- Healthcare Services

- Recreational Drugs Market

Recreational Drugs Market Size, Share, and Growth Forecast, 2026 - 2033

Recreational Drugs Market by Product Type (Cannabis, MDMA, Others), Consumption Method (Inhalation, Ingestion, Sublingual), Distribution Channel (Online Stores, Physical Retail Stores), and Regional Analysis 2026 - 2033

Recreational Drugs Market Size and Trends Analysis

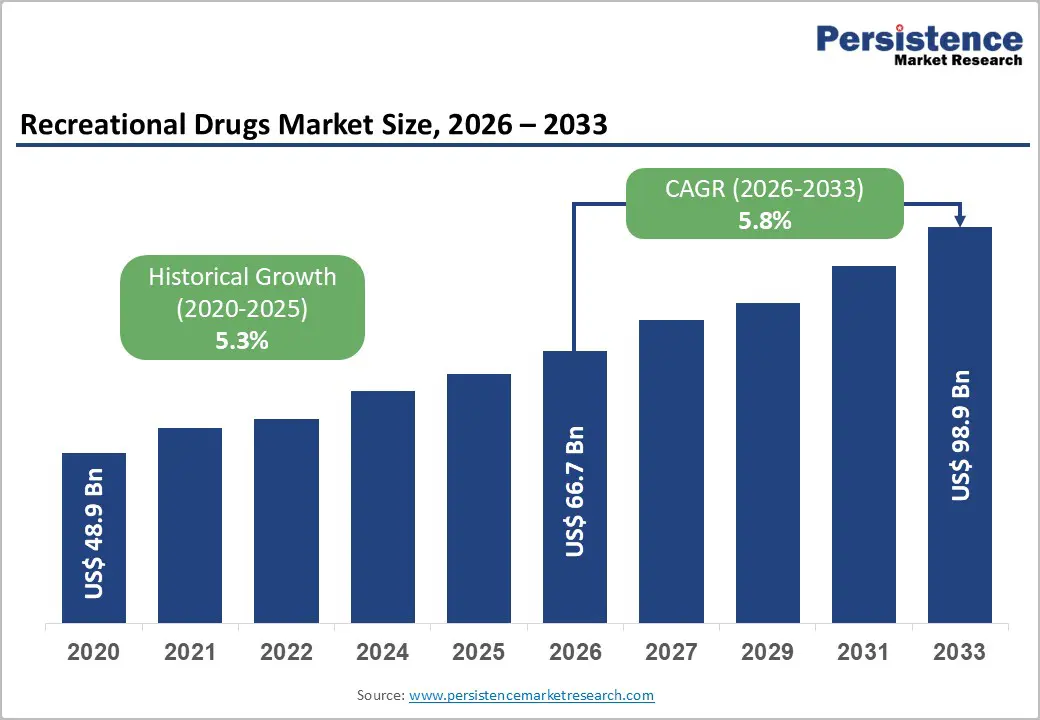

The global recreational drugs market size is likely to be valued at US$66.7 billion in 2026, and is expected to reach US$98.9 billion by 2033, growing at a CAGR of 5.8% during the forecast period from 2026 to 2033, driven by evolving legal frameworks that are shaping global demand dynamics.

Increasing consumer interest in varied consumption formats is driving notable technological advancements across the industry. The transformation of retail channels is also expected to reshape procurement trends, particularly in established markets. Strategic capital investments are further strengthening the sector’s long-term commercial prospects. Collectively, these factors point to a stable and resilient growth trajectory. Market analysts foresee continued interest from both institutional and private investors worldwide, with regulatory clarity acting as a key enabler for cross-border participation. Additionally, emerging segments are well-positioned to gain incremental market share through niche and specialized offerings. Overall, the market outlook reflects a progressively maturing industry marked by increasing professionalization.

