- Animal Feed & Additives

- Mycotoxin Binders Market

Mycotoxin Binders Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Mycotoxin Binders Market by Product Type (Clay-based Binders, Activated Carbon, Biological Binders, Polysaccharide-based Binders, Polymer-based Binders, and Others), Livestock (Poultry, Swine, Ruminants, Aquaculture, Equine, and Others), Application (Animal Feed Additives, Pet Food Additives, Food & Beverages, and Others) Distribution Channel (Feed Manufacturers, Veterinary & Livestock Service Providers, Premix & Feed Additive Companies, and Online Retail), and Regional Analysis from 2026 - 2033

Mycotoxin Binders Market Share and Trend Analysis

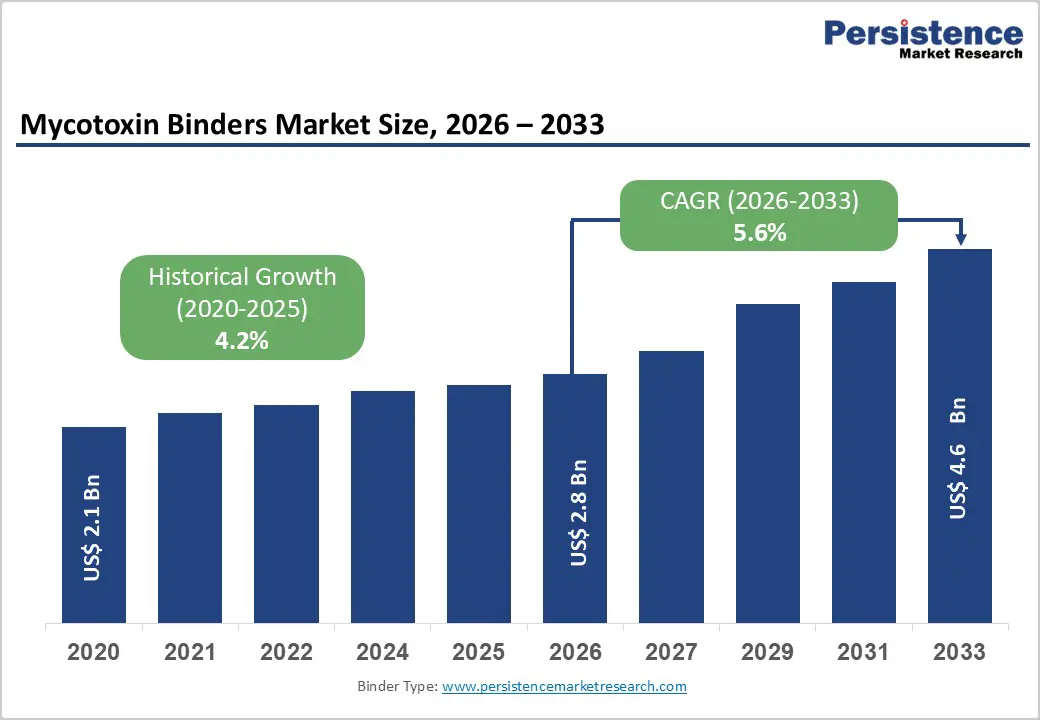

The global mycotoxin binders market size is estimated to grow from US$ 2.8 Bn in 2026 to US$ 4.6 Bn by 2033. The market is projected to record a CAGR of 5.6% during the forecast period from 2026 to 2033. Rising concerns over feed contamination and its direct impact on livestock productivity are significantly driving the adoption of mycotoxin binders across global feed systems. Producers are increasingly incorporating these solutions to minimize toxin absorption, protect animal health, and maintain consistent performance levels.

Mycotoxin binders play a critical role in improving feed safety by reducing the bioavailability of harmful compounds such as aflatoxins and fumonisins. With increasing awareness regarding economic losses linked to contaminated feed, manufacturers are prioritizing preventive strategies within feed formulations. Additionally, advancements in binder technologies are enhancing multi-toxin adsorption capabilities and improving compatibility with diverse feed compositions. The expansion of commercial livestock farming, along with stricter regulatory oversight on feed quality, continues to reinforce the importance of mycotoxin binders in modern animal nutrition.

