- Beauty & Personal Care

- Luxury Perfume Market

Luxury Perfume Market Size, Share, and Growth Forecast 2026 - 2033

Luxury Perfume Market by User (Men, Women, Unisex), Price Range (US$ 50 - US$ 100, US$ 100 - US$ 200, Above US$ 200), Distribution Channel (Offline, Online), and Regional Analysis for 2026 - 2033

Luxury Perfume Market Size and Trend Analysis

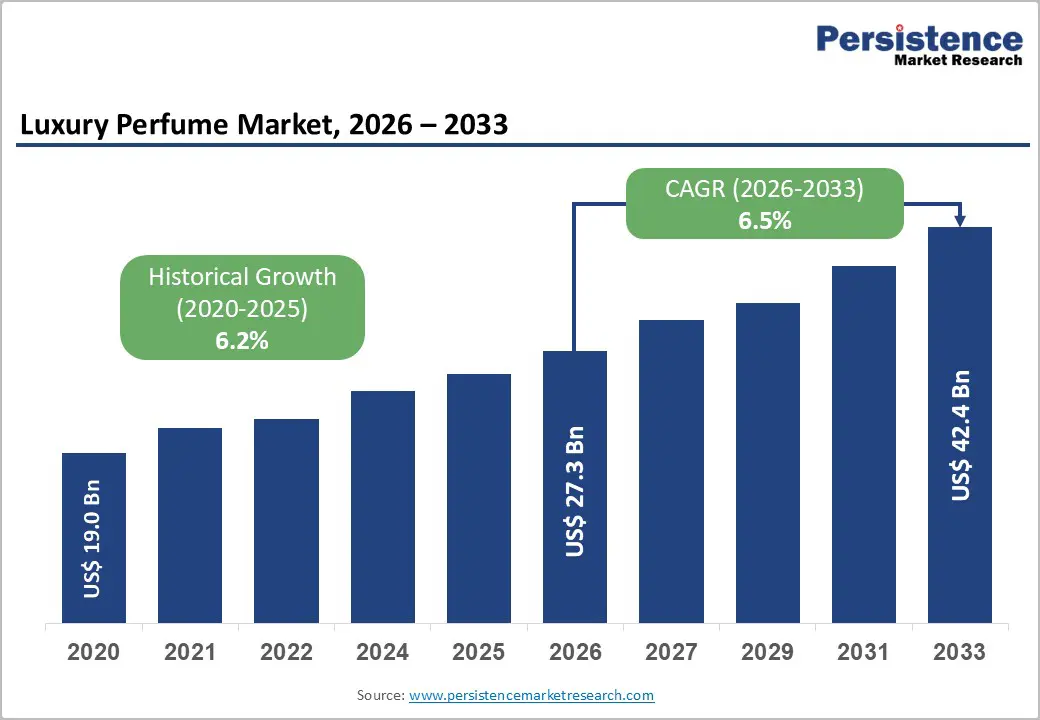

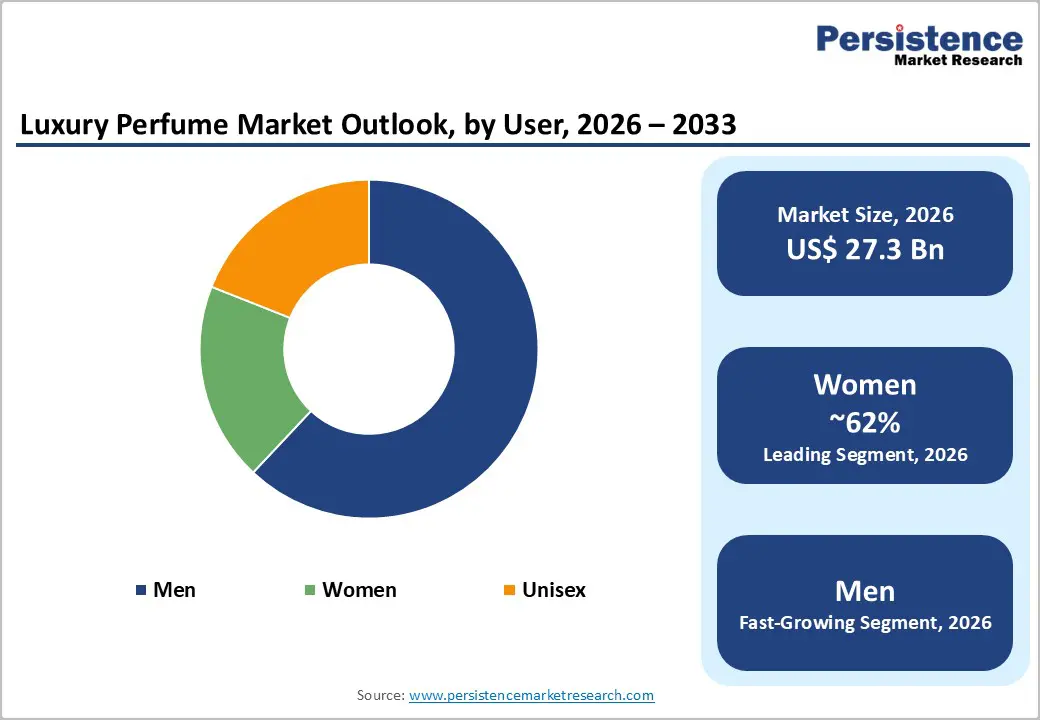

The global luxury perfume market size is valued at US$ 27.3 billion in 2026 and is projected to reach US$ 42.4 billion by 2033, growing at a CAGR of 6.5% between 2026 and 2033.

Growth is driven by higher spending on premium personal care, expanding affluent consumers in emerging markets, and fragrance’s role in identity and self-expression. The influence of social media platforms, the proliferation of luxury e-commerce channels, and the growing appetite for niche and artisanal perfumery are further reinforcing demand across both established Western markets and high-growth regions in the Asia Pacific and the Middle East.

Key Industry Highlights:

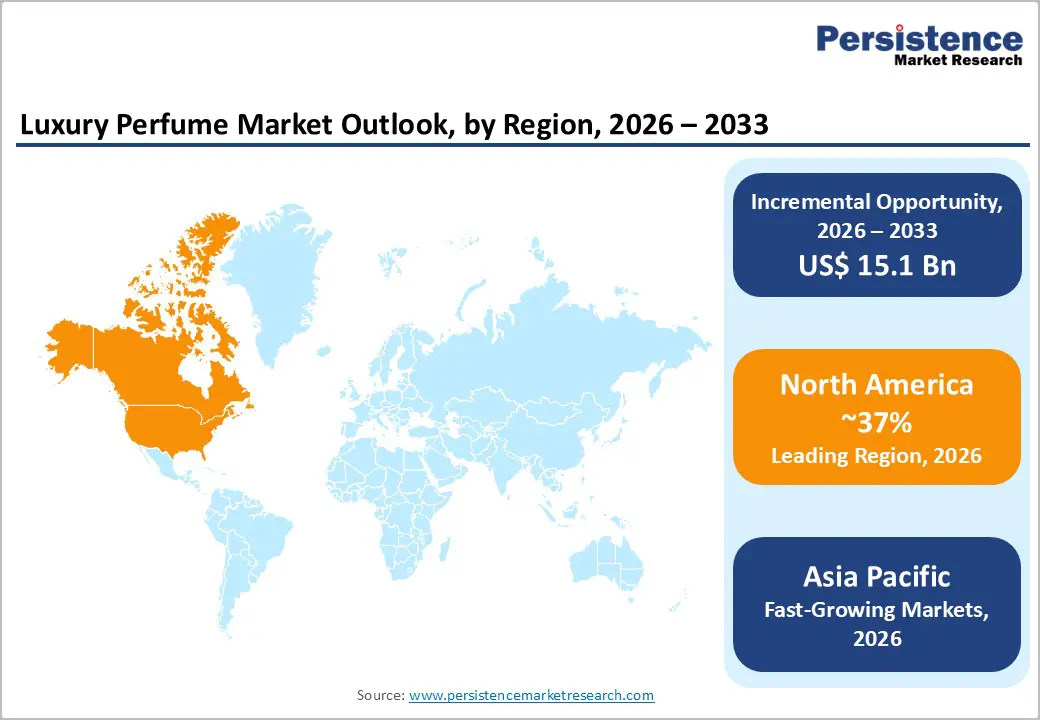

- Leading Region: North America leads the global Luxury Perfume market with approximately 37% of total revenues in 2026, driven by high consumer affluence, a robust luxury retail infrastructure, strong brand awareness, and a deeply embedded culture of premium personal care consumption.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market, fueled by rising disposable incomes, rapid urbanization, and the expanding aspirational luxury consumer base across China, India, and Japan, with the region forecast to grow at a CAGR exceeding the global average through 2033.

- Dominant Segment: The Women segment dominates the Luxury Perfume market with approximately 62% share, reflecting higher purchase frequency, strong brand engagement, social media-driven fragrance discovery, and the deep integration of premium fragrance into female personal grooming routines globally.

- Fastest-Growing User Segment: The Men’s luxury fragrance segment is among the fastest-growing categories, underpinned by evolving male grooming norms and a 26% increase in teen male spending on premium fragrance reported by Piper Sandler in 2023, signaling durable structural demand growth.

- Key Market Opportunity: The rise of niche and artisanal fragrances, particularly offerings priced above US$200, presents a high-value opportunity for market participants, as affluent consumers increasingly prioritize exclusivity, sustainability credentials, and distinctive olfactory experiences over mainstream designer lines.

DRO Analysis

Drivers - Rising Affluence and Premiumization Across Emerging Economies

Rising per capita incomes and the rapid expansion of middle- and upper-class consumers across emerging economies, especially in Asia-Pacific, the Middle East, and Latin America, are strengthening long-term demand for luxury fragrances. The World Bank projects the global middle class will reach about 5.3 billion people by 2030, with much of the incremental growth concentrated in China, India, and Southeast Asia.

As purchasing power rises, luxury perfume is increasingly viewed as an accessible status symbol and lifestyle marker, not merely a functional personal-care item. Leading fragrance groups such as LVMH, CHANEL, and The Estée Lauder Companies have reported strong momentum in these markets. Retailers are responding by adding flagship stores, deepening distribution partnerships, and launching market-specific collections.

Growing Male Grooming Culture and the Rise of Unisex Fragrances

Male grooming habits are evolving rapidly, making fine fragrance one of the fastest-growing categories in men’s personal care. In a 2023 teen spending survey by Piper Sandler, male teen spending on premium perfume rose 26% year over year, with demand skewing toward luxury names such as Dior’s Sauvage, Jean Paul Gaultier, and Valentino. The shift signals that Gen Z and millennial men increasingly treat fragrance as a daily ritual tied to identity, confidence, and social aspiration rather than occasional use.

Simultaneously, growing acceptance of gender-fluid style is boosting unisex and gender-neutral launches, with heritage houses such as Hermès and Gucci rolling out collections designed to move beyond traditional gender boundaries. The convergence of evolving grooming culture, progressive gender norms, and luxury positioning is generating sustainable demand momentum across the men’s and unisex fragrance segments globally.

Market Restraints

Stringent Regulatory Pressure and Rising Ingredient Restrictions

Stricter regulations on fragrance ingredients are creating significant cost and operational challenges for luxury perfume manufacturers. The International Fragrance Association frequently updates standards, forcing costly reformulations that may alter legacy scents. In 2025, the European Chemicals Agency restricted certain synthetic musks, raising R&D costs by an estimated 15-20%. Varying compliance requirements across regions, including the European Union, the United States, and the Gulf Cooperation Council, further complicate global operations, impacting innovation timelines and pressuring margins for internationally active brands.

Proliferation of Counterfeit Products and Brand Equity Erosion

The rapid rise of counterfeit luxury perfumes is undermining brand equity, consumer trust, and revenues globally. The Organisation for Economic Co-operation and Development estimates that counterfeit goods account for about 2.5% of global trade, with fragrances heavily impacted. Fake products, often sold via informal online channels, divert sales from legitimate brands. Regions with weaker IP enforcement face higher risks. In response, companies are adopting technologies like QR-based authentication, blockchain tracking, and tamper-evident packaging to safeguard authenticity, though these measures increase operational costs and place additional pressure on profit margins.

Market Opportunities

Expansion of Luxury E-Commerce and AI-Powered Fragrance Personalization

The rapid digitization of luxury retail is creating a major growth avenue for luxury perfume brands to broaden reach, deepen engagement, and build data-led relationships with younger consumers. Online luxury perfume sales are expected to expand at a CAGR of 6.8% through 2030, outpacing overall category growth, as digital ecosystems enable personalized, premium shopping at scale. Brand-owned direct-to-consumer sites and curated luxury platforms such as Net-a-Porter and Harrods Online are becoming high-value distribution touchpoints.

Simultaneously, AI-enabled scent profiling, recommendation engines, and AR product experiences are helping replicate in-store consultation online and improve conversion. Market leaders, including LVMH and The Estée Lauder Companies, are increasing investment in digital transformation, underscoring e-commerce’s role as a core growth engine through the next decade.

Surge in Consumer Demand for Niche, Artisanal, and Sustainable Fragrances

Consumer preference for exclusivity, authentic brand storytelling, and distinctive scent signatures is accelerating the rise of niche and artisanal perfumery within the luxury fragrance market. Compared with mass designer launches, niche fragrances are typically produced in limited runs, often featuring rare materials and sustainably sourced or ethically certified ingredients, and they command premium prices, frequently above the US$ 200 threshold.

Strategic investor interest is also intensifying. In November 2024, a major global beauty retailer acquired a fast-growing niche fragrance brand for approximately US$ 150 million. Established houses such as Diptyque, Creed, and Le Labo continue to build loyal communities through experiential retail, heritage positioning, and ingredient transparency that resonates with environmentally and ethically conscious Gen Z and millennial consumers.

Category-wise Analysis

User Insights

The Women segment leads the global luxury perfume market, accounting for about 62% of total share, reflecting structurally higher purchase frequency and stronger engagement with prestige beauty and personal-grooming routines. Female consumers also tend to be more responsive to scent storytelling and brand cues, supporting repeat buying across designer and niche lines.

Recent launches reinforce this strength. Coty Inc.’s Burberry Goddess (launched August 2023) achieved a standout sales performance across key markets. Discovery and purchase intent are increasingly shaped by social platforms, especially Instagram and TikTok, which amplify reviews, trends, and creator-led recommendations, sustaining the segment’s dominance.

Price Range Insights

The US$ 100-US$ 200 price band holds the largest share of the global Luxury Perfume market, accounting for roughly 56% of total revenue. It is anchored by core Eau de Parfum (EDP) and Eau de Toilette (EDT) lines from leading houses such as CHANEL, Dior, Hermès, and Gucci, offering a strong balance of scent complexity, brand prestige, and perceived value.

Positioned as an “accessible luxury,” this tier appeals to a broad aspirational affluent base and fits comfortably within discretionary budgets while still signaling premium status. It is also a critical gifting segment: fragrances priced in this range are consistently chosen for festive periods, anniversaries, and other celebrations. Broad accessibility and repeat purchase behavior make this band central to overall market revenue stability.

Distribution Channel Insights

Offline channels dominate the global luxury perfume market, accounting for around 74% of sales, as in-store environments allow consumers to experience fragrances directly before purchase. Luxury department stores, flagship boutiques, and specialty perfumeries remain preferred touchpoints, with over 60% of buyers favoring physical testing.

Brands are enhancing this experience through immersive retail concepts, such as Maison Diptyque, which blends fragrance discovery with lifestyle elements. Despite this dominance, online channels are gaining traction as companies adopt digital tools like virtual sampling, AI-driven recommendations, and seamless direct-to-consumer platforms, enabling broader reach and convenience while complementing the sensory advantages of offline retail.

Regional Insights

North America Luxury Perfume Market Trends & Analysis

North America leads the global luxury perfume market with around 37% revenue share in 2026, driven by affluent consumers, advanced retail infrastructure, and strong lifestyle branding culture. Growth is supported by celebrity-driven trends, digital marketing, and the expansion of premium retail and direct-to-consumer channels.

U.S. Luxury Perfume Market Trends

The U.S. Luxury Perfume market is estimated at US$ 8.3 billion in 2026, representing approximately 82% of the total North America regional market, driven by high disposable incomes, a deeply entrenched luxury consumption culture, and a highly competitive retail and e-commerce landscape.

Europe Luxury Perfume Market Trends, Drivers, & Insights

Europe represents the world’s most historically significant luxury fragrance hub, contributing approximately 34% of global market revenues in 2026. Regulatory complexity, particularly regarding ingredient restrictions imposed by the European Chemicals Agency (ECHA), presents localized operational challenges, though European luxury brands have strategically pivoted toward premium natural ingredient formulations and sustainability-led product development to address evolving regulatory requirements.

Germany Luxury Perfume Market: Estimated at US$ 2.2 Bn in 2026, underpinned by a high-income consumer base, strong brand sophistication, and an established appreciation for both designer and niche fragrance offerings.

U.K. Luxury Perfume Market: Estimated at US$ 1.9 Bn in 2026, with demand driven by affluent urban consumers, a vibrant luxury department store sector, robust travel retail infrastructure, and the growing influence of online luxury retail platforms.

France Luxury Perfume Market: Estimated at US$ 2.5 Bn in 2026, reflecting the nation’s unrivaled cultural leadership in global haute perfumeries and the enduring commercial strength of iconic French fragrance maisons.

Asia Pacific Luxury Perfume Market Drivers & Analysis

Asia Pacific is the fastest-growing regional market in the global Luxury Perfume industry, projected to expand at a CAGR of 8.2%, driven by rapidly rising disposable incomes, accelerating urbanization, and the explosive growth of aspirational luxury consumption across China, India, and Japan. Increasing exposure to global luxury fragrance brands through social media platforms, international travel, and cross-border e-commerce is substantially amplifying brand awareness and purchase intent among younger demographics across the region.

China Luxury Perfume Market: Estimated at US$ 2.0 Bn in 2026, supported by a rapidly expanding urban affluent class, booming prestige beauty consumption, and the rapid maturation of domestic luxury e-commerce platforms.

India Luxury Perfume Market: Estimated at US$ 0.8 Bn in 2026, with significant long-term growth potential driven by a large young consumer demographic, accelerating luxury brand penetration, and rising aspirational spending on premium personal care products.

Japan Luxury Perfume Market: Estimated at US$ 1.2 Bn in 2026, characterized by mature consumer sophistication, entrenched brand loyalty, and a distinctive cultural affinity for refined, understated, and high-quality fragrance experiences.

Competitive Landscape

The global luxury perfume market is moderately consolidated, with leaders like LVMH, CHANEL, The Estée Lauder Companies, Coty Inc., and L’Oréal Groupe holding a dominant share. Competition centers on portfolio breadth, experiential retail, and digital-first strategies targeting younger consumers. Investment is rising in sustainable sourcing, refillable packaging, and AI-driven personalization. Meanwhile, niche fragrance brands are gaining traction, attracting partnerships and acquisitions, while fashion and lifestyle players are increasingly entering the segment through licensing deals, intensifying competitive dynamics.

Key Developments

- April 2026: French luxury house Chanel announced Australian actor Jacob Elordi as the new global ambassador for its flagship men’s fragrance Bleu de Chanel, marking a significant brand positioning move in the luxury perfume market.

- March 2026: L'Oréal announced the completion of its €4 billion acquisition of Kering Beauté, marking one of the largest deals in the luxury perfume and beauty segment. The transaction includes the integration of House of Creed, a leading niche fragrance house, into L’Oréal’s portfolio.

- March 2026: The Estée Lauder Companies announced a new phase in its long-standing partnership with Forest Essentials by agreeing to acquire full ownership of the brand after an 18-year collaboration. The move builds on Estée Lauder’s initial minority investment in 2008, later increased to 49% in 2020, and reflects strong confidence in Forest Essentials’ brand equity, vertically integrated operations, and sustainability positioning.

Top Companies in Luxury Perfume

- CHANEL (Neuilly-sur-Seine, France), as a private, family-controlled global luxury powerhouse, maintains unparalleled brand equity within the fine fragrance category, anchored by iconic commercial franchises including CHANEL No. 5, which celebrated over a century of market leadership in 2024. The company’s vertically integrated supply chain, rigorous selective distribution strategy, and steadfast refusal to dilute brand prestige through mass-market channels collectively underpin its sustained global market leadership.

- LVMH Moët Hennessy Louis Vuitton (Paris, France) operates one of the world’s most comprehensive and commercially powerful luxury fragrance portfolios through its dedicated Perfumes & Cosmetics division, encompassing globally recognized brands including Christian Dior, Givenchy, Guerlain, and Acqua di Parma. The conglomerate’s unmatched retail scale spanning over 75 countries, strategic investments in digital transformation, and the consistent double-digit growth performance of flagship lines such as Dior’s Sauvage collectively position it as the segment’s foremost commercial force.

- The Estée Lauder Companies (New York, U.S.) commands a formidable and strategically diversified luxury fragrance portfolio through brands including Jo Malone London, Tom Ford Beauty, Le Labo, and Editions de Parfums Frédéric Malle. Its dual strategic approach, simultaneously scaling core designer fragrance franchises through digital and travel retail channels while acquiring high-growth niche brands, has enabled the company to capture meaningful share across multiple consumer segments, price tiers, and geographic markets.

Luxury Perfume Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 19.0 Bn |

| Current Market Value (2026) | US$ 27.4 Bn |

| Projected Market Value (2033) | US$ 42.4 Bn |

| CAGR (2026 - 2033) | 6.5% |

| Leading Region | North America, 37% |

| Dominant Segment | Women (User), 62% |

| Top-ranking Segment | US$ 100-US$ 200 (Price Range), 56% |

| Incremental Opportunity | US$ 15.0 Bn |

Companies Covered in Luxury Perfume Market

- CHANEL

- Coty Inc.

- LVMH Moët Hennessy Louis Vuitton

- The Estée Lauder Companies

- L’Oréal Groupe

- Burberry Group PLC

- Hermès International S.A.

- Kering S.A.

- Prada S.p.A.

- Ralph Lauren Corporation

- Shiseido Company Limited

Frequently Asked Questions

The global Luxury Perfume market is valued at US$ 27.3 Bn in 2026 and is projected to reach US$ 42.4 Bn by 2033, growing at a CAGR of 6.5% during the forecast period. Growth is driven by rising affluence in emerging economies, premiumization trends, and increasing consumer preference for niche and experiential fragrance products across global markets.

Key growth drivers include rising per capita incomes and premiumization trends in the Asia Pacific, the Middle East, and Latin America. The rapidly evolving male grooming culture and a 26% surge in teen male fragrance spending. Growing consumer demand for niche and artisanal fragrances.

The Women segment leads the global Luxury Perfume market, accounting for approximately 62% of total revenues. Its dominance is supported by higher purchase frequency, strong brand loyalty, social media-driven discovery on platforms such as Instagram and TikTok, and the deep cultural integration of premium fragrance into female personal grooming and lifestyle rituals across global markets.

North America leads the global Luxury Perfume market, holding approximately 37% of total market revenues in 2026, with the United States accounting for approximately 82% of the regional total at an estimated US$ 8.3 Bn. The region’s leadership is anchored by high per capita incomes, a deeply embedded luxury consumption culture, a robust premium retail and e-commerce infrastructure, and strong brand awareness across all luxury fragrance tiers.

The most compelling growth opportunities include the rapid expansion of niche and artisanal fragrances, exemplified by a major beauty retail acquisition of a niche brand for approximately US$ 150 million in November 2024, driven by affluent consumer demand for exclusivity and sustainable credentials, and the accelerating growth of luxury e-commerce, underpinned by AI-driven personalization and digital innovation.

The global Luxury Perfume market is led by CHANEL, LVMH Moët Hennessy Louis Vuitton, The Estée Lauder Companies, Coty Inc., and L’Oréal Groupe, which collectively command a dominant share of total market revenues. Other significant participants include Hermès, Kering, Prada, Burberry Group PLC, Ralph Lauren Corporation, and Shiseido Company Limited.