- Healthcare Services

- Injection Lipolysis Market

Injection Lipolysis Market Size, Share and Growth Forecast, 2026 - 2033

Injection Lipolysis Market by Technology (Deoxycholic Acid, Phosphatidylcholine, Combination Therapies), Clinical Application (Body Contouring, Facial Contouring, Cellulite Reduction), Service Providers (Hospitals, Dermatology & Skin Clinics, Plastic Surgery Clinics, Aesthetic Specialty Clinics), and Regional Analysis for 2026 - 2033

Injection Lipolysis Market Share and Trends Analysis

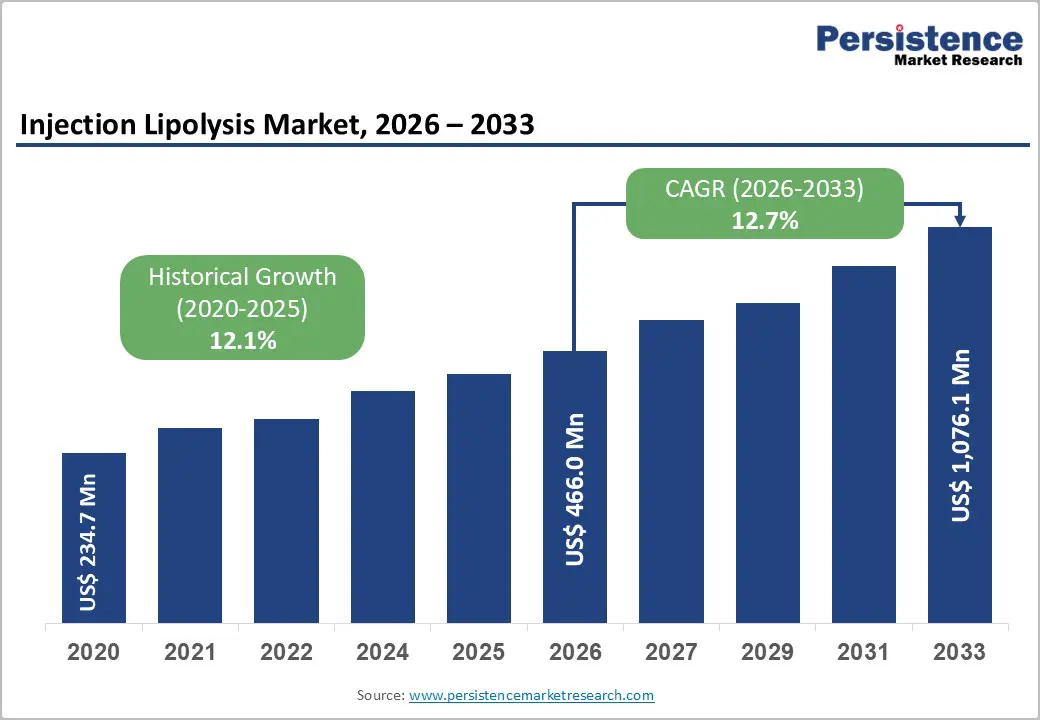

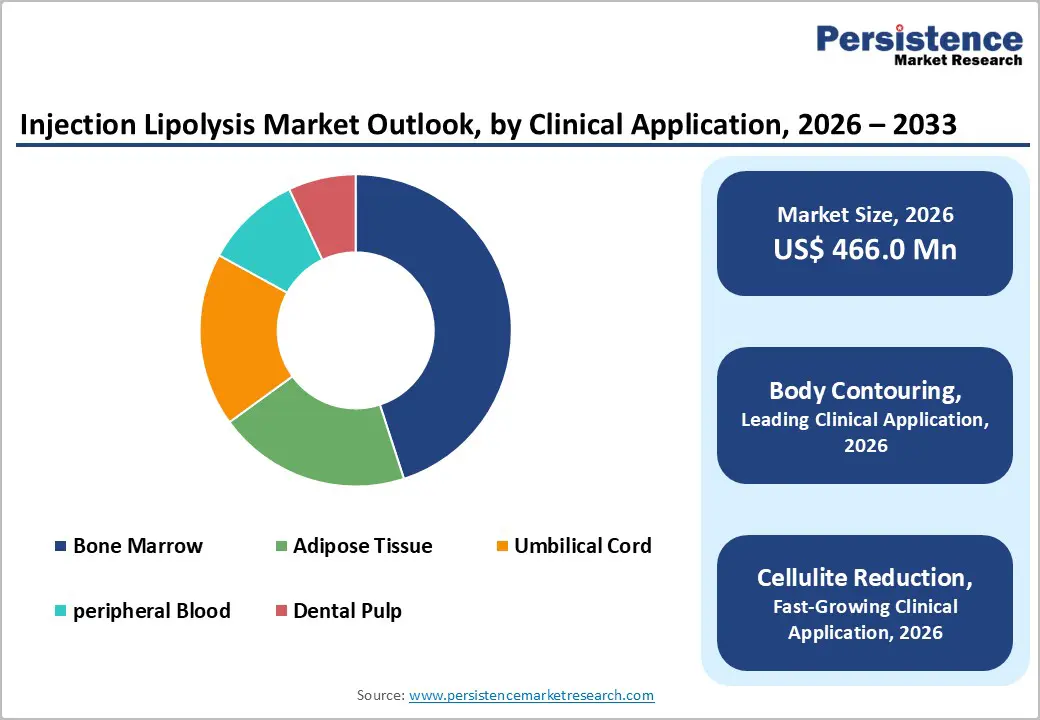

The global injection lipolysis market size is likely to be valued at US$ 466.0 million in 2026 and is projected to reach US$ 1,076.1 million by 2033, growing at a CAGR of 12.7% during the forecast period 2026 - 2033.

The injection lipolysis market is growing as consumers shift toward minimally invasive, non-surgical fat-reduction procedures, driven by increased awareness of aesthetic health and body-contouring options. Deoxycholic acid and combination therapies offer clinically proven efficacy, rapid recovery, and targeted adipose reduction, enhancing patient adoption.

Expansion of dermatology clinics, aesthetic specialty centers, and plastic surgery practices supports broader application across body and facial contouring, as well as cellulite reduction. Growth is further accelerated in emerging markets by rising disposable incomes, urbanization, and greater healthcare access, creating a larger addressable patient base and higher treatment penetration rates globally.

Key Industry Highlights:

- Leading Technology: Deoxycholic acid is expected to lead with an estimated 58% share in 2026, while combination therapies are projected to grow the fastest, driven by multi-ingredient formulations and enhanced clinical outcomes.

- Clinical Application: Body contouring is anticipated to dominate with approximately 61% share in 2026, whereas cellulite reduction is likely to register the fastest growth, reflecting rising adoption among younger demographics and aesthetic-conscious populations.

- Service Providers: Dermatology & skin clinics are projected to hold the largest share at 54% in 2026, while aesthetic specialty clinics are expected to grow fastest, driven by urban expansion and specialized service offerings.

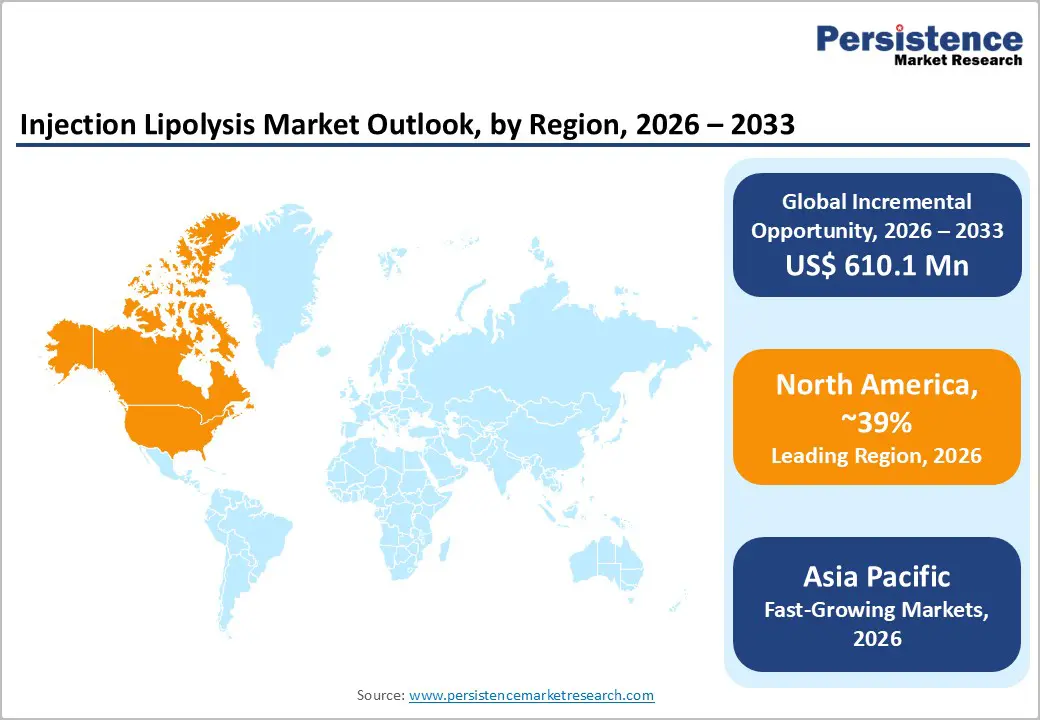

- Regional Leadership: North America is poised to lead with a 39% share in 2026, while Asia Pacific is projected to expand at the fastest rate, with a CAGR of 14.3% through 2033, driven by rising disposable incomes, urbanization, and growing medical tourism.

- Competitive Environment: Market growth is supported by new product launches, technology partnerships, and geographic expansions, allowing key players to strengthen presence, drive innovation, and capture high-growth regional opportunities.

| Key Insights | Details |

|---|---|

| Injection Lipolysis Market Size (2026E) | US$ 466.0 Mn |

| Market Value Forecast (2033F) | US$ 1,076.1 Mn |

| Projected Growth (CAGR 2026 to 2033) | 12.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 12.1% |

DRO Analysis

Driver - Rising Demand for Non-Surgical Cosmetic Procedures

The preference for minimally invasive aesthetic treatments, such as injection lipolysis, is expanding rapidly due to increasing awareness of safe, quick, and low-downtime alternatives to surgery. In 2025, non-surgical procedures, including body contouring and fat reduction injections, were highlighted as top growth trends in aesthetic care, driven by urban populations seeking subtle enhancements. Clinics in North America and the Asia Pacific reported double-digit annual increases in patient volumes, reflecting higher adoption among both younger and aging demographics. Social media influence and rising body image consciousness further amplified interest in cosmetic procedures. Patients now actively prefer treatments that deliver natural-looking outcomes without significant recovery periods.

The expansion of aesthetic clinics, dermatology centers, and specialty treatment hubs has made access to injection lipolysis more convenient, fueling adoption across age groups. Younger adults (18-50 years) increasingly pursue cellulite reduction and body contouring solutions, while older populations opt for less invasive procedures to maintain appearance with minimal risk. The mainstream acceptance of non-surgical alternatives is reinforcing the market base, particularly in high-income and urbanized regions.

Verified trend reports in 2025 show non-surgical procedures as among the fastest-growing segments globally, confirming sustained demand. Overall, consumer preference, clinic accessibility, and cultural shifts collectively drive the expansion of the injection lipolysis market.

Technological Innovation and Expanding Clinical Adoption

Technological advancements in active ingredients such as deoxycholic acid and phosphatidylcholine have improved the efficacy and safety of injection lipolysis. Regulatory approvals in key markets, including the U.S. FDA, have boosted clinical confidence and wider adoption. Innovations in delivery methods and treatment protocols have reduced adverse effects, enhanced precision, and increased patient satisfaction. In 2025, clinical trials and developments in combination therapy were highlighted as key drivers of market innovation. These improvements allow dermatology and specialty clinics to offer expanded applications in body and facial contouring, increasing the total addressable market.

Emerging economies, particularly in the Asia Pacific, are seeing rapid adoption due to rising disposable incomes, improved healthcare access, and growing aesthetic awareness. Younger demographics actively seek non-invasive fat-reduction solutions, while aging populations in North America and Europe prefer less disruptive procedures to surgery. Regulatory updates, including the Modernization of Cosmetics Regulation Act (MoCRA), enhance safety and standardization, fostering innovation and trust. The integration of advanced formulations, delivery technologies, and supportive regulation is expanding clinical acceptance and patient reach, further driving market growth.

Restraint - Regulatory Hurdles and Safety Concerns

Regulatory scrutiny remains a major restraint, as agencies like the U.S. FDA and European CE authorities require rigorous clinical validation for new injection lipolysis formulations. Multiple treatment sessions and variable patient outcomes increase hesitancy to adopt. The lack of standardized clinical protocols increases perceived risk among practitioners and patients. Safety monitoring and reporting obligations further raise operational overheads in clinics. These requirements slow new product launches and limit market penetration. The combination of clinical complexity and regulatory burden constrains growth, particularly for innovative formulations.

Recent developments highlight these challenges. In September 2025, the FDA rescinded an LDT oversight rule after a court decision, demonstrating legal and regulatory uncertainty. Simultaneously, the EU IVDR implementation continues to impose strict compliance standards for in vitro diagnostics, requiring extensive documentation and performance evaluation. These evolving regulations extend approval timelines, affect cross-border launches, and necessitate additional clinical studies, confirming that regulatory hurdles directly influence adoption rates and market strategy.

Cost Barriers in Emerging Markets

High treatment costs restrict uptake in low- and middle-income regions, despite rising demand for non-surgical procedures. Injection lipolysis requires skilled practitioners, specialized facilities, and repeat sessions, resulting in substantial out-of-pocket expenses. Clinics also invest in safety protocols and equipment, which raises pricing. In cost-sensitive markets, patients may opt for alternative procedures, slowing market penetration. Rising operational costs for healthcare providers further amplify this barrier. Consequently, financial constraints remain a persistent limitation for short-term revenue growth.

Supporting evidence comes from the 2025-2026 financial trends. Global medical costs were projected to rise by 10.3% in 2026, putting pressure on clinics’ operational budgets. In India, nearly 40% of healthcare expenses are out-of-pocket, while tariffs and supply chain disruptions increase reagent and consumable costs. Rising import duties on medical devices and fluctuations in raw material prices have further elevated treatment costs in emerging markets, reinforcing that financial constraints significantly limit patient access and slow market expansion.

Opportunities - Expansion into Untapped Emerging Markets

Emerging regions such as Southeast Asia, Latin America, the Middle East, and Africa present significant growth potential for injection lipolysis. Rising medical tourism, higher disposable incomes, and increasing consumer awareness of aesthetic treatments are driving patient demand. Improvements in clinical infrastructure and expansion of specialty clinics support faster adoption of non-surgical procedures. With forecasted CAGR exceeding 12% through 2033, these markets can meaningfully contribute to global revenue. Public health initiatives aimed at improving healthcare access further enhance market readiness. This creates a favorable environment for aesthetic clinics and product suppliers to scale operations.

A report from the Kingdom of Saudi Arabia’s Ministry of Health, which highlighted expanded licensing and infrastructure upgrades for aesthetic and cosmetic treatment centers to boost medical tourism and attract regional patients. In Latin America, Mexico’s tourism board reported a surge in cross-border cosmetic procedure inquiries in 2026, with non-invasive treatments ranking among the fastest-growing segments. These developments demonstrate how regional health policy and tourism promotion are enhancing demand for aesthetic procedures, including injection lipolysis.

Integration of Hybrid Treatments and Advanced Delivery Systems

The convergence of non-invasive technologies such as ultrasound, radiofrequency, and laser-assisted fat reduction with lipolytic injections is driving hybrid treatment adoption. Combining modalities enhances clinical outcomes, reduces session frequency, and improves patient satisfaction. Early adopters integrating multi-modal solutions also benefit from broader insurance reimbursement potential and higher clinic throughput. Strategic collaborations between device manufacturers and injectable suppliers create synergistic revenue streams and differentiated offerings. Regulatory approvals for advanced delivery systems facilitate broader adoption across premium clinics and hospitals. The rising demand for precision body-contouring treatments further supports market expansion.

Supporting industry developments include Cynosure’s May 2025 launch of an AI-based body contouring platform that integrates real-time treatment feedback, improving clinical precision and confirming demand for hybrid solutions. In March 2026, healthcare news outlets reported a strategic collaboration between a global aesthetic device maker and a biotech firm to develop next-generation injectable delivery systems, reinforcing that innovation is being supported by industry partnerships.

Additionally, reported 2026 market data shows injectable procedures are expected to comprise 36% of the non-invasive aesthetic market, validating the rising adoption of advanced injectables alongside other technologies. These examples underscore how technological integration is unlocking new avenues for growth.