Key Industry Highlights:

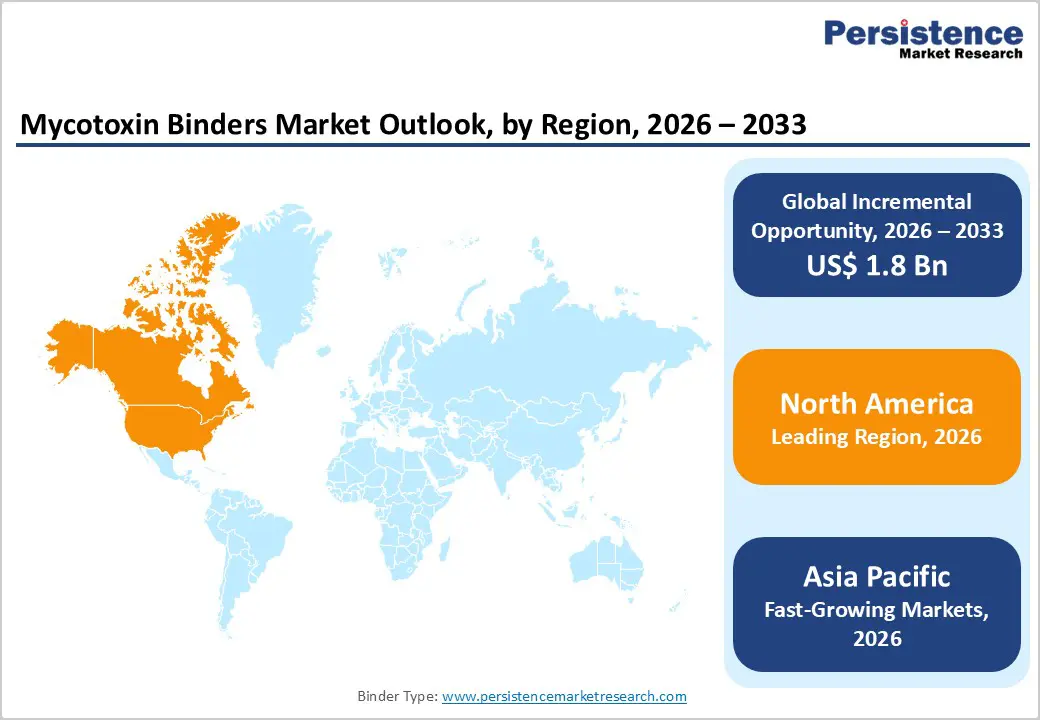

- Leading Region: North America accounts for 46.7% share, supported by a well-established livestock industry, stringent feed safety regulations, and high adoption of advanced feed additives.

- Fastest-Growing Region: Asia Pacific is experiencing strong growth, driven by expanding livestock production, rising feed demand, and increasing awareness regarding contamination risks in emerging economies.

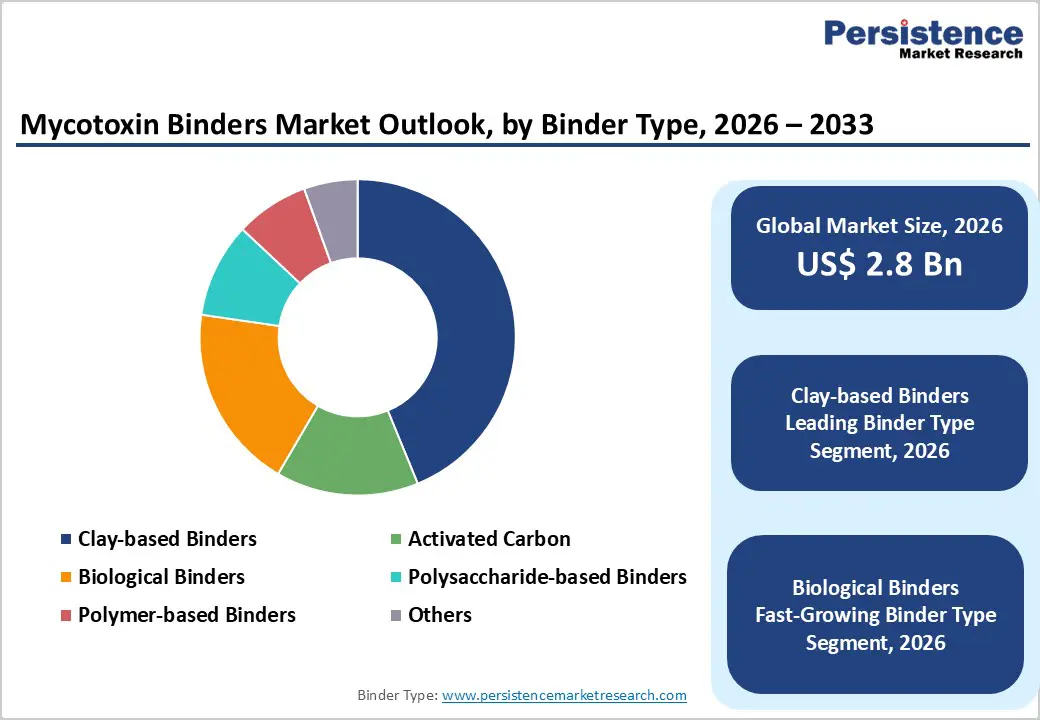

- Leading Binder Type Segment: Clay-based binders dominate due to their high adsorption efficiency, cost-effectiveness, and widespread usage across large-scale feed operations.

- Fastest-Growing Binder Type Segment: Biological binders are gaining momentum as demand increases for multi-functional and sustainable toxin management solutions.

- Leading Application Segment: Animal feed additives remain the primary segment, supported by extensive use in improving feed safety, animal health, and overall productivity.

- Fast-Growing Application Segment: Pet food additives are steadily expanding as manufacturers focus on enhancing safety standards and incorporating preventive nutrition solutions.

| Key Insights | Details |

|---|---|

|

Mycotoxin Binders Market Size (2026E) |

US$ 2.8 Bn |

|

Market Value Forecast (2033F) |

US$ 4.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.2 % |

Market Dynamics

Driver - Increasing Incidence of Mycotoxin Contamination and Heightened Focus on Feed Safety

A primary force accelerating adoption is the rising prevalence of mycotoxin contamination in feed ingredients such as corn, wheat, and barley, driven by changing climatic conditions including high humidity and temperature fluctuations. These toxins, produced by fungal species, significantly impact animal health, leading to reduced feed intake, lower productivity, and compromised immunity. As a result, livestock producers are increasingly prioritizing preventive solutions to safeguard performance and minimize economic losses.

Regulatory authorities across major markets are also enforcing strict limits on permissible mycotoxin levels in animal feed, compelling feed manufacturers to integrate effective mitigation strategies. Mycotoxin binders have emerged as a practical and scalable solution due to their ability to adsorb toxins within the gastrointestinal tract and prevent systemic absorption. Additionally, the intensification of commercial livestock farming, particularly in poultry and swine sectors, has amplified the need for consistent feed quality. Growing awareness among farmers regarding the long-term benefits of toxin management further supports adoption. Continuous advancements in binder formulations, including multi-mycotoxin targeting capabilities, are reinforcing their role as an essential component of modern feed safety protocols.

Restraints - Variability in Binding Efficiency and Challenges in Multi-Mycotoxin Management

Despite widespread utilization, limitations in efficacy across diverse toxin types remain a critical challenge. Different mycotoxins possess distinct chemical structures, making it difficult for a single binder to effectively adsorb all variants. For instance, while clay-based binders demonstrate strong affinity toward aflatoxins, their effectiveness against toxins such as fumonisins or zearalenone is comparatively limited. This variability often necessitates the use of combination products, increasing formulation complexity for feed manufacturers.

Another constraint lies in the potential interaction of binders with essential nutrients, where non-specific adsorption may reduce the bioavailability of vitamins and minerals. This creates formulation trade-offs that must be carefully managed to avoid compromising animal nutrition. Additionally, inconsistencies in raw material quality, particularly in naturally derived binders, can lead to performance variability across batches. Regulatory discrepancies across regions regarding approved additives and inclusion rates further complicate market expansion strategies. Cost sensitivity in developing markets also restricts adoption of advanced or premium solutions. Collectively, these technical and economic barriers limit the uniform effectiveness and scalability of mycotoxin binder applications across diverse livestock systems.

Opportunity - Advancements in Multi-Functional Binders and Expansion in Emerging Livestock Markets

The market presents strong growth potential through the development of next-generation binder solutions designed to address multiple mycotoxins simultaneously while enhancing overall feed efficiency. Innovations combining adsorption, biotransformation, and immune-modulating properties are gaining traction, offering a more holistic approach to toxin mitigation. These advanced formulations not only neutralize contaminants but also contribute to improved gut health and nutrient utilization, creating added value for livestock producers.

