- Pharmaceuticals

- Major Depressive Disorder Market

Major Depressive Disorder Market Size, Share, and Growth Forecast, 2026 - 2033

Major Depressive Disorder Market by Drug Type (Antidepressants, Atypical Antidepressants, Antipsychotics, Neuromodulators, Others), Application (Hospitals, Clinics, Others), and Regional Analysis for 2026 - 2033

Major Depressive Disorder Market Size and Trends Analysis

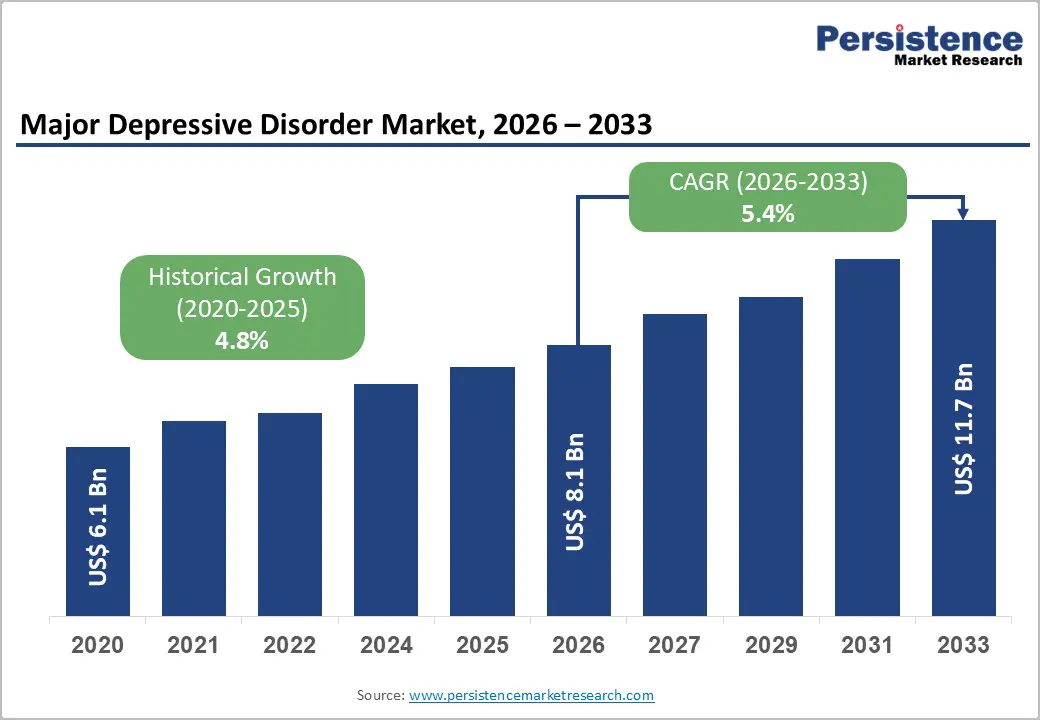

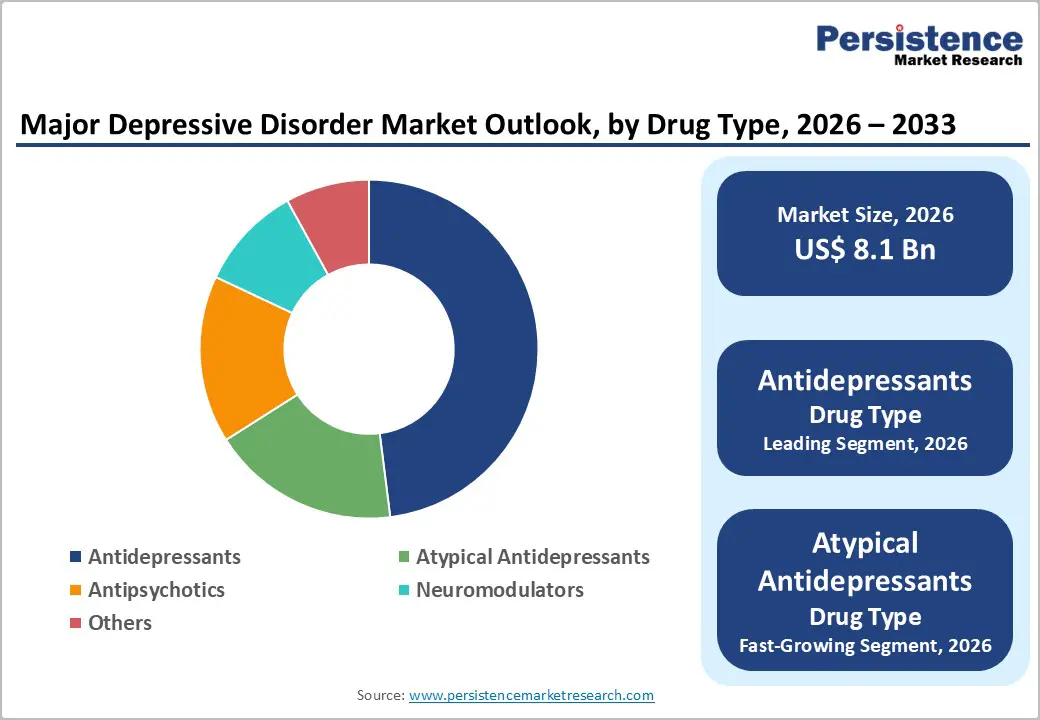

The global major depressive disorder market size is likely to be valued at US$8.1 billion in 2026, and is expected to reach US$11.7 billion by 2033, growing at a CAGR of 5.4% during the forecast period from 2026 to 2033, driven by increasing demand for effective treatment options for a widespread psychiatric condition marked by persistent low mood, anhedonia, fatigue, cognitive impairment, and, in severe cases, suicidal ideation.

