- Agrochemicals

- Jet Fuel Additives Market

Jet Fuel Additives Market Size, Share, and Growth Forecast, 2026 - 2033

Jet Fuel Additives Market by Additive Type (Icing Inhibitors, Antioxidants, Corrosion Inhibitors, Antiknock, Metal Deactivators), End-user (Passenger, Cargo), and Regional Analysis for 2026 - 2033

Jet Fuel Additives Market Size and Trends Analysis

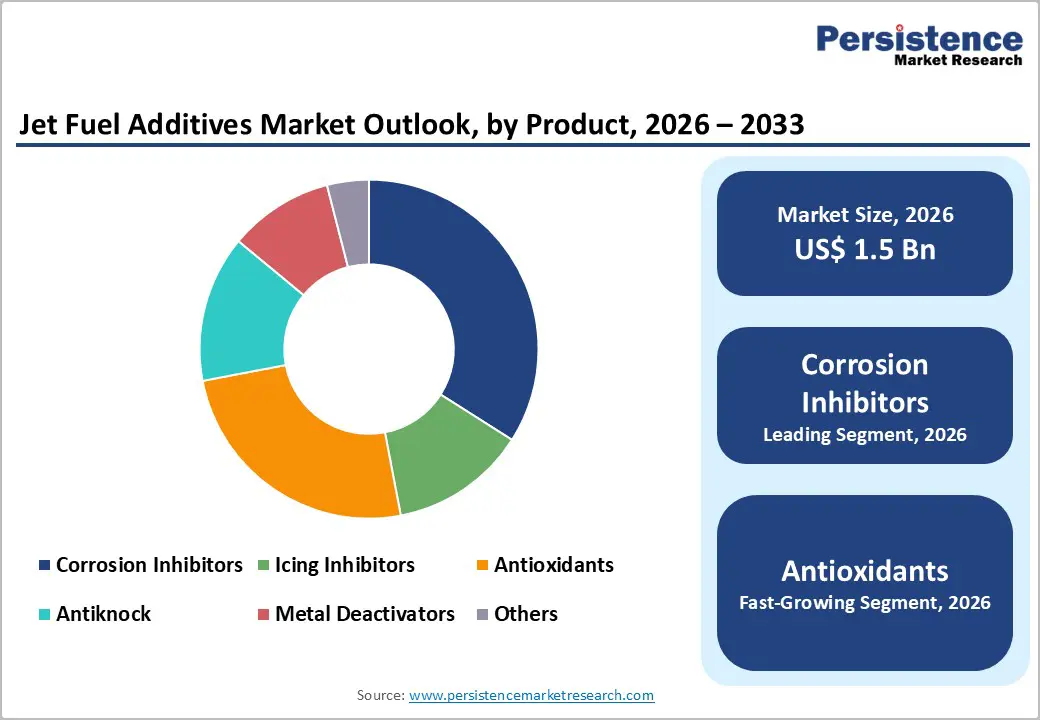

The global jet fuel additives market size is likely to be valued at US$1.5 billion in 2026 and is expected to reach US$2.2 billion by 2033, growing at a CAGR of 5.5% during the forecast period from 2026 to 2033, driven by increasing commercial air traffic, expanding cargo aviation networks, and rising demand for high-performance aviation fuels.

The market is supported by stringent international fuel quality standards such as ASTM D1655 and DEF STAN 91-91, which require the use of additives for thermal stability, corrosion protection, conductivity improvement, and icing prevention. Growing integration of sustainable aviation fuels (SAF) is accelerating demand for advanced additive formulations compatible with next-generation aircraft engines. The market is also benefiting from increasing military aviation activities and the aviation industry’s focus on reducing maintenance costs, improving engine efficiency, and ensuring operational reliability under extreme flight conditions.

Key Industry Highlights:

