- LED & Lighting (Optoelectronics)

- Cable Blowing Equipment Market

Cable Blowing Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Cable Blowing Equipment Market by Power Type (Hydraulically Powered, Pneumatically Powered, Electric-Driven, Drill-Driven), Cable Type (Micro Duct, Normal Duct), Tube Diameter (3-16 mm, 7-12 mm, 12-63 mm), and Regional Analysis for 2026 - 2033

Cable Blowing Equipment Market Size and Trend Analysis

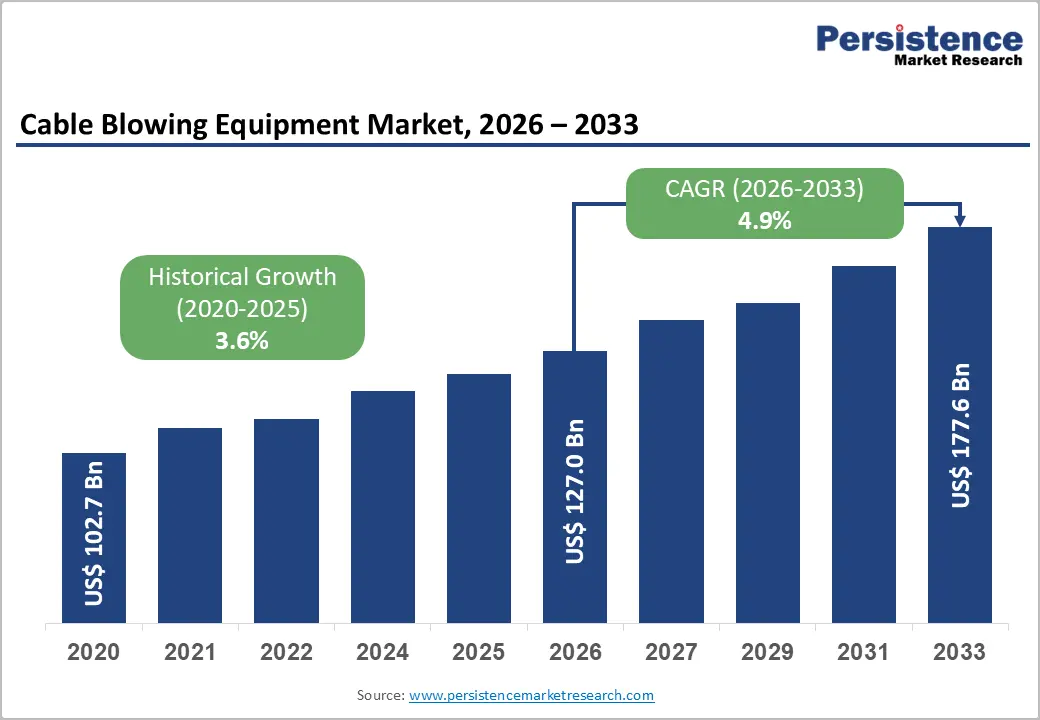

The global cable blowing equipment market size is expected to be valued at approximately US$ 127.0 billion in 2026 and is projected to reach US$ 177.6 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033. This sustained growth is fundamentally driven by the global fiber optic broadband infrastructure buildout encompassing national FTTH/FTTB programs, 5G backhaul network densification, and data centre interconnect expansion, all of which require cable blowing equipment as the primary installation method for fiber optic cables in pre-installed micro duct networks.