The market includes pharmacological therapies, neuromodulation treatments, and integrated care approaches focused on improving patient outcomes. As a leading cause of global disability, MDD continues to create significant clinical and economic burden, supporting sustained demand for innovative therapies.

Key Industry Highlights:

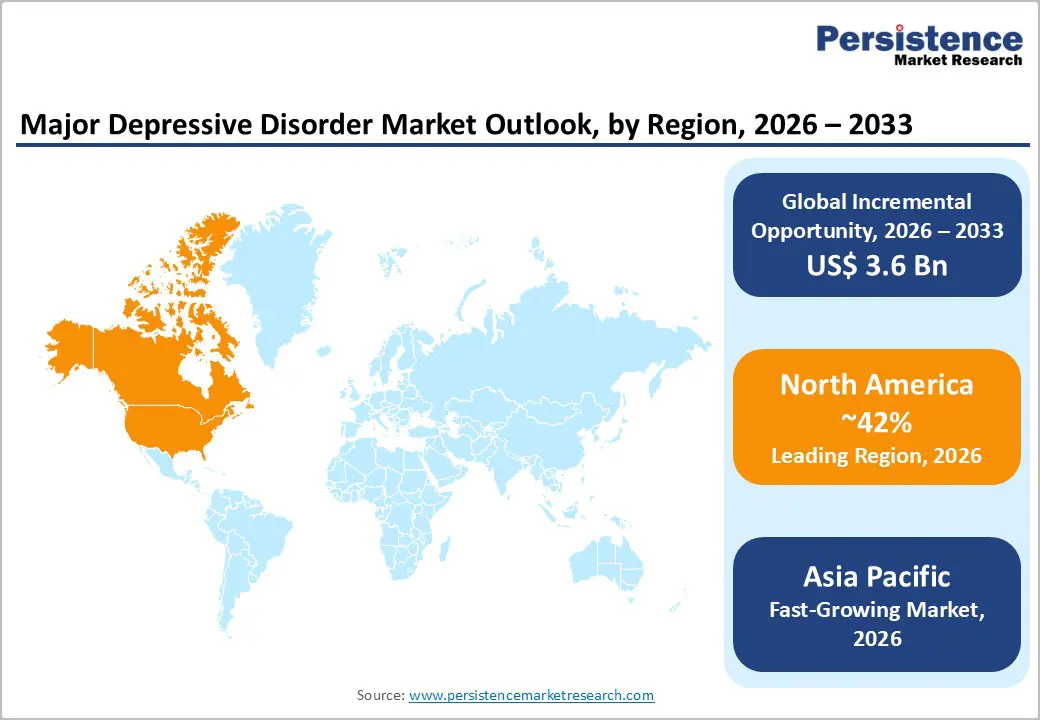

- Leading Region: North America, anticipated to account for a 42% market share in 2026, driven by the U.S. mental health treatment infrastructure, high per-capita antidepressant utilization, and the FDA approval of breakthrough MDD therapies, including SPRAVATO (esketamine).

- Fastest-growing Region: Asia Pacific, fueled by rising mental health awareness, improving access to care, and a growing patient population in China and India.