Category-wise Analysis

Technology Segment Insights

Deoxycholic acid is expected to command approximately 58% of the technology segment in 2026, driven by its clinically validated mechanism of targeted adipocyte destruction and widespread regulatory acceptance in key markets such as North America and Europe. This active ingredient’s efficacy in localized fat reduction, particularly submental fat (double chin) treatments, reinforces trust among providers and patients, leading to high adoption in dermatology and aesthetic clinics globally.

In 2025, China’s NMPA approved “Rongzhi®,” a deoxycholic acid-based fat-dissolving injectable, marking the first compliant domestic product and significantly expanding market access in Asia. Russian and Korean equivalents further exemplify geographic broadening. Consistent clinical outcomes and regulatory clarity are strengthening its foundational dominance in the injection lipolysis framework.

Combination therapies blending deoxycholic acid with phosphatidylcholine or adjunct agents are emerging as the most dynamic technology sub-segment. These therapies offer enhanced adipocyte breakdown with optimized side-effect profiles, attracting both practitioners and patients seeking tailored solutions for complex areas such as cellulite and multi-region body contouring.

Industry trends in 2025 highlight increasing physician experimentation with integrated injectable approaches that combine lipolytic agents with supportive regenerative or tightening technologies, improving aesthetic outcomes and satisfaction. This trend supports broader clinical applications and reflects the momentum of innovation in injectable fat-reduction solutions.

Clinical Application Insights

Body contouring is anticipated to capture an estimated 61% share of clinical applications in 2026, driven by its broad utility addressing fat deposits resistant to diet and exercise across the abdomen, flanks, and thighs. Patients increasingly prefer injectable options over surgical liposuction due to shorter recovery times, lower risk, and discrete results, reinforcing its leading position in clinics. An industry overview reported early 2025 momentum in global body contouring treatment markets, with non-surgical fat reduction options among the fastest-expanding segments.

This macro trend reflects a shift in patient behavior toward safe, effective non-invasive enhancements, contributing to body contouring’s commanding clinical share. With stronger demand in urban centers worldwide, clinics are expanding their service portfolios to prioritize these treatments.

Cellulite reduction is poised to register the fastest growth through 2033, supported by rising patient interest and advances in the specificity of injectable treatments. Unlike weight loss or simple fat reduction, cellulite is a complex cosmetic concern that affects skin texture and drainage patterns, prompting clinicians to innovate beyond traditional solutions. In 2025, non-surgical cellulite treatments, including advanced injectables combined with supportive technologies, were widely featured in aesthetics trend coverage, highlighting improved effectiveness and patient demand.

This reflects consumer desire for smoother, firmer skin without surgery. As practitioners incorporate these advanced approaches, cellulite reduction is emerging as a differentiated growth driver within injection lipolysis clinical applications.

Regional Insights

North America Injection Lipolysis Market Trends

North America is expected to remain the leading regional market, with an estimated 39% share of the global non-invasive aesthetic treatment market in 2026, supported by strong consumer demand, advanced clinical infrastructure, and high healthcare spending. Consumer adoption of injectable and minimally invasive procedures continues to grow as patients prioritize natural results with minimal downtime, contributing to overall procedural volume. In March 2025, major aesthetic firms launched next-generation injectable products with enhanced longevity and onset of results, driving heightened patient interest and clinic utilization. Regulatory progress and heightened safety awareness reported in 2025 also underscored continued innovation in dermal fillers, micro needling, and energy-based platforms.

The United States leads regional performance, with widespread availability of dermatology and cosmetic specialty clinics offering diverse treatment portfolios. Rising awareness of preventive aesthetic care, including early injectable interventions and personalized treatment approaches, is strengthening patient engagement, including among male consumers, a noted trend in 2025 toward broader demographic participation.

Urban population centers are expanding clinic density and service variety, facilitating competitive differentiation and enhancing service accessibility. Continued innovation and stable regulatory frameworks underpin North America’s sustained leadership and supportive environment for new clinical applications and technologies.

Europe Injection Lipolysis Market Trends

Europe holds a significant mature market position with strong demand for non-surgical and minimally invasive aesthetic procedures, supported by harmonized regulatory environments like the CE mark, ensuring product quality and clinical safety. A shift toward preventive cosmetic treatments alongside traditional aesthetic services is observed, with clinics offering integrated protocols that combine injectable therapies with energy-based treatments to meet evolving patient expectations. Consumer awareness is rising across age groups, particularly among aging populations seeking minimally disruptive solutions. In 2025, broader adoption of combined approaches (e.g., injectables paired with micro needling or laser resurfacing) was reported as a key trend among dermatology practices.

