- Beauty & Personal Care

- Mineral Cosmetics Market

Mineral Cosmetics Market Size, Share, and Growth Forecast 2026 - 2033

Mineral Cosmetics Market by Product Type (Face, Eye, Lips, Others), End-user (Men, Women), Distribution Channel (Hypermarkets & Supermarkets, Specialty Stores, Online), and Regional Analysis for 2026 - 2033

Mineral Cosmetics Market Size and Trend Analysis

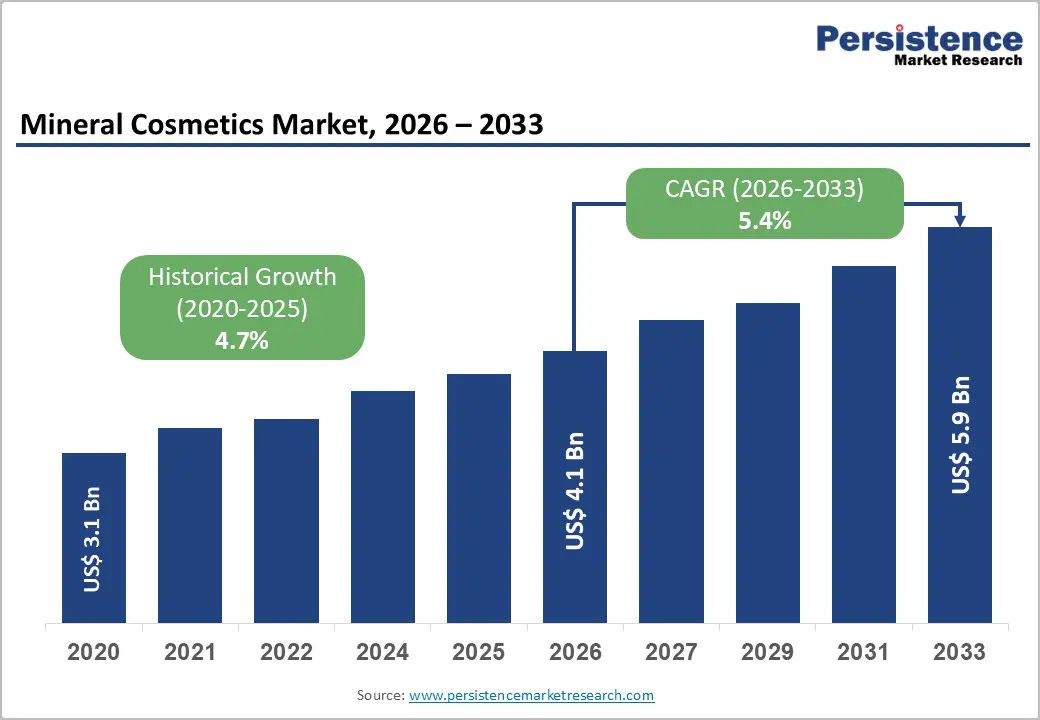

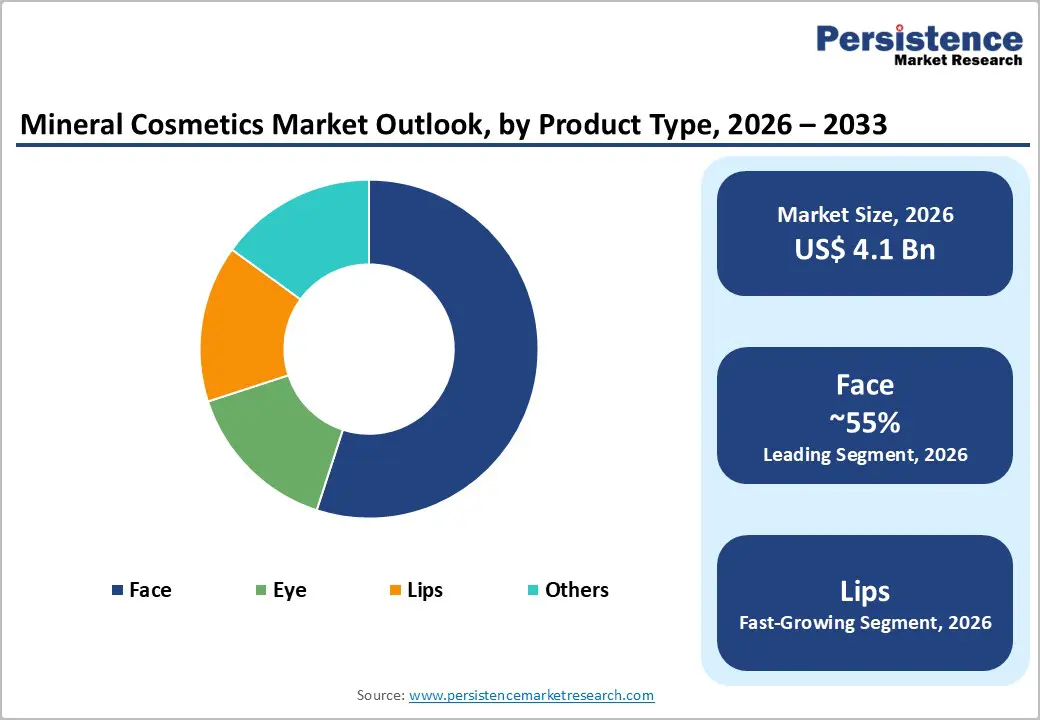

The global mineral cosmetics market size is supposed to be valued at US$ 4.1 billion in 2026 and is projected to reach US$ 5.9 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

The market growth is anchored in a powerful consumer pivot toward clean-label and skin-friendly beauty, supported by rising awareness about the harmful effects of synthetic ingredients such as parabens, talc, and bismuth oxychloride. According to the U.S. Food and Drug Administration (FDA), consumer complaints related to cosmetic adverse events have increased steadily, encouraging brands to reformulate with naturally derived minerals like zinc oxide, titanium dioxide, mica, and iron oxides that also offer broad-spectrum sun protection.

