- Animal Feed & Additives

- Feed Amino Acid Market

Feed Amino Acid Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Feed Amino Acid Market by Product Type (Lysine, Methionine, Threonine, Tryptophan), Livestock (Ruminants, Swine, Poultry, Aquatic animals), Form (Powder, Liquid, Blenches), and Regional Analysis for 2026 - 2033

Feed Amino Acid Market Share and Trends Analysis

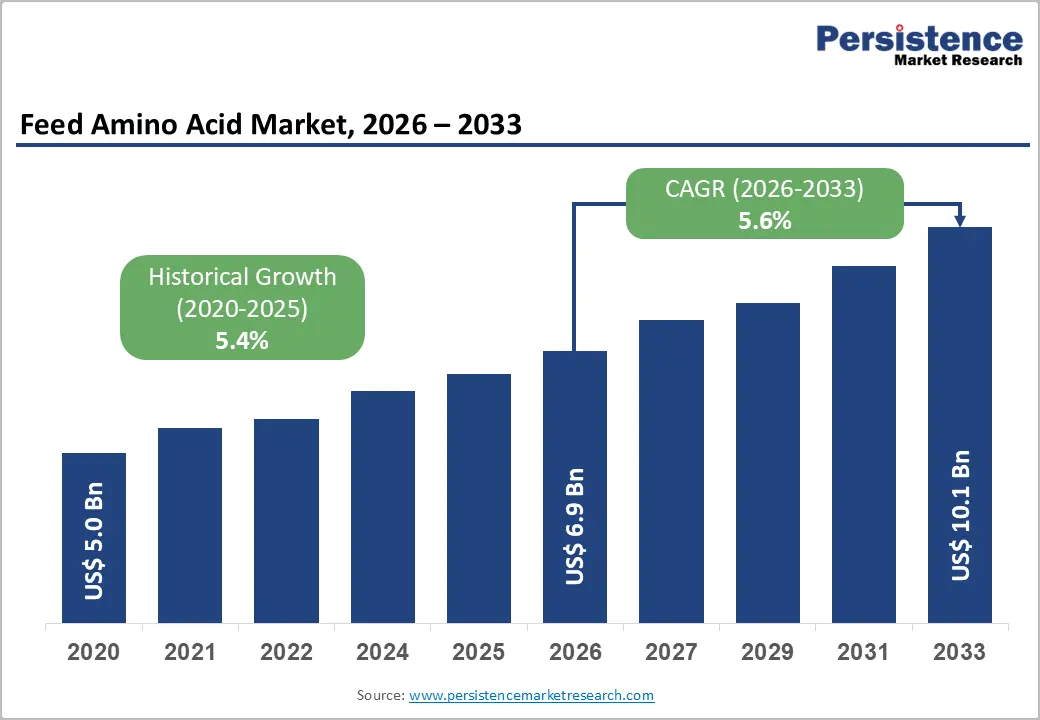

The global feed amino acid market size is likely to be valued at US$ 6.9 Bn in 2026 and is projected to reach US$10.1 Bn by 2033, growing at a CAGR of 5.6% during the forecast period 2026 - 2033.

The primary growth engine behind this expansion is the escalating global demand for high-quality animal protein, driven by a rising global population, rapid urbanization in emerging economies, and shifting dietary preferences toward meat-rich diets in the Asia Pacific and Latin America. Amino acids such as lysine, methionine, threonine, and tryptophan are integral to optimizing livestock nutrition, improving feed conversion ratios, and reducing nitrogen excretion, positioning them as indispensable inputs in modern animal agriculture.

Simultaneously, advances in fermentation-based biosynthesis and precision feeding technologies are driving cost efficiencies and enabling customized amino acid formulations that match specific livestock requirements. Regulatory tailwinds in Europe and North America, emphasizing sustainable and antibiotic-free livestock production, are further accelerating market adoption.

