- Sensors & Controls

- Intelligent Platform Management Interface Market

Intelligent Platform Management Interface Market Size, Share, and Growth Forecast 2026 - 2033

Intelligent Platform Management Interface Market by Component Type (Hardware, Software, Services), Application (Server Management, Storage Management, Telecom Equipment Management, Data Center Management, Remote Management, Network Management), Deployment Mode (On-Premises, Cloud-Based, Hybrid), Industry (IT and Telecom, BFSI, Healthcare, Government and Public Sector, Manufacturing, Retail, Education and Research), and Regional Analysis, 2026-2033

Global Intelligent Platform Management Interface Market Size and Trend Analysis

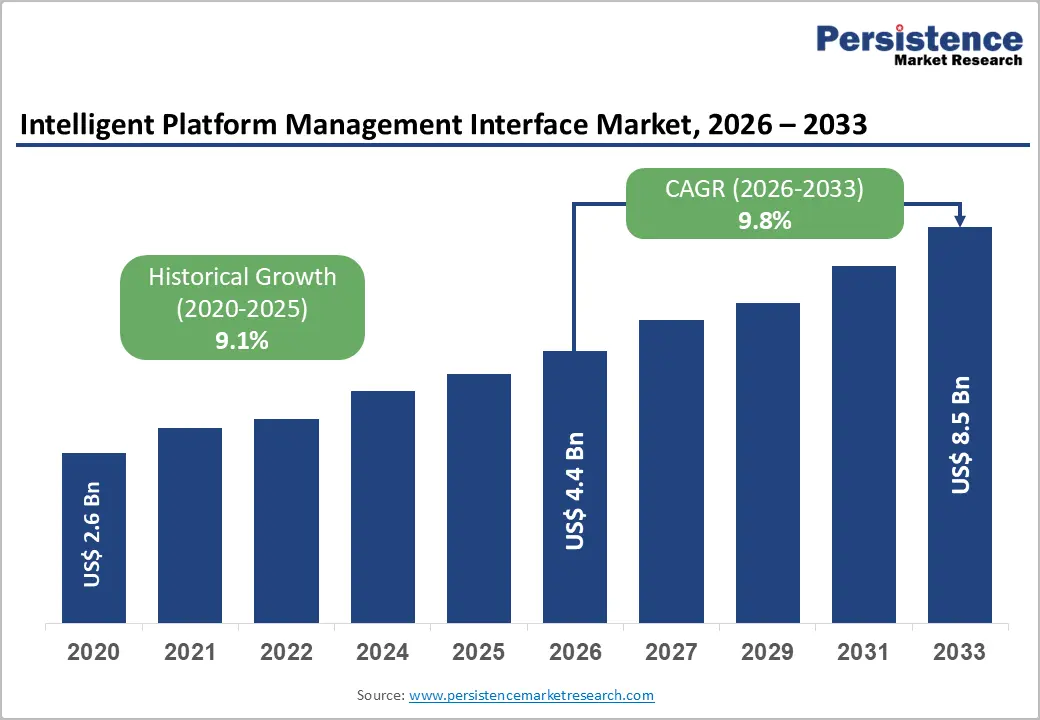

The global Intelligent Platform Management Interface (IPMI) market size is expected to reach US$ 4.4 billion in 2026 and is projected to reach US$ 8.5 billion by 2033, growing at a CAGR of 9.8% between 2026 and 2033. The demand for IPMI solutions is propelled primarily by the global build-out of hyperscale and edge data centres, the operational shift to lights-out and out-of-band server management, and the broader enterprise transition to hybrid and multi-cloud architectures.

According to the International Energy Agency (IEA), global data centre electricity consumption reached approximately 415 TWh in 2024 and is projected to nearly double by 2030, intensifying the need for remote firmware-level monitoring, thermal supervision, and energy-aware platform management. Concurrent enterprise digitalisation, 5G rollout, and AI-server densification are accelerating IPMI adoption across mission-critical infrastructure.