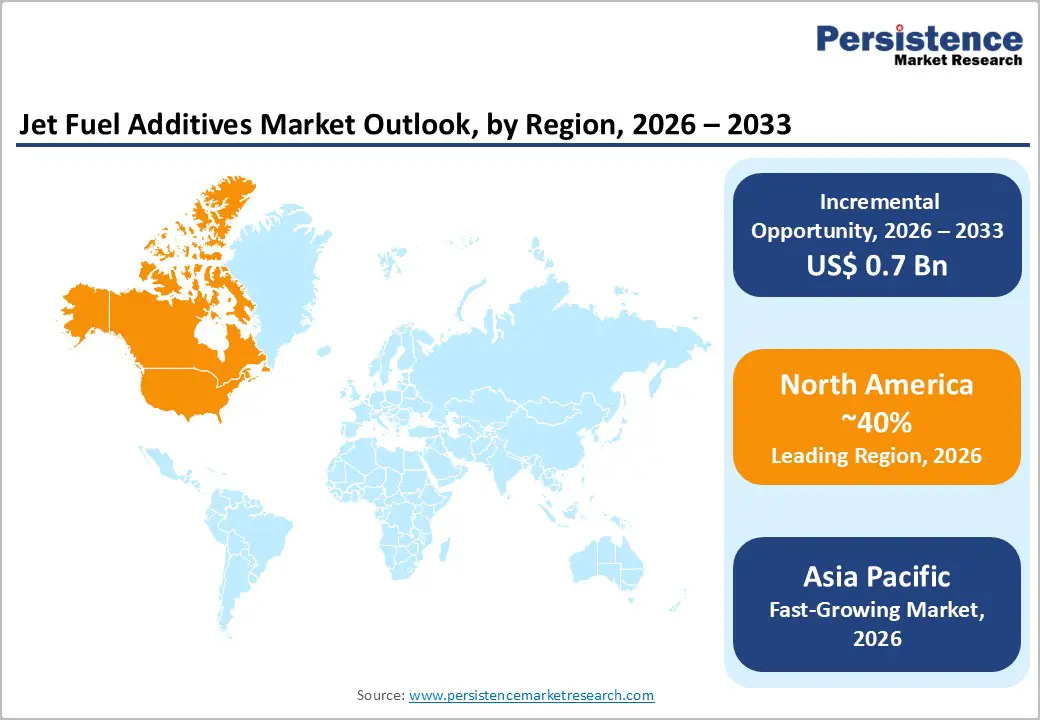

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by strong U.S. aviation activity, stringent FAA fuel regulations, expanding SAF adoption, and continuous aerospace innovation.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by rapid airline expansion, rising aircraft deliveries, growing airport infrastructure, and increasing aviation fuel consumption.

- Leading Additive Type: Corrosion inhibitors are projected to represent the leading product type in 2026, accounting for 48% of the revenue share, driven by their critical role in protecting aircraft fuel systems and maintaining fuel stability.

- Leading End-user: Passenger aircraft are anticipated to be the leading technology, accounting for over 70% of the revenue share in 2026, supported by high commercial flight activity and strict aviation safety requirements.

- Key Opportunity: The growing transition toward sustainable aviation fuels, coupled with rising aircraft modernization and expanding air travel networks, is creating significant opportunities for advanced jet fuel additives that enhance fuel efficiency, engine reliability, and low-emission aviation performance.

DRO Analysis

Driver - Rising Air Passenger and Cargo Traffic

Commercial airlines are expanding flight frequencies and long-haul routes to meet growing travel demand. Rising aircraft utilization increases the need for high-performance jet fuel additives that improve fuel stability, prevent corrosion, and ensure safe engine operation under varying climatic conditions. Cargo aviation growth driven by e-commerce and trade has also accelerated additive demand, as freight carriers require reliable fuel performance for extended operations and heavy-duty aircraft applications worldwide.

Increasing fleet modernization and aircraft deliveries are strengthening the demand for jet fuel additives across the commercial and military aviation sectors. Airlines are focusing on operational efficiency, lower maintenance costs, and improved engine durability, encouraging the use of advanced additives such as antioxidants, icing inhibitors, and metal deactivators.

Aviation authorities, including the FAA and international fuel standard organizations, continue emphasizing stringent fuel quality and safety requirements, supporting additive adoption. Growing airport infrastructure investments and rising regional connectivity are also contributing to higher jet fuel consumption.

Restraint - Volatility in Crude Oil and Petroleum-Based Feedstock Availability

Most aviation fuel additives are derived from petrochemical compounds, making manufacturers highly dependent on refinery output and raw material pricing trends. Geopolitical tensions, refinery shutdowns, transportation disruptions, and changing energy policies often create instability in feedstock availability and production costs. Such fluctuations directly affect additive pricing and profit margins for manufacturers and suppliers.

Stringent environmental regulations and the transition toward cleaner energy sources are adding additional pressure on petroleum-derived additive production. Governments and aviation organizations are increasingly promoting sustainable aviation fuel adoption and lower-emission operations, encouraging manufacturers to reformulate products and reduce dependency on traditional petrochemical feedstocks.