Key Industry Highlights

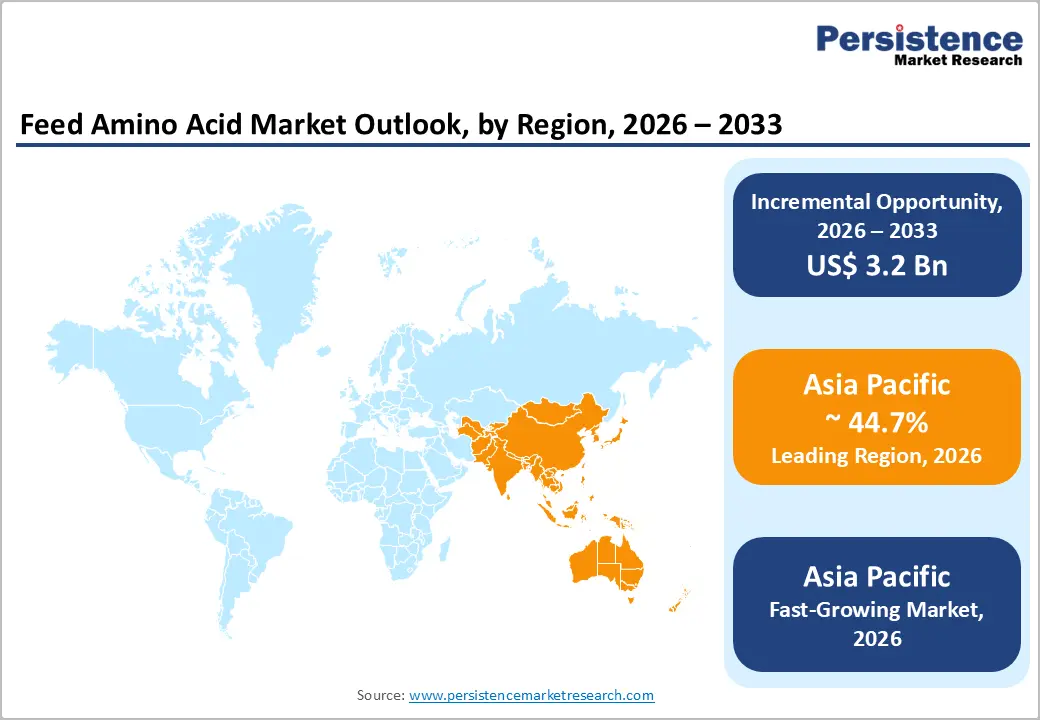

- Dominant Region: Asia Pacific is likely to be the leading regional market for feed amino acids in 2026, accounting for approximately 44.7% of the market share, due to the expansion of livestock production and feed manufacturing that is scaling across the region.