Key Industry Highlights:

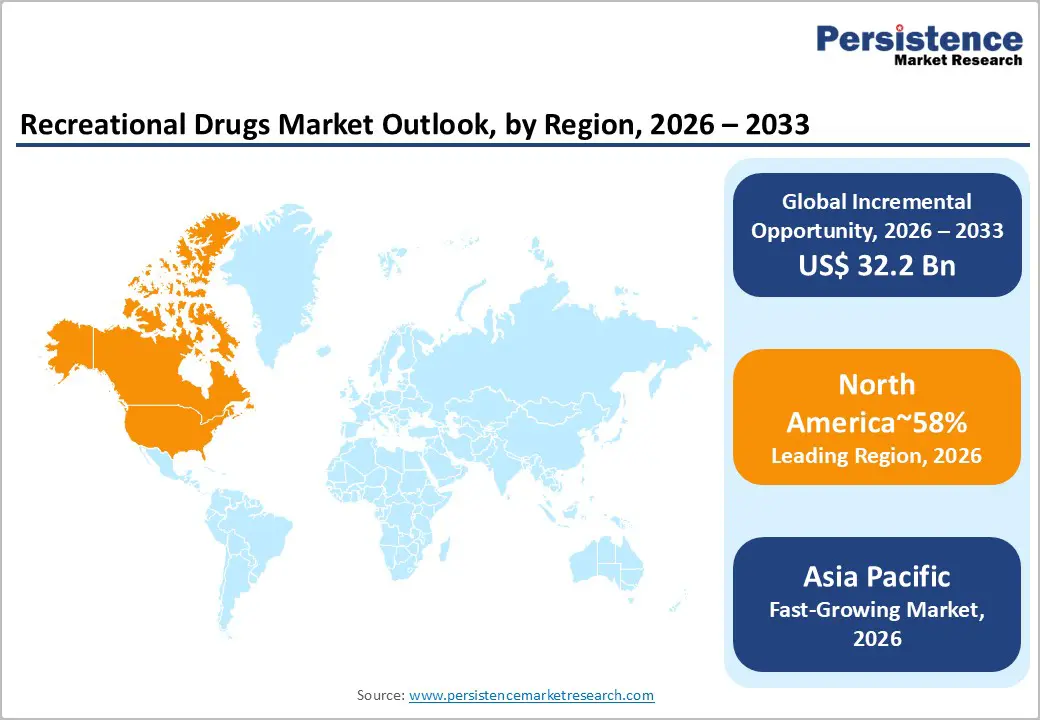

- Leading Region: North America is projected to lead, accounting for approximately 58% share in 2026, supported by federal rescheduling momentum, established retail infrastructure, and high consumer spending power.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest, driven by evolving medical frameworks, large population bases, and increasing urbanization.

- Leading Product Type: Cannabis is expected to lead, accounting for approximately 83% share in 2026, anchored by widespread decriminalization, diverse product portfolios, and mature supply chains.

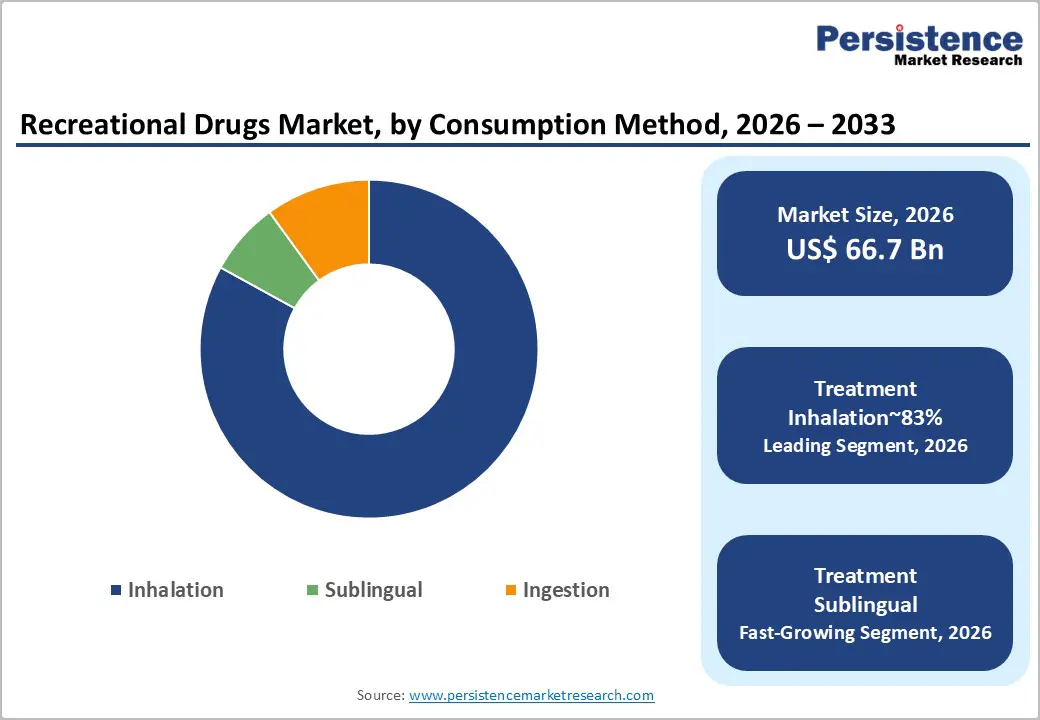

- Leading Consumption Method: Inhalation is anticipated to dominate, accounting for approximately 61% share in 2026, anchored by immediate onset effects, traditional preferences, and advanced vaporizer technology.

| Key Insights | Details |

|---|---|

| Recreational Drugs Market Size (2026E) | US$66.7 Bn |

| Market Value Forecast (2033F) | US$98.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

DRO Analysis

Driver Analysis - Diversification of Consumer Formats and Product Portfolios

Demand for non-traditional consumption formats is reshaping manufacturing, formulation, and processing workflows across regulated markets. Consumers prioritize precision, consistency, and portability, driving evolution in product design and delivery systems. This behavioral shift compels vendors to invest in advanced extraction technologies and formulation capabilities. Enhanced delivery mechanisms broaden accessibility, attracting new user segments with differentiated consumption preferences. Emerging categories such as beverages and edibles gain traction through convenience and controlled dosing attributes. Regulatory frameworks emphasize standardization, reinforcing quality assurance and dosage consistency across product lines. These factors collectively accelerate innovation and diversification within consumer-focused product ecosystems.

Tilray Brands with Good Supply demonstrates diversified product portfolios aligned with evolving consumer format preferences. Manufacturers refine offerings to ensure consistent dosing accuracy and improved sensory experiences across categories. Discrete consumption methods gain acceptance within urban demographics seeking convenience and privacy. Product innovation increasingly focuses on flavor optimization and rapid-onset delivery technologies. Competitive positioning is strengthened through alignment with consumer expectations for reliability and usability. These developments reinforce brand differentiation and sustained engagement within expanding regulated markets.

Professionalization of Retail and Distribution Infrastructure

The emergence of sophisticated retail environments is enhancing consumer engagement and elevating overall purchasing experiences. Physical dispensaries evolve into consultative spaces supporting informed product discovery and guided selection processes. Strategic location planning strengthens market penetration by aligning outlets with high-demand urban consumption zones. Advanced inventory management systems improve product availability and optimize assortment planning across retail networks. Digital integration within storefronts streamlines procurement workflows and accelerates transaction efficiency at checkout stages. Regulatory compliance frameworks reinforce standardized retail practices and operational transparency within licensed environments. These developments collectively drive higher footfall and increased consumer spending across organized retail channels.

Curaleaf Holdings, in collaboration with Select, is advancing retail modernization through enhanced storefront experiences and well-defined consumer engagement strategies. Trained staff focus on product education, helping to build consumer trust and ensure safe purchasing within regulated environments. Retailers are increasingly adopting omnichannel models that integrate physical outlets with digital platforms, enabling a more seamless customer journey. At the same time, distribution systems are being optimized to maintain consistent product availability and reduce stock inconsistencies across locations. The use of data analytics further supports informed merchandising and inventory management, aligning offerings with evolving consumer preferences. Together, these capabilities strengthen operational efficiency and support sustained growth within structured and regulated retail ecosystems.

Restraint Analysis - Restraint - Punitive Taxation and Financial Constraints

Heavy tax burdens and limited access to banking services continue to significantly constrain profitability for regulated market participants worldwide. High effective tax rates reduce the capital available for reinvestment in operations, expansion, and innovation. Additionally, the lack of federal bankruptcy protections increases financial risk for companies facing distress. These fiscal challenges contribute to higher retail prices, reducing the competitiveness of legal operators against unregulated alternatives. As a result, illicit markets often gain an advantage, while regulatory fragmentation further complicates financial planning and restricts access to institutional funding. Collectively, these pressures undermine the long-term financial stability of formalized market ecosystems.

In response, Trulieve, alongside Modern Flower, is focusing on cost optimization strategies to navigate restrictive financial conditions and maintain operational efficiency. Financial constraints are also accelerating industry consolidation, as smaller players struggle to remain viable independently. Companies are increasingly targeting high-margin segments to counterbalance the impact of taxation on profitability. Capital allocation decisions are becoming more closely aligned with regulatory and tax structures that shape revenue potential. Meanwhile, competitive intensity is rising as firms vie for limited margins in a constrained environment. These trends underscore the growing importance of financial discipline in sustaining operations within heavily taxed and regulated markets.