Key Industry Highlights

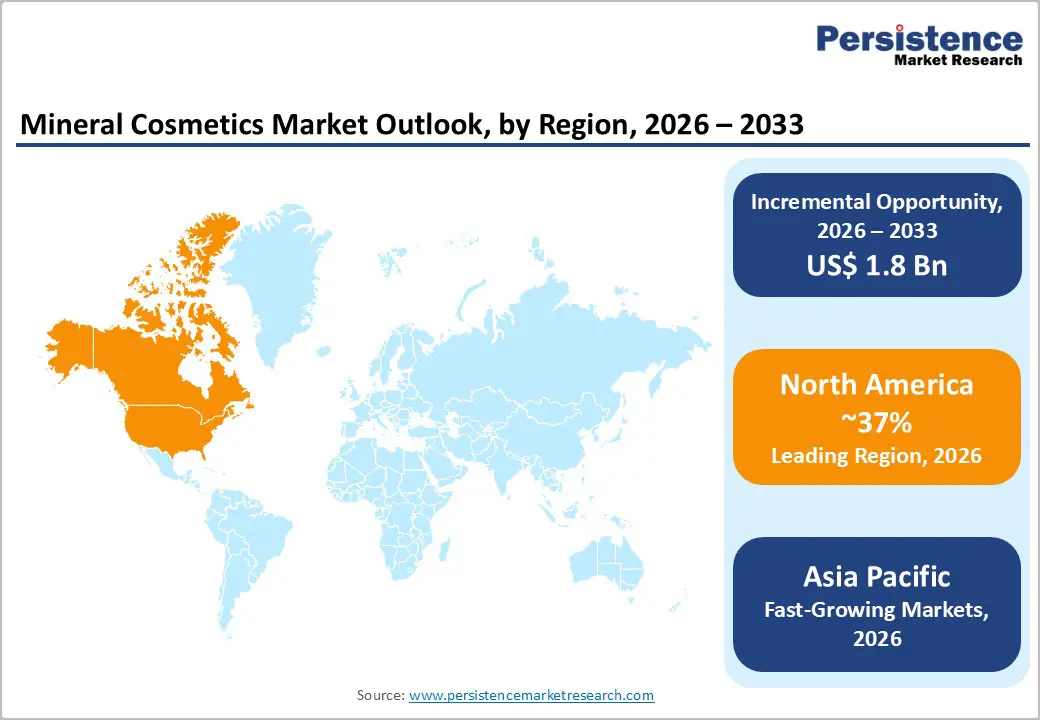

- Leading Region: North America leads the global mineral cosmetics market with nearly 37% share in 2026, driven by clean-beauty regulation, dermatology-led adoption, and strong specialty-retail penetration through Sephora and Ulta Beauty.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a projected CAGR of about 6.8%, supported by rising disposable incomes, K-beauty influence, and tightening cosmetic safety regulations across China, India, and Japan.

- Dominant Product Segment: The face product type leads with around 55% share in 2026, propelled by daily-use foundations, mineral powders, and BB creams offering non-comedogenic formulations and natural SPF protection.

- Fastest Growing Product Segment: The online distribution channel is the fastest-growing segment as D2C platforms, virtual try-on, and AI shade matching have a global reach for mineral cosmetics brands among Gen Z and millennial consumers.

- Key Market Opportunity: Rising adoption among male consumers and Gen Z represents a major opportunity, with nearly 47% of Gen Z men using mineral grooming products, opening fresh white space for gender-neutral lines.

DRO Analysis

Drivers - Rising Consumer Demand for Clean-Label and Hypoallergenic Beauty Products

A decisive shift toward clean beauty is the strongest tailwind for the mineral cosmetics market. According to a 2024 consumer survey by the Personal Care Products Council (PCPC), over 73% of U.S. consumers actively check ingredient labels before buying a cosmetic, and nearly 62% avoid products containing synthetic dyes or fragrances. Mineral-based formulations, certified by bodies such as ECOCERT and COSMOS, appeal to consumers with sensitive skin, rosacea, and acne-prone conditions.

The American Academy of Dermatology also recommends mineral-based sunscreens containing zinc oxide and titanium dioxide as a safer alternative, directly boosting demand within the broader natural cosmetics market.

Expanding Vegan and Cruelty-Free Beauty Movement

The vegan beauty wave is materially accelerating mineral cosmetics adoption. Data published by PETA shows that the number of certified cruelty-free brands grew by more than 32% between 2021 and 2024, with mineral makeup forming a core pillar of these portfolios.

Regulatory action is reinforcing the trend: Regulation (EC) No. 1223/2009 of the European Union prohibits animal testing on finished cosmetic products, while California’s S.B. 1249 bans the sale of cosmetics tested on animals. As lifestyle preferences and ESG mandates converge, mineral cosmetics, naturally derived from inert pigments such as iron oxides and ultramarines, are positioned as the default upgrade path within the global vegan cosmetics market.

Restraints - High Production Cost and Premium Retail Pricing

Mineral cosmetics typically command a price premium of 20% to 40% over conventional alternatives due to costlier raw materials, micronization processes, and stricter purity testing. Pigment-grade titanium dioxide and ultrafine mica require specialized milling, and prices for high-purity mica rose by nearly 18% during 2022-2024, according to the U.S. Geological Survey (USGS) Mineral Commodity Summaries. This makes mineral makeup less accessible in price-sensitive emerging markets and creates resistance among mass-market consumers, slowing volume penetration.

Regulatory Scrutiny Around Mica Sourcing and Nano-Ingredients

Supply-chain ethics and ingredient safety are creating execution risk for brand owners. Investigations by the International Labour Organization (ILO) have flagged child-labor concerns in mica mining belts of Jharkhand and Bihar, prompting tighter audits. In parallel, the European Commission requires nano-form titanium dioxide and zinc oxide to be labeled and assessed under Regulation (EC) No. 1223/2009. Compliance costs, reformulation pressures, and reputational exposure linked to the natural mica supply chain restrain near-term scalability for smaller players.

Opportunities - Rapid Growth of E-commerce and Direct-to-Consumer Beauty Channels

Digital retail has emerged as the most decisive growth pocket. According to the U.S. Census Bureau, the e-commerce share of total retail sales reached 16.1% in Q4 2024, with health and personal care leading category growth. Mineral cosmetics brands such as Iredale Cosmetics, Inc. and Glo Skin Beauty are expanding D2C platforms, leveraging influencer partnerships, virtual try-on technologies, and AI-driven shade matching to convert dermatology-conscious shoppers. Cross-border sales through marketplaces like Amazon and Sephora are unlocking access to APAC and Middle East buyers, where the broader online cosmetics market is widely expected to outpace offline retail by 2033.

Rising Adoption Among Male Consumers and Gen Z

Demographic expansion is opening fresh white space. A 2024 study by Mintel noted that nearly 47% of Gen Z men in the U.S. and U.K. now use some form of grooming or makeup product, with mineral-based BB creams and tinted SPFs being entry points. Brands like The Estée Lauder Companies and Shiseido Company Limited have launched gender-neutral mineral lines, while social platforms such as TikTok have made hashtags like #cleanboybeauty and #mineralmakeupformen viral, with billions of cumulative views. As stigma erodes and dermatologists endorse non-comedogenic mineral formulations, this consumer base will continue to feed the men’s grooming products market with high-margin SKUs.

Category-wise Analysis

Product Type Insights

The face segment dominates the mineral cosmetics market with a share of about 55% in 2026. Foundations, mineral powders, blushes, bronzers, and BB/CC creams account for the bulk of consumer spending because face products are used daily and benefit most from skin-friendly attributes such as oil control, non-comedogenic finishes, and natural SPF from titanium dioxide and zinc oxide.

According to the U.S. FDA, facial cosmetics are the most regulated and most consumed sub-category in personal care, which has pushed major players such as L’Oréal Groupe and Iredale Cosmetics, Inc. to invest heavily in mineral-based foundation lines. Rising dermatologist recommendations for mineral SPF formulations further reinforce the segment’s dominance within the broader facial cosmetics market.

End-user Insights

Women remain the dominant End-user segment, accounting for nearly 82% of mineral cosmetics revenue in 2026. Higher daily usage frequency, broader SKU adoption across face, eye, and lip categories, and a deep-rooted preference for clean-label products drive this share. More than 70% of women aged 18-44 in the U.S. have purchased mineral or natural makeup at least once.

Women are also the primary audience for premium dermatologist-endorsed brands such as Glo Skin Beauty and Mineralissima, while marketing budgets across the broader women’s personal care market remain heavily skewed toward female buyers, ensuring sustained dominance.

Distribution Channel Analysis

Specialty stores hold the leading share of about 41% in 2026, supported by curated brand portfolios, in-store consultations, and shade-matching services. Banners such as Sephora and Ulta Beauty have built dedicated clean-beauty zones featuring Iredale Cosmetics, Inc., Glo Skin Beauty, and BWX Limited.

According to data from the U.S. Bureau of Labor Statistics, consumer spending on beauty specialty retail grew by more than 9% year-over-year in 2024, outpacing mass-channel growth. Trained beauty advisors, premium brand storytelling, and loyalty programs offer experiential value that purely digital channels still struggle to replicate, anchoring specialty stores as the leading distribution route.