Key Industry Highlights:

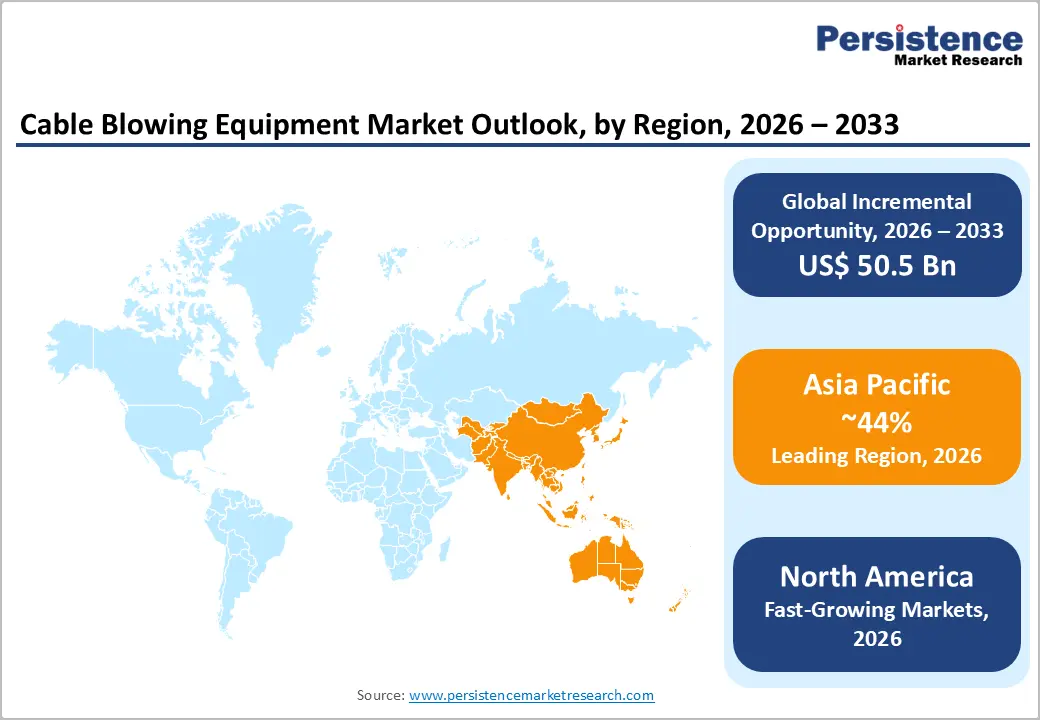

- Leading Region - Asia Pacific commands approximately 44% of the global cable blowing equipment market in 2025, anchored by China's 560 million FTTH connected households (MIIT), India's BharatNet Phase III deployment, and Japan and South Korea's ongoing 5G backhaul and F5G fiber densification programs.

- Fastest Growing Region - North America is experiencing a structural acceleration in cable blowing equipment demand driven by the BEAD Program's USD 42.45 billion broadband funding wave, the largest single public investment in U.S. telecommunications infrastructure since the Rural Electrification Act, which is creating the largest state-coordinated fiber deployment program in U.S. history.

- Dominant Power Type - Hydraulic cable blowing machines lead with approximately 42% power type market share in 2025, entrenched by their superior cable pushing force and proven reliability in long-haul backbone fiber installation applications requiring 500-3,000 meter single-pass installation distances.

- Fastest Growing Cable Type - Micro duct cable blowing is the fastest-growing segment, driven by the global FTTH industry's adoption of pre-installed micro duct network architecture endorsed by the BEAD Program, EU Gigabit Society, and ETSI technical standards as the future-proof broadband infrastructure standard.

- Key Opportunity: The BEAD Program's USD 42.45 billion U.S. fiber deployment funding with domestic content preference provisions creates an unprecedented, government-guaranteed demand event for U.S.-manufactured or U.S.-qualified cable blowing equipment that first-mover suppliers with BEAD qualification certificates are positioned to capture exclusively.

DRO Analysis

Drivers - Global FTTH and 5G Infrastructure Rollout Programs Are Creating Sustained, Government-Backed Demand for Fiber Optic Cable Installation Equipment

Cable blowing equipment manufacturers are direct beneficiaries of the global fiber-to-the-home (FTTH) and 5G network infrastructure buildout the most consequential telecommunications capital expenditure cycle in a generation as fiber optic cable blowing (air-jetting) is the predominant installation methodology for fiber deployment in pre-installed micro duct network architectures.

