- Sensors & Controls

- Automotive Crash Sensor Market

Automotive Crash Sensor Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Crash Sensor Market by Product Type (Accelerometers, Pressure Sensors, Gyroscopes, Acoustic Sensors), Application (Airbag Systems, Active Safety Systems), Vehicle Type (Hatchback/Sedan, SUVs, LCVs, HCVs), Placement (Front Bumper, Side Doors, Roof and Pillars, Rear Bumper), and Regional Analysis for 2026 - 2033

Automotive Crash Sensor Market Size and Trend Analysis

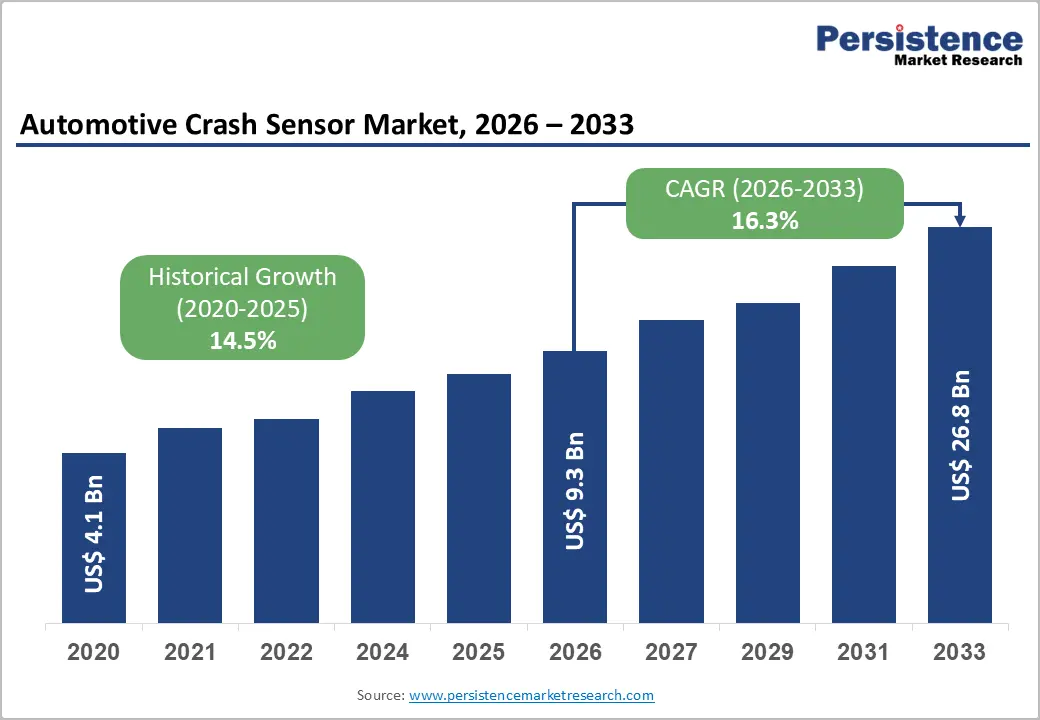

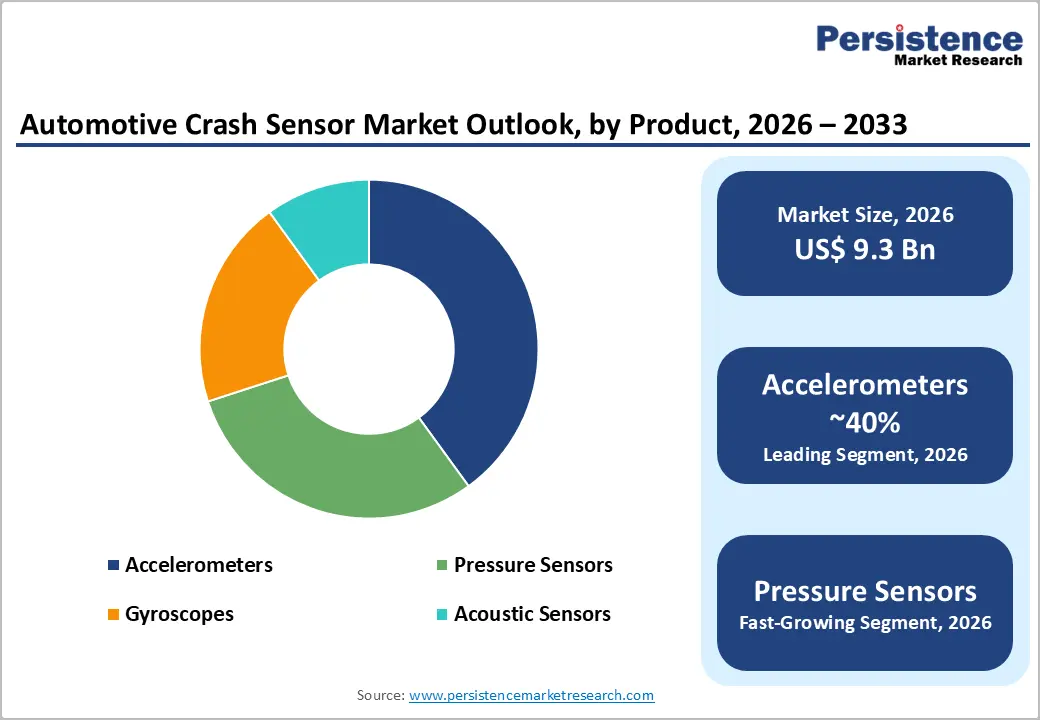

The global Automotive Crash Sensor market size is valued at US$ 9.3 Bn in 2026 and is projected to reach US$ 26.8 Bn by 2033, growing at a CAGR of 16.3% between 2026 and 2033.

Exceptional growth is anchored by three converging imperatives: the mandatory deployment of advanced sensor-dependent safety architectures under FMVSS No. 127 (AEB standard effective September 2029), the expansion of Euro NCAP protocols, and the proliferation of electric and autonomous vehicles that demand higher sensor counts per platform.

The integration of Micro-Electro-Mechanical Systems (MEMS) technology into crash sensor architectures has driven rapid miniaturization and cost reduction, enabling adoption across all vehicle segments from entry-level hatchbacks to heavy commercial vehicles, further accelerating the market's double-digit compounded expansion trajectory.