Regulatory Reversals and Compliance Instability

Sudden government policy shifts introduce operational uncertainty across regulated markets dealing with controlled substances. Re-criminalization efforts in select jurisdictions force abrupt business closures and capital withdrawal from affected regions. These reversals disrupt established supply chains and weaken investor confidence in long-term market stability. Fragmented regulatory oversight increases compliance complexity, requiring continuous adaptation to evolving legal frameworks. Rising administrative and legal costs place additional pressure on operating margins and expansion strategies. Institutional lenders remain cautious due to heightened regulatory risk and unpredictable enforcement environments. These dynamics collectively constrain strategic planning and limit sustained market development across affected sectors.

Aurora Cannabis with Aurora Drift aligns operations within strictly regulated clinical environments to mitigate exposure to policy volatility. Regional instability alters expansion strategies, redirecting investments toward compliant and lower-risk jurisdictions. Legal reversals necessitate rapid restructuring of distribution and product positioning within constrained frameworks. Valuation adjustments reflect increased uncertainty tied to shifting regulatory landscapes and enforcement actions. Market participants emphasize compliance resilience to maintain operational continuity under fluctuating policies. These pressures collectively shape cautious growth trajectories within highly regulated and politically sensitive markets.

Opportunity Analysis -Therapeutic Integration of Psychedelic Compounds

The convergence of clinical research and evolving regulatory frameworks is opening new therapeutic segments for psychedelic compounds. Legalization of supervised psilocybin use enables structured clinical pathways targeting unmet mental health conditions. Early-stage clinical validation strengthens institutional confidence and supports gradual regulatory acceptance across jurisdictions. These compounds demonstrate potential in addressing complex disorders within mental wellness and neuropsychiatric treatment domains. Strategic collaborations emerge between biotechnology developers and healthcare delivery networks to scale controlled access models. Regulatory emphasis on safety, dosing standardization, and clinical oversight shapes development trajectories. These dynamics collectively position psychedelic therapeutics within an emerging, high-value healthcare innovation segment.

Compass Pathways with COMP360 advances standardized synthetic psilocybin protocols aligned with regulated therapeutic delivery frameworks. Clinical programs focus on establishing efficacy, safety, and reproducibility within controlled treatment environments. Integration within structured care settings enhances patient monitoring and outcome consistency across trials. Institutional adoption increases as evidence frameworks mature and regulatory clarity improves. Development strategies prioritize scalable manufacturing and compliance with pharmaceutical-grade standards. These interdependencies reinforce long-term expansion of medically integrated psychedelic treatment ecosystems.

End Lifestyle and Wellness Branding in Premium

A structural shift toward premiumization is creating demand for luxury-oriented, wellness-focused product portfolios globally. Consumers increasingly prioritize artisanal quality, organic sourcing, and ethically aligned production standards within purchasing decisions. This behavioral transition elevates average transaction values and strengthens margin profiles for differentiated offerings. Wellness-centric branding reduces legacy stigma by repositioning products within health and lifestyle narratives. Older and affluent demographics demonstrate a higher affinity toward boutique formats emphasizing exclusivity and product authenticity. Regulatory emphasis on transparency reinforces the adoption of traceable and responsibly sourced premium goods. These dynamics collectively establish lifestyle integration as a critical competitive differentiator across evolving markets.

Canopy Growth Corporation, with Deelish, targets premium consumer segments through curated product experiences and elevated brand positioning strategies. High-quality packaging and narrative-driven marketing reinforce perceived value and exclusivity within luxury-oriented categories. Brand differentiation increasingly relies on authenticity, sustainability credentials, and consistent product quality assurance. Retail environments adapt to showcase premium offerings aligned with wellness and lifestyle positioning frameworks. Consumer engagement strengthens through storytelling that connects sourcing practices with end-user benefits. These factors collectively sustain demand growth within high-end, wellness-integrated product ecosystems.

Category-wise Analysis

Product Type Insights

Cannabis is expected to dominate, accounting for approximately 83% share in 2026, supported by extensive global decriminalization and diverse product availability. Widespread acceptance across diverse age groups is currently reinforcing this segment's dominance. Manufacturers continue to innovate with high-potency strains and specialized extraction methods. Tilray Brands with Good Supply and Curaleaf with Select exemplify this sector leadership. Mature retail infrastructures in North America are set to sustain high procurement volumes. Consumers prioritize the predictability and variety offered by established cannabis brands today. Ongoing investments in indoor cultivation technology further strengthen supply chain consistency. This structural alignment between consumer demand and regulatory progress underpins market leadership.

Psilocybin is anticipated to be the fastest-growing segment, driven by emerging research into therapeutic and wellness applications. Increasing public interest in mental health alternatives is currently accelerating adoption across clinical settings. Regulatory breakthroughs in specific Western jurisdictions are providing a roadmap for future expansion. Advancements in synthetic manufacturing are poised to ensure consistent product quality and safety. Analysts expect that broader decriminalization will unlock substantial new consumer demographics globally. Strategic positioning within the mental wellness sector remains a primary growth catalyst. This convergence of clinical validation and social acceptance is driving exceptional momentum.

Consumption Method Insights

Inhalation is expected to lead, accounting for approximately 61% share in 2026, underpinned by the immediate physiological effects and traditional consumer habits. Vaporization technology is currently enhancing the safety and discretion of this delivery method. Sophisticated hardware designs are attracting tech-savvy users who prioritize control and flavor. Canopy Growth with Claybourne Gassers and Verano Holdings with MÜV illustrate this technical evolution. High-throughput manufacturing of pre-rolled products continues to support consistent retail volume growth. Adoption remains anchored in the efficiency of pulmonary absorption for a rapid onset. Ongoing refinements in heating element materials are anticipated to improve the user experience. This category's dominance is reinforced by a robust and diverse hardware ecosystem.

Sublingual is anticipated to be the fastest-growing segment, driven by increasing consumer demand for smoke-free and discreet drug delivery. This method offers a balance between rapid absorption and long-lasting functional effects. Users are increasingly seeking alternatives to combustion and ingestion due to health concerns. Tilray Brands, with Redecan and Aurora Cannabis, with Aurora Drift, are leading in this niche. Precision dosing through tinctures and strips is expected to appeal to medicalized users. Analysts suggest that the high bioavailability of sublingual formats will attract performance-oriented consumers. Strategic expansion into lifestyle and wellness channels is forecast to accelerate segment growth. This shift toward non-invasive delivery methods is redefining traditional consumption patterns.

Regional Insights

North America Recreational Drugs Market Trends

North America is expected to remain the leading regional market, accounting for approximately 58% share in 2026, supported by federal rescheduling initiatives and a deeply embedded retail culture. The region benefits from highly mature supply chains and significant institutional capital inflows. Large-scale cultivation facilities are currently optimizing production costs to maintain competitive pricing. Regulatory progress at both state and federal levels is anticipated to harmonize compliance. Advanced consumer analytics are driving the development of highly targeted product portfolios. This structural depth continues to attract the world's most prominent market participants.

The U.S. is expected to anchor regional momentum through the anticipated shift of cannabis to Schedule III status. This legislative change is projected to eliminate the punitive impact of specific federal tax codes. Curaleaf with Select is likely to benefit from increased operational cash flows. Investment in multi-state infrastructure is anticipated to accelerate as banking restrictions ease. Trulieve with Modern Flower remains positioned to scale its presence in emerging eastern markets. Analysts suggest that federal reform will trigger a new wave of industry consolidation. Sustained consumer demand for premium flower and edibles reinforces this national market dominance.

Europe Recreational Drugs Market Trends

Europe is projected to remain a mature and structurally stable market, with demand largely driven by established medical frameworks and gradual progress in adult-use legalization. Growth across the region is expected to be supported by stringent quality standards and a strong emphasis on pharmaceutical-grade production. Ongoing recreational pilot programs are generating insights that will inform future regulatory decisions. Public health-focused policies are likely to favor standardized, transparent product offerings. Increasing regulatory alignment is also expected to facilitate cross-border trade, enhancing market integration. This stable environment continues to attract companies seeking long-term, low-risk growth opportunities.

Within Europe, Germany is anticipated to lead the market following the rollout of its comprehensive cannabis legalization framework. The new regulations permit non-commercial social clubs and limited personal cultivation. Tilray Brands, in collaboration with Redecan, is well-positioned to support the growing medical and therapeutic segments. Strict quality requirements in the country are expected to establish a benchmark for other European markets. Canopy Growth, through its MTL Cannabis brand, is also actively pursuing strategic distribution partnerships across the region. Greater regulatory clarity is likely to stimulate investments in domestic processing infrastructure, while Germany’s approach is expected to shape legalization strategies in neighboring countries.

