- Processed Food

- Europe Gluten-free Food Market

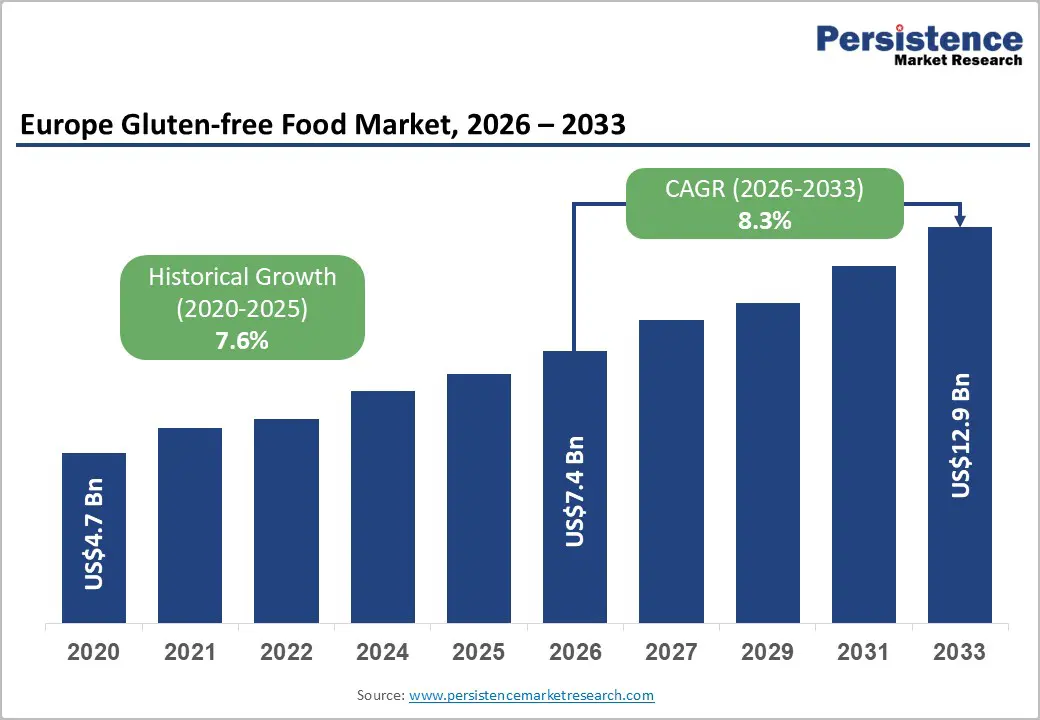

Europe Gluten-free Food Market Size, Share, and Growth Forecast 2026 - 2033

Europe Gluten-free Food Market by Product Type (Bakery Products, Meats/Meat Substitutes, Dairy/Dairy Substitutes), Nature (Organic, Conventional), Distribution Channel (Supermarkets/Hypermarkets), and Country Analysis, 2026 - 2033

Europe Gluten-free Food Market Size and Trends Analysis

The Europe gluten-free food market size is likely to be valued at US$7.4 billion in 2026 and is expected to reach US$12.9 billion by 2033, growing at a CAGR of 8.3% during the forecast period from 2026 to 2033, driven by rising prevalence of gluten intolerance and celiac disease as well as surging consumer preference for clean-label products. Increasing product development across gluten-free bakery, snacks, and ready-to-eat categories is further boosting growth.

Key Industry Highlights:

- Leading Country: Germany, with about 21.3% share in 2026, owing to rising awareness of coeliac disease and high penetration of private-label products across supermarket chains.

- Fast-growing Country: Italy, backed by government-backed subsidies for coeliac patients and high diagnosed population.

- Latest Product: In September 2025, Genius Foods launched its Naturally Genius range, co-created with TV personality, singer, and cookbook author Megan McKenna. The six-strong lineup of artisan and sliced loaves marks a transformative moment for gluten-free consumers.

- Leading Product Type: Bakery products, approximately 46.5% share in 2026, as bread and baked goods are daily staples that require immediate gluten-free substitutes after diagnosis.

- Dominant Nature: Conventional, nearly 87.3% in 2026, as it provides low prices and wide availability.

DRO Analysis

Driver - Rising Prevalence and Diagnosis Rates of Celiac Disease

Celiac disease has a particularly strong foothold in Europe. Prevalence in the continent stands at around 0.8%, but actual diagnosis is catching up fast. New celiac diagnoses have grown at approximately 7.5% per year over recent decades across the industrialized West. In the EU specifically, newly confirmed celiac cases rose 12% annually between 2020 and 2024, mainly due to better serological screening and endoscopic protocols in primary care.