Key Market Highlights

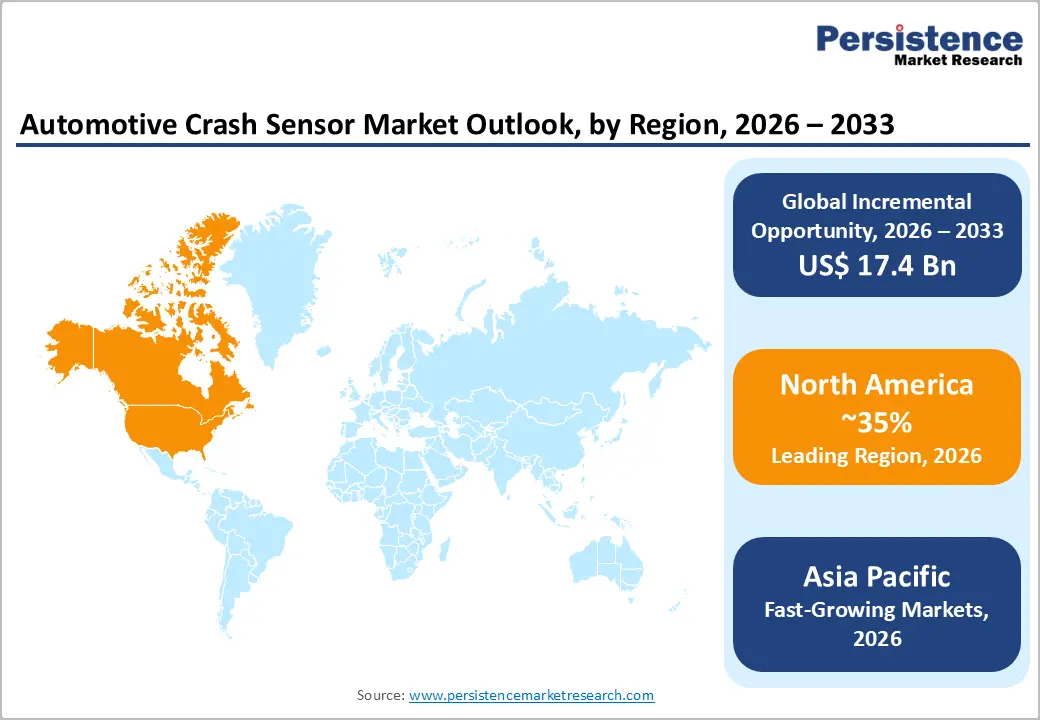

- Leading Region: North America leads the global market, driven by NHTSA's FMVSS No. 127 AEB mandate (effective 2029), a mature regulatory framework, and robust innovation by leading suppliers including Bosch, Continental, and Honeywell International.

- Fastest Growing Region: Asia Pacific is the fastest growing region, propelled by China's C-NCAP safety mandates, India's Bharat NCAP adoption, accelerating EV production by BYD, NIO, and Geely, and expanding localization of MEMS sensor manufacturing across China and Japan.

- Dominant Segment: Accelerometers dominate the Product Type segment with approximately 38% market share, anchored by their foundational role in airbag deployment, electronic stability control, and ADAS inputs supported by Bosch's world-leading MEMS manufacturing expertise and scale.

- Fastest Growing Segment: EV-specific crash sensor architectures are the fastest growing segment, driven by the 35% annual growth in global EV sales and the unique requirement for battery isolation crash detection, creating high-value content opportunities for specialized sensor manufacturers.

- Key Market Opportunity: Key market opportunity lies in AI-integrated sensor fusion and predictive pre-crash activation technologies, as Euro NCAP 2030 protocols and FMVSS No. 127 reward advanced predictive safety features, enabling suppliers to command premium platform pricing.

| Key Insights | Details |

|---|---|

|

Automotive Crash Sensor Market Size (2026E) |

US$ 9.3 Billion |

|

Market Value Forecast (2033F) |

US$ 26.8 Billion |

|

Projected Growth CAGR (2026–2033) |

16.3% |

|

Historical Market Growth (2020–2025) |

14.5% |

DRO Analysis

Drivers - Binding Global Safety Regulations Mandating Multi-Sensor Crash Detection Systems

Regulatory imperatives are the single most powerful demand accelerator for automotive crash sensors. In May 2024, the U.S. National Highway Traffic Safety Administration (NHTSA) finalised Federal Motor Vehicle Safety Standard (FMVSS) No. 127, requiring automatic emergency braking (AEB) including pedestrian AEB on all new passenger cars, SUVs, and light trucks by September 1, 2029. NHTSA projects this mandate will save at least 360 lives and prevent 24,000 injuries annually.

Simultaneously, Euro NCAP's evolving crash protection protocols including dedicated side-impact and frontal collision test enhancements compel OEMs to deploy multi-zone accelerometer, pressure sensor, and gyroscope arrays. These compliance demands structurally elevate sensor content per vehicle and expand the addressable crash sensor market across all global regions.

Accelerating ADAS and Electric Vehicle Adoption Driving Per-Vehicle Sensor Content Growth

The rapid proliferation of Advanced Driver Assistance Systems (ADAS) and battery electric vehicles (BEVs) is generating a step-change increase in per-vehicle crash sensor demand. Modern vehicles require crash sensors not only for airbag deployment but also as core inputs to active safety architectures covering lane-keeping assist, automatic emergency braking, and rollover detection.

Bosch the world's leading supplier of automotive MEMS sensors has manufactured over 23 billion MEMS sensors to date, with every modern automobile equipped with more than 50 MEMS sensors. Electric vehicles create additional demand for specialised crash sensors to protect high-voltage battery packs and automatically isolate circuits during severe impacts. The International Energy Agency (IEA) reported that global electric car sales surpassed 14 million units in 2023a 35% year-on-year increase directly amplifying demand for EV-specific crash sensing solutions.