- Dominant Drug Type: Antidepressants encompassing SSRIs, SNRIs, and TCAs remain the dominant drug type, representing approximately 48% of total MDD market revenues in 2026, while Neuromodulators are the fastest-growing category at an estimated CAGR exceeding 8% through 2033.

- Leading Application: Hospitals hold the leading application share at approximately 55% of MDD market revenues in 2026, anchored by in-patient psychiatric care, TMS administration, and ketamine/esketamine infusion centers within hospital-based mental health units.

| Key Insights | Details |

|---|---|

|

Major Depressive Disorder Market Size (2026E) |

US$8.1 Bn |

|

Market Value Forecast (2033F) |

US$11.7 Bn |

|

Projected Growth CAGR (2026-2033) |

5.4% |

|

Historical Market Growth (2020-2025) |

4.8% |

DRO Analysis

Driver - Rising Global MDD Prevalence and Post-Pandemic Mental Health Crisis

The foundational growth driver for the Major Depressive Disorder Market is the substantial and accelerating global prevalence of depression, which has been dramatically amplified by the COVID-19 pandemic's unprecedented psychosocial disruption. The WHO estimated that global depression prevalence increased by approximately 25% in the first year of the COVID-19 pandemic alone, the largest single-year increase in depression incidence ever recorded, with 280 million people worldwide now living with depression as a chronic condition. The Lancet Global Mental Health Commission reported that the economic cost of untreated mental illness will reach US$16 trillion globally by 2030, with MDD representing the single largest contributor to this burden.

Critically, rising MDD prevalence is not uniformly distributed across demographics; it is disproportionately affecting younger populations. The U.S. Surgeon General's Advisory on Youth Mental Health (2021) identified a dramatic escalation in adolescent and young adult depression rates, with the Centers for Disease Control and Prevention (CDC) reporting that 29% of U.S. high school students experienced persistent sadness or hopelessness in 2021, up from 26% in 2009. This generational shift in depression epidemiology is creating a substantially larger long-term patient pool for MDD pharmacotherapy, expanding the total addressable market for antidepressants, atypical antipsychotics, adjunctive therapies, and neuromodulation approaches across the 2026–2033 forecast horizon.

The global expansion of mental health awareness campaigns including WHO's World Mental Health Day, the U.S. National Alliance on Mental Illness (NAMI) advocacy programs, and national mental health strategy frameworks in the UK (NHS Long Term Plan), EU (EU4Health Mental Health priority), and Australia (National Mental Health and Suicide Prevention Plan) is progressively reducing stigma and increasing treatment-seeking behavior among previously undiagnosed or untreated MDD populations.

Launch of Novel Mechanism Antidepressants and Breakthrough Therapy Approvals

The commercial launch of novel mechanism antidepressants represents the most powerful near-term revenue growth catalyst for the MDD Market, injecting therapeutic innovation and premium pricing into a landscape previously dominated by genericized SSRIs and SNRIs with limited commercial differentiation. The paradigm shift began with Johnson & Johnson's SPRAVATO (esketamine), the first intranasal, rapid-acting antidepressant with a novel glutamatergic mechanism, which generated approximately US$800 million in global net sales in 2023 and is growing at over 40% year-over-year, reflecting strong unmet need in the treatment-resistant depression segment.

Axsome Therapeutics' AUVELITY (dextromethorphan-bupropion HBr extended-release) received FDA approval in August 2022 as the first oral NMDA receptor antagonist antidepressant, combining rapid onset of action with a convenient oral dosing format. AUVELITY's AXS-05 program demonstrated statistically significant and clinically meaningful antidepressant efficacy within one week of treatment initiation in the GEMINI Phase III trial, a differentiated speed-of-onset profile highly valued by both patients and prescribers.

Restraint - Generic Erosion of Established Antidepressants and Pricing Pressure

The major depressive disorder market faces a structural revenue headwind from the broad genericization of the antidepressant drug class. Most of the first-line MDD treatments, including fluoxetine (Prozac), sertraline (Zoloft), escitalopram (Lexapro), venlafaxine (Effexor), and duloxetine (Cymbalta), are available as low-cost generics with negligible pricing power. Generic antidepressants account for over 80% of total antidepressant prescription volume in the U.S. (IQVIA), with average prescription costs measured in single-digit dollars per month values that generate minimal revenue contribution per patient to the branded pharmaceutical market.