Finland's national registry also recorded a 30% jump in adult celiac diagnoses since 2021, pushed by public health campaigns. What makes this significant for the field of gluten-free food is the nature of the demand it creates. Medically diagnosed consumers represent a non-discretionary segment whose buying behavior is consistent and price-insensitive compared to lifestyle adopters. As more people receive confirmed diagnoses, they become long-term and committed buyers of certified gluten-free products.

Surging Awareness of Non-Celiac Gluten Sensitivity

Non-Celiac Gluten Sensitivity (NCGS) is gradually broadening the gluten-free consumer base far beyond the medically diagnosed. NCGS is estimated to affect around 6% of Europe's population, and as awareness rises, healthcare professionals are recommending gluten-free diets for this group too. In 2024, NCGS prevalence in Europe reached 12%, with 40% of affected individuals following a gluten-free diet despite lacking a formal celiac diagnosis.

Research from Portugal in 2024 further showed that gluten-free product positioning complies with broad clean-eating and gut-health trends, appealing well beyond those with formal diagnoses. Unlike celiac patients, NCGS consumers make dietary choices voluntarily, which makes them more responsive to product quality, taste, and branding. This segment is what's pushing gluten-free from a medical necessity category into a mainstream food choice.

Restraint - Strict Regulatory Framework to Put Pressure on Small Producers

Getting a product to market with a legitimate gluten-free claim in Europe is far more demanding than in most other regions. Under EU Implementing Regulation No 828/2014, rules governing gluten-free labeling fall under the broad food information framework of Regulation (EU) No 1169/2011, requiring manufacturers to verify and declare gluten content across all ingredients. Products labeled gluten-free must contain less than 20 mg/kg of gluten in the finished product, a threshold applied universally across all food items.

Beyond labeling, earning the trusted crossed-grain symbol requires passing the Association of European Coeliac Societies (AOECS)-standard audits conducted by approved certification bodies such as Eurofins Food Control Services, which assess full production compliance. The European Commission itself acknowledges that removing gluten from grain-based products involves considerable technical difficulties and economic constraints. For small and mid-sized manufacturers, the cost of repeated lab testing, third-party audits, and facility segregation creates a barrier to entry. It is predicted to hinder product launches and limit competition in the category.

Opportunity - Emergence of Alternative Flours and Binding Agents

Taste and texture have long been the weak points of gluten-free products. This scenario is now changing, owing to a new wave of ingredient development. Manufacturers are slowly moving away from basic rice flour and potato starch blends toward more functional alternatives. According to Eurostat, the EU imported over 420,000 metric tons of cassava products in 2023, and native cassava starch has become a key ingredient in Europe's gluten-free food market due to its high binding capacity and freeze-thaw stability.

A 2024 trial by the German Institute of Food Technologies found that cassava flour improved water-holding capacity in plant-based food applications by 18% compared to rice flour. On the biotech side, Prozymi Biolabs launched enzyme technology in February 2025 that degrades gluten peptides in wheat flour to below the EU's 20 ppm threshold. Spain-based start-ups are also developing coeliac-safe wheat through enzymatic treatment. These developments are making it possible to create gluten-free products that compete on taste and texture, not just safety.

Brands to Strengthen Premium Positioning to Attract Consumers

The fastest-growing gluten-free buyers in Europe are not celiac patients, but they are wellness-oriented consumers who choose to avoid gluten. This group, which far exceeds the diagnosed population, views gluten avoidance as a wellness choice rather than a medical necessity. Leading domestic supermarket chains such as Carrefour, Tesco, REWE, Waitrose, and Sainsbury's have extended dedicated free-from aisles and launched gluten-free private-label portfolios. Brands are positioning accordingly. In Germany, awareness of the Nutri-Score nutritional labeling system rose from 44% in 2021 to 88% in 2024. It shows the rising appetite for transparent and health-forward food choices.

Netherlands-based Revyve also launched a yeast-based egg replacer in September 2024, targeting clean-label formulations for vegan and allergen-sensitive consumers. It is a sign that the gluten-free space is merging with broad premium health trends. For brands that position gluten-free as part of a clean and functional diet, there is clear room to command high price points and build lasting loyalty.

Category-wise Analysis

Product Type Insights

Bakery products are predicted to lead with a share of approximately 46.5% in 2026 in Europe gluten-free food market, as gluten affects the structure of bread, cakes, and biscuits. When people are diagnosed with coeliac disease, the first foods they must replace are daily staples such as bread and breakfast items. This creates immediate and repeat demand. According to the European Food Safety Authority, strict gluten limits apply to staple foods, pushing manufacturers to invest heavily in gluten-free bakery reformulation.