Restraints - High Integration Complexity and System Calibration Burdens

Despite robust demand tailwinds, automotive crash sensor integration presents significant engineering challenges. Ensuring seamless compatibility between sensors, electronic control units (ECUs), and restraint systems while maintaining millisecond-level response times creates complex calibration burdens for OEMs and Tier 1 suppliers.

Compliance with ISO 26262 Functional Safety standards mandates rigorous Automotive Safety Integrity Level (ASIL B or higher) certification throughout the entire sensor development lifecycle, significantly extending qualification timelines and increasing development costs. These barriers disproportionately impact smaller suppliers seeking to enter the market.

Raw Material and Semiconductor Supply Constraints Compressing Margins

Automotive crash sensors depend critically on MEMS wafers, application-specific integrated circuits (ASICs), and high-reliability microcontroller components subject to persistent semiconductor supply bottlenecks. The lengthy OEM validation and qualification cycles for automotive-grade MEMS components often spanning 18–24 months, restrict supply-chain agility.

Global MEMS output reached 34 billion units in 2024, though expanding 300 mm foundry capacity is progressively easing price pressure. Localisation requirements across key markets such as China and India further complicate global supply chain management for sensor manufacturers.

Opportunities - EV-Specific Crash Sensor Architectures as a High-Value Emerging Revenue Stream

The structural transition to battery electric vehicles creates a transformative opportunity for crash sensor manufacturers to develop and commercialise EV-specific sensor architectures. Unlike conventional ICE vehicles, EVs require crash sensors that simultaneously detect impact severity, trigger occupant protection systems, and execute high-voltage battery pack isolation within milliseconds to prevent post-collision thermal runaway. This dual-function requirement elevates the engineering complexity and per-unit value of crash sensor modules in EV platforms.

In September 2025, Denso Corporation unveiled a new line of crash sensors specifically designed to improve vehicle response times during accidents. With global EV sales growing at 35% annually per IEA data and OEMs such as Toyota, Hyundai, BYD, and NIO scaling EV production volumes, suppliers capable of delivering certified EV-grade crash sensor systems stand to capture significant long-term platform contracts.

AI-Integrated Sensor Fusion and Pre-Crash Predictive Activation Technologies

The evolution from reactive to predictive crash sensing represents a significant technology and revenue opportunity. Emerging sensor fusion platforms integrating accelerometers, pressure sensors, gyroscopes, and acoustic sensors into unified safety domain controllers enable pre-crash activation of occupant protection systems before physical impact, rather than merely responding to it.

In June 2024, Robert Bosch GmbH and Microsoft announced a partnership to utilise generative AI in enhancing automated driving and safety systems. Similarly, in March 2024, Continental AG launched a sensor fusion platform integrating multiple sensor modalities for enhanced safety systems. Companies leading in AI-driven crash sensing and multimodal integration will command higher average selling prices and secure long-term OEM platform wins, particularly under Euro NCAP 2030 protocols that reward advanced predictive safety features.

Category-wise Analysis

Product Type Insights

Accelerometers are the dominant product type in the automotive crash sensor market, accounting for approximately 38% of market revenue. Their pre-eminence stems from their foundational role in detecting vehicle deceleration the primary physical signal triggering airbag deployment and their versatility across multiple active safety applications, including electronic stability control, rollover detection, and ADAS inputs.

Bosch, which produced MEMS technology at scale from 1995, has reduced sensor size by a factor of 50 and power consumption by a factor of 100 over the past three decades, enabling accelerometers to be embedded in all vehicle segments cost-effectively. Inertial sensors, which include accelerometers and gyroscopes, collectively represented 28.13% of total automotive sensor revenue in 2024, underpinning their indispensability in modern vehicle safety and dynamics management architectures.

Application Insights

Airbag systems constitute the leading application segment, representing approximately 55% of the global automotive crash sensor market. Airbag deployment relies exclusively on high-precision crash sensors to detect collision severity within milliseconds and trigger multi-stage inflator activation. The global proliferation of multi-airbag configurations driven by Euro NCAP, NHTSA, and regional NCAP testing protocols has structurally elevated per-vehicle airbag counts. China's C-NCAP and India's Bharat NCAP safety ratings are accelerating the adoption of six-to-eight airbag configurations even in mid-range passenger cars. In February 2025, ZF LIFETEC introduced the Active Heel Airbag, requiring dedicated sensor inputs for foot-injury protection illustrating the deepening per-vehicle sensor content expansion within the airbag application segment.

Vehicle Type Insights

The Hatchback/Sedan segment is the leading vehicle type in the automotive crash sensor market, commanding approximately 45% of market revenue. The sheer production volume of passenger cars globally particularly across Asia Pacific, Europe, and North America anchors the segment's dominance. High-volume platforms from Toyota, Volkswagen, Hyundai, Honda, and Ford drive substantial OEM procurement of crash sensor assemblies.

Stricter crash-test requirements under Euro NCAP and NHTSA FMVSS No. 127 further elevate per-vehicle sensor content in this segment. The growing adoption of hybrid sedan platforms requiring both conventional occupant protection sensors and battery isolation crash detection reinforces the long-term revenue primacy of the hatchback/sedan segment.

Placement Insights

Front Bumper placement represents the leading segment in the placement category, accounting for approximately 40% of market revenue. Frontal crash sensors are the most critical and highest-volume placement, directly linked to AEB, forward collision warning, and multi-stage front airbag deployment systems.

The NHTSA's AEB mandate under FMVSS No. 127requiring detection of lead-vehicle collisions at speeds up to 90 mph and pedestrian impacts at up to 45 mph specifically relies on front-mounted sensor arrays integrating accelerometers, pressure sensors, and acoustic sensors. The Insurance Institute for Highway Safety (IIHS) data demonstrates that AEB reduces front-to-rear crashes by 50%, underscoring the safety-critical role of front bumper-placed sensors and ensuring their ongoing dominant revenue contribution.

Regional Analysis

North America Automotive Crash Sensor Market Insights

North America leads the global automotive crash sensor market in regulatory enforcement and technological innovation. The landmark NHTSA FMVSS No. 127 standard finalised in May 2024 and requiring AEB on all new U.S. passenger cars and light trucks by September 2029represents the most consequential regulatory driver in the region. The rule is projected to save over 360 lives and prevent 24,000 injuries annually, creating a structurally expanded, non-negotiable demand base for crash sensors across the entire U.S. new vehicle production pipeline.

The U.S. market benefits from a dense innovation ecosystem anchored by global sensor leaders. In January 2024, Bosch announced a new generation of crash sensors with improved accuracy and reduced power consumption. The National Highway Traffic Safety Administration (NHTSA)'s Bipartisan Infrastructure Law further mandates AEB for heavy vehicles, with NHTSA and FMCSA projecting that heavy-vehicle AEB rules will prevent 19,118 crashes and save 155 lives annually. Canada's alignment with U.S. safety protocols further reinforces North America's position as a premium-value crash sensor demand region.

Asia Pacific Automotive Crash Sensor Market Insights

Asia Pacific is the fastest growing region in the automotive crash sensor market, driven by the convergence of rapidly expanding vehicle production, tightening national NCAP regimes, and accelerating EV adoption. China leads regional growth as proactive C-NCAP safety ratings and government mandates for multi-airbag configurations push local brands including BYD, Geely, and NIO to adopt six-to-eight airbag systems across mid-range models significantly expanding per-vehicle crash sensor demand.

In India, the introduction of Bharat NCAP has catalysed rapid safety feature adoption. At SIAT 2026, Tenneco Inc. showcased a BS-VII ready emission and sensor system, illustrating the convergence of emissions and crash-sensing compliance demands in the market. Japan contributes advanced MEMS sensor manufacturing expertise through Denso Corporation and Mitsubishi Electric Corporation.