This genericization dynamic compresses the overall market average selling price and creates a commercially bifurcated landscape where volume growth (driven by rising prescription rates for generic antidepressants) contributes limited revenue, while value growth depends entirely on premium-priced branded innovations in TRD, novel mechanism antidepressants, and neuromodulation therapies.

Intensifying payer scrutiny through prior authorization requirements, step therapy protocols mandating generic antidepressant trials before branded approvals, and reference pricing in European healthcare systems further constrain the commercial ramp of high-value branded MDD therapies, moderating overall market growth relative to the underlying disease burden.

High Clinical Trial Failure Rates and Placebo Response Challenge in MDD

MDD drug development is characterized by exceptionally high clinical trial attrition rates, driven in significant part by the notoriously high and variable placebo response in antidepressant clinical trials. Meta-analyses published in JAMA Psychiatry have demonstrated that the placebo response rate in MDD Phase III trials ranges from 30% to 50%, among the highest of any therapeutic area, which substantially inflates the statistical burden required to demonstrate drug-placebo separation and contributes to high Phase III failure rates. The National Institute of Mental Health's STAR*D study demonstrated that only 28% of MDD patients achieve remission with a first antidepressant trial, highlighting both the heterogeneity of the patient population and the complexity of achieving consistent clinical trial outcomes.

These clinical development challenges translate into substantial capital inefficiency for MDD drug developers. High-profile late-stage clinical failures, including Relmada Therapeutics' REL-1017 (esmethadone) failing to meet co-primary endpoints in its Phase III RELIANCE-1 trial in 2023, underscore the persistent drug development risk even for compounds with strong Phase II signals and novel mechanisms. This elevated clinical risk profile increases the cost of capital for MDD-focused development programs and can deter investment from smaller biotechnology companies without the balance sheet resilience to absorb late-stage program failures.

Opportunity- Treatment-Resistant Depression (TRD) - Addressing a High-Value Unmet Need

Treatment-Resistant Depression (TRD), conventionally defined as inadequate response to at least two adequate antidepressant trials of sufficient dose and duration, represents the single highest-value commercial opportunity within the MDD Market. Approximately 30% of MDD patients are classified as TRD, translating to an estimated 84 million patients globally who derive insufficient benefit from available first- and second-line antidepressant therapies. The clinical severity, healthcare resource intensity, and economic burden associated with TRD are disproportionately high. TRD patients generate healthcare costs estimated at 3–5 times those of treatment-responsive MDD patients (U.S. Agency for Healthcare Research and Quality), justifying premium therapy pricing and aggressive managed care investment in effective TRD solutions.

Beyond SPRAVATO (esketamine), an active pipeline of TRD-focused programs is advancing in clinical development. Neumora Therapeutics' NMRA-335140 (selective kappa opioid receptor antagonist), Vistagen Therapeutics' itruvone and PH94B nasal sprays, and multiple psychedelic-assisted therapy programs (psilocybin, MDMA-assisted therapy) are targeting the TRD population with differentiated mechanisms. The FDA's Breakthrough Therapy designation granted to multiple TRD candidates is accelerating development timelines and providing a clear regulatory pathway for this high-priority therapeutic category.

Digital Therapeutics Integration and Precision Psychiatry Biomarker Approaches

The convergence of digital health technologies, neuroscience research, and pharmacotherapy is creating a new dimension of opportunity in the MDD Market through precision psychiatry, the application of biological, genetic, imaging, and digital biomarkers to predict individual patient treatment response and enable personalized therapeutic selection. The current standard of care for MDD is characterized by empirical, trial-and-error antidepressant prescribing that results in long delays to effective treatment (average 6–12 months to achieve remission) and high rates of treatment discontinuation. Validated predictive biomarkers that guide initial treatment selection would substantially improve patient outcomes and generate significant commercial value for diagnostic-therapeutic companion products.

Prescription digital therapeutics (PDTs), software-based therapeutic interventions clinically validated for MDD treatment, represent an emerging complementary commercial opportunity. Companies including Alto Neuroscience, Freespira, and Spring Health are developing AI-powered digital mental health platforms integrated with pharmacotherapy management. The integration of cognitive behavioral therapy (CBT) digital platforms with antidepressant prescribing through collaborative care models is demonstrating additive efficacy and improved medication adherence outcomes.

Category-wise Analysis

Drug Type Insights

Antidepressants are expected to maintain their leading position in the market, accounting for over 48% of total revenue in 2026. Their dominance is driven by their role as the first-line treatment across major clinical guidelines, including those from the American Psychiatric Association (APA), National Institute for Health and Care Excellence (NICE), and World Federation of Societies of Biological Psychiatry (WFSBP).

High prescription volumes of generic formulations, combined with the sustained commercial presence of branded drugs such as escitalopram, desvenlafaxine, and levomilnacipran in select markets, further reinforce this leadership. Escitalopram (Lexapro), originally developed by Lundbeck and licensed to Forest Laboratories in the U.S., remains one of the most widely prescribed selective serotonin reuptake inhibitors (SSRIs) globally, owing to its well-established efficacy and favorable tolerability profile.

Atypical antidepressants represent the fastest-growing segment, due to their improved tolerability and innovative mechanisms of action compared to traditional SSRIs and SNRIs. Drugs such as Bupropion and Mirtazapine offer benefits such as fewer sexual side effects, reduced weight gain, and faster symptom relief.

Newer agents such as Esketamine target novel pathways, including glutamate modulation, addressing treatment-resistant depression. A key example of a novel-mechanism antidepressant is esketamine (SPRAVATO). Unlike traditional antidepressants, it works through a novel glutamate (NMDA receptor) pathway, offering a different mechanism of action.

Application Insights

Hospitals are anticipated to lead, accounting for approximately 55% of total application revenues in 2026. Hospitals' dominant position reflects their role as the primary sites for high-acuity MDD management, including inpatient psychiatric admissions, partial hospitalization programs (PHPs), and intensive outpatient programs (IOPs), as well as the administration of specialized MDD interventions requiring clinical infrastructure unavailable in outpatient settings.

Hospital-based psychiatry departments and dedicated mental health units are the exclusive sites for esketamine (SPRAVATO) administration under FDA-mandated REMS (Risk Evaluation and Mitigation Strategy) protocols, ECT administration, and ketamine infusion therapy, collectively generating significant hospital-setting MDD revenue.

Clinics represent the fastest-growing application segment, propelled by the rapid proliferation of dedicated TMS clinic networks (NeuroStar-certified centers, BrainsWay Deep TMS centers), the growing availability of SPRAVATO administration at certified outpatient psychiatric practices, and the expansion of collaborative care models integrating mental health into primary care clinics, which are driving outpatient clinical setting growth.

Telehealth-enabled psychiatric clinic models accelerated by pandemic-era regulatory relaxations on prescribing and follow-up requirements are further expanding clinic-based MDD treatment access to previously underserved patient populations.

Regional Insights

North America Major Depressive Disorder Market Trends

The North America Major Depressive Disorder (MDD) market is witnessing significant evolution, driven by rising disease prevalence, growing mental health awareness, and continuous advancements in pharmacological and therapeutic interventions. The U.S. represents the largest market contributor, supported by a well-established healthcare infrastructure, robust reimbursement frameworks, and strong pharmaceutical research and development activity.

Increasing recognition of MDD as a critical public health priority has prompted substantial government funding, expanded insurance coverage for mental health services, and growing integration of behavioral health within mainstream healthcare systems. The rising adoption of telepsychiatry and digital mental health platforms is significantly improving patient access to diagnosis and treatment, particularly across underserved and rural populations.

Pharmacological treatment remains the cornerstone of MDD management, with antidepressants including selective serotonin reuptake inhibitors and serotonin-norepinephrine reuptake inhibitors dominating prescribing patterns. However, novel treatment modalities, including esketamine nasal spray, transcranial magnetic stimulation, and psychedelic-assisted therapies, are emerging as transformative alternatives for treatment-resistant depression cases. Pipeline innovation remains robust, with numerous late-stage clinical trials targeting novel mechanisms of action.

Europe Major Depressive Disorder Market Trends

Market growth in Europe is shaped by a combination of high disease burden, the European Brain Council estimates that depression affects 44.3 million Europeans annually, making it the most prevalent neuropsychiatric disorder in the EU, alongside complex multi-payer reimbursement architectures, national health technology assessment processes, and significant variation in antidepressant prescribing practices across member states.

Germany is the leading Continental European MDD market, benefiting from high healthcare expenditure per capita, a mandatory insurance-based GKV system that provides broad pharmaceutical coverage, and a highly developed specialist psychiatry network. Germany's AMNOG process for novel antidepressant benefit assessment, recently applied to SPRAVATO and newer branded antidepressants, creates a structured but nuanced reimbursement pathway that balances innovation access with value-based pricing.