Meats/Meat substitutes are estimated to be the fastest growing segment in the forecast period, as gluten is widely used as a filler or binder in processed meat. Consumers with gluten intolerance are now actively checking labels on sausages, nuggets, and ready meals. The U.K. Food Standards Agency has repeatedly issued guidance on allergen labeling, which has increased awareness around hidden gluten in processed meats. Companies are also reformulating their products using pea protein, soy, and fava beans to attract consumers preferring plant-based meat substitutes.

Nature Insights

The conventional segment is anticipated to dominate with a share of nearly 87.3% in 2026, as they are affordable and widely available. Gluten-free foods already cost more due to specialized processing and certification. Adding organic certification further increases costs. This makes conventional options the default choice for most consumers. Supply chain limitations also play a key role. Gluten-free ingredients such as rice flour, corn starch, and potato starch are easier to source in conventional form. Organic versions require strict farming and certification standards under EU regulations such as those enforced by the European Commission, which limits large-scale production.

The organic segment is expected to remain in the second position, as consumers are shifting from free-from to clean-label plus free-from. They are no longer satisfied with just removing gluten. They also want fewer additives and more natural sourcing. The European Commission noted that organic food consumption in Europe has been rising steadily, especially in countries such as France and Denmark. Parents and health-focused consumers are bolstering this shift. Several gluten-free buyers are managing long-term conditions, including coeliac disease. Hence, they prefer organic products to avoid pesticide residues and artificial ingredients.

Country Insights

Germany Gluten-free Food Market Trends

Germany is anticipated to dominate in 2026, with a share of nearly 21.3%, owing to a large patient base, strict food safety standards, and consumer willingness to pay more for quality. The country is home to an estimated 800,000 to 900,000 celiac patients. Its regulatory framework is strengthened by the German Celiac Society's certification program, which extended its approved product portfolio by 18% since 2024. Diagnosed patients, however, are not the primary buyers.

Only 3% of the country’s population purchased gluten-free foods in 2023, indicating that lifestyle preferences, rather than medical necessity, are augmenting much of the market growth. This points to a broad consumer base of wellness-driven shoppers.

Consumer trust is also rising steadily. Awareness of the Nutri-Score nutritional labeling system rose significantly, from 44% in 2021 to 88% in 2024, reflecting increasing consumer interest in healthy food choices. Retailers and manufacturers have responded accordingly. Demand is concentrated in urban and high-income regions such as Bavaria and Baden-Württemberg, where consumers have increased purchasing power and access to premium products. Germany is also the largest food and beverage market in Europe, and rising health concerns along with an aging population are pushing demand for specialty ingredients in functional foods.

Italy Gluten-free Food Market Trends

In 2026, Italy will likely showcase the fastest-growth and account for approximately 14.8% of share in Europe gluten-free food market. The country’s growth is not accidental but the result of deliberate government policy and one of Europe's highest celiac diagnosis rates. The country has one of the highest diagnosed rates of celiac disease in Europe, propelled by effective screening programs and well-established public health initiatives. The most distinctive factor is the government's financial support system.

Italy is renowned among the global celiac community for its monthly allowance system, known as the ‘bonus celiachia.’ It was established by the National Health Service (Servizio Sanitario Nazionale) since the 1980s.

Diagnosed celiacs receive vouchers to buy specifically produced gluten-free foods worth up to €140 (US$163.04) per month. The Italian Celiac Association and the government have also worked to ensure that gluten-free meals are available in schools, hospitals, and other public establishments. Citizens over the age of 10 with celiac disease also receive additional leave time to shop and prepare gluten-free food. In January 2024, the Italian Ministry of Health launched a new national screening program for children aged 1 to 17, screening for both type 1 diabetes and celiac disease every couple of years, with a budget of €3.85 million authorized for each of 2024 and 2025.

France Gluten-free Food Market Trends

A share of nearly 13.2% is expected to be recorded by France in 2026 in Europe gluten-free food market. Growth is being propelled by shifting consumer values, especially around clean eating and digestive health. Modern consumers are constantly scrutinizing ingredient labels. Brand transparency and ingredient simplicity are boosting purchasing decisions, and retailers are prominently highlighting allergen-free items on dedicated shelves. This clean-label preference is drawing in consumers who have no medical diagnosis but are choosing gluten-free as part of a broad wellness lifestyle.

The food-service and café sector is also playing a key role. Gluten-free cookies, crackers, chips, breads, and ready meals are gaining traction among busy consumers. This trend is supported by expanding café menus and modern foodservice formats. Manufacturers are responding as well. Several companies have started innovating with alternative grains such as quinoa, millet, sorghum, and rice to improve product texture.