Europe Automotive Crash Sensor Market Insights

Europe is a leading innovation hub for automotive crash sensor technology, shaped by harmonised regulatory frameworks and premium OEM demand. Euro NCAP's continuously updated crash protection protocols, including Euro NCAP 2025 side-impact v1.1 requirements drive sustained OEM investment in side-door, roof, pillar, and rear-bumper sensor upgrades. The European Union's General Safety Regulation, which made multiple ADAS systems mandatory for new vehicle approvals from July 2022, has elevated sensor fitment rates across all European OEM platforms.

Germany remains the regional technology leader, hosting Robert Bosch GmbH, Continental AG, and ZF Friedrichshafen (TRW Automotive). In March 2024, Continental AG launched an integrated sensor fusion platform combining multiple modalities for advanced safety applications. France, the U.K., and Spain reinforce regional demand through fleet renewal programmes and urban low-emission zone mandates.

Competitive Landscape

The global automotive crash sensor market exhibits a moderately consolidated structure, with a small number of multinational Tier 1 suppliers primarily Bosch Mobility Solutions, Continental AG, ZF Friedrichshafen (TRW Automotive), and Denso Corporation commanding significant OEM platform relationships.

Key differentiators include MEMS sensor expertise, ISO 26262 functional safety certification, and sensor fusion software capability. Leading companies pursue expansion through R&D partnerships exemplified by Bosch and Microsoft's AI integration alliance and geographic footprint growth in Asia Pacific. Emerging business model trends include zonal safety domain controller architectures and software-defined sensor platforms, enabling OEMs to upgrade sensing capabilities via over-the-air updates.

Key Developments:

- In March 2025, Zoox began commercial robotaxi operations in Las Vegas using purpose-built vehicles with bi-directional sensor arrays, eliminating the need for a human safety driver and reducing per-mile operating costs by an estimated 30% compared to retrofitted platforms.

- In March 2025, Hesai Technology announced a USD 150 million expansion of its solid-state LiDAR production facility in Shanghai, targeting annual capacity of 1 million units by 2027 to meet demand from Chinese OEMs and autonomous-vehicle developers. The investment includes automated assembly lines and in-house production of VCSEL arrays, reducing per-unit costs below USD 400 and positioning Hesai to compete with incumbent radar suppliers on price.

Companies Covered in Automotive Crash Sensor Market

- Bosch Mobility Solutions

- TRW Automotive (ZF Friedrichshafen)

- Denso Corporation

- Continental AG

- Honeywell International Inc.

- Visteon Corporation

- Joyson Safety Systems

- Mitsubishi Electric Corporation

- NXP Semiconductors

- InvenSense (TDK Corporation)

- Valeo

- Kistler Group

Frequently Asked Questions

The global Automotive Crash Sensor market is valued at US$ 9.3 Bn in 2026 and is projected to reach US$ 26.8 Bn by 2033, growing at a CAGR of 16.3% during 2026–2033.

The primary drivers are binding global safety regulations including NHTSA's FMVSS No. 127 (AEB mandatory by September 2029) and evolving Euro NCAP crash protocols combined with the rapid proliferation of electric vehicles requiring EV-specific crash sensors for battery protection, and the integration of ADAS architectures that demand higher per-vehicle sensor counts.

Accelerometers lead the product type segment, accounting for approximately 38% of market revenue. Their dominance is driven by their foundational role in detecting vehicle deceleration for airbag deployment, their integration into ADAS stacks, and their scalability across all vehicle segments supported by Bosch's industry-leading MEMS manufacturing capability.

North America leads the global Automotive Crash Sensor market, anchored by the U.S.'s FMVSS No. 127 mandate, the presence of global sensor innovators, and a mature OEM ecosystem. NHTSA projects the AEB standard will save over 360 lives annually, reinforcing North America's structural dominance as a high-compliance, premium-value crash sensor demand region.

Leading companies operating in the global Automotive Crash Sensor market include Bosch Mobility Solutions, Continental AG, Denso Corporation, TRW Automotive (ZF Friedrichshafen), Honeywell International Inc., NXP Semiconductors, InvenSense (TDK Corporation), Valeo, Joyson Safety Systems, Mitsubishi Electric Corporation, Visteon Corporation, and Kistler Group.