Key Industry Highlights:

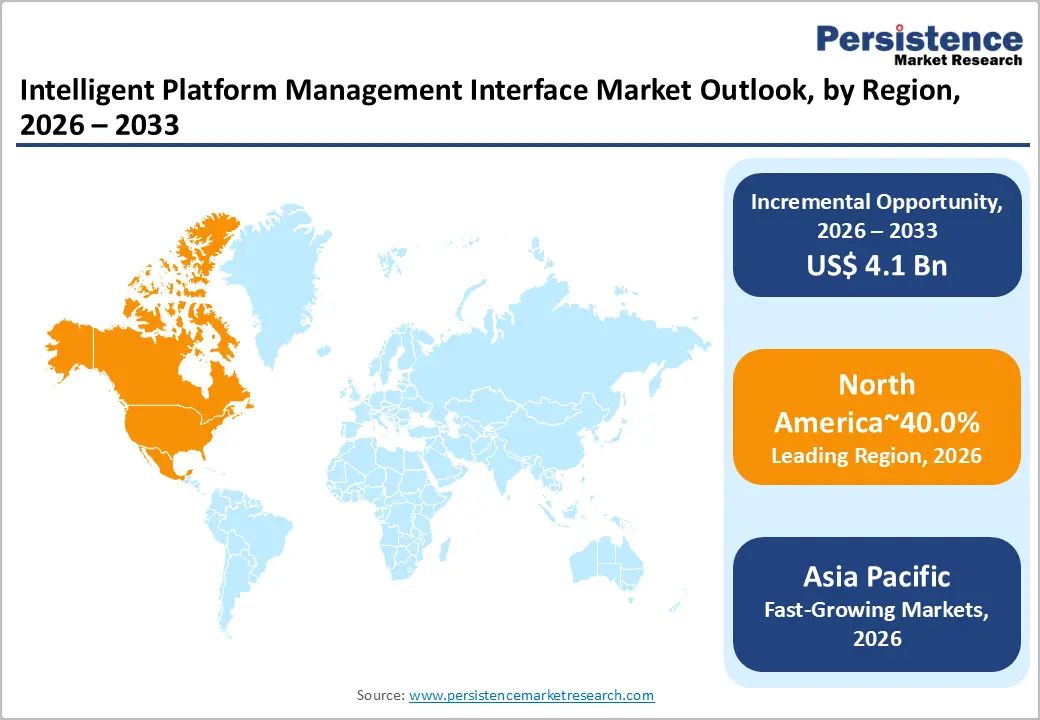

- Leading Region: North America commands approximately 40% of the global IPMI market in 2025, driven by hyperscale capex from AWS, Microsoft, Google, and Meta, plus federal AI compute initiatives across the U.S.

- Fastest Growing Region: Asia Pacific is projected to register the highest CAGR through 2033, propelled by sovereign AI programs in India and China, 5G densification, and aggressive Southeast Asian data centre expansion.

- Dominant Component: Hardware leads the component category with 52% share in 2025, anchored by Baseboard Management Controllers, sensors, and memory devices integrated into every enterprise-class server motherboard globally.

- Fast-Growing Component: Software is forecast to reach approximately at 10% CAGR between 2026 and 2033, driven by Redfish-native management platforms, AI fabric orchestration, and integrated security analytics.

- Key Opportunity: Sovereign AI compute build-outs across India, Saudi Arabia, UAE, and Brazil, alongside liquid-cooled accelerator deployments, represent a multi-billion-dollar opportunity for BMC silicon and platform management software vendors.

DRO Analysis

Drivers - Hyperscale Data Centre Build-Out and AI Workload Densification

Capital expenditure on data centre infrastructure has reached unprecedented levels, with the U.S. Energy Information Administration (EIA) noting that data centre load has become one of the fastest-expanding categories of electricity demand in the United States. Research shows that the global hyperscale operator footprint surpassed 1,100 facilities by the end of 2024, with another 130-140 in the pipeline.

AI training clusters built around accelerators such as NVIDIA H100 and GB200 systems consume 6-10x more power per rack compared to legacy compute, making firmware-level visibility, thermal sensor telemetry, and Baseboard Management Controller (BMC)-driven remediation operationally indispensable. This density-driven complexity is anchoring IPMI as a foundational layer of modern infrastructure.

Out-of-Band Management for Distributed and Edge Workloads

Enterprise operations are shifting decisively toward distributed compute models that demand secure remote administration. The International Telecommunication Union (ITU) estimates that approximately 74% of the global population will be online in 2025, up from 60% in 2020, with around 1.3 billion new users gaining connectivity, fueling latency-sensitive workloads at the network edge.

Out-of-band management via IPMI, Redfish, and successor BMC standards allows administrators to power-cycle, reflash, and diagnose servers across geographically dispersed sites without on-site intervention. With telecom operators globally densifying 5G infrastructure, IPMI-enabled remote orchestration has become essential for maintaining uptime SLAs at scale.

Restraints - Firmware-Level Security Vulnerabilities and Exploit History

Persistent BMC firmware vulnerabilities remain a significant adoption barrier. The U.S. Cybersecurity and Infrastructure Security Agency (CISA) has issued multiple advisories on IPMI authentication weaknesses, including the long-standing CVE-2013-4786 cypher-zero flaw and more recent BMC supply-chain exposures catalogued through 2024.