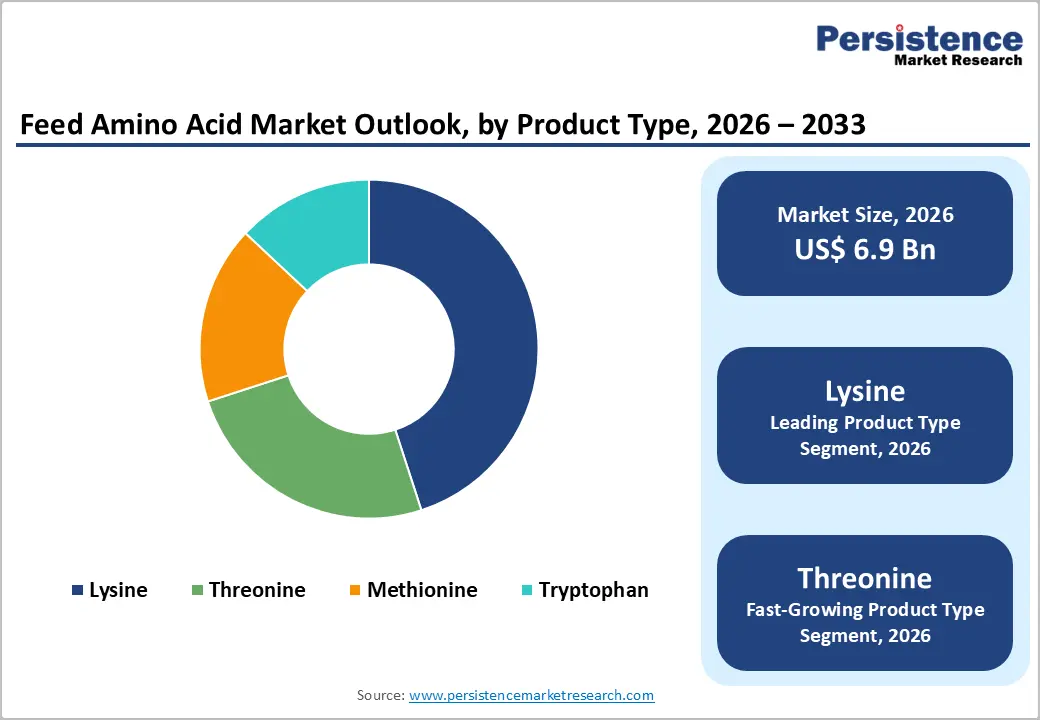

- Leading Product Type: Lysine currently dominates the product type segment, commanding approximately 36.2% of total market revenue in 2026, because it is functioning as the first-limiting amino acid in corn and soybean meal-based diets.

- Leading Livestock: Poultry represents the dominant segment, capturing approximately 44% of market revenue share in 2026, as production systems are becoming highly standardized and efficiency-driven.

- Growth Indicator: Demand for meat is rising steadily, driven by population growth and a shift in dietary preferences toward higher protein consumption.

- Market Opportunities: Stricter environmental regulations on nitrogen and ammonia emissions are driving changes in livestock nutrition strategies across key production regions.

| Key Insights | Details |

|---|---|

| Feed Amino Acid Market Size (2026E) | US$6.9 Bn |

| Market Value Forecast (2033F) | US$10.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Global Demand for Animal Protein

Global demand for meat is continuing to rise as population growth is increasing and dietary preferences are shifting toward higher protein intake. Developing regions in the Asia Pacific and Sub-Saharan Africa are experiencing a clear transition, where consumers are moving toward more animal-based nutrition as incomes are improving and urbanization is expanding. This shift is encouraging livestock producers to scale operations while maintaining efficiency and consistency. Poultry, swine, and aquaculture sectors are becoming more structured and commercially driven, which is increasing the need for precise and science-based feeding practices. Producers are focusing on improving productivity while ensuring sustainability, and they are adopting advanced nutritional strategies to meet evolving consumption patterns.

Feed amino acids are becoming an essential component in modern livestock nutrition as producers are optimizing feed formulations to achieve better growth outcomes. These nutrients help in reducing excess crude protein levels while maintaining animal performance and health. Production systems are becoming more intensive, and farmers are relying on amino acid supplementation to enhance feed conversion and reduce environmental impact. The industry will have fully integrated amino acids into standard feeding programs across species. This approach supports cost efficiency, improves resource utilization, and ensures consistent output quality in global animal protein production systems.

Technological Advancements in Fermentation-Based Production

Fermentation-based amino acid production undergoes a major transformation. Companies enable affordable, pure manufacturing on large scales. Experts engineer microbial strains for better yields. They apply real-time process monitoring and metabolic flux optimization. Producers cut costs through these methods. Firms such as Evonik Industries and CJ CheilJedang invest in advanced fermentation platforms. Evonik optimizes its MetAMINO methionine production to lower carbon emissions compared to industry norms. Technology upgrades expand profit margins and ensure steady product quality.

These advances introduce specialty and precision amino acid products. Manufacturers broaden market reach and draw fresh investors. Engineers design strains that resist contamination and boost output efficiency. Facilities integrate automation for precise control over fermentation cycles. Nutrition specialists develop custom blends for livestock feeds. Innovations will dominate supply chains and support sustainable practices. Global producers scale operations to meet demand from poultry, swine, and aquaculture sectors. This shift strengthens competitiveness and aligns with green chemistry goals.

Stringent Regulatory Compliance Requirements

Feed amino acid manufacturers are operating within a complex and fragmented global regulatory environment that is shaping how they develop and commercialize products. In the European Union (EU), Regulation (EC) No 1831/2003 governs the approval of feed additives, and companies are preparing detailed dossiers to demonstrate both safety and efficacy before authorization. In the United States (U.S.), the Food and Drug Administration (FDA) is applying the Generally Recognized as Safe (GRAS) framework, which requires scientific validation and transparent documentation. In China, the Ministry of Agriculture (MOA) is overseeing certification processes that are adding further procedural layers. These region-specific systems are increasing compliance requirements and are demanding strong technical expertise and regulatory planning from manufacturers.

Regulatory divergence is creating operational challenges for global producers who are managing multi-market portfolios. Companies are adapting formulations to meet country-specific standards, which is increasing production complexity and limiting scalability. This situation is also raising costs and extending product development cycles. Firms are expanding into new markets, and they are investing in regulatory intelligence and local partnerships to navigate approval pathways more efficiently. Manufacturers will have strengthened compliance frameworks and streamlined documentation practices, which will help them to reduce delays and improve global market access.

Competition from Alternative Protein Sources and Feed Additives

The growing availability of alternative protein sources is reshaping the competitive landscape for feed amino acids. Single-cell proteins, insect-based meals, and algae-derived ingredients are gaining attention as sustainable and nutritionally efficient options. Companies such as Protix and Beta Hatch are expanding production capabilities and are offering insect protein with naturally balanced amino acid profiles. These innovations are reducing dependence on synthetic supplementation by delivering more complete nutrient solutions within a single ingredient. Plant biotechnology is advancing rapidly, with firms such as Corteva and Bunge developing soybean varieties that are containing improved amino acid compositions. These developments are strengthening the nutritional value of traditional feedstocks.

These emerging solutions are still in early stages, but they are attracting strong investment and technological interest. Venture capital firms and institutional investors are supporting research, scaling, and commercialization efforts, which is accelerating market readiness. As production systems are maturing, these alternatives will have improved cost efficiency and supply consistency. Feed producers are evaluating these options to diversify sourcing and reduce reliance on conventional inputs. The industry will have faced increasing substitution pressure as these technologies gain acceptance. This change is encouraging amino acid manufacturers to innovate, differentiate their offerings, and enhance value through precision nutrition and integrated feed solutions.

Sustainable and Low-Protein Diet Formulations

Environmental policies that target nitrogen and ammonia emissions are reshaping livestock nutrition strategies across major producing regions. In the European Union (EU), frameworks such as the Nitrates Directive and the National Emission Ceilings Directive are pushing producers to adopt cleaner and more efficient feeding systems. Farmers are reducing crude protein levels in feed while incorporating synthetic amino acids to maintain animal health and productivity. This approach is aligning environmental compliance with operational efficiency, as lower nitrogen output is helping farms meet regulatory thresholds. Producers are also strengthening monitoring practices and are adopting precision feeding methods to ensure consistent nutrient delivery across poultry and swine operations.

Scientific assessments are reinforcing the benefits of this transition by demonstrating improved nutrient utilization and reduced waste output. Low-protein diets that are balanced with essential amino acids support stable growth performance while minimizing environmental impact. Feed manufacturers are responding by developing targeted formulations that match species-specific requirements and production goals. Adoption is spreading across North America and Europe as sustainability targets are becoming more integrated into agricultural policy frameworks. This shift is positioning amino acids as a core nutritional input, and demand will have increased steadily as producers continue prioritizing emission reduction and resource efficiency in intensive livestock systems.

Expansion of Specialty and Functional Amino Acids

Specialty amino acids like valine, isoleucine, and arginine are becoming more important because of their specific physiological roles. These nutrients help support immune response, boost metabolic efficiency, and improve reproductive performance in animals. Ruminant nutrition is gaining attention as dairy and beef producers aim to maximize output from high-performing herds. Precision feeding practices are growing in popularity, and nutritionists are creating balanced diets that meet precise amino acid requirements instead of just relying on broad protein inclusion. This shift is strengthening the importance of advanced amino acid solutions in enhancing both productivity and animal well-being.

Innovation accelerates in formulation technologies, particularly with encapsulated and rumen-protected amino acids. These products allow nutrients to bypass rumen degradation and reach the small intestine for effective absorption. Manufacturers invest in coating techniques and delivery systems that enhance stability and bioavailability. Premium formulations command higher value because they deliver measurable performance benefits, such as increased milk yield, improved fertility, and better feed efficiency. Competitive positioning now depends more on functional efficacy than on volume alone. Companies differentiate their portfolios through specialized solutions that meet the evolving demands of modern livestock production systems.