The European Commission's Gigabit Society connectivity targets mandate 1 Gbps broadband to all households and 480 Mbps mobile connectivity by 2030 targets that are compelling EU member states to accelerate FTTH deployment programs supported by EUR 135 billion from the Digital Decade connectivity investment framework.

In the United States, the Broadband Equity, Access, and Deployment (BEAD) Program funded at USD 42.45 billion under the Infrastructure Investment and Jobs Act (IIJA) is one of the largest publicly funded broadband infrastructure programs in U.S. history, with fiber optic deployment specified as the preferred technology standard.

Data Centre Expansion and Dense Urban 5G Small Cell Deployment Are Amplifying Demand for Precision Micro Duct Cable Blowing Solutions

Beyond residential broadband, the global proliferation of hyperscale and edge data centers, combined with 5G small cell densification in urban corridors is generating a parallel and growing demand stream for cable blowing equipment specialized in micro duct fiber installation in confined, underground, and building-interior conduit pathways.

The International Data Corporation (IDC) projects that global data centre capacity will more than double by 2030, with each new facility requiring extensive internal fiber optic cabling infrastructure installed in tight-tolerance micro duct systems where cable blowing equipment is the only practical installation method. The 5G Infrastructure Association (5GIA) has documented that dense urban 5G network deployment requires 10-15 times more fiber connections per square kilometre than 4G LTE equivalents, driving demand for compact, electric-driven cable blowing machines capable of operating in the constrained work environments of urban underground infrastructure and multi-story buildings.

Restraints - High Capital Cost of Professional-Grade Cable Blowing Machines Creates Procurement Barriers for Small Installation Contractors

Professional-grade hydraulic and pneumatic cable blowing machines capable of installing fiber optic micro duct cables at 100-3,000+ meters per session, depending on cable and duct specification, carry purchase prices of USD 15,000-60,000 per unit for full-specification commercial models, creating a significant capital threshold that constrains adoption among small and medium telecom installation contractors who would otherwise represent a large addressable market for equipment suppliers.

For independent contractors operating in developing markets where fiber program volumes are variable, and project duration is uncertain, the return on capital investment from equipment ownership is difficult to model with sufficient confidence to justify procurement suppressing equipment sales in Favor of equipment rental from larger installation firms, which reduces new unit procurement velocity.

Skilled Operator Shortage Limits Deployment Velocity and Creates Quality Assurance Risk in High-Volume Fiber Installation Programs

Cable blowing equipment operation, particularly for high-speed, long-distance micro duct fiber installation in complex conduit pathway configurations, requires trained operators capable of managing cable tension, air pressure regulation, and real-time fault detection to prevent cable damage and ensure compliant installation quality. The Fiber Broadband Association (FBA) has documented that the U.S. alone faces a shortage of tens of thousands of trained fiber installation technicians needed to meet current broadband program deployment timelines, a workforce gap that limits the pace at which cable blowing equipment can be productively deployed even when machines are available.

For fiber program contractors, skilled operator shortage creates project scheduling risk and quality assurance challenges that can generate installation defect rates that significantly increase remediation cost on long-haul micro duct cable deployments.

Opportunities - Micro Duct Cable Blowing Is the Fastest-Growing Segment, Aligned with the Global Shift to Pre-Installed Duct Network Infrastructure Architecture

The micro duct cable blowing segment represents the most dynamic and fastest-growing product category within the cable blowing equipment market driven by the global telecom industry's progressive adoption of pre-installed micro duct conduit networks that enable flexible fiber deployment, upgrades, and replacement without ground disturbance or conduit excavation.

The European Telecommunications Standards Institute (ETSI) has published technical specifications for micro duct fiber deployment methodologies that establish cable blowing as the standard installation approach for fiber cables in micro duct networks below 16 mm inner diameter, creating a regulatory and technical standards framework that makes micro duct blowing equipment procurement a specifications-driven rather than discretionary decision.