Organisations face elevated risk because compromised BMCs grant adversaries persistent, OS-invisible access. Compliance-sensitive sectors such as BFSI and government often delay or constrain IPMI rollouts pending hardened TPM 2.0-anchored attestation, increasing total cost of ownership and slowing replacement cycles for legacy controller silicon.

Standards Fragmentation and Migration Complexity

The technical transition from legacy IPMI 2.0 to DMTF Redfish-based management introduces integration friction. Several enterprises operate mixed fleets where older servers expose IPMI-only interfaces while newer platforms support Redfish APIs, forcing dual-stack tooling and elevating operational overhead.

The Distributed Management Task Force (DMTF) has formalised Redfish as the modern successor, yet co-existence is expected to persist through 2030. Skill gaps among administrators, the cost of refactoring monitoring scripts, and inconsistent vendor implementations continue to slow modernisation, particularly among mid-market enterprises with constrained IT budgets.

Opportunities - AI-Optimised Data Centres and Liquid-Cooled Server Management

The accelerator-driven build-out of AI infrastructure represents a structural opportunity for advanced platform management. According to the IEA, AI-specific data centre capacity is projected to more than quadruple between 2024 and 2030, with liquid-cooled and direct-to-chip systems becoming standard for racks above 50 kW. These deployments demand far richer telemetry: coolant flow sensors, leak detection, accelerator-level thermal envelopes, and granular power capping.

BMC vendors integrating support for OCP DC-MHS and Open BMC specifications, alongside NVIDIA Mission Control and similar AI fabric managers, are positioned to capture premium pricing. Platform management vendors offering Redfish-native, AI-fabric-aware controllers will benefit disproportionately from accelerator capex cycles through 2033.

Sovereign Cloud and Data Centre Expansion in Emerging Economies

National sovereign cloud initiatives and rapid Cloud Service Provider expansion across Asia, the Middle East, and Latin America create a substantial greenfield opportunity. India's government, through the MeitY IndiaAI Mission, has approved deployment of more than 34,000 GPUs for sovereign AI compute, while Saudi Arabia's HUMAIN and UAE G42 have committed multi-billion-dollar data centre programs.

Brazil, leveraging its position as Latin America's largest digital economy, is expanding regional cloud zones from operators including AWS, Microsoft Azure, and Google Cloud. Each new megawatt of installed compute capacity translates directly into demand for Baseboard Management Controllers, sensor arrays, and management software licenses, presenting a durable revenue pocket for IPMI vendors.

Category-wise Analysis

Component Type Insights

The hardware segment dominates the global market with an estimated 52% revenue share in 2026, anchored by Baseboard Management Controllers (BMCs), thermal and voltage sensors, and dedicated memory devices embedded within every enterprise-grade server motherboard. According to the Open Compute Project (OCP), BMC silicon is now a mandatory component of the DC-MHS modular hardware specification adopted by hyperscalers.

With global server unit shipments tracked by IDC approaching 14 million units annually and AI-server ASPs rising sharply, hardware revenue scales directly with infrastructure investment. Vendors such as ASPEED Technology, which holds an estimated 70%+ share of standalone BMC silicon, alongside Nuvoton, anchor this segment, making hardware the structural backbone of the IPMI ecosystem.

