - 2033. China dominates regional demand with approximately 3 million strokes annually (Chinese Stroke Association) and a rapidly expanding network of thrombectomy-capable stroke centers under the Healthy China 2030 initiative. Japan, South Korea, India, and Australia have well-established neurosurgery device markets, while Southeast Asia, India, and Indonesia offer the highest growth potential as tertiary care capacity expands.

India Neurosurgery Market Size

India accounts for approximately 14% of the Asia Pacific's neurosurgery market. India reports over 1.8 million strokes annually (Indian Stroke Association), with thrombectomy adoption expanding through Ayushman Bharat-funded tertiary hospitals. Domestic neurosurgeons number approximately 2,000 nationally (Neurological Society of India), creating significant unmet surgical capacity relative to disease burden.

Competitive Landscape

The neurosurgery market is highly competitive, driven by continuous advancements in minimally invasive procedures, robotic-assisted systems, neuronavigation, and high-precision imaging technologies. Companies focus on improving surgical accuracy, reducing recovery time, and enhancing patient safety through innovative devices and advanced implants. Strong investment in research and development supports the launch of next-generation neurostimulation systems, surgical microscopes, and cranial fixation products.

Key Developments

- In May 2026, the U.S. FDA announced a shortage of neurosurgical patties, sponges, and strip devices used in neurosurgery and microsurgery, stating that the disruption was expected to continue through the remainder of 2026.

- In February 2025, Medtronic plc received approval from the U.S. Food and Drug Administration (FDA) for its BrainSense™ Adaptive Deep Brain Stimulation (aDBS) and BrainSense™ Electrode Identifier (EI).

- In September 2024, Stryker acquired NICO Corporation, a privately-held company that provided a systematic approach to minimally invasive surgery for tumor and intracerebral hemorrhage (ICH) procedures.

Companies Covered in Neurosurgery Market

- B. Braun Melsungen AG

- Medtronic

- DePuy Synthes (Johnson & Johnson Services, Inc)

- Boston Scientific Corporation

- Stryker

- Terumo Corporation

- KARL STORZ GmbH & Co KG

- Integra LifeSciences

- Penumbra Inc

- Adeor Medical AG

- Elekta

- Clarus Medical LLC

- Brainlab AG

Frequently Asked Questions

The global neurosurgery market size is estimated to be valued at US$ 5.9 billion in 2026.

Key drivers include the global neurological disease burden: 1 billion+ people affected by neurological disorders; 69 million TBIs annually (Neurosurgical Focus); 13.7 million strokes per year (WHO) combined with rapid innovation in minimally invasive neurosurgery, mechanical thrombectomy systems, stereotactic radiosurgery, and AI-assisted neuronavigation technologies from Medtronic, Brainlab AG, and Elekta.

North America leads with approximately 38% of the global neurosurgery market revenue in 2025.

Stroke and Brain Hemorrhage the fastest growing indication where thrombectomy expansion in Asia Pacific (China's 3 million annual strokes) and next-generation devices like Medtronic Solitaire X are driving rapid procedural volume growth.

The market is led by Medtronic (neuronavigation, thrombectomy, DBS), Stryker (neurovascular devices, neuro instruments), DePuy Synthes/Johnson & Johnson, and B. Braun Melsungen AG. Specialty leaders include Penumbra Inc.