Spain Gluten-free Food Market Trends

Spain is predicted to account for a share of nearly 11.6% in 2026 and showcase steady growth. The Spanish Federation of Coeliac Associations (FACE) has played a central role in building consumer trust. FACE launched the Controlado por FACE quality label, which certifies that products contain less than 10 ppm of gluten, stricter than the EU's 20 ppm threshold, and these products are available in hypermarkets, supermarkets, and pharmacies. The country is also becoming a manufacturing hub for Europe.

For example, Dr. Schär invested €6.8 million to add a new production line at its Alagón, Zaragoza facility. It produces gluten-free pastries and confectionery, with 85% of the plant's output destined for export to markets across Europe.

U.K. Gluten-free Food Market Trends

The U.K. is estimated to hold a share of approximately 7.4% in 2026 in Europe gluten-free food market, backed by increasing consumer awareness. According to Coeliac U.K., 1 in 100 people has coeliac disease in the country, and this is a key structural driver of gluten-free demand. The retail landscape is highly developed. Supermarkets play an important role in product distribution, supported by private-label expansion and dedicated free-from sections. Superior healthcare support systems, including NHS screening programs, are improving diagnosis rates and influencing demand.

Policy is also catching up with market requirements. For instance, Wales introduced the U.K.'s first gluten-free subsidy card in autumn 2025. It was an initiative designed to improve the affordability of gluten-free food and reduce the medicalization associated with accessing it.

The Netherlands Gluten-free Food Market Trends

The Netherlands is anticipated to be one of the key countries in Europe gluten-free food market, with a share of approximately 6.9% in 2026. Growth is attributed to its role as a prominent food technology hub. The standout example of this is ingredient development. In September 2024, for instance, Revyve B.V., a food technology firm based in the Netherlands, introduced a next-generation gluten-free ingredient line focused on improving the texture and mouthfeel of gluten-free products.

Condiment and sauce sales in the country are further showcasing rising pantry-level substitution beyond main meals. It suggests that gluten-free purchasing behavior is becoming embedded in everyday cooking rather than being limited to specialty products.

Competitive Landscape

The Europe gluten-free food market is moderately consolidated with a handful of specialist gluten-free brands controlling premium segments. Multinational food companies and retailer private labels are intensifying competition across mainstream categories. A defining feature is the dominance of specialist players such as Dr. Schär, which has built strong brand loyalty through certified gluten-free production, extensive product portfolios, and collaborations with healthcare professionals.

Competition has shifted beyond simply providing gluten-free alternatives. Companies are now focusing on improving taste, texture, nutritional value, and clean-label formulations using ingredients such as chickpea flour, sorghum, teff, and pulse-based proteins. Product quality and contamination-free manufacturing have become prominent differentiators because consumer trust can be easily damaged by labeling or safety issues.

Key Industry Developments:

- In May 2026, the European Parliament hosted its first-ever dedicated debate on safe gluten-free catering, convened by AOECS under the auspices of MEP Peter Agius. Policymakers, industry representatives, and patient organizations came together to address food accessibility, awareness, and safe dining for people with coeliac disease across Europe.

- In May 2026, the U.K.-based FREEE extended its popular breakfast portfolio with the launch of its first-ever gluten-free muesli range. The products are high in fiber, made without the top 14 allergens, Coeliac U.K. certified, and free from artificial colors, flavors, and preservatives.

- In June 2025, the U.K.-based gluten-free producer Juvela, a subsidiary of Tooru plc, launched a disruptive new retail brand called OAF. Unlike most gluten-free brands that rely on rice flour, OAF products are made using specially formulated wheat starch with the gluten removed, making the taste and texture as close to conventional bread as possible.

Companies Covered in Europe Gluten-free Food Market

- Dr. Schär AG/SPA

- General Mills Inc.

- Warburtons Ltd.

- Genius Foods Ltd.

- Hain Celestial Group

- Conagra Brands Inc.

- Nestlé SA

- Amy’s Kitchen Inc.

- Bob’s Red Mill Natural Foods

- Barilla Group

- Kraft Heinz Company

- Kellogg Company

- Hero Group

- Dawn Foods

- London Food Corporation

- Golden West Specialty Foods

- Schärbäckerei GmbH

- Grupo Airos

- Freee Foods Ltd

- Beneo GmbH

- Others

Frequently Asked Questions

The Europe gluten-free food market is projected to be valued at US$7.4 billion in 2026.

The Europe gluten-free food market is expected to reach US$12.9 billion by 2033.

Key market trends include rising organic gluten-free launches and expansion of plant-based gluten-free products.

Bakery products are expected to be the leading product type with a share of nearly 46.5% in 2026, as prominent retailers prioritize gluten-free bakery shelves.

The Europe gluten-free food market is expected to grow at a CAGR of 8.3% from 2026 to 2033.

Dr. Schär AG/SPA, General Mills Inc., Warburtons Ltd., and Genius Foods Ltd. are a few key market players.