Application Insights

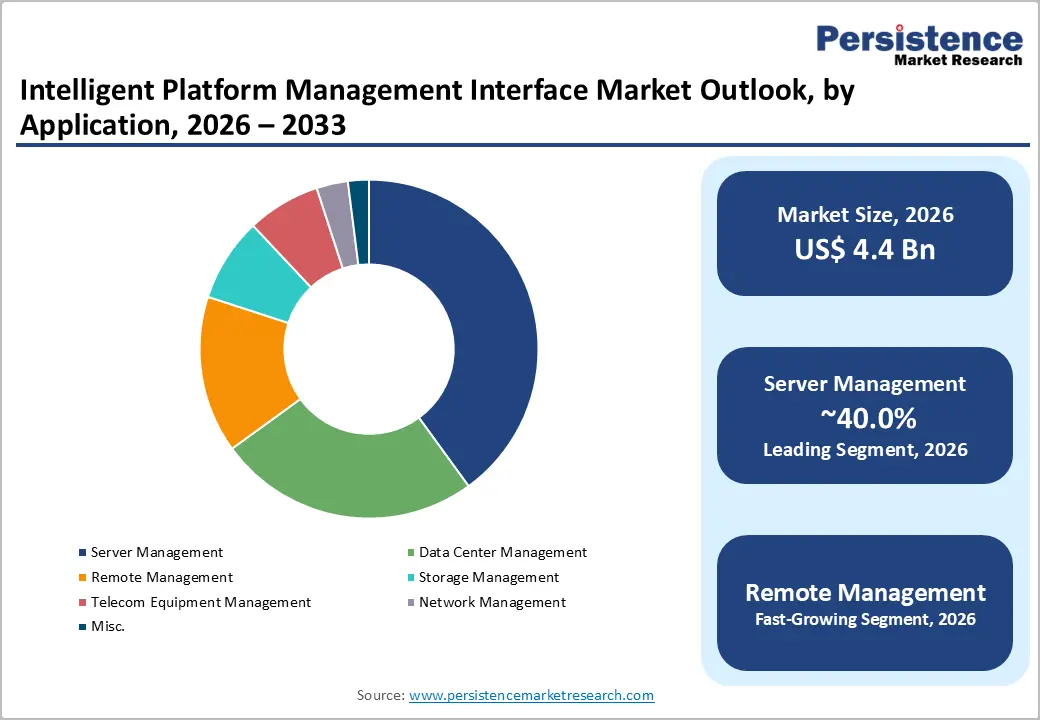

Server management leads the application landscape with approximately 38% share in 2026, driven by the sheer volume of rack, blade, and tower server deployments across enterprise and cloud environments. Rack servers in particular dominate within this category, as hyperscale and colocation operators standardise on OCP-compliant 1U and 2U form factors.

The Uptime Institute's 2024 Global Data Centre Survey reported that more than 60% of operators rate remote server management as "mission critical," with average rack densities climbing past 8 kW and AI racks exceeding 50 kW. IPMI's role in BIOS/firmware updates, KVM-over-IP, and power capping makes server management the operational backbone for both legacy and modern compute estates worldwide.

Industry Insights

Cloud service providers and data centres represent the leading end-use vertical with approximately 34% market share in 2025, reflecting the concentration of compute capacity within hyperscalers and colocation operators. The IEA estimates global data center electricity consumption at around 415 TWh in 2024, with operators including AWS, Microsoft Azure, Google Cloud, Oracle Cloud, and Meta collectively operating millions of servers requiring continuous platform-level supervision.

According to research, hyperscale capex exceeded US$ 280 billion in 2024, with a substantial portion flowing into BMC-equipped accelerator infrastructure. The IT and Telecom sector follows closely, supported by 5G core densification and the ITU-tracked expansion of nearly 6 billion internet users globally, anchoring the segment's structural dominance.

Regional Insights

North America Intelligent Platform Management Interface Market Trends and Insights

North America holds a share of 40% in 2025, is the leading position in the global market, anchored by the highest concentration of hyperscale data centers, AI training clusters, and federal compute modernisation initiatives globally.

The region is home to top BMC-equipped server OEMs and dominant cloud operators, with the U.S. Department of Energy and Department of Defence directing significant capital toward sovereign AI compute. North America holds a share of 40% in 2025, driven by sustained hyperscale capex and accelerator adoption.

U.S. Intelligent Platform Management Interface Market Size

The U.S. Intelligent Platform Management Interface market is valued at approximately US$ 1,408.0 Million in 2025, propelled by record-setting hyperscale data center construction across Northern Virginia, Dallas, and Phoenix. JLL reports U.S. data center inventory crossed 40 GW in 2024, with AWS, Microsoft, Meta, and Google committing collectively over US$ 200 billion in 2024-2025 infrastructure capex, alongside CHIPS Act-funded domestic server manufacturing expansion.

Europe Intelligent Platform Management Interface Market Trends and Insights

Europe represents a mature, regulation-driven environment shaped by stringent data sovereignty requirements under GDPR and the EU Data Act. The region's information and communication services sector employs nearly 7.2 million people and generated €667 billion in value added in 2022, anchoring sustained demand for managed compute infrastructure. Europe holds a share of 20% in 2025, supported by sovereign cloud programs such as Gaia-X and rising green data center investment.

Germany Intelligent Platform Management Interface Market Size

The Germany Intelligent Platform Management Interface market is valued at approximately US$ 224.0 Million in 2025, driven by Frankfurt's position as Europe's largest data center hub by installed capacity, Industrie 4.0 manufacturing automation, and the country's contribution of over 22% of EU information and communication services value added. Sovereign cloud demand and automotive OEM edge-computing deployments further reinforce Germany's IPMI consumption base.