Opportunity - Technological Convergence with SAF and Advanced Formulations

Airlines and aviation regulators are increasingly focusing on reducing carbon emissions and improving fuel efficiency, creating demand for additives compatible with sustainable aviation fuel (SAF) blends and next-generation aviation fuels. Advanced formulations are being developed to improve thermal stability, lubricity, oxidation resistance, and fuel system cleanliness while supporting lower-emission flight operations.

As SAF production expands, additive manufacturers are investing in innovative multifunctional solutions capable of maintaining engine performance and safety standards across varying biofuel compositions. This technological convergence is expected to transform long-term market dynamics significantly.

Research and development activities are accelerating across the aviation industry to create specialized additives that enhance the operational reliability of sustainable aviation fuels under extreme flight conditions. Companies are collaborating with airlines, fuel producers, engine manufacturers, and regulatory agencies to develop products aligned with evolving American Society for Testing and Materials (ASTM) and international aviation fuel standards.

Category-wise Analysis

Additive Type Insights

Corrosion inhibitors are expected to lead the jet fuel additives market, accounting for approximately 48% of revenue in 2026, driven by their critical role in protecting aircraft fuel systems, pipelines, and storage tanks from moisture-related degradation and oxidation. These additives are extensively used across commercial aviation, military aircraft, and cargo fleets to maintain fuel quality and improve engine durability during long operational cycles. For example, the widespread use of corrosion inhibitor additives in U.S. military aviation fuel systems is where long-term storage stability and equipment protection remain operational priorities across defense aviation networks.

Antioxidants are likely to represent the fastest-growing segment, supported by increasing sustainable aviation fuel adoption and rising demand for thermal stability in modern aircraft engines. These additives help prevent oxidation, gum formation, and fuel degradation during high-temperature operations and extended storage periods. A notable example includes the increasing integration of antioxidant additives in SAF blending programs across Europe, where airlines are prioritizing fuel stability and low-emission aviation operations within commercial flight networks.

End-user Insights

Passenger aircraft are expected to lead the jet fuel additives market, accounting for approximately 70% of revenue in 2026, driven by high commercial flight frequencies, expanding airline fleets, and stringent aviation fuel safety requirements worldwide. Commercial airlines require advanced additives to maintain fuel stability, prevent icing, reduce corrosion, and improve engine efficiency during continuous long-distance operations. For example, Delta Air Lines operates large commercial fleets requiring consistent fuel quality and operational safety standards.

Cargo aviation is likely to represent the fastest-growing segment, supported by expanding e-commerce activity, international trade growth, and increasing demand for time-sensitive logistics services. Air cargo operators require high-performance fuel additives to ensure engine reliability, fuel stability, and efficient aircraft performance during long-haul freight transportation. For instance, FedEx Express utilizes advanced aviation fuel management practices across its cargo fleet to maintain reliability and long-distance operational efficiency.

Regional Insights

North America Jet Fuel Additives Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by strong commercial aviation activity, advanced aerospace infrastructure, and increasing sustainable aviation fuel integration. The region benefits from strict aviation fuel quality standards established by the FAA and ASTM, encouraging widespread use of corrosion inhibitors, antioxidants, and anti-icing additives. For example, Innospec Inc. continues expanding aviation additive technologies for fuel efficiency and thermal stability applications.

U.S. Jet Fuel Additives Market Trends

The U.S. dominates the regional market, driven by its extensive commercial airline operations and strong military aviation presence. Rising domestic air passenger traffic continues to increase jet fuel consumption across major airports and airline fleets. The country is also witnessing growing investments in sustainable aviation fuel production and blending infrastructure. Aviation companies are focusing on advanced fuel additive technologies to meet evolving FAA and ASTM standards.

Canada Jet Fuel Additives Market Trends

Canada is a significant market for jet fuel additives supported by increasing regional aviation activity and expanding cargo transportation networks. Harsh climatic conditions across several provinces increase demand for anti-icing additives and fuel stability solutions. Canadian airlines are focusing on fuel efficiency improvements and lower-emission aviation operations to align with environmental sustainability goals.

Europe Jet Fuel Additives Market Trends

Europe is likely to be a significant market for jet fuel additives in 2026, due to stringent environmental regulations, SAF adoption targets, and strong aerospace manufacturing capabilities. Airlines and aviation fuel suppliers across the region are increasingly adopting advanced additives to improve fuel efficiency, reduce emissions, and maintain operational reliability under strict European Union aviation standards. A notable example includes BASF SE, which continues to develop specialty aviation additive technologies supporting fuel performance and sustainability.