Regional Analysis

North America Mineral Cosmetics Market Trends & Analysis

North America is the leading regional market, accounting for an estimated 37% share in 2026, driven by high consumer awareness, dermatology-led prescribing, and the presence of category leaders such as The Estée Lauder Companies and Revlon, Inc. The U.S. FDA’s Modernization of Cosmetics Regulation Act (MoCRA), enacted in 2022 and being phased in through 2025, has intensified ingredient transparency, accelerating the shift toward mineral-based, hypoallergenic formulations.

U.S. Mineral Cosmetics Market Size

The U.S. is the single largest national market, contributing nearly 84% of North American revenue in 2026. Strong distribution through Sephora and Ulta Beauty, high per-capita beauty spending of more than US$ 320 annually as per U.S. Bureau of Labor Statistics data, and dermatologist-led adoption underpin growth.

Europe Mineral Cosmetics Market Trends, Drivers, & Insights

Europe is the second-largest region with around 29% market share in 2026. Strong regulatory protection under Regulation (EC) No. 1223/2009, high consumer demand for organic-certified products, and the presence of L’Oréal Groupe and BASF SE sustain regional momentum. According to Cosmetics Europe, retail sales of cosmetics across the EU exceeded €88 Bn in 2023, with natural and mineral cosmetics being the fastest-growing sub-segment.

Germany Mineral Cosmetics Market Size

Germany is the largest European country market with approximately 23% regional share. Per Eurostat, Germany has the highest absolute personal care spending in the EU, supported by drugstore-led distribution through dm-drogerie markt and Rossmann.

U.K. Mineral Cosmetics Market Size

The U.K. holds about 18% of the European market. Data from the Office for National Statistics (ONS) shows U.K. cosmetics retail sales growing steadily, while clean-beauty initiatives by Boots and John Lewis Beauty accelerate mineral cosmetics adoption.

France Mineral Cosmetics Market Size

France contributes nearly 16% of European revenue, anchored by its global beauty-export leadership. FEBEA (Fédération des Entreprises de la Beauté) reported French cosmetic exports worth more than €20 Bn in 2023, with naturals and mineral makeup among the fastest-growing categories.

Asia Pacific Mineral Cosmetics Market Drivers & Analysis

Asia Pacific is the fastest-growing region, projected to expand at a CAGR of nearly 6.8% between 2026 and 2033. The region accounts for around 24% of the market in 2026, supported by rising disposable incomes, rapid urbanization, K-beauty and J-beauty influence, and growing dermatology consultations across China, India, and Japan.

China Mineral Cosmetics Market Size

China is the largest APAC contributor with about 38% regional share. The National Medical Products Administration (NMPA) has tightened cosmetic safety regulations under the Cosmetic Supervision and Administration Regulation (CSAR), boosting demand for naturally derived mineral formulations.

India Mineral Cosmetics Market Size

India is the fastest-growing APAC country market, projected to expand at over 9% CAGR. Data from the Ministry of Commerce and Industry, Government of India, shows beauty and personal care exports rising steadily, while domestic D2C clean-beauty brands accelerate mineral cosmetics penetration.

Japan Mineral Cosmetics Market Size

Japan accounts for nearly 21% of APAC revenue, led by Shiseido Company Limited and supported by an aging consumer base prioritizing skin-safe, sensitive-skin-friendly mineral product. According to the Japan Cosmetic Industry Association (JCIA), domestic cosmetics shipments exceeded ¥1.6 trillion in 2023.

Competitive Landscape

The mineral cosmetics market is moderately fragmented, with the top five players accounting for nearly 42% of global revenue. Multinationals such as L’Oréal Groupe, The Estée Lauder Companies, and Shiseido Company Limited compete on R&D depth, dermatologist endorsements, and global retail penetration, while specialist players like Iredale Cosmetics, Inc. and Glo Skin Beauty differentiate via professional-channel partnerships. Strategies emphasize clean-label reformulation, vegan certification, sustainable mica sourcing, D2C expansion, and AI-led personalization.

Key Developments

- March 2026: KYT Group, a consumer-focused investment and advisory firm, announced the acquisition of professional skincare and mineral cosmetics brand Glo Skin Beauty, marking its first major deal in the beauty segment.

- February 2026: Shiseido Company Ltd. announced the 70th anniversary of its Life Quality Makeup initiative, reinforcing its long-standing innovation in advanced cosmetic solutions, including mineral-based and skin-sensitive formulations. The program focuses on developing specialized makeup products designed for individuals with skin concerns such as vitiligo, scars, burns, and post-medical treatment effects.

- April 2026: Clariant unveiled its “Let True Beauty Glow” Formulation Concept 2026, introducing a portfolio of 15 multifunctional formulations aimed at redefining natural beauty and mineral-friendly cosmetic innovation. The concept emphasizes natural radiance, authentic self-expression, and simplified beauty routines, aligning with rising consumer demand for minimalist, skin-friendly formulations often associated with mineral and clean beauty trends.

Top Companies in the Mineral Cosmetics Market

- L’Oréal Groupe (Clichy, France), through brands such as Garnier, La Roche-Posay, and Vichy, leads in mineral-based SPF, clean-label foundations, and dermatologist-recommended portfolios across more than 150 countries.

- The Estée Lauder Companies (New York, USA) operates marquee brands including Estée Lauder, Clinique, MAC, and Bobbi Brown. Its mineral and clean-beauty assortments are anchored in dermatologist endorsements and global prestige retail channels.

- Shiseido Company Limited (Tokyo, Japan)’s Anessa, NARS, and Clé de Peau Beauté brands lead innovation in mineral SPF and skincare-makeup hybrids across the Asia Pacific and globally.

Mineral Cosmetics Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 3.1 Bn |

| Current Market Value (2026) | US$ 4.1 Bn |

| Projected Market Value (2033) | US$ 5.9 Bn |

| CAGR (2026 - 2033) | 5.4% |

| Leading Region | North America, 37% |

| Dominant Segment | Face (Product Type), 55% |

| Top-ranking Segment | Women (End-user), 82% |

| Incremental Opportunity | US$ 1.8 Bn |

Companies Covered in Mineral Cosmetics Market

- L’Oréal Groupe

- The Estée Lauder Companies

- Shiseido Company Limited

- Clariant

- BASF SE

- KYT Group

- Iredale Cosmetics, Inc.

- Pure Colors Cosmetics Inc.

- Mineralissima

- Revlon, Inc.

- BWX Limited

- Coty Inc.

- Amway Corporation

- LVMH Moët Hennessy Louis Vuitton

Frequently Asked Questions

The global mineral cosmetics market is valued at US$ 4.1 Bn in 2026 and is projected to reach US$ 5.9 Bn by 2033, expanding at a CAGR of 5.4% between 2026 and 2033.

Rising consumer demand for clean-label, vegan, and hypoallergenic beauty, reinforced by U.S. FDA ingredient-transparency rules and dermatologist endorsements of mineral SPF, remains the strongest demand driver for mineral cosmetics worldwide.

The face segment leads the mineral cosmetics market with around 55% share in 2026, supported by daily-use foundations, mineral powders, and BB creams offering a non-comedogenic finish and natural SPF benefits.

North America leads the global mineral cosmetics market with nearly 37% share in 2026, driven by clean-beauty regulation under MoCRA, strong specialty retail, and high dermatology-led consumer adoption.

Rapid e-commerce growth and rising adoption among male and Gen Z consumers represent the biggest opportunity, enabling brands to scale gender-neutral and dermatologist-endorsed mineral cosmetics globally through D2C channels.

Key players include L’Oréal Groupe, The Estée Lauder Companies, Shiseido Company Limited, BASF SE, Clariant, Iredale Cosmetics, Inc., Glo Skin Beauty, Mineralissima, Revlon, Inc., and BWX Limited.