France is the second-largest European MDD market, with high antidepressant prescribing rates and significant public health investment in mental health through the national mental health strategy (Feuille de Route Santé Mentale et Psychiatrie). H. Lundbeck A/S maintains particularly strong European market positions through Brintellix (vortioxetine) and Cipralex (escitalopram), leveraging decades of CNS therapeutic expertise and established European prescriber relationships. Sweden, Denmark, the Netherlands, and Spain each represent meaningful MDD market contributors, shaped by distinct mental health system architectures and prescribing cultures.

Asia Pacific Major Depressive Disorder Market Trends

Asia Pacific is likely to be the fastest-growing region, powered by China, India, and Japan. The region's growth is driven by a convergence of rising depression prevalence (accelerated by urbanization, social media exposure, and post-pandemic mental health deterioration), rapidly improving mental health awareness and treatment-seeking behavior, strengthening healthcare system capacity for psychiatric care, and active market development by global MDD pharmaceutical companies through regional partnerships and clinical program investments.

Japan is expected to lead, characterized by high pharmaceutical expenditure, universal health insurance coverage extending to MDD pharmacotherapy, and a well-established psychiatry specialty infrastructure. Otsuka Pharmaceutical and Takeda Pharmaceutical, both headquartered in Japan, are globally significant MDD drug developers, with Otsuka's aripiprazole (Abilify) and brexpiprazole (Rexulti) generating billions in global MDD adjunctive therapy revenues. China represents the most significant growth opportunity in the Asia Pacific, with an estimated 54 million people living with depression (WHO) and a mental health infrastructure that, despite rapid expansion, still faces severe shortages of psychiatrists relative to population need.

Competitive Landscape

The global Major Depressive Disorder (MDD) market features a highly competitive landscape, including global pharmaceutical companies, CNS-focused specialists, and emerging biotech firms. Competitive strength is increasingly driven by novel mechanisms of action, treatment-resistant depression (TRD) focus, and strong specialty psychiatry commercialization capabilities.

Key strategies center on differentiating drug mechanisms, advancing TRD therapies, and strengthening specialty channel reach. Innovation is shifting beyond traditional monoaminergic drugs toward new approaches such as glutamatergic, GABAergic, neuroplasticity-based, and psychedelic therapies, with companies like Neumora Therapeutics, Vistagen, and COMPASS Pathways leading pipeline development in these areas.

Key Industry Developments:

- In November 2025, Johnson & Johnson announced that the FDA approved caplyta® (lumateperone) as an adjunctive treatment for adults with major depressive disorder. The company based the approval on phase 3 trials showing significant symptom improvement and potential for remission. It expanded Caplyta’s use beyond schizophrenia and bipolar depression, addressing unmet needs in mental health treatment.

- In August 2025, Abbott launched the Transcend clinical trial to evaluate its new deep-brain stimulation (DBS) device for treating difficult-to-treat depression. The study assessed patients with major depressive disorder who did not respond to at least two prior treatments. The company initiated the trial after receiving the FDA’s breakthrough device designation, which accelerated the review of innovative technologies for serious conditions.

Companies Covered in Major Depressive Disorder Market

- Novartis AG

- Biogen Inc

- Otsuka Pharmaceutical Co., Ltd.

- Neurocrine Biosciences Inc.

- H. Lundbeck A/S

- Takeda Pharmaceutical Company Limited

- Alkermes

- Janssen Research & Development LLC

- Intra-Cellular Therapies Inc.

- Axsome Therapeutics Inc.

- Luye Pharma Group; BioLite Inc.

- Neumora Therapeutics Inc.

- Relmada Therapeutics Inc.

- Fabre-Kramer Pharmaceuticals

- Vistagen Therapeutics Inc.

- Pfizer Inc.

- Johnson & Johnson

- Abbott Laboratories

- AbbVie Inc.

- Merck & Co., Inc.

Frequently Asked Questions

The global major depressive disorder market is projected to reach US$8.1 billion in 2026.

The major depressive disorder market is primarily driven by the rising prevalence of depression and growing awareness about mental health treatment. Introduction of novel antidepressants with improved efficacy and safety further supports market growth.

The major depressive disorder market is poised to witness a CAGR of 5.4% from 2026 to 2033.

Key opportunities in the major depressive disorder market include the development of faster-acting therapies for treatment-resistant depression, the expansion of outpatient clinic services, and growth in emerging markets through improved mental health awareness.

Key players in the major depressive disorder market include Novartis AG, Otsuka Pharmaceutical Co., Ltd., H. Lundbeck A/S, Takeda Pharmaceutical Company Limited, and Johnson & Johnson.