Emerging markets across Asia, Latin America, and parts of Africa are also creating significant expansion opportunities, supported by rapid growth in animal protein consumption and increasing industrialization of livestock farming. As feed production scales up in these regions, the need for consistent quality control mechanisms is becoming more pronounced. Rising awareness regarding the economic impact of contaminated feed is encouraging adoption of preventive additives. Furthermore, integration of digital feed management systems and precision nutrition practices is enabling more targeted use of binders, improving efficiency. Strategic collaborations between feed manufacturers and additive producers are also accelerating product penetration. These factors collectively position the market for sustained innovation and long-term growth.

Category-wise Analysis

By Binder Type Insights

Clay-based binders are expected to lead the global mycotoxin binders market in 2026, capturing 43.8% of total revenue. Their dominance is primarily attributed to superior toxin adsorption capacity, particularly against aflatoxins, along with cost efficiency and widespread availability. These binders, including bentonite and aluminosilicates, are extensively incorporated into livestock feed due to their proven efficacy and ease of integration. Increasing regulatory focus on feed safety and contamination control has further strengthened their adoption. While advanced biological and polymer-based solutions are gaining momentum, clay-based variants continue to offer a reliable and scalable solution, especially in price-sensitive markets. Their stability under diverse feed processing conditions and compatibility across livestock categories further reinforce their leading position in the market.

By Application Insights

Animal feed additives are projected to dominate the market, accounting for 72.6% of total revenue in 2026. This segment’s leadership is driven by the essential role mycotoxin binders play in mitigating toxin exposure in livestock, thereby improving productivity, immunity, and overall animal performance. With rising incidences of mycotoxin contamination in feed grains, producers are increasingly incorporating binders as a preventive measure. The growing scale of commercial livestock farming and heightened awareness regarding feed quality have accelerated adoption globally. In comparison, applications in pet food and human food systems remain relatively niche due to stricter regulatory frameworks and limited direct usage. As feed efficiency and animal health become key priorities, the demand for effective toxin management solutions continues to strengthen this segment’s market position.

By Distribution Channel Insights

Feed manufacturers are anticipated to hold the largest share, contributing 41.3% of market revenue in 2026. Their leading position is supported by direct incorporation of mycotoxin binders during feed formulation, enabling large-scale and consistent usage. These manufacturers operate at the core of the value chain, supplying compound feed to poultry, swine, and ruminant sectors, thereby driving bulk demand. Additionally, integrated livestock producers often rely on in-house or partnered feed production systems, further strengthening this segment. While premix companies and veterinary service providers play a crucial supporting role in distribution and advisory, their volumes remain comparatively lower. The increasing industrialization of animal farming and emphasis on preventive nutrition strategies continue to reinforce feed manufacturers as the primary consumption hub for mycotoxin binders.

Regional Insights

North America Mycotoxin Binders Market Trends

North America is projected to account for 46.7% of the global mycotoxin binders market in 2026, with the United States serving as the central contributor. The region benefits from a highly organized livestock and feed industry, where quality control and contamination management are integral to operations. Mycotoxin occurrence in key crops such as corn and wheat has necessitated widespread adoption of binder solutions, particularly in large-scale poultry and swine production systems. Regulatory frameworks led by agencies like the Food and Drug Administration emphasize feed safety standards, encouraging routine inclusion of toxin mitigation strategies.

Moreover, strong awareness among producers regarding the economic impact of mycotoxicosis—such as reduced feed efficiency and animal performance—has driven consistent demand. The presence of leading feed additive manufacturers and continuous investments in R&D further support innovation in multi-mycotoxin binding solutions. Advanced feed management practices, coupled with precision nutrition approaches, are also influencing adoption patterns. Additionally, growing demand for high-quality animal protein continues to sustain feed production volumes, indirectly reinforcing the need for effective contamination control solutions across the region.

Europe Mycotoxin Binders Market Trends

Europe remains a mature and regulation-intensive market, characterized by stringent feed safety standards and proactive contamination monitoring systems. Countries such as Germany, France, Netherlands, Spain, and United Kingdom play a pivotal role in regional demand. The European Union enforces strict regulations on permissible mycotoxin levels in animal feed, compelling manufacturers to adopt preventive solutions such as binders and detoxifying agents.

The region’s well-established livestock sector, particularly in dairy and pork production, further supports consistent consumption of feed additives. In addition, sustainability considerations and emphasis on animal welfare have encouraged the use of safe and effective feed ingredients. Collaboration between research institutions and feed additive companies has accelerated the development of advanced binder technologies with broader toxin coverage. Import dependency for feed raw materials also increases exposure to contamination risks, making mitigation strategies essential. As regulatory scrutiny continues to tighten, adoption of mycotoxin binders is expected to remain strong across both Western and Eastern Europe.

Asia Pacific Mycotoxin Binders Market Trends

Asia Pacific is expected to be the fastest-growing region, expanding at a CAGR of approximately 7.3% between 2026 and 2033. Growth is primarily driven by rapid expansion of livestock production in countries such as China and India, where rising protein consumption is fueling demand for high-quality feed. Climatic conditions in the region, particularly high humidity and temperature, create a favorable environment for fungal growth, increasing the risk of mycotoxin contamination in feed crops.

Additionally, feed producers are increasingly incorporating binders to maintain animal health and productivity. The region is also witnessing significant investments in feed manufacturing infrastructure, enabling greater penetration of feed additives. Growing awareness among farmers regarding the economic losses associated with contaminated feed is further accelerating adoption. In addition, multinational companies are expanding their footprint to tap into the region’s high-growth potential. Government initiatives focused on improving feed quality standards and livestock productivity are also playing a supportive role. With evolving farming practices and increasing commercialization, Asia Pacific continues to emerge as a key growth engine for the market.

Competitive Landscape

The global mycotoxin binders market is highly competitive, with strong participation from Cargill, Incorporated, BIOMIN Holding GmbH, G. M. Biochem, BASF SE, Alltech, Inc., and Impextraco NV. These companies leverage advanced binding technologies, toxin adsorption efficiency, and integrated feed additive portfolios to strengthen market presence while improving livestock health and feed safety. Rising concerns over mycotoxin contamination are accelerating innovation, with manufacturers expanding production capacities, ensuring regulatory compliance, and investing in R&D to develop next-generation, multi-mycotoxin binding solutions.

Key Developments:

- In October 2025, Alltech, Inc. introduced Mycosorb® A+ Evo and Mycosorb® Evo, the latest additions to its established Mycosorb® portfolio of mycotoxin management solutions. These next-generation products mark a significant advancement in safeguarding livestock health and productivity, offering enhanced protection against complex multi-mycotoxin contamination challenges.

- In March 2025, Cargill, Incorporated Animal Nutrition & Health announced it would showcase new research at the World Mycotoxin Forum (April 7–9, 2025), highlighting global mycotoxin contamination patterns and their effects on poultry gut health. Conducted by its Micronutrition & Health Solutions division, the studies underscore Cargill’s focus on science-driven risk management and the development of advanced solutions aimed at improving livestock productivity.

- In March 2025, dsm-firmenich announced plans to expand its presence in Asia by establishing a new mycotoxin binder production facility in India, as highlighted during VIV Asia 2025.

- This strategic move is aimed at strengthening regional supply capabilities while addressing the growing demand for advanced feed safety solutions across emerging livestock markets.

Companies Covered in Mycotoxin Binders Market

- Cargill, Incorporated

- BIOMIN Holding GmbH

- G. M. Biochem

- BASF SE

- Alltech, Inc.

- Impextraco NV

- Micron Bio-Systems

- Perstorp Holding AB

- Special Nutrients, Inc.

- Clariant AG

- Olmix S.A.

- Kemin Industries, Inc.

- Novus International, Inc.

- Anpario plc

- Archer Daniels Midland Company (ADM)

- Others

Frequently Asked Questions

The global mycotoxin binders market is projected to be valued at US$ 2.8 Bn in 2026.

Rising contamination of feed by mycotoxins coupled with increasing demand for high-quality livestock productivity and stringent feed safety regulations globally.

The global mycotoxin binders market is poised to witness a CAGR of 5.6% between 2026 and 2033.

Growing shift toward biological and multi-functional binders alongside expanding livestock production in emerging markets creates significant growth potential.

Cargill, Incorporated, BIOMIN Holding GmbH, G. M. Biochem, BASF SE, Alltech, Inc., and Impextraco NV. are some of the key players in the clean label starch market.