Asia Pacific Recreational Drugs Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as medicinal framework buildouts and shifting social perceptions accelerate market expansion. The region's massive population base presents a substantial long-term opportunity for wellness-focused products. Urbanization and rising disposable incomes are currently driving interest in premium consumption formats. Strategic interest is anticipated to focus on CBD and non-psychoactive compounds initially. Local governments are exploring the economic benefits of industrial and medical drug cultivation. This emerging landscape is attracting global players seeking early-mover advantages in untapped areas.

Australia is expected to anchor regional momentum through sustained growth in its legal medicinal cannabis sector. Community attitudes are shifting toward the potential legalization and regulation of adult personal use. Penington Institute reports indicate that the illicit market currently generates billions annually. Aurora Cannabis with Aurora Drift is set to benefit from this expanding clinical demand. Regulatory inquiries are increasingly recommending significant reforms to current criminalization policies. Analysts suggest that a regulated market could generate substantial tax revenue for states. Ongoing innovation in vaporized and sublingual delivery methods is expected to drive procurement.

Competitive Landscape

The recreational drugs market is fragmented, with gradual consolidation led by expanding operators such as Tilray Brands and Canopy Growth. These firms exert influence through established retail footprints, intellectual property assets, and compliance capabilities across regulated markets. Their products set benchmarks for safety, potency consistency, and brand positioning within evolving consumer segments. Their operational scale enables effective navigation of complex regulatory frameworks across multiple jurisdictions. This structure reflects the coexistence between localized producers and globally integrated entities, shaping industry standards.

Competitive positioning reflects horizontal expansion across product categories alongside vertical integration in cultivation, processing, and distribution. Premium participants emphasize differentiated branding, formulation precision, and lifestyle alignment, while value providers focus on scale efficiencies and affordability. Industry dynamics include sustained merger activity, enabling geographic expansion and portfolio diversification. Platform evolution increasingly incorporates digital engagement tools and advanced formulation technologies enhancing user experience. Forward-looking strategies prioritize regulatory compliance, supply chain transparency, and ethical sourcing aligned with maturing market expectations.

Key Industry Developments:

- In April 2026, Cresco Labs secured conditional approval for a Texas Compassionate Use Program license, strengthening its vertically integrated presence in a key emerging market.

- In March 2026, Canopy Growth launched “Deelish,” a high-THC brand aimed at everyday consumers, intensifying competition through potency and price-driven positioning.

- In January 2026, AtaiBeckley outlined its 2026 pipeline strategy post-merger, backed by funding through 2029 to advance mebufotenin (5-MeO-DMT) and R-MDMA toward commercialization.

Companies Covered in Recreational Drugs Market

- Curaleaf Holdings, Inc.

- Tilray Brands, Inc.

- Canopy Growth Corporation

- Green Thumb Industries

- Trulieve Cannabis Corp.

- Cresco Labs Inc.

- Verano Holdings Corp.

- Aurora Cannabis Inc.

- Cronos Group Inc.

- Organigram Holdings Inc.

- SNDL Inc.

- TerrAscend Corp.

- Village Farms International

- Compass Pathways plc

- Mind Medicine (MindMed) Inc.

- Jazz Pharmaceuticals

Frequently Asked Questions

The global recreational drugs market is projected to be valued at US$66.7 billion in 2026 and is expected to reach US$98.9 billion by 2033, driven by expanding legalization frameworks, increasing consumer acceptance, and diversification of product formats across regulated markets.

The shift toward edibles, beverages, vaporizers, and sublingual formats is a key driver, as it enhances consumer accessibility, ensures controlled dosing, and aligns with evolving preferences for convenience, discretion, and improved sensory experiences across different user segments.

The recreational drugs market is forecast to grow at a CAGR of 5.8% from 2026 to 2033, reflecting steady expansion supported by regulatory clarity, retail infrastructure development, and increasing institutional investment.

North America is the leading regional market, accounting for approximately 58% share, supported by federal rescheduling momentum, mature retail ecosystems, high consumer spending capacity, and well-established supply chain infrastructure.

The recreational drugs market is fragmented, with key players including Tilray Brands, Canopy Growth Corporation, Curaleaf Holdings, Trulieve Cannabis Corp., and Aurora Cannabis Inc. These companies compete through vertical integration, product innovation, and strong compliance capabilities across regulated markets.