U.K. Intelligent Platform Management Interface Market Size

The U.K. Intelligent Platform Management Interface market is valued at approximately US$ 128.0 Million in 2025, supported by London's status as a top-five global financial center and the city's ranking as Europe's second-largest data center market by capacity. Demand is reinforced by the Bank of England's operational resilience framework and BFSI core banking modernization across institutions including HSBC, Barclays, and Lloyds.

Asia Pacific Intelligent Platform Management Interface Market Trends and Insights

Asia Pacific is the fastest-evolving regional IPMI market, propelled by rapid hyperscale build-out across China, India, Japan, Singapore, and Australia. The region benefits from massive internet user expansion tracked by the ITU, sovereign AI compute initiatives, and aggressive 5G densification by operators such as China Mobile, NTT Docomo, and Reliance Jio. Asia Pacific holds a share of 32.0% in 2025, with strong momentum from sovereign GPU programs and emerging data center hubs.

China Intelligent Platform Management Interface Market Size

The China Intelligent Platform Management Interface market is valued at approximately US$ 742.4 Million in 2025, anchored by the Eastern Data, Western Computing national initiative, domestic AI accelerator programs from Huawei, Alibaba, and Tencent, and the MIIT-led expansion of computing power to over 246 EFLOPS by year-end 2024, making China the second-largest national compute base globally after the United States.

India Intelligent Platform Management Interface Market Size

The India Intelligent Platform Management Interface market is valued at approximately US$ 179.2 Million in 2025, driven by the IndiaAI Mission's sanctioned deployment of 34,000+ GPUs, India's position as the world's second-largest telecom market with 1.21 billion subscribers, and 979 million internet users as of June 2025, alongside large-scale data center investments by Reliance, Adani, and Yotta.

Competitive Landscape

The global intelligent platform management interface market exhibits a moderately consolidated structure at the silicon layer and a fragmented profile at the software and services layers. Standalone BMC silicon is dominated by ASPEED Technology, which holds an estimated 70%+ share of merchant BMCs, alongside Nuvoton Technology.

At the platform level, server OEMs, including Dell Technologies, Hewlett Packard Enterprise, Lenovo, Supermicro, Cisco, and Inspur integrate proprietary management stacks atop standardized BMC hardware. Strategic priorities include DMTF Redfish API adoption, integration with Open BMC, hardened firmware attestation via TPM 2.0, and AI-fabric management interoperability. Differentiation increasingly centres on security posture, telemetry granularity, and Redfish-native ecosystem extensibility.

Key Developments:

- March 2025, ASPEED Technology announced sampling of its next-generation AST2700 BMC, supporting PCIe Gen5, multi-host management, and enhanced security primitives for AI server platforms.

- March, 2025, Supermicro Inc., a leading provider of AI, cloud, and edge server infrastructure solutions, announced the launch of a new generation of compact edge and embedded server systems optimized for real-time AI inferencing, telecom workloads, and distributed computing environments. These systems are built on Intel Xeon 6 SoC processors and are designed to support high-density computing environments where intelligent platform management capabilities are essential for monitoring, diagnostics, and remote system control.

Companies Covered in Intelligent Platform Management Interface Market

- Intel Corporation

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Super Micro Computer Inc.

- Cisco Systems Inc.

- International Business Machines Corporation

- Fujitsu Limited

- NEC Corporation

- Oracle Corporation

- Huawei Technologies Co Ltd

- Lenovo Group Limited

- Inspur Group Co Ltd

- Microsoft Corporation

- Arm Holdings plc

- Emerson (including Vertiv heritage)

Frequently Asked Questions

The global Intelligent Platform Management Interface market is expected to be valued at approximately US$ 4.4 billion in 2026, with steady expansion projected through 2033 at a CAGR of 9.8%.

Demand is driven by hyperscale and AI data center build-out, with IEA noting global data center electricity consumption reached 415 TWh in 2024, alongside 5G densification and out-of-band server management requirements.

North America leads the global IPMI market with approximately 40% share in 2025, anchored by U.S. hyperscale capex, federal AI compute initiatives, and the world's largest installed base of enterprise servers.

The largest opportunity lies in AI-optimized, liquid-cooled data center deployments and sovereign cloud programs across India, Saudi Arabia, UAE, and Brazil, requiring advanced BMC silicon and Redfish-native platform management software.

Leading participants include Intel Corporation, AMD, Dell Technologies, Hewlett Packard Enterprise, Lenovo, Supermicro, Cisco Systems, Inspur, Fujitsu, and American Megatrends International.