European clinics are also enhancing practitioner expertise through standardized education and certification initiatives, which boost confidence in advanced treatments. Cross-border mobility of patients within the EU reinforces knowledge exchange and clinical best practices, further supporting market growth. Local regulatory focus on safety standards and professional oversight is creating an environment that balances innovation with patient protection, reinforcing Europe’s position as a stable, quality-driven market for non-surgical aesthetic care.

Asia Pacific Injection Lipolysis Market Trends

Asia Pacific is projected to expand at the fastest rate with a CAGR of 14.3% through 2033, with demand expanding rapidly due to rising disposable incomes, heightened aesthetic awareness, and robust medical tourism infrastructure. The region is projected to experience significant CAGR through the late 2020s, driven by evolving beauty preferences and broader acceptance of non-invasive treatments such as injectables and laser therapies.

Countries such as China, South Korea, and Thailand are emerging as major aesthetic hubs; for example, Thailand’s medical tourism sector accounts for nearly half of the region’s total volume, reflecting strong global appeal for quality, cost-competitive services.

In 2025, industry activity in the Asia Pacific included tailored product launches and the adoption of advanced diagnostic and AI-powered technologies in clinics, particularly to meet localized aesthetic preferences and deliver more precise outcomes. Consumer demand in key markets is supported by growing middle-income groups and expanding urban population, with a broad demographic base embracing minimally invasive solutions. Ongoing investment by global and regional players in infrastructure and training is strengthening market capabilities, positioning Asia Pacific as a major growth engine for the injection lipolysis and broader aesthetic market.

Competitive Landscape

The global cell therapy bioprocessing market is moderately consolidated, with top players such as Lonza Group, Thermo Fisher Scientific, Miltenyi Biotec, and GE Healthcare controlling over 50% of revenue. These companies leverage strong biopharma partnerships, regulatory expertise, and integrated bioprocessing platforms. Heavy R&D investment and process innovation maintain technological leadership in cell culture, viral vectors, and downstream processing. Advanced automation and analytics improve scalability, safety, and clinical reliability. Their extensive global footprint reinforces dominance across commercial and clinical markets.

Regional and niche players, including Fujifilm Cellular Dynamics and Hitachi Chemical Advanced Therapeutics, target specialized segments such as allogeneic therapies and gene-modified cells. Regulatory complexity and process integration barriers limit new entrants, but AI-driven analytics and digital monitoring enable software-focused solutions to participate. Market consolidation is expected as leading players pursue acquisitions and strategic partnerships. Expansion into emerging markets and technology collaborations are driving competitive dynamics. Innovation and regulatory alignment remain key differentiators.

Key Industry Developments:

- In April, 2026, Allergan Aesthetics (AbbVie) opened applications for its fourth year of the initiative, providing US$ 20,000 grants to 20 women entrepreneurs and mentorship for 250 participants to strengthen women-led aesthetic businesses.

- In March 2025, Raziel Therapeutics and Tianjin JuveStar Biotech launched a Phase 3 registration trial for RZL-012 in China, with JuveStar managing clinical studies, marketing, and sales, and Raziel responsible for drug manufacturing, aiming for a Chinese market launch in 2027.

Companies Covered in Injection Lipolysis Market

- Allergan plc

- Merz Pharma GmbH & Co. KGaA

- Cynosure, Inc.

- Bausch Health Companies Inc.

- Galderma S.A.

- Cutera, Inc.

- Lumenis Ltd.

- Syneron Medical Ltd.

- Venus Concept Ltd.

- Solta Medical, Inc.

- Prollenium Medical Technologies

- Thrive Bioscience

- Huons Co., Ltd.

- Revitacare SAS

Frequently Asked Questions

The global injection lipolysis market is projected to reach US$ 466 million in 2026.

Rising demand for non-surgical fat reduction, technological innovations, and growing aesthetic awareness drive the market.

The market is expected to grow at a CAGR of 12.7% from 2026 to 2033.

Expanding adoption in emerging markets, combination therapy innovations, and new clinic networks offer key opportunities.

Leading players include Kythera Biopharmaceuticals, Allergan, Lipolysis Technologies, and Medytox.