- LED & Lighting (Optoelectronics)

- High-Brightness Light-Emitting Diodes (LED) Headlamps Market

High-Brightness Light-Emitting Diodes (LED) Headlamps Market Size, Share, and Growth Forecast 2026 - 2033

High-Brightness Light-Emitting Diodes (LED) Headlamps Market by Product Type (Front LED Headlamps, Adaptive / Matrix LED Headlamps, Laser-LED Hybrid Headlamps, Static LED Headlamps, Smart / Connected LED Headlamps), by Technology (Standard LED, OLED-assisted LED, Matrix LED, Adaptive Driving Beam (ADB), Pixel Lighting), Vehicle Type, Application, Sales Channel, and Regional Analysis, 2026 - 2033

High-Brightness LED Headlamps Market Size and Trend Analysis

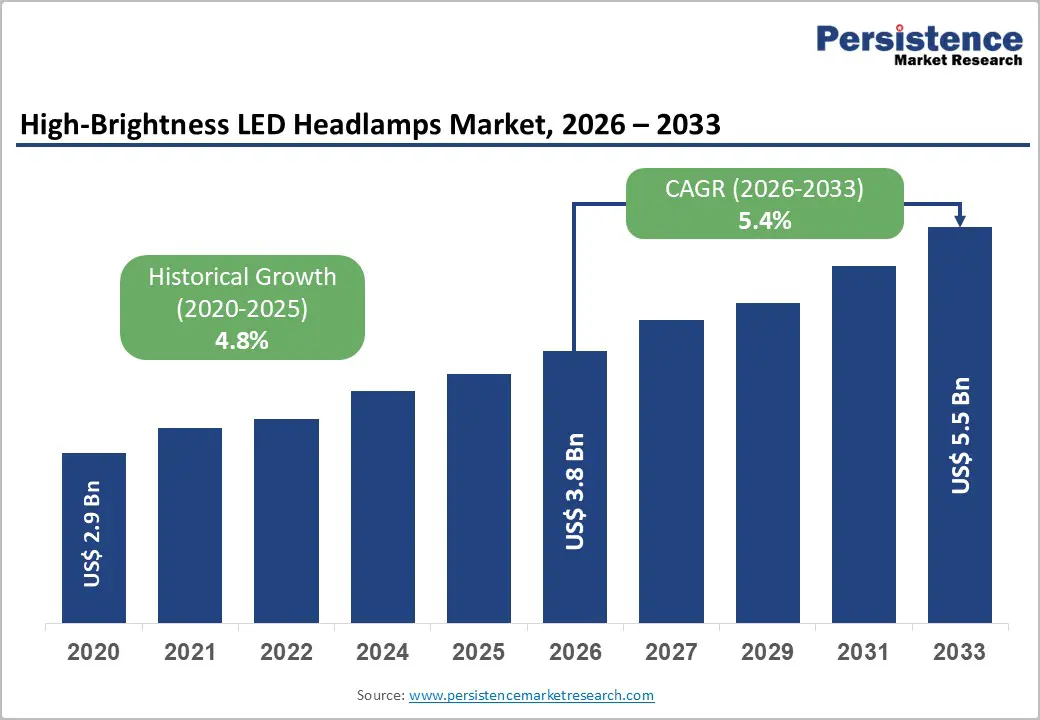

The global high-brightness light-emitting diodes (LED) headlamps market size is likely to be valued at US$3.8 billion in 2026 and is expected to reach US$5.5 billion by 2033, growing at a CAGR of 5.4% during the forecast period from 2026 to 2033.

The market is advancing on the strength of accelerating global vehicle electrification, mandatory lighting safety regulations mandating superior beam performance, and rapid consumer adoption of adaptive and intelligent lighting technologies that enhance nighttime driving safety.

Key Industry Highlights:

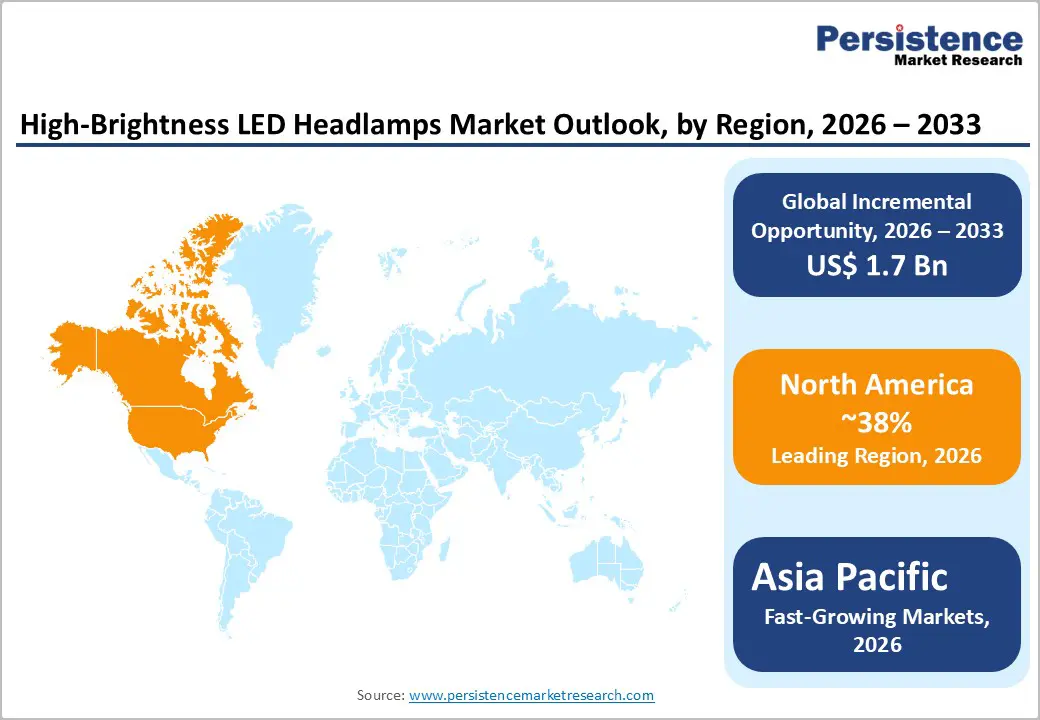

- Leading Region: Europe dominates the global High-Brightness LED Headlamps Market technology landscape holding 38% share, home to pioneering OEMs including BMW, Mercedes-Benz, and Volkswagen and Tier 1 innovators Valeo S.A. and Hella GmbH, with LED headlamps standard on the majority of new vehicles per ACEA's approximately 10.5 Million EU new car registrations in 2023.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market with rising CAGR of 6.8%, driven by China's 30 Million+ annual vehicle production, India's mandatory AHO regulation accelerating two-wheeler LED adoption, and explosive electric two-wheeler growth with the global e2W fleet surpassing 300 Million vehicles per IEA data.

- Dominant Segment: Passenger Cars lead the Vehicle Type category with approximately 55% market share, reflecting the highest absolute production volumes globally (67 Million units in 2023 per OICA) and the most advanced LED headlamp penetration rate, with LED systems now standard on the majority of new passenger car models sold in Europe.

- Fastest Growing Segment: Adaptive Driving Beam (ADB) technology is the fastest-growing technology sub-segment, catalyzed by the NHTSA's landmark 2022 regulatory approval for ADB on U.S. roads and IIHS research demonstrating up to 20% nighttime crash rate reduction from advanced headlamp systems, compelling OEM platform upgrades.

- Key Market Opportunity: NHTSA's ADB regulatory clearance in the U.S. combined with the global EV transition, with the IEA projecting 240 Million EVs by 2030, creates a dual growth catalyst for advanced pixel-LED and matrix headlamp systems, enabling manufacturers investing in ADB and connected LED platforms to capture premium OEM supply contracts across North America and globally.

| Key Insights | Details |

|---|---|

| High-Brightness LED Headlamps Market Size (2026E) | US$ 3.8 Billion |

| Market Value Forecast (2033F) | US$ 5.5 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.4% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - Stringent Global Vehicle Lighting Safety Regulations Mandating LED Adoption

Evolving automotive lighting safety regulations across major markets are compelling OEMs to adopt high-brightness LED headlamp technology as a baseline specification, displacing legacy halogen and high-intensity discharge (HID) systems. The United Nations Economic Commission for Europe (UNECE) Regulation No. 112 and Regulation No. 123 govern headlamp performance standards for adaptive front-lighting systems (AFS) and high-intensity discharge lamps respectively, with LED-specific amendments progressively raising minimum luminous intensity and beam quality thresholds.

In the United States, the National Highway Traffic Safety Administration (NHTSA) finalized a rule in 2022 allowing Adaptive Driving Beam (ADB) technology for the first time on U.S. roads, a landmark regulatory shift expected to unlock significant demand for advanced LED headlamp systems. According to the European Road Safety Observatory, inadequate or poor-quality vehicle lighting contributes to a measurable proportion of nighttime road fatalities, reinforcing the policy imperative for high-performance LED adoption.

Rapid Electrification of the Global Vehicle Fleet and EV-Specific LED Requirements

The global transition toward electric vehicles is creating a structurally differentiated demand driver for high-brightness LED headlamp systems. Unlike internal combustion engine vehicles, EVs prioritize energy efficiency at the component level, LED headlamps consume approximately 75% less energy than equivalent halogen systems per the U.S. Department of Energy (DOE), directly extending driving range.

According to the International Energy Agency (IEA), global EV sales exceeded 14 Million units in 2023, representing approximately 18% of total new car sales, with the global EV fleet projected to reach 240 Million vehicles by 2030. EV manufacturers including Tesla, BYD, and Rivian have adopted LED and matrix LED headlamps as standard equipment across their lineups, setting consumer expectation benchmarks that are cascading into conventional vehicle segments and accelerating the industry-wide transition to LED lighting systems.

Restraints - High Cost Premium of Advanced Adaptive and Matrix LED Systems

Adaptive matrix LED headlamp systems, while delivering superior road illumination and glare reduction capabilities, carry a significant price premium over conventional halogen or entry-level LED systems, limiting adoption in cost-sensitive vehicle segments and emerging market automotive markets. According to industry analyses published by the Society of Automotive Engineers (SAE International), full matrix LED systems with individual pixel control can add US$ 300-US$ 800 per headlamp unit to vehicle bill-of-materials costs.

This cost barrier restricts standard fitment of advanced LED technologies to mid-range and premium vehicle segments, with mass-market vehicles in price-sensitive markets in Southeast Asia, India, and Latin America largely retaining halogen or basic LED systems, constraining addressable market expansion in high-volume, lower-cost vehicle categories.

Thermal Management Challenges and LED Degradation in High-Intensity Applications

High-brightness LED headlamp systems generate significant thermal loads that must be managed through passive heat sinks, active cooling, or advanced thermal interface materials to prevent LED junction temperature exceedance, luminous flux degradation, and premature device failure.

According to the U.S. Department of Energy's (DOE) Solid-State Lighting Program, LED lumen maintenance and color stability are directly correlated with junction temperature control, with every 10°C increase in operating temperature reducing LED rated lifetime by approximately 50%. Inadequate thermal management in poorly engineered aftermarket replacement units and cost-optimized OEM systems can accelerate performance degradation, creating warranty liability and consumer satisfaction risks that constrain market confidence in budget-tier LED headlamp offerings.

Opportunities - Regulatory Approval of Adaptive Driving Beam (ADB) Technology in North America

The NHTSA's 2022 final rule permitting Adaptive Driving Beam (ADB) headlamp systems on U.S. roads, after decades of regulatory prohibition, represents a landmark growth catalyst for the High-Brightness LED Headlamps Market in the world's second-largest automotive market. ADB technology uses individually controllable LED pixel arrays to dynamically shape and redirect the high-beam pattern, eliminating glare for oncoming drivers while maintaining full road illumination, a capability proven to significantly improve nighttime visibility versus conventional switched high/low beam systems.

The Insurance Institute for Highway Safety (IIHS) has published research demonstrating that advanced headlamp systems can reduce nighttime crash rates by up to 20%. With major OEMs including General Motors, Ford, Toyota, and BMW actively developing ADB-equipped vehicle platforms for the U.S. market, the commercial rollout of this technology is expected to generate a significant volume upgrade cycle across the North American LED headlamp supply chain.

Booming Electric Two-Wheeler and EV Motorcycle LED Headlamp Demand in Asia Pacific

The explosive growth of electric two-wheelers (e2W) across Asia Pacific, particularly in China, India, Vietnam, and Indonesia, is creating a rapidly expanding and largely underserved demand opportunity for high-brightness LED headlamp systems tailored to two-wheeler applications. According to the International Energy Agency (IEA), the global electric two-wheeler fleet surpassed 300 Million vehicles in 2023, with China home to the vast majority.

In India, the Society of Indian Automobile Manufacturers (SIAM) reports that electric two-wheeler sales have grown from negligible levels to over 800,000 units in fiscal year 2022-23, with exponential growth projected under FAME-II and successor EV subsidy programs. LED headlamps are increasingly specified as standard equipment on mid- and premium-tier electric two-wheelers for energy efficiency and brand differentiation, creating a high-volume, cost-optimized LED headlamp demand pool that represents a significant adjacent growth market for established headlamp manufacturers.

Category-wise Analysis

Product Type Insights

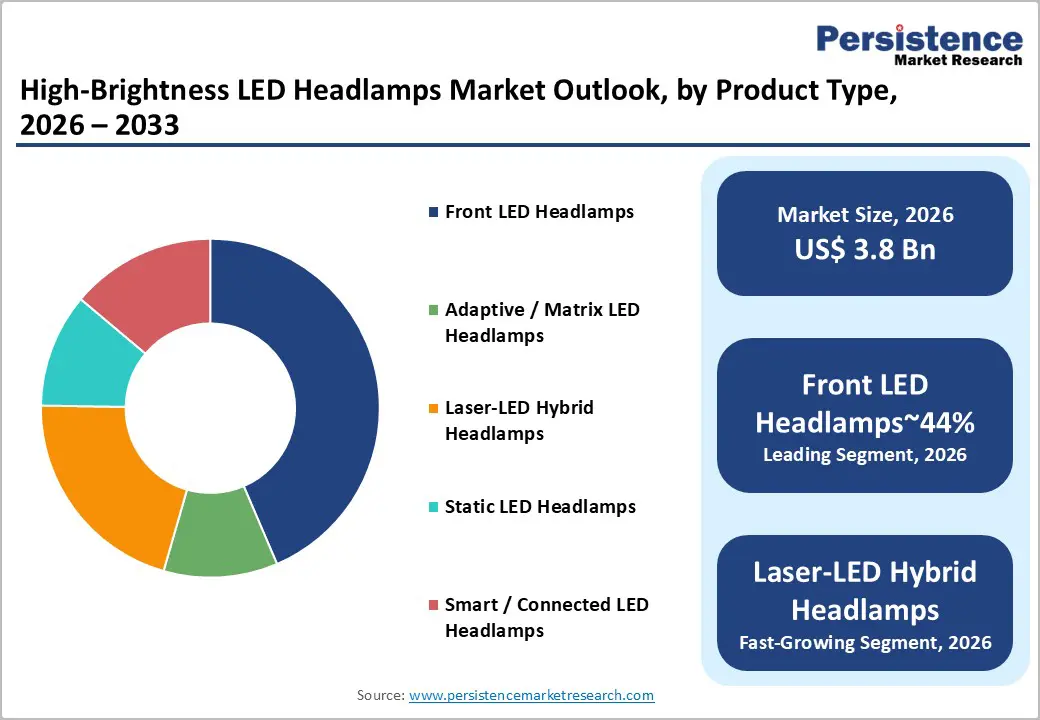

Front LED Headlamps represent the dominant product type segment, accounting for approximately 44% of total High-Brightness LED Headlamps Market revenue. Standard front LED headlamp systems, incorporating high and low beam LED modules within a fixed housing, have achieved broad penetration across passenger car and commercial vehicle platforms as automotive OEMs pursue total halogen replacement.

Their leadership reflects mature technology readiness, established supply chain infrastructure, and competitive pricing driven by LED component cost deflation over the past decade. According to the U.S. Department of Energy (DOE) Solid-State Lighting Program, the cost-per-lumen for LED lighting components has declined by more than 90% since 2008, enabling LED front headlamps to achieve cost parity with HID systems and near-parity with premium halogen configurations, accelerating OEM adoption across volume vehicle segments globally.

Technology Insights

Standard LED technology constitutes the leading technology segment, accounting for approximately 46% of total market revenue. Standard LED headlamp systems, utilizing high-flux LED packages from suppliers including Osram GmbH, Lumileds Holding B.V., and Nichia Corporation, have achieved widespread OEM adoption across passenger car, commercial vehicle, and two-wheeler platforms by delivering superior luminous efficacy, longer service life exceeding 25,000 hours, and improved beam quality versus halogen and HID predecessors.

According to the U.S. DOE, white LEDs have surpassed 200 lumens per watt in laboratory conditions, with commercial automotive-grade packages delivering efficacy levels that make them the unambiguous energy efficiency benchmark for vehicle forward lighting. Matrix LED and Adaptive Driving Beam (ADB) technologies represent the fastest-growing sub-segments within the technology category, driven by regulatory clearance and premium vehicle OEM adoption.

Vehicle Type Insights

Passenger cars dominate the vehicle type segment, accounting for approximately 55% of total High-Brightness LED Headlamps Market revenue. The passenger car segment's leadership reflects the combination of the highest absolute vehicle production volumes globally, with OICA reporting approximately 67 Million passenger cars produced in 2023, and the most rapid LED headlamp penetration rate across all vehicle categories, driven by consumer safety preferences, regulatory mandates, and OEM competitive differentiation through premium lighting features.

According to the European Automobile Manufacturers' Association (ACEA), LED headlamps are now standard equipment on the majority of new passenger car models sold in Europe, reflecting the segment's technology leadership. The Electric Vehicles sub-segment is growing fastest, as EV OEMs systematically specify LED and adaptive LED systems to optimize energy efficiency and reinforce brand technology credentials.

Application Insights

OEM (Original Equipment Manufacturer) fitment represents the dominant application segment, accounting for approximately 72% of total market revenue. OEM-fitted LED headlamp systems benefit from deep integration into vehicle electrical architecture, lighting control units (LCUs), and ADAS sensor networks, integration capabilities unavailable to aftermarket replacement units. Leading automotive OEMs including Toyota, Volkswagen Group, Stellantis, and Hyundai-Kia have progressively standardized LED headlamps across their global production platforms, driven by consumer demand, regulatory compliance, and platform engineering efficiency.

According to the Society of Automotive Engineers (SAE International), the complexity of modern matrix LED and ADB systems, which require calibration, coding, and integration with vehicle safety networks, is reinforcing the OEM channel's dominant market position and creating significant technical barriers to aftermarket substitution.

Sales Channel Insights

Dealerships represent the leading sales channel, accounting for approximately 38% of total High-Brightness LED Headlamps Market revenue through aftermarket and replacement unit sales. Authorized OEM dealerships provide brand-validated LED headlamp replacement systems with guaranteed compatibility, factory-level calibration support, and warranty coverage, attributes that command significant value among consumers seeking assured performance in safety-critical lighting applications.

According to the National Automobile Dealers Association (NADA), U.S. dealer service departments handle tens of millions of vehicle service events annually, with lighting system replacement representing a consistent revenue category. Online Retail is the fastest-growing sales channel, driven by the proliferation of e-commerce platforms, increasing consumer confidence in LED headlamp specifications, and competitive pricing for aftermarket LED upgrade kits targeting consumers in cost-sensitive replacement markets.

Regional Insights

North America High-Brightness LED Headlamps Market Trends

The United States leads the North American High-Brightness LED Headlamps Market, supported by one of the world's largest vehicle parc, exceeding 290 Million registered vehicles per the U.S. Bureau of Transportation Statistics (BTS), and a consumer preference for premium safety and lighting technology that drives above-average LED headlamp penetration among new vehicle purchases. The NHTSA's 2022 ADB rule change is the most significant regulatory development in North American automotive lighting in decades, unlocking demand for adaptive and pixel-LED headlamp systems from major OEMs that had been constrained by legacy beam-switching regulations. Key LED headlamp technology developers including Lumileds and Osram maintain R&D facilities in the U.S., reinforcing the region's innovation role.

Canada's market mirrors U.S. regulatory standards and consumer preferences, with LED headlamp adoption rates closely tracking North American OEM platform introductions. The U.S. Insurance Institute for Highway Safety (IIHS) headlamp ratings program, which evaluates and publicly ranks the performance of OEM headlamp systems annually, has become a powerful market driver, compelling automakers to upgrade LED headlamp specifications to achieve top safety ratings that influence consumer purchase decisions. This unique market dynamic has accelerated adoption of advanced LED and matrix systems in the U.S. ahead of other global markets.

Europe High-Brightness LED Headlamps Market Trends

Europe represents the most technologically advanced and dominant regional market for high-brightness LED headlamps, characterized by high LED penetration rates, the world's most sophisticated adaptive lighting regulations under UNECE, and a concentration of premium automotive brands that lead global headlamp technology innovation. Germany is the epicenter of European LED headlamp R&D, home to Hella GmbH & Co. KGaA, OSRAM GmbH, ZKW Group GmbH, and the engineering centers of global OEMs including BMW, Mercedes-Benz, and Volkswagen, which have pioneered matrix LED and laser-LED hybrid headlamp technology. According to the European Automobile Manufacturers' Association (ACEA), new car registrations in the EU totaled approximately 10.5 Million in 2023, with LED headlamps standard on the significant majority of new models.

The European Commission's General Safety Regulation (GSR 2019/2144) mandates AEBS (Advanced Emergency Braking Systems) and other active safety technologies across new vehicle categories, indirectly driving demand for high-performance LED headlamps that support camera-based safety systems requiring optimal illumination. France is home to global Tier 1 supplier Valeo S.A., a leading developer of adaptive front lighting and matrix LED systems. Spain's vehicle manufacturing sector, producing approximately 2.4 Million vehicles annually, generates substantial LED headlamp procurement demand. The United Kingdom's Vehicle Certification Agency (VCA) administers UNECE lighting regulations post-Brexit, maintaining regulatory alignment with European LED headlamp standards.

Asia Pacific High-Brightness LED Headlamps Market Trends

Asia Pacific is fastest-growing consumption market for high-brightness LED headlamps, anchored by China's dominant role as the world's largest automotive market and a global hub for LED component and headlamp module manufacturing. According to the China Association of Automobile Manufacturers (CAAM), China produced over 30 Million vehicles in 2023, with LED headlamp penetration growing rapidly across domestic brands including BYD, SAIC-GM-Wuling, and Geely, driven by consumer safety consciousness and competitive differentiation. Japan is home to the two largest global headlamp Tier 1 suppliers, Koito Manufacturing Co., Ltd. and Stanley Electric Co., Ltd., which collectively supply a significant share of global OEM headlamp production.

India is the world's largest two-wheeler market, with SIAM reporting approximately 16 Million two-wheeler sales in fiscal year 2022-23, and is experiencing rapid LED headlamp adoption driven by Ministry of Road Transport and Highways (MoRTH) regulations mandating AHO (Automatic Headlamp On) functionality for all two-wheelers, which has accelerated the transition from halogen to LED. South Korea's Hyundai Mobis Co., Ltd. is a globally significant LED headlamp developer, supplying advanced matrix LED systems for Hyundai and Kia premium vehicle platforms. Across Southeast Asia, rapidly growing vehicle markets in Thailand, Indonesia, and Vietnam are transitioning to LED headlamps in new vehicle launches, creating expanding procurement demand for both OEM and aftermarket LED headlamp systems.

Competitive Landscape

The global High-Brightness LED Headlamps Market is moderately consolidated, with a core group of automotive Tier 1 lighting specialists, Koito Manufacturing Co., Ltd., Valeo S.A., Hella GmbH & Co. KGaA, Stanley Electric Co., Ltd., and ZKW Group GmbH, commanding the majority of global OEM headlamp supply contracts. LED component suppliers including OSRAM GmbH, Lumileds Holding B.V., Nichia Corporation, and Koninklijke Philips N.V. compete at the upstream component layer.

Key differentiators include matrix pixel control density, ADB software algorithms, thermal management innovation, and ADAS integration capabilities. Emerging business model trends include lighting-as-a-service platforms and over-the-air headlamp software updates. Robert Bosch GmbH and Continental AG are leveraging sensor-lighting integration expertise for connected and autonomous vehicle headlamp systems.

Key Developments:

- February 2025: Koito Manufacturing Co., Ltd. announced mass production readiness for its next-generation 1,024-pixel matrix LED headlamp module, targeting premium passenger car OEM customers in Japan, Europe, and North America for 2026 model year vehicle platforms.

- October 2024: Valeo S.A. unveiled its Valeo SCALA® 3 automotive LiDAR-integrated headlamp system, combining high-brightness LED illumination with embedded LiDAR sensing in a single front-of-vehicle unit, targeting Level 3 autonomous driving vehicle platforms for commercial launch in 2026.

- April 2024: OSRAM GmbH introduced its SYNIOS® P2720 high-brightness LED component series specifically engineered for automotive headlamp matrix applications, offering a 15% improvement in luminous efficacy and enhanced thermal stability for pixel-LED and ADB headlamp module integration.

Companies Covered in High-Brightness Light-Emitting Diodes (LED) Headlamps Market

- Koito Manufacturing Co., Ltd.

- Valeo S.A.

- Magneti Marelli S.p.A.

- Hella GmbH & Co. KGaA

- Stanley Electric Co., Ltd.

- ZKW Group GmbH

- SL Corporation

- Varroc Lighting Systems

- Hyundai Mobis Co., Ltd.

- OSRAM GmbH

- Koninklijke Philips N.V.

- Lumileds Holding B.V.

- Nichia Corporation

- Robert Bosch GmbH

- Continental AG

- Cree LED

- Marelli Holdings Co., Ltd.

- Ichikoh Industries Ltd.

Frequently Asked Questions

The global High-Brightness LED Headlamps Market is projected to reach US$ 5.5 Billion by 2033, growing at a CAGR of 5.4% during the forecast period 2026-2033, from an estimated US$ 3.8 Billion in 2026. The market recorded a historical CAGR of 4.8% between 2020 and 2025, driven by accelerating OEM LED adoption across vehicle segments, global electrification trends, and progressive halogen phase-out mandates across major automotive markets.

The primary drivers are stringent global vehicle lighting safety regulations, including UNECE Regulation No. 112 and the NHTSA's 2022 ADB approval for U.S. roads, and the accelerating EV transition, with global EV sales exceeding 14 Million units in 2023 per the IEA. LED headlamps consume approximately 75% less energy than halogen equivalents per the U.S. DOE, making them the standard specification for energy-efficiency-focused EV OEMs globally.

Front LED Headlamps dominate the Product Type segment with approximately 44% market share, reflecting their broad penetration across passenger car and commercial vehicle platforms as OEMs execute halogen replacement programs. Their leadership is supported by significant LED component cost deflation, over 90% since 2008 per the U.S. DOE, enabling LED front headlamps to achieve cost parity with HID systems and accelerating standard fitment across volume vehicle segments globally.

Europe leads the global market in technology sophistication and LED headlamp penetration rate, home to pioneering OEMs including BMW, Mercedes-Benz, and Volkswagen, and Tier 1 innovators Valeo S.A. and Hella GmbH & Co. KGaA. The ACEA reported approximately 10.5 Million new EU vehicle registrations in 2023, with LED headlamps standard on the majority of new models. Asia Pacific is the largest market by volume and the fastest-growing, driven by China's 30 Million+ annual vehicle production.

The NHTSA's regulatory approval of Adaptive Driving Beam (ADB) technology in the U.S., combined with IIHS research demonstrating up to 20% nighttime crash reduction from advanced headlamp systems, is unlocking a significant demand upgrade cycle in the world's second-largest automotive market. Simultaneously, the booming Asian electric two-wheeler market, with the global e2W fleet surpassing 300 Million vehicles per the IEA, presents a high-volume LED headlamp opportunity in a rapidly electrifying, cost-sensitive segment.

Key market participants include Koito Manufacturing Co., Ltd., Valeo S.A., Hella GmbH & Co. KGaA, Stanley Electric Co., Ltd., ZKW Group GmbH, Hyundai Mobis Co., Ltd., OSRAM GmbH, Lumileds Holding B.V., Nichia Corporation, Robert Bosch GmbH, Continental AG, Magneti Marelli S.p.A., SL Corporation, Varroc Lighting Systems, and Koninklijke Philips N.V., alongside emerging innovators such as Cree LED (Wolfspeed) and Ichikoh Industries Ltd.