Category-wise Analysis

Product Type Insights

Lysine currently dominates the product type segment, commanding approximately 36.2% of total market revenue, because it is functioning as the first-limiting amino acid in corn and soybean meal-based diets, which are widely used across global livestock production systems. Nutritionists are consistently including lysine to balance essential amino acid profiles and support optimal growth performance in animals. Its supplementation is becoming a standard practice in commercial poultry and swine operations, where precise formulation is ensuring efficient feed utilization. Inclusion levels are remaining carefully calibrated in broiler diets, as producers are maintaining performance consistency while optimizing overall feed cost and nutrient efficiency.

Threonine is likely to be the fastest-growing segment during the 2026-2033 forecast period. Threonine is gaining importance in feed formulation as producers are shifting toward lower crude protein diets that depend on multiple amino acids to maintain proper nutrient balance. It is functioning as the second-limiting amino acid in swine diets and the third-limiting amino acid in poultry diets based on corn and soybean meal. As lysine supplementation is increasing to optimize growth, threonine levels require careful adjustment to maintain the correct ratio. Nutritionists are including threonine to support gut health, protein synthesis, and overall performance, ensuring that animals are achieving consistent productivity under more precise feeding strategies.

Livestock Insights

Poultry represents the dominant segment, capturing approximately 44% of market revenue share in 2026, as production systems are becoming highly standardized and efficiency-driven. Broiler and layer operations rely on scientifically balanced feed formulations to achieve consistent growth and output. Amino acid supplementation is playing a central role in optimizing feed conversion, supporting muscle development, and maintaining bird health. Corn and soybean meal-based diets require precise nutrient balancing, which increases dependence on synthetic amino acids. Large-scale commercial integration is further strengthening adoption, as producers are prioritizing cost control and uniform performance across flocks in intensive production environments.

Aquatic animals are expected to be the fastest-growing segment in the forecast period. Fish and shrimp farming systems are becoming more intensive, which is increasing the need for nutritionally optimized feed. Amino acids support growth performance, stress resistance, and feed efficiency in controlled aquatic environments. Traditional fishmeal usage is declining, and plant-based alternatives require supplementation to maintain amino acid balance. Feed producers are developing species-specific formulations, and this approach will have accelerated adoption as aquaculture operations are focusing on productivity, disease management, and environmental sustainability.

Regional Insights

Asia Pacific Feed Amino Acid Market Trends

Asia Pacific is likely to be the leading regional market for feed amino acids in 2026, accounting for approximately 44.7% of the market share. It is continuing to expand as livestock production and feed manufacturing are scaling across the region. China is strengthening its position as a central force in both consumption and production, supported by its large pork and poultry industries. The country is also serving as a major manufacturing hub, with companies such as Meihua Holdings Group, Fufeng Group, and Global Bio-Chem Technology operating integrated fermentation facilities. These firms are supplying domestic demand while expanding export capabilities. Regulatory authorities are tightening environmental and food safety standards, which is encouraging modernization and consolidation across the industry.

India is emerging as the fastest-growing market as poultry production is expanding and aquaculture is gaining commercial traction. Southeast Asian nations such as Vietnam, Indonesia, and Thailand are strengthening compound feed industries to support rising animal protein demand. Japan and South Korea are focusing on high-purity and specialty amino acids, supported by strong research and development ecosystems. Regional players are investing in advanced production technologies and precision nutrition solutions, and the market will expand further as efficiency, sustainability, and quality standards continue shaping long-term growth.

Europe Feed Amino Acid Market Trends

Europe is holding a strong position in the market, with countries such as Germany, France, Spain, the United Kingdom, and the Netherlands serving as the main consumption hubs. Poultry and swine sectors in Germany and France are driving demand for amino acid supplementation, as producers are focusing on high feed conversion efficiency and consistent livestock performance. European livestock systems are adopting precision nutrition practices, where amino acids are supporting optimized growth, improved protein utilization, and reduced feed costs. The combination of sophisticated production standards and regulatory expectations is creating structural demand for premium feed additives, positioning amino acids as a core element in modern livestock diets.

European policy frameworks are guiding transformative changes in feed formulation, with strategies such as the Farm to Fork Strategy and the Nitrates Directive encouraging lower crude protein diets supplemented with synthetic amino acids to reduce nitrogen emissions. Producers are responding by developing innovative formulations that maintain performance while supporting environmental goals. Companies such as Evonik and Adisseo are leveraging local production, regulatory expertise, and strong customer networks to sustain competitiveness. Market growth is being reinforced by sustainability-driven product innovation, and feed manufacturers will have strengthened adoption of advanced amino acid solutions that deliver both economic and environmental benefits across Europe’s intensive livestock operations.

North America Feed Amino Acid Market Trends

North America maintains a strong and well-established position in the global feed amino acid market, led by the United States, which is supporting large-scale poultry and swine production as well as integrated beef operations. Feed manufacturers are increasingly relying on amino acids to optimize nutrition, improve growth performance, and enhance feed efficiency. Companies such as ADM are operating extensive production and distribution networks for lysine and other essential amino acids, supplying a broad base of commercial feed operations. Producers are adopting precision nutrition strategies to maintain uniform performance across flocks and herds while managing feed costs effectively.

The regulatory environment is shaping industry transformation, with frameworks such as the Food and Drug Administration (FDA), Veterinary Feed Directive, and sustainable agriculture programs from the United States Department of Agriculture (USDA) promoting antibiotic-free and environmentally responsible livestock production. Amino acids support this transition by enabling lower-protein, balanced diets that maintain productivity. In Canada, aquaculture growth in regions such as British Columbia is driving the adoption of formulations enriched with tryptophan for salmon and trout. Feed companies are focusing on innovative delivery systems and sustainable solutions, and the market will have advanced as producers are increasingly prioritizing precision, efficiency, and environmental stewardship across livestock and aquaculture sectors in North America.

Competitive Landscape

The global feed amino acid market structure is moderately fragmented, dominated by leading players such as Evonik Industries AG, Ajinomoto Co., Inc., and CJ CheilJedang. These players collectively capture 35-40% of the market share. The market is operating within a dual-structured competitive landscape. One tier focuses on high-volume commodity amino acids such as lysine and threonine, where large-scale production and cost efficiency are determining factors for success. The other tier emphasizes premium and specialty products, including protected methionine, tryptophan, and encapsulated formulations. Companies competing in this segment are leveraging technical innovation, product stability, and regulatory expertise to differentiate themselves. Producers are investing in research and advanced manufacturing technologies, and the market will have strengthened as these specialized solutions continue to command higher value and performance-based adoption across livestock and aquaculture operations.

Key Developments:

- In February 2026, Danish feed company BioMar launched a new functional seabass feed, “SmartCare Defence,” in Europe to help Mediterranean seabass farmers better manage seasonal bacterial outbreaks such as those caused by Photobacterium, Vibrio, and Aeromonas. The product, developed over five years through lab and farm trials, contains a tailored blend of functional ingredients and micronutrients designed to strengthen intestinal integrity and immune function, cutting mortality during high-risk periods without relying on medicated feeds.

- In December 2025, Orffa launched its branded Elovital amino acids and vitamins line for South Asia, expanding its portfolio of science-based feed additives for poultry, aquaculture, and livestock. The new range, unveiled at Poultry India 2025, strengthens Orffa’s position as a comprehensive nutrition partner in the region by offering essential amino acids and both fat- and water-soluble vitamins under a unified, high-quality brand.

Companies Covered in Feed Amino Acid Market

- Evonik Industries AG

- Ajinomoto Co., Inc.

- CJ CheilJedang Corporation

- Archer Daniels Midland

- Adisseo

- Meihua Holdings Group Co., Ltd.

- Fufeng Group Company Limited

- Novus International, Inc.

- Kemin Industries, Inc.

- Global Bio Chem Technology Group

- Phibro Animal Health Corporation

- Sunrise Nutrachem Group

- Kyowa Hakko Bio Co., Ltd.

- dsm firmenich

- Sumitomo Chemical Co., Ltd.

Frequently Asked Questions

The feed amino acid market is projected to reach US$6.9 Bn in 2026.

The market is driven by rising demand for high-efficiency animal nutrition to improve feed conversion, reduce nitrogen excretion, and support sustainable livestock and aquaculture production.

The feed amino acid market is poised to witness a CAGR of 5.6% from 2026 to 2033.

Major opportunities lie in expanding the use of specialty amino acids, functional feeds, and precision nutrition in emerging markets and antibiotic‑free production systems.

Evonik Industries AG, Ajinomoto Co., Inc., and CJ CheilJedang are some of the key players in the market.