U.K. Jet Fuel Additives Market Trends

The U.K. is a significant market for jet fuel additives, supported by expanding sustainable aviation initiatives and strong international airline connectivity. The country continues investing in SAF production facilities and low-carbon aviation strategies to support long-term environmental targets. British airlines are emphasizing advanced fuel management systems and additive integration to improve aircraft efficiency and operational safety. Cargo aviation growth and international freight movement are also supporting higher additive consumption across the aviation sector.

Germany Jet Fuel Additives Market Trends

Germany dominates the regional market, driven by its strong aerospace engineering sector and advanced aviation manufacturing ecosystem. The country is actively investing in sustainable aviation fuel development and low-emission aviation technologies. German airlines are focusing on fuel optimization strategies to improve operational efficiency and reduce environmental impact. Increasing cargo transportation activity and industrial exports are driving aviation fuel demand across logistics networks.

Asia Pacific Jet Fuel Additives Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by expanding airline fleets, rising air passenger traffic, and rapid airport infrastructure development. Countries across the region are increasing investments in aviation modernization and fuel efficiency technologies to support growing domestic and international air travel demand. For example, Dorf-Ketal Chemicals India Pvt. Ltd. continues expanding specialty fuel additive solutions for aviation applications across the Asia Pacific markets.

China Jet Fuel Additives Market Trends

China dominates the regional market, driven by rapid airline expansion and continuous airport infrastructure development. Rising domestic air travel and international connectivity are significantly increasing aviation fuel consumption across the country. Chinese airlines are modernizing fleets with fuel-efficient aircraft to support long-term operational efficiency goals. The government is actively promoting sustainable aviation fuel development and aviation decarbonization strategies.

India Jet Fuel Additives Market Trends

India is a significant market for jet fuel additives, supported by rapid airline expansion, increasing regional air connectivity, and rising passenger travel demand. The country is witnessing significant investments in airport infrastructure and aviation modernization programs. Indian airlines are expanding domestic and international operations, increasing demand for fuel additives that improve operational reliability and engine efficiency.

Competitive Landscape

The global jet fuel additives market exhibits a moderately fragmented structure, driven by the presence of multinational chemical manufacturers, aviation fuel technology providers, and specialized additive formulators competing across commercial and military aviation sectors. Rising adoption of sustainable aviation fuels, stringent ASTM and DEF STAN fuel specifications, and increasing airline focus on fuel efficiency are intensifying competition across the market.

With key leaders including BASF SE, Afton Chemical Corporation, Innospec Inc., LANXESS AG, The Lubrizol Corporation, and Dorf-Ketal Chemicals, the competitive environment continues evolving through innovation-focused strategies and regional expansion initiatives. Several manufacturers are also emphasizing research and development activities to strengthen low-emission fuel technologies and improve compliance with international aviation safety standards.

Key Industry Developments:

- In September 2025, BASF SE launched its next-generation Keropur® fuel additive series designed to meet upgraded TOP TIER+™ fuel standards, supporting cleaner combustion, enhanced engine protection, and improved fuel efficiency.

- In November 2025, LanzaJet produced the world’s first commercial-scale jet fuel from ethanol at its Freedom Pines Fuels facility in Georgia, marking a breakthrough in sustainable aviation fuel (SAF) technology and low-emission aviation development.

- In August 2025, Afton Chemical Corporation launched the HiTEC® 65522 gasoline performance additive series approved for TOP TIER+™ gasoline standards, designed to improve engine cleanliness, fuel efficiency, and overall fuel system performance in advanced engine technologies.

Companies Covered in Jet Fuel Additives Market

- Afton Chemical Corporation

- BASF SE

- Cummins Filtration

- Dorf-Ketal Chemicals India Pvt., Ltd.

- Dow, Inc.

- DuPont de Nemours, Inc.

- General Electric Company

- Hammonds

- Innospec, Inc.

- Lanxess AG

- Meridian Fuels

Frequently Asked Questions

The global jet fuel additives market is projected to reach US$1.5 billion in 2026.

The jet fuel additives market is driven by rising air passenger and cargo traffic, increasing adoption of sustainable aviation fuels, and stringent aviation fuel safety and performance regulations.

The jet fuel additives market is expected to grow at a CAGR of 5.5% from 2026 to 2033.

Key market opportunities in the jet fuel additives market lie in the growing adoption of sustainable aviation fuels (SAF), advanced additive formulations, and expanding aviation infrastructure across emerging economies.

Afton Chemical Corporation, BASF SE, Cummins Filtration, and Dorf-Ketal Chemicals India Pvt., Ltd. are the leading players.