- Processed Food

- Natural Sweeteners Market

Natural Sweeteners Market Size, Share, and Growth Forecast 2026 - 2033

Natural Sweeteners Market by Product Type (Stevia, Honey, Molasses, Date Palm, Sugar Alcohols, Others), Application (Food and Beverage, Pharmaceuticals, Personal Care and Cosmetics), and Regional Analysis, 2026 - 2033

Natural Sweeteners Market Share and Trends Analysis

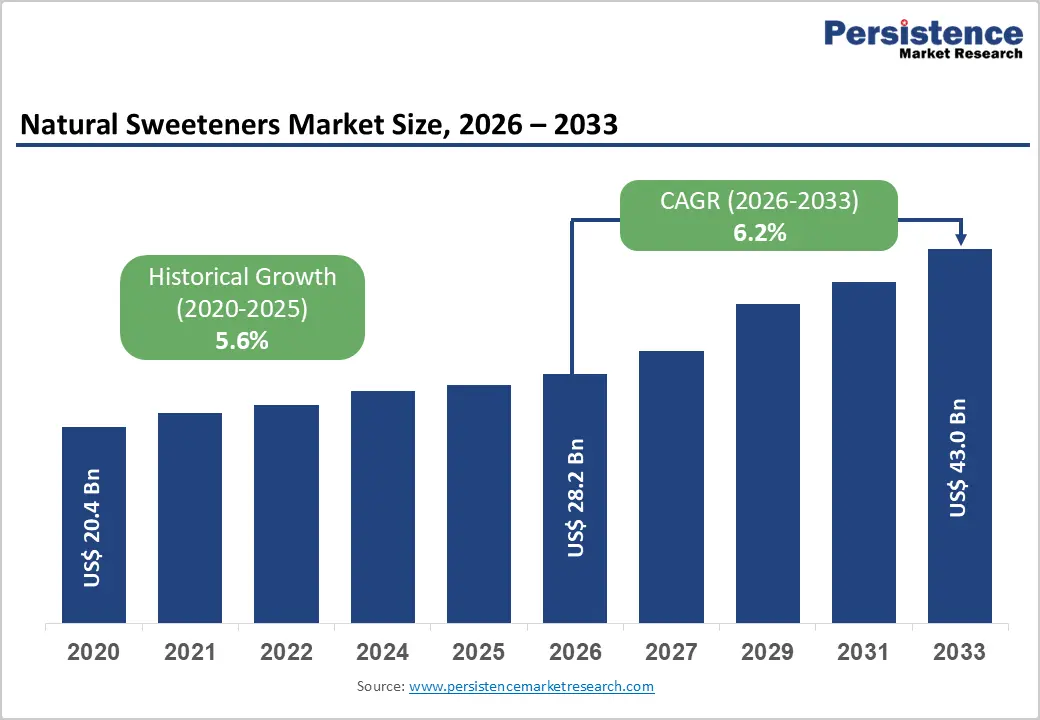

The global natural sweeteners market size is expected to be valued at US$ 28.2 billion in 2026 and projected to reach US$ 43.0 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033. This is driven by the global health crisis surrounding added sugar consumption, accelerating regulatory action to reduce sugar content in processed foods and beverages, and the mass-market proliferation of clean-label consumer products demanding plant-derived, minimally processed sweetening alternatives.

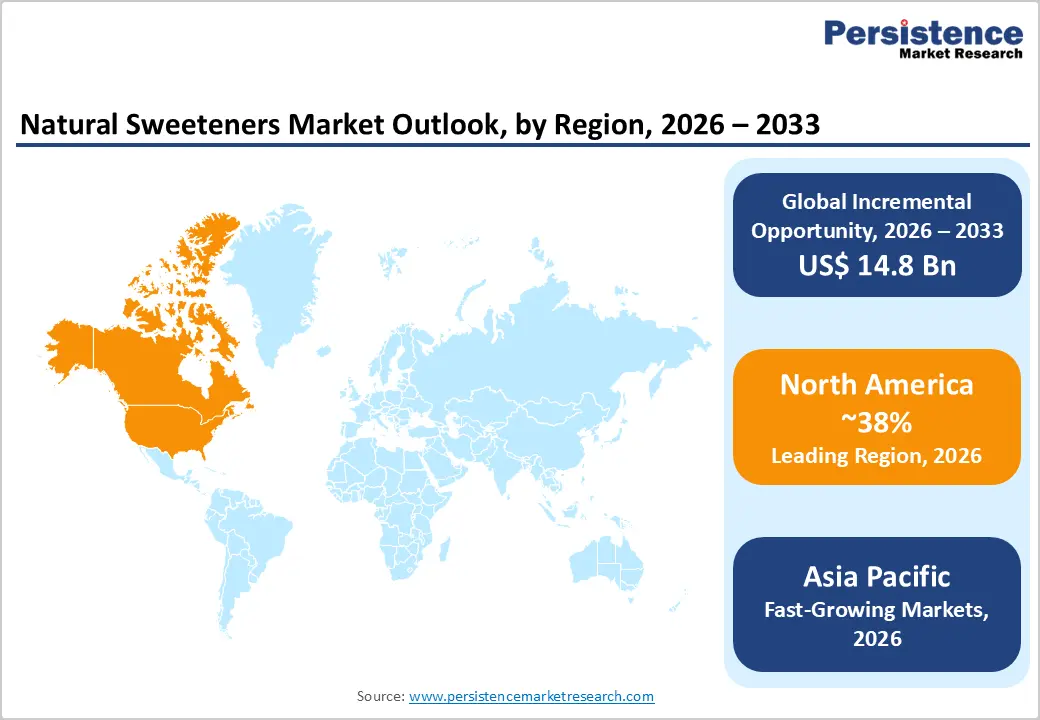

The World Health Organization (WHO) recommends reducing free sugar intake to below 10% of total daily energy intake, a guideline now embedded in national dietary policies across over 100 countries, directly stimulating demand for natural sweetener replacements in food and beverage formulations. The verified historical CAGR of 5.6% between 2020 and 2025 confirms structural consumer and regulatory demand underpinning the forecast trajectory, with North America leading at 38% global share and Asia Pacific emerging as the fastest-growing region.

Key Industry Highlights:

- Leading Region - North America leads the global natural sweeteners market with approximately 38% share in 2025, anchored by a health-conscious consumer base, mature stevia and sugar alcohol regulatory frameworks, and the concentration of leading natural sweetener producers, including Cargill, Ingredion, and Tate & Lyle.

- Fastest Growing Region - Asia Pacific is projected to grow at approximately 8.1% CAGR through 2033, catalyzed by China's Healthy China 2030 sugar reduction initiative, India's growing diabetic population driving demand for low-glycemic alternatives, and expanding SSB tax frameworks across Thailand, Malaysia, and Indonesia.

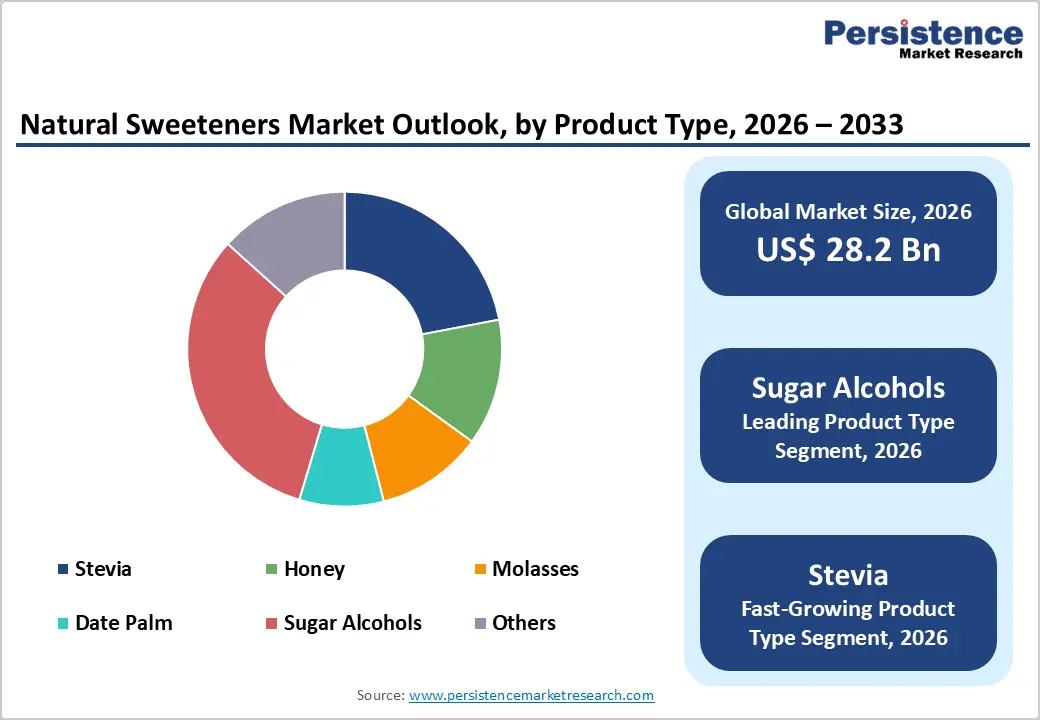

- Dominant Segment - Sugar alcohols hold approximately 32% of the global natural sweeteners market in 2025, sustained by broad application coverage across sugar-free confectionery, oral care, pharmaceutical excipients, and diabetic-friendly food products, supported by FDA and EFSA regulatory approvals across all major grades.

- Fastest Growing Product Segment - Stevia is the fastest growing natural sweetener product type through 2033, driven by next-generation Reb M and Reb D commercialization by Ingredion, Cargill, and SweeGen, which resolves the bitter aftertaste barrier that limited first-generation stevia adoption across mass-market carbonated beverages.

- Key Opportunity - Companies investing in Asia Pacific distribution infrastructure and next-generation fermentation-derived stevia platforms will capture the highest-growth, highest-margin opportunities as China's regulatory environment matures and regional SSB taxes accelerate beverage reformulation through 2033.

Market Dynamics

Drivers - Global Sugar Reduction Policies and Sugar Tax Legislation Mandating Natural Sweetener Reformulation

National sugar reduction policies and sugar-sweetened beverage (SSB) tax legislation represent the most structurally powerful drivers of natural sweetener adoption, compelling food and beverage manufacturers to reformulate with lower-calorie, naturally derived sweetening ingredients to maintain consumer price competitiveness and regulatory compliance. As of 2024, over 50 countries and territories have implemented SSB taxes, including the United Kingdom's Soft Drinks Industry Levy, Mexico's 1-peso-per-liter SSB tax, and levies across South Africa, Saudi Arabia, and multiple EU member states.

The WHO's Global Action Plan for the Prevention and Control of Noncommunicable Diseases (2013-2020, extended to 2030) explicitly targets sugar reduction in the food supply as a priority intervention, prompting major food manufacturers including Nestlé, PepsiCo, and Unilever to accelerate reformulation programs using stevia, sugar alcohols, and honey-based sweetening systems. For natural sweetener producers, this legislative environment creates a durable, policy-backed demand engine that operates independently of consumer trend cycles.

Rising Global Prevalence of Diabetes and Obesity Accelerating Demand for Calorie-Free Natural Sweeteners

The escalating global burden of type 2 diabetes and obesity is directly translating into consumer and clinical demand for sugar alternatives that deliver sweetness without glycemic impact, a value proposition uniquely served by zero-calorie natural options, including stevia and certain sugar alcohols that are both plant-derived and metabolically inert. The International Diabetes Federation (IDF) Diabetes Atlas 2023 estimates that 537 million adults globally were living with diabetes in 2021, projected to reach 783 million by 2045, representing a patient population actively managing carbohydrate intake and seeking diabetic-friendly food products.

The WHO estimates that global obesity rates have tripled since 1975, with over 1 billion adults living with obesity as of 2022. Healthcare professionals' active recommendation of low-glycemic sweetening alternatives in diabetic dietary management is converting this epidemiological trend into structured retail and foodservice demand for natural sweetener-containing products, reinforcing adoption across food, beverage, and pharmaceutical channels.

Restraints - Taste and Organoleptic Limitations of Natural Sweeteners Restricting Application Breadth

Natural sweeteners, particularly stevia and certain sugar alcohols, exhibit sensory limitations, including bitter or licorice-like aftertastes, cooling sensations, and reduced mouthfeel that complicate direct one-to-one sucrose substitution in complex food and beverage formulations.

The Institute of Food Technologists (IFT) has documented consumer acceptance challenges with stevia-sweetened products across carbonated beverage and dairy categories, where the high sweetness intensity and off-note profile of steviol glycosides require careful blending with masking agents. These technical constraints elevate formulation complexity and R&D costs for food manufacturers, limiting natural sweetener penetration in applications where organoleptic parity with sugar is critical.

Opportunities - Stevia Innovation Pipeline Next-Generation Steviol Glycosides Unlocking Mass-Market Beverage Reformulation

Stevia is positioned as the highest-growth product type in the natural sweeteners market and presents actionable near-term opportunities for producers and food ingredient companies that lie in commercializing next-generation, taste-optimized steviol glycosides, particularly Reb M and Reb D, that deliver superior sweetness profiles without the bitter aftertaste that limited first-generation Reb A adoption.

PureCircle (now part of Ingredion), SweeGen Inc., and Cargill have been leading commercial development of bioconversion and fermentation-derived Reb M and Reb D, which achieved GRAS (Generally Recognized as Safe) status from the U.S. FDA and EU Novel Food approval. Coca-Cola and PepsiCo have both launched major reformulation programs incorporating next-generation stevia into flagship carbonated soft drinks in North America and Europe, validating the commercial scalability of this opportunity. Stevia's positioning at the intersection of clean-label, zero-calorie, and plant-derived consumer demand trends makes it the most strategically positioned growth platform in the natural sweeteners market through 2033.

Category-wise Analysis

Product Type Insights

Sugar alcohols command the leading share of approximately 32% of the global natural sweeteners market by product type in 2025, reflecting their broad commercial deployment across sugar-free confectionery, chewing gum, baked goods, oral care products, and pharmaceutical tablet formulations applications where their unique combination of bulk sweetness, reduced caloric value, low glycemic index, and non-cariogenic properties is unmatched by any single-ingredient alternative.

Xylitol, sorbitol, maltitol, and erythritol collectively represent the dominant sugar alcohol grades, with erythritol gaining share due to its near-zero calorie content (0.24 kcal/g) and favorable digestive tolerance profile relative to other polyols. The European Food Safety Authority (EFSA) and U.S. FDA have granted xylitol and erythritol GRAS/approved additive status across a wide range of food applications, underpinning the technical confidence of formulators. Sugar alcohols' dominance is structurally stable, anchored in the scale of the global sugar-free confectionery and oral care markets.

Stevia is the fast-growing product type driven by next-generation Reb M and Reb D steviol glycoside commercialization, mass-market carbonated beverage reformulation programs by Coca-Cola and PepsiCo, and its unmatched combination of zero calories, plant-derived origin, and regulatory approvals across all major markets.

Application Insights

Food and beverage are the dominant application segment with approximately 72% of global natural sweeteners demand in 2025, underpinned by the sector's massive scale the Food and Agriculture Organization (FAO) values global food and beverage industry output in the trillions of dollars annually and the universal relevance of sugar reduction across virtually every food and beverage sub-category from carbonated soft drinks and dairy to confectionery, baked goods, and condiments.

The WHO sugar reduction guidelines, national SSB tax frameworks, and voluntary sugar reduction pledges by major food companies are collectively displacing sucrose across processed food portfolios with natural sweetener alternatives. Tate & Lyle, Cargill, and Ingredion are the primary ingredient suppliers enabling food and beverage brand owners to achieve sugar reduction targets while maintaining consumer-acceptable taste profiles.

The fastest growing application is pharmaceuticals, driven by the expanding use of natural sweeteners in oral solid dosage forms, liquid syrups, and nutraceutical preparations, where the combination of diabetic-patient-safe sweetness, clean-label positioning, and regulatory compliance across global pharmacopoeia requirements makes sugar alcohols and stevia the preferred excipient sweetening agents.

Regional Insights

North America Natural Sweeteners Market Trends and Insights

North America leads the global natural sweeteners market with approximately 38% share in 2025, driven by a highly health-conscious consumer base, the world's largest market for sugar-free and reduced-sugar food and beverage products, a mature stevia regulatory environment under U.S. FDA GRAS approvals, and the concentration of major natural sweetener producers and innovators including Cargill, Ingredion, and Tate & Lyle. SSB taxes in U.S. cities and the clean-label movement sustain above-average adoption rates.

U.S. Natural Sweeteners Market Size

The United States accounts for approximately 80% of North America's natural sweeteners market in 2025, anchored by the world's largest stevia ingredient market, a US$ 25 billion+ sugar-free confectionery sector, and extensive xylitol and erythritol usage in oral care and keto-diet aligned food products. PureCircle and SweeGen lead next-generation stevia innovation from U.S. operations. Growth through 2033 is forecast as steady and above the global average.

Europe Natural Sweeteners Market Trends and Insights

Europe holds approximately 23% of the global natural sweeteners market in 2025, shaped by EU sugar reduction policy frameworks, Novel Food Regulation (EU) 2015/2283 governing stevia approvals, and strong consumer demand for clean-label, organic-certified natural sweeteners across Germany, France, and the U.K. SSB levies in the U.K., France, and Belgium are accelerating sugar reduction reformulation programs across the European food and beverage industry.

Germany Natural Sweeteners Market Size

Germany represents approximately 22% of Europe's natural sweeteners market in 2025, driven by its large functional food and beverage market, strong consumer preference for natural ingredients, and a well-developed organic food retail sector where natural sweetener adoption is above the European average. Germany's food industry anchored in confectionery, bakery, and dairy generates sustained sugar alcohol demand. Growth through 2033 is forecast to be steady and above the European average.

U.K. Natural Sweeteners Market Size

The U.K. holds approximately 18% of Europe's natural sweeteners market in 2025, directly shaped by the Soft Drinks Industry Levy (SDIL), which has driven extensive natural sweetener reformulation across British beverage brands. The U.K.'s National Food Strategy further reinforces sugar reduction in processed foods. Stevia and sugar alcohol adoption rates are among the highest in Europe, and growth is expected to remain robust through 2033.

Asia Pacific Natural Sweeteners Market Trends and Insights

Asia Pacific is the fastest-growing natural sweeteners region, forecast to expand at approximately 8.1% CAGR through 2033, driven by China's Healthy China 2030 initiative reducing sugar consumption, India's growing stevia adoption under FSSAI standards, and the rapid expansion of health-positioned food and beverage product portfolios across Japan, South Korea, and Southeast Asia. China is also the world's leading stevia leaf production hub, supplying the majority of global steviol glycoside extract volumes. The region holds approximately 26% of the global market in 2025.

India Natural Sweeteners Market Size

India accounts for approximately 13% of Asia Pacific's natural sweeteners market in 2025, driven by a diabetic population of over 100 million (the world's second largest per the IDF Diabetes Atlas 2023), growing demand for diabetic-friendly food products, and the FSSAI's progressive expansion of stevia usage approvals. India is also a significant honey producer and consumer. Growth through 2033 is forecast to accelerate as health-positioning in food and beverage premiumizes rapidly.

Competitive Landscape

The natural sweeteners market is highly competitive, driven by increasing demand for sugar alternatives and clean-label ingredients. Competition is shaped by continuous product innovation, with companies focusing on plant-based and low-calorie formulations to meet health-conscious consumer preferences. Strategic expansion in food, beverage, and nutraceutical applications is intensifying rivalry among players. Market participants are investing in advanced extraction technologies, sustainable sourcing of raw materials, and improved taste profiles to gain differentiation.

Pricing pressure and regulatory compliance also influence competition dynamics. Additionally, rising demand for natural sugar substitutes in emerging economies is encouraging new entrants, further increasing fragmentation and competitive intensity across the global market.

Key Developments

- In July 2025, Layn Natural Ingredients introduced its new plant-based sweetener SteviUp M2 (Reb M2) for food and beverage applications. The ingredient was developed using enzyme-based bioconversion of steviol glycosides derived from Stevia rebaudiana, enabling a clean-label, non-GMO solution with improved taste performance.

- In November 2025, the US sugar and sweeteners market witnessed a shift toward clean-label, natural, and plant-based innovation, as consumers increasingly preferred sugar reduction while still seeking natural taste experiences. Product development focused on alternative sweeteners such as stevia, monk fruit, allulose, and erythritol, often used in combination to improve taste and functionality.

Natural Sweeteners Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 20.4 billion |

| Current Market Value (2026) | US$ 28.2 billion |

| Projected Market Value (2033) | US$ 43.0 billion |

| CAGR (2026 - 2033) | 6.2% |

| Leading Region | North America, 38% market share (2025) |

| Dominant Product Type | Sugar Alcohols, 32% share (2025) |

| Top-Ranking Application | Food and Beverage, 62% share (2025) |

| Incremental Opportunity | US$ 14.8 billion (Absolute Dollar Opportunity) |

Companies Covered in Natural Sweeteners Market

- Cargill, Inc.

- Tate & Lyle PLC

- Ingredion Incorporated

- PureCircle (a part of Ingredion)

- GLG Life Tech Corporation

- NOW Foods

- Whole Earth Brands

- NutraEx Food Inc.

- SweeGen Inc.

- HYET Sweet

Frequently Asked Questions

The global Natural Sweeteners market is valued at US$ 28.2 billion in 2026 and is projected to grow at a CAGR of 6.2% to reach US$ 43.0 billion by 2033.

The two primary demand drivers are: first, the proliferation of national sugar reduction policies and SSB tax legislation with over 50 countries having implemented such measures by 2024 which compels food and beverage manufacturers to reformulate with natural sweetener alternatives to maintain consumer price competitiveness and regulatory compliance.

North America leads the global Natural Sweeteners market with approximately 38% of market share in 2025.

The most strategically compelling opportunities are: the Asia Pacific market expansion, where the Asian Development Bank projects 3.5 billion middle-class consumers by 2030.

The leading companies in the global Natural Sweeteners market include Cargill Inc., Tate & Lyle PLC, Ingredion Incorporated (including its PureCircle division), GLG Life Tech Corporation, Whole Earth Brands, SweeGen Inc., etc.