- Medical Devices

- Hygiene Components Market

Hygiene Components Market Size, Share, and Growth Forecast 2026 - 2033

Hygiene Components Market by Component Type (Absorbent Core, Top Sheet, Back Sheet, Acquisition/Distribution Layer, Elastic Components, Adhesives & Fastening Systems, Barrier/Leakage Control Components, Hygienic Equipment Components), Material Type (Nonwoven Fabrics, Films, Fluff Pulp, Superabsorbent Polymers, Elastomers, Plastics, Metals), Application, End-user, and Regional Analysis, 2026 - 2033

Hygiene Components Market Size and Trend Analysis

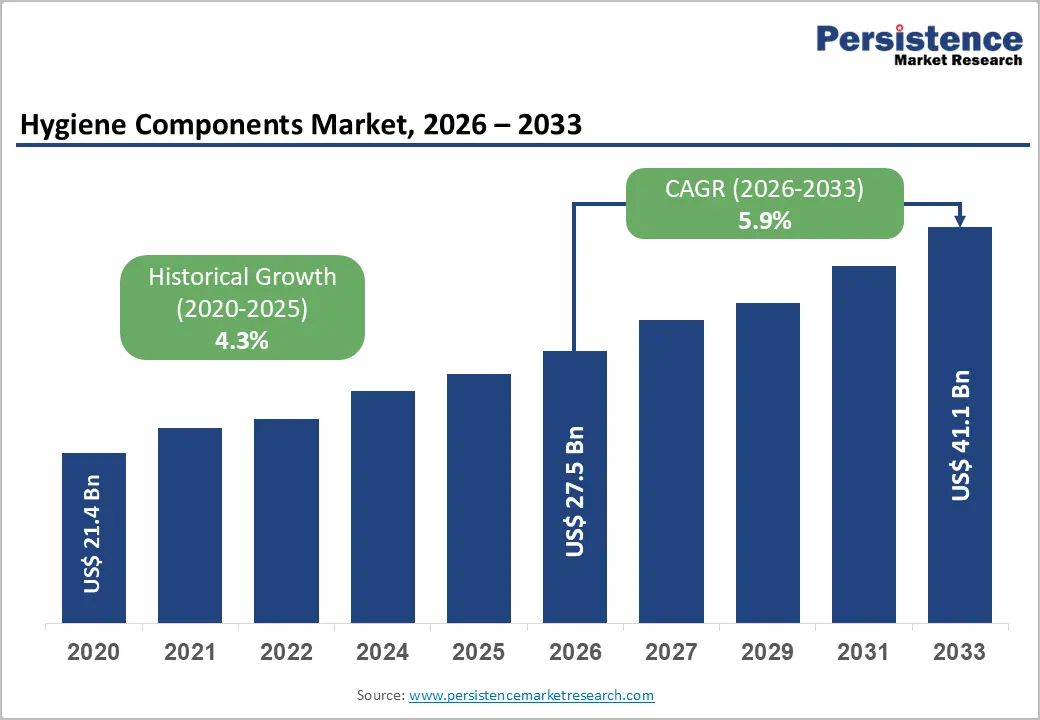

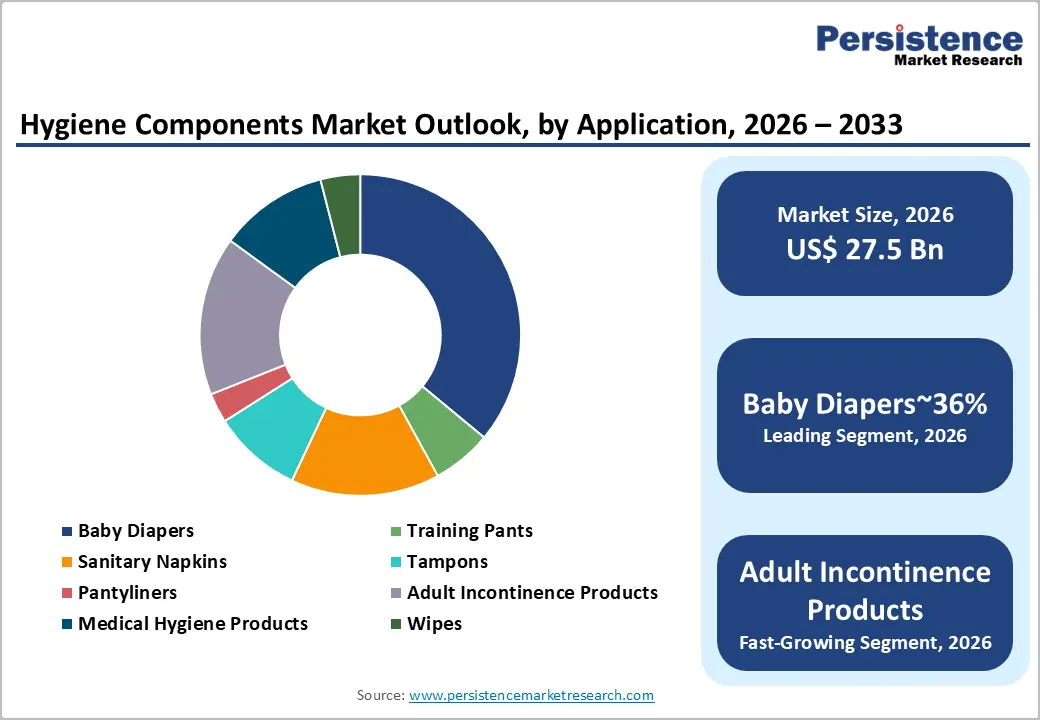

The global hygiene components market size is likely to be valued at US$ 27.5 billion in 2026 and is expected to reach US$ 41.1 billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033.

The market is advancing on the strength of a globally expanding population, rising hygiene awareness in emerging economies, an ageing demographic driving adult incontinence product demand, and intensifying quality and safety standards in food processing, pharmaceutical, and healthcare manufacturing that are compelling investment in hygienic equipment components and fluid handling systems.

Key Market Highlights

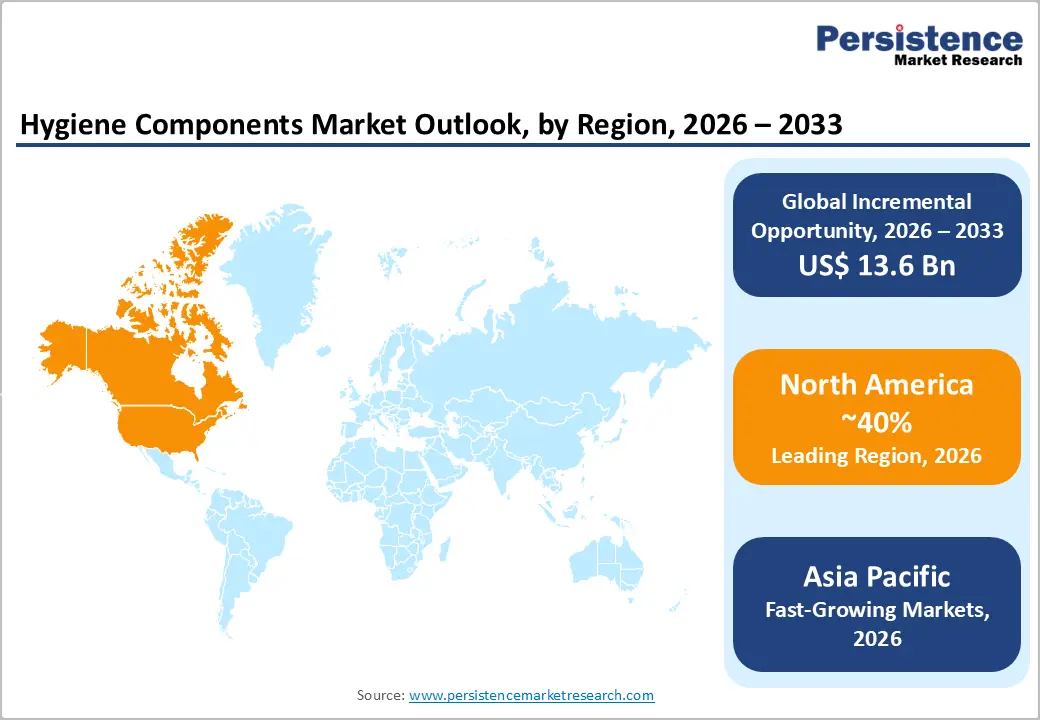

- Leading Region: North America, led by the United States, dominates the Hygiene Components Market holding 40% share, supported by a major personal care converting industry anchored by Procter & Gamble and Kimberly-Clark, stringent FDA FSMA regulations driving hygienic equipment investment, and an ageing population of 58 Million+ Americans over 65 creating adult incontinence product component demand.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, driven by a population exceeding 4.7 billion, India's GST-exempt sanitary napkin demand expansion under PMBJP, China's booming domestic hygiene industry, and rapidly growing ASEAN food processing sector investment in certified hygienic equipment components.

- Leading Application: Baby diapers lead the application category with approximately 36% market share, sustained by approximately 140 million annual global births per UNICEF and rising diaper adoption rates in Africa and South Asia, driving continuous high-volume demand for superabsorbent polymers, nonwoven top sheets, elastic waistbands, and polyethylene back sheets.

- Fastest Growing Application: Adult incontinence products represent the fastest-growing application segment, driven by the WHO's projection that the global population aged 60+ will reach 2 billion by 2050, double current levels, with incontinence affecting an estimated 420 million people globally and premium component demand accelerating in high-income markets.

- Key Opportunity: Hygienic equipment modernization in emerging market food, dairy, and pharmaceutical processing, supported by FAO projections of 20% global dairy production growth by 2030 and ASEAN food safety regulatory harmonization, creates a large-scale, long-cycle procurement opportunity for certified hygienic component suppliers including Alfa Laval, GEA Group, and Tetra Pak.

Market Dynamics

Drivers - Rapidly Ageing Global Population Driving Adult Incontinence Product Demand

The global demographic transition toward an older population is emerging as one of the most durable structural growth drivers for the Hygiene Components Market. According to the World Health Organization (WHO), the global population aged 60 years and above will double from approximately 1 billion in 2020 to over 2 billion by 2050, with individuals aged 80 years and above projected to triple over the same period.

Urinary incontinence affects an estimated 420 million people globally per the WHO, with prevalence rates rising sharply among the elderly population. This demographic reality is driving accelerating demand for adult incontinence products, including pull-up pants and underpads, which require high-performance superabsorbent polymers (SAP), nonwoven top sheets, elastic waistband components, and leak-barrier systems. Manufacturers of hygiene components including Ecolab, Mettler-Toledo, and component specialists are scaling capacity to serve this growing and premium-priced product category.

Stringent Hygienic Standards in Food, Beverage, and Pharmaceutical Processing

Rise in regulatory requirements for hygienic design and sanitary process equipment across food & beverage, dairy, pharmaceutical, and biotechnology manufacturing sectors are creating robust and structurally growing demand for hygienic equipment components, including sanitary valves, pumps, fittings, sensors, and filtration assemblies.

The U.S. Food and Drug Administration (FDA) Food Safety Modernization Act (FSMA) and the European Commission's food hygiene regulations under Regulation (EC) No. 852/2004 mandate Hazard Analysis Critical Control Point (HACCP) compliance, driving continuous investment in certified hygienic process equipment. According to the 3-A Sanitary Standards, Inc., the number of certified hygienic equipment approvals has grown consistently year-on-year as food and pharmaceutical manufacturers upgrade aging infrastructure to meet current good manufacturing practice (cGMP) and FDA validation standards.

Restraints - Environmental Concerns and Regulatory Pressure on Single-Use Plastic Hygiene Components

The dominant role of single-use plastics, including polyethylene films, polypropylene nonwovens, and plastic-based elastic components, in disposable hygiene products has attracted growing regulatory scrutiny globally. The European Union's Single-Use Plastics Directive (SUPD) and extended producer responsibility (EPR) frameworks for hygiene product packaging are increasing compliance costs for hygiene component manufacturers and compelling material reformulation toward bio-based and biodegradable alternatives.

According to the Ellen MacArthur Foundation, only a small fraction of hygiene product materials are currently recyclable or compostable, creating reputational and regulatory risk for manufacturers heavily reliant on conventional plastic-based component architectures.

Volatility in Raw Material Prices, Fluff Pulp, SAP, and Nonwoven Feedstocks

The Hygiene Components Market is highly exposed to price volatility in key raw materials including fluff pulp, superabsorbent polymers (SAP), and polypropylene-based nonwoven fabrics. According to the Food and Agriculture Organization (FAO) and RISI Forest Products Intelligence, global wood pulp prices have exhibited significant cyclical volatility, with price spikes of 30-50% observed during supply disruptions in major producing regions including Canada, Chile, and Brazil. SAP prices are similarly linked to propylene feedstock market dynamics.

These input cost fluctuations compress manufacturer margins, complicate long-term customer contract pricing, and create operational uncertainty that constrains capacity investment planning among mid-tier hygiene component suppliers.

Opportunities - Rising Feminine Hygiene Awareness and Menstrual Health Policy Initiatives in Emerging Markets

Government-led menstrual health programs, NGO distribution initiatives, and rising female workforce participation in South Asia, Sub-Saharan Africa, and Southeast Asia are creating a rapidly expanding demand frontier for feminine hygiene components, including non-woven top sheets, absorbent cores, and pantyliner leak-barrier systems. According to UNICEF, approximately 500 million women and girls globally lack access to adequate menstrual hygiene products and facilities. Policy initiatives such as India's abolition of the GST on sanitary napkins in 2018 and government-subsidized distribution programs under Pradhan Mantri Bhartiya Janaushadhi Pariyojana (PMBJP) have materially expanded sanitary napkin consumption in the country.

The United Nations Population Fund (UNFPA) has identified menstrual health as a development priority, catalyzing multi-stakeholder programs that are expanding the addressable market for sanitary napkin and pantyliner components in previously underserved geographies.

Hygienic Equipment Modernization in Emerging Market Food and Dairy Processing

The rapid growth of organized food, beverage, and dairy processing industries in India, Southeast Asia, Brazil, and Africa is creating an expanding demand pool for hygienic equipment components, including sanitary pumps, valves, heat exchangers, and CIP (Clean-In-Place) systems supplied by companies including Alfa Laval, GEA Group, Tetra Pak, and SPX FLOW. According to the Food and Agriculture Organization (FAO), global dairy production is projected to grow by over 20% by 2030, with the majority of incremental output concentrated in emerging markets.

The World Bank's agribusiness investment programs and regional food safety regulatory harmonization initiatives in ASEAN and Africa are compelling food manufacturers to upgrade processing facilities to meet international hygienic standards, driving sustained long-cycle procurement of certified hygienic equipment components from qualified suppliers.

Category-wise Analysis

Component Type Insights

The absorbent core is the dominant component type in the hygiene components market, accounting for approximately 29% of total market revenue. The absorbent core, comprising a blend of fluff pulp and superabsorbent polymer (SAP), is the single most critical performance component in baby diapers, adult incontinence products, and sanitary napkins, directly determining product fluid acquisition speed, gel blocking resistance, and dry-back performance.

According to the European Disposables and Nonwovens Association (EDANA), the global nonwovens and absorbent hygiene product industry consumed approximately 4.8 Million tonnes of nonwoven fabrics and absorbent materials in recent years, with absorbent core materials constituting the largest single material category by weight. Ongoing innovation in thin-core and coreless architectures using high-concentration SAP is driving product performance improvements and material efficiency gains that reinforce the absorbent core's central role in hygiene product design.

Material Type Insights

Nonwoven fabrics represent the dominant material type in the Hygiene Components Market, accounting for approximately 34% of total material revenue. Nonwoven fabrics, manufactured through spunbond, meltblown, and spunlace processes using polypropylene and polyethylene fibers, serve as the primary top sheet, acquisition layer, and outer cover material in virtually all categories of disposable hygiene products including baby diapers, adult incontinence products, sanitary napkins, and medical wipes.

According to the Association of the Nonwoven Fabrics Industry (INDA), global nonwoven fabric production reached approximately 12 Million tonnes in 2023, with hygiene applications accounting for the largest single end-use category. The European Disposables and Nonwovens Association (EDANA) similarly reports hygiene products as the primary driver of global nonwoven demand, underscoring nonwoven fabrics' foundational role across the hygiene components supply chain.

Application Insights

Baby diapers represent the dominant application segment, accounting for approximately 36% of total hygiene components market revenue. The baby diaper category generates the largest absolute consumption of hygiene components including superabsorbent polymers, nonwoven top sheets, polyethylene back sheets, elastic waistbands, and fastening tapes.

According to UNICEF, approximately 140 Million babies are born globally each year, each requiring diaper components for an average of 2-3 years, creating a vast and continuously renewing installed demand base. The global baby diaper market is further supported by rising birth rates in Africa and South Asia and increasing diaper adoption rates in emerging markets where cloth diaper usage remains prevalent. Premium product innovation, including ultra-thin cores, wetness indicators, and breathable back sheets, is driving per-unit component value escalation in developed markets.

Usability Insights

Disposable hygiene products dominate the Usability segment, accounting for approximately 83% of total hygiene components market revenue. The disposable segment's dominance reflects the deep entrenchment of single-use hygiene product culture across developed markets and the rapid adoption of disposable diapers, sanitary napkins, and adult incontinence products in emerging economies as rising disposable incomes enable consumers to transition from reusable cloth alternatives.

According to the World Bank, the global middle-income population is projected to expand by one Billion people by 2030, primarily in Asia and Africa, with rising income levels directly correlated with increased disposable hygiene product adoption. The Reusable segment, while accounting for a minority share, is growing at an above-market rate driven by sustainability-conscious consumer trends, reusable menstrual product innovation, and cloth diaper advocacy programs in developed markets.

End-user Insights

Personal care represents the dominant end-use segment, accounting for approximately 52% of total hygiene components market revenue. The personal care end-use encompasses the full range of consumer-facing hygiene products, baby diapers, sanitary napkins, pantyliners, tampons, adult incontinence products, and personal wipes, which collectively represent the largest and most diversified consumption pool for hygiene components globally.

According to the Procter & Gamble Company's annual reports, its baby, feminine, and family care business units, which rely entirely on hygiene components including SAP, nonwovens, films, and elastics, collectively generate revenues exceeding US$ 20 billion annually, illustrating the massive scale of component consumption in the personal care end-use.

Regional Insights

North America Hygiene Components Market Trends & Analysis

North America accounts for approximately 40% of the global hygiene components market in 2026. Growth is driven by a mature personal care industry, rising adult incontinence demand, and strict food and pharmaceutical hygiene regulations. Regulatory frameworks such as FSMA and strong domestic manufacturing ecosystems sustain continuous demand for high-performance hygienic materials and equipment components.

- U.S. Hygiene Components Market Size

The U.S. dominates North America with an estimated market size of USD 7.0 Billion in 2026. Growth is fueled by an ageing population, strong presence of major personal care manufacturers, and continuous investments in hygienic processing equipment across the food, dairy, and pharmaceutical industries.

Europe Hygiene Components Market Trends, Drivers & Insights

Europe holds around 25% of the global market, valued at approximately USD 6.5 Billion in 2026. The region is characterized by stringent hygiene regulations, high product penetration, and a strong sustainability push. EU directives are accelerating innovation in biodegradable materials and eco-friendly nonwoven components, while advanced manufacturing infrastructure sustains steady demand.

- Germany Hygiene Components Market Size

Germany leads Europe with an estimated USD 2.1 billion market in 2026. Strong industrial base, leading hygienic equipment manufacturers, and robust food processing and pharmaceutical sectors drive demand for certified hygienic components and advanced process systems.

- U.K. Hygiene Components Market Size

The U.K. market is estimated at USD 1.2 Billion in 2026, supported by high hygiene awareness, advanced retail supply chains, and increasing demand for sustainable personal care products. Regulatory alignment and sustainability commitments are driving innovation in recyclable and bio-based hygiene materials.

- France Hygiene Components Market Size

France is projected at USD 1.1 Billion in 2026, driven by strong demand for sustainable hygiene solutions and regulatory compliance requirements. Leading manufacturers are investing in eco-friendly absorbent materials and nonwoven technologies to meet evolving consumer and policy expectations.

Asia Pacific Hygiene Components Market Drivers & Analysis

Asia Pacific fastest growing globally with approximately 35% market share, equating to USD 11.5 Billion in 2026. Growth is fueled by large population base, rising disposable incomes, expanding hygiene awareness, and rapid growth in food processing industries. The region represents the fastest-growing market, supported by both domestic manufacturing capacity and increasing consumption.

- China Hygiene Components Market Size

China leads the region with an estimated USD 5.0 Billion market in 2026. Growth is driven by large-scale domestic production of nonwovens and superabsorbent polymers, rising middle-class consumption, and rapid expansion of hygiene product manufacturing and exports.

- India Hygiene Components Market Size

India is one of the fastest-growing markets, estimated at USD 2.2 Billion in 2026. Growth is supported by increasing awareness of feminine hygiene, government initiatives, rising income levels, and expanding domestic manufacturing of hygiene products and components.

- Japan Hygiene Components Market Size

Japan’s market is valued at approximately USD 1.5 Billion in 2026, driven by premium product demand, advanced hygiene standards, and a rapidly ageing population. Innovation in ultra-thin, high-performance absorbent materials continues to shape market growth.

Competitive Landscape

The global hygiene components market is moderately fragmented, encompassing two distinct competitive sub-segments: hygiene product material and component suppliers, including SAP producers, nonwoven manufacturers, and converting equipment specialists, and hygienic equipment component manufacturers serving food, pharma, and industrial processing. The equipment segment is led by Alfa Laval, GEA Group, Tetra Pak, Pentair, and SPX FLOW, competing on 3-A and EHEDG certification, application engineering support, and digital hygiene monitoring capabilities.

Material component suppliers compete on formulation innovation, sustainability credentials, and global supply chain reliability. Emerging business model trends include predictive maintenance service contracts, digital CIP optimization platforms, and bio-based material co-development partnerships with hygiene brand manufacturers. Strategic acquisitions and geographic expansion into high-growth Asia Pacific and Latin American markets are prominent growth strategies.

Key Developments:

- March 2025: Alfa Laval announced the launch of its next-generation AlfaNova hygienic heat exchanger series with enhanced cleanability and 3-A certification, targeting dairy, beverage, and pharmaceutical manufacturers seeking energy-efficient, fully hygienic thermal processing components.

- November 2024: GEA Group unveiled its expanded GEA Plug & Win hygienic processing system platform, integrating automated CIP (Clean-In-Place) functionality and real-time digital hygiene monitoring for food and beverage manufacturers, designed to reduce water and chemical consumption by up to 30%.

- June 2024: Ecolab introduced its ECOLAB 3D TRASAR™ digital hygiene management platform upgrade for food and beverage processing facilities, incorporating AI-driven cleaning cycle optimization, contamination risk prediction, and remote audit capabilities targeting compliance with FSMA and EU food hygiene regulations.

Hygiene Components Market- Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 21.4 Bn |

| Current Market Value (2026) | US$ 27.5 Bn |

| Projected Market Value (2033) | US$ 41.1 Bn |

| CAGR (2026 - 2033) | 5.9% |

| Leading Region | North America, 40% share |

| Dominant Application | Baby Diapers, 36% share |

| Top-ranking Product | Disposable, 83% |

| Incremental Opportunity | US$ 13.6 Bn |

Companies Covered in Hygiene Components Market

- Alfa Laval

- GEA Group

- Pentair

- SPX FLOW

- Tetra Pak

- Bürkert Fluid Control Systems

- Ecolab

- Mettler-Toledo

- Watson-Marlow Fluid Technology Group

- Donaldson Company

- Anderson-Negele

- Sani-Matic

- ITT Inc.

- Fristam Pumps

- KIESELMANN GmbH

- EVONIK Industries AG

- Freudenberg Performance Materials

- Berry Global Group, Inc.

Frequently Asked Questions

The global hygiene components market is projected to reach US$ 41.1 Billion by 2033, growing at a CAGR of 5.9% during the forecast period 2026 - 2033, from an estimated US$ 27.5 Billion in 2026. The market recorded a historical CAGR of 4.3% between 2020 and 2025, driven by global population growth, with the UN projecting 9.7 Billion people by 2050, rising hygiene product adoption in emerging markets, and surging adult incontinence demand.

The primary drivers are the global demographic transition toward an ageing population, with the WHO projecting the population aged 60+ to reach 2 Billion by 2050, and incontinence affecting 420 Million people globally, and stringent food safety and pharmaceutical processing regulations including the U.S. FDA FSMA and EU Regulation (EC) No. 852/2004, compelling sustained investment in hygienic equipment components and certified processing infrastructure.

The absorbent core dominates the component type segment with approximately 29% market share. Its leadership reflects the critical performance role of fluff pulp and superabsorbent polymer (SAP) blends in delivering fluid acquisition and retention performance across baby diapers, adult incontinence products, and sanitary napkins. EDANA reports hygiene applications as the largest single consumption category for nonwoven and absorbent materials globally, validating the absorbent core's central market position.

North America, led by the United States, is the dominant regional market, supported by major personal care converting operations anchored by Procter & Gamble and Kimberly-Clark, rigorous FDA FSMA compliance requirements driving continuous hygienic equipment investment, and a rapidly ageing population of over 58 million Americans aged 65+ per the U.S. Census Bureau, generating above-average adult incontinence component demand. Asia Pacific is the largest market by volume and the fastest growing.

Hygienic equipment modernization across rapidly expanding emerging market food, dairy, and pharmaceutical processing sectors represents the highest-growth opportunity. The FAO's projection of over 20% global dairy production growth by 2030, concentrated in India, Southeast Asia, and Africa, and ASEAN food safety regulatory harmonization, are compelling large-scale procurement of certified hygienic pumps, valves, heat exchangers, and CIP systems from suppliers including Alfa Laval, GEA Group, and Tetra Pak.

Key market participants in the hygienic equipment component segment include Alfa Laval, GEA Group, Tetra Pak, Pentair, SPX FLOW, Bürkert Fluid Control Systems, Ecolab, Mettler-Toledo, Watson-Marlow Fluid Technology Group, Donaldson Company, Anderson-Negele, Sani-Matic, ITT Inc., Fristam Pumps, and KIESELMANN GmbH. Material component suppliers active in the market include EVONIK Industries AG, Freudenberg Performance Materials, and Berry Global Group, Inc.