Asia Pacific's Broadband Infrastructure Gap and Active Government Program Funding Create the Largest Underpenetrated Volume Market for Cable Blowing Equipment

Asia Pacific represents the cable blowing equipment market's largest underpenetrated volume growth opportunity, where the combination of massive broadband infrastructure gaps, actively funded government connectivity programs, and rapidly expanding telecommunications operator capital expenditure cycles are creating equipment demand at a pace that existing regional distribution networks have not yet scaled to serve efficiently.

India's BharatNet Phase III programme targeting fiber connectivity to all 600,000 villages across India by 2025 represents one of the world's largest rural fiber deployment programs, with cable blowing equipment a direct and required input for every kilometre of fiber optic cable installed in the program's micro duct networks. The ASEAN Smart Cities Network and individual national broadband programs in Vietnam, Indonesia, the Philippines, and Thailand are each independently generating cable installation project pipelines that collectively represent hundreds of millions of dollars of cable blowing equipment utilization demand.

Category-wise Analysis

Power Type Insights

Hydraulically powered cable blowing machines lead the power type segment with approximately 42% market share in 2026, a position entrenched by their superior cable pushing force. Hydraulic systems generate the highest thrust-force-to-machine-weight ratios of any cable blowing power type, and their proven reliability in the most demanding long-haul fiber installation applications, including inter-city backbone networks, submarine cable landing station connections, and large-diameter duct highway infrastructure.

Hydraulically powered machines from leading manufacturers, including Plumettaz SA and Fremco, are deployed by the world's major fiber optic cable installers for projects requiring installation distances of 500-3,000 meters per blow in a single continuous pass performance specification that pneumatic and electric alternatives cannot match in equivalent equipment size categories.

Cable Type Insights

Micro Duct cable type leads the market with approximately 58% market share in 2026, reflecting the global fiber telecommunications industry's progressive adoption of micro duct conduit network infrastructure as the preferred architecture for new FTTH and 5G backhaul deployments across developed and developing markets alike.

Micro duct networks comprising small-diameter HDPE conduit tubes of 3.5-16 mm inner diameter pre-installed in underground conduit bundles enable flexible, progressive fiber deployment through cable blowing without excavation for each cable addition, providing a lifetime infrastructure investment that reduces total fiber network lifecycle cost below the alternative of direct-buried or large-conduit approaches.

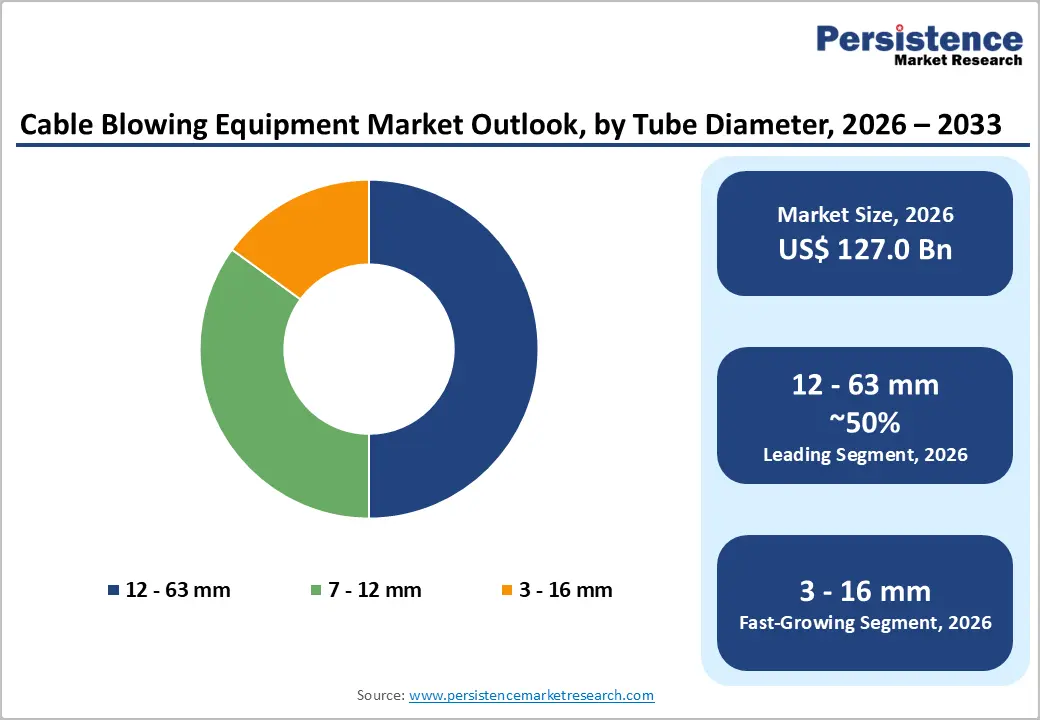

Tube Diameter Insights

The 12-63 mm tube diameter range leads the market with approximately 48% market share in 2026, serving the broadest range of mainstream telecom infrastructure applications from standard FTTH distribution ducts and campus network conduit systems to 5G backhaul direct-buried conduit networks where larger fiber ribbon cables and armored fiber cables require higher bore diameters than micro duct alternatives.

This diameter range accommodates the standard IEC 60794 outer-diameter fiber optic cable types specified in most national broadband program procurement specifications, making compatible cable blowing machines the most broadly deployable equipment category across operator, government, and contractor customer segments.

Regional Analysis

North America Cable Blowing Equipment Market Trends & Analysis

North America is experiencing a structural acceleration in cable blowing equipment demand driven by the BEAD Program's USD 42.45 billion broadband funding wave, the largest single public investment in U.S. telecommunications infrastructure since the Rural Electrification Act, which is creating the largest state-coordinated fiber deployment program in U.S. history. The FCC's National Broadband Map identifies over 42 million Americans without access to 25 Mbps/3 Mbps broadband service, with rural and tribal communities as the priority deployment targets, geographies where micro duct cable blowing is the technically and economically preferred installation method given the long rural conduit runs involved.

U.S. Cable Blowing Equipment Market Size

The United States commands approximately 82% of the North American cable blowing equipment market, with the BEAD Program's 50-state deployment programs generating multi-year fiber installation equipment demand that is unprecedented in U.S. telecommunications history. The U.S. market grows at approximately 5.2% CAGR through 2033, with equipment rental fleet expansion by major fiber contractors including MYR Group, Dycom Industries, and Mastec driving above-market equipment procurement volume as program deployment accelerates from planning into active construction phases.

Europe Cable Blowing Equipment Market Trends, Drivers, & Insights

Europe is the world's most technically mature cable blowing equipment market, where micro duct fiber deployment has been the established standard installation methodology for over two decades, particularly in the Scandinavian, Benelux, and UK markets that pioneered the technology and where equipment manufacturers, including Plumettaz (Switzerland) and Fremco (Denmark) established the global technical standards for cable blowing that are now applied worldwide.

Germany Cable Blowing Equipment Market Size

Germany holds approximately 20% of the European cable blowing equipment market, with demand driven by the federal government's ambitious Gigabitstrategie fiber rollout program targeting FTTH and FTTB coverage for all German households by 2030, one of Europe's largest nationally funded fiber broadband programs. Germany's sophisticated telecom contractor ecosystem and preference for technically advanced hydraulic cable blowing equipment sustain premium per-unit average equipment values. Germany's market grows at approximately 5.1% CAGR through 2033.

U.K. Cable Blowing Equipment Market Size

The United Kingdom represents approximately 16% of the European cable blowing equipment market, with demand sustained by Openreach's nationwide FTTP (Fiber to the Premises) rollout targeting 25 million UK premises with full-fiber connectivity and by the growing alternative network fiber operator ecosystem, including CityFibre, Hyperoptic, and Gigaclear. The UK is one of Europe's most active cable blowing equipment markets by deployment velocity.

France Cable Blowing Equipment Market Size

France accounts for approximately 14% of the European market, with demand generated by the Plan France Très Haut Débit (Very High-Speed France Plan) and the successor France Numérique 2030 strategy targeting 100% fiber coverage of French households by 2025. Orange, SFR, and Bouygues Telecom are collectively deploying millions of fiber connections annually across France's urban and rural territory each requiring cable blowing equipment as the standard installation method. France's market grows at approximately 4.9% CAGR through 2033.

Asia Pacific Cable Blowing Equipment Market Drivers & Analysis

Asia Pacific is the fastest-growing regional cable blowing equipment market, driven by the world's largest scale of active fiber broadband deployment across China, India, Japan, South Korea, and Southeast Asia simultaneously. China's telecommunications operators China Telecom, China Mobile, and China Unicom have deployed the world's largest FTTH network, connecting over 560 million households to fiber broadband per the Ministry of Industry and Information Technology (MIIT), and continued capacity expansion and quality upgrade programs sustain ongoing cable blowing equipment demand.

China Cable Blowing Equipment Market Size

China holds approximately 38% of the Asia Pacific cable blowing equipment market, operating the world's largest installed fiber broadband network with over 560 million FTTH connected households per MIIT data. China's market grows at approximately 5.5% CAGR through 2033, driven by ongoing 5G backhaul fiber densification, rural broadband extension programs, and the planned buildout of next-generation F5G (Fifth Generation Fixed Network) ultra-high-speed infrastructure that requires new fiber cable installation in upgraded micro duct systems.

India Cable Blowing Equipment Market Size

India accounts for approximately 16% of the Asia Pacific market and is the region's fastest-growing country market at approximately 6.8% CAGR through 2033. India's BharatNet Phase III programme, Jio Fiber, and Airtel Xstream Fiber are simultaneously deploying fiber infrastructure at an unprecedented scale across both urban and rural India, with cable blowing equipment essential for all micro duct fiber installation phases. India's enormous broadband infrastructure deficit relative to population represents the market's largest long-term volume growth runway.

Japan Cable Blowing Equipment Market Size

Japan represents approximately 14% of the Asia Pacific cable blowing equipment market, operating a highly advanced fiber broadband network. NTT's nationwide FTTH infrastructure covers over 95% of Japanese households, according to the Ministry of Internal Affairs and Communications (MIC) data, where demand is driven by ongoing network quality upgrades, 5G backhaul fiber densification, and enterprise campus network fiber infrastructure investment. Japan's market grows at approximately 4.7% CAGR through 2033, with precision electric-driven and drill-driven machines favoured for urban and building interior deployment scenarios.

Competitive Landscape

The global cable blowing equipment market is moderately fragmented, with European specialist manufacturers including Plumettaz SA (Switzerland), Fremco A/S (Denmark), and General Machine Products (GMP) (USA) commanding the premium hydraulic and pneumatic machine segments through decades of product development, international installation contractor relationships, and certified technical training programs that create strong distributor loyalty.

Competitive differentiation centers on machine cable-handling gentleness critical for preventing micro duct fiber cable damage during high-speed installation distance performance per blow, and compatibility certification with the major fiber and micro duct cable manufacturers' product specifications.

Key Developments:

- In September 2024, Fremco A/S introduced its Fremco Micro-Maxi next-generation micro duct cable blowing machine with integrated Bluetooth installation data logging enabling real-time installation speed, distance, and cable tension telemetry upload to cloud project management platforms targeting large-scale BEAD and FTTH program contractors requiring digital installation compliance documentation.

- In April 2024, General Machine Products (GMP) received BEAD Program equipment qualification certification for its CableWay Pro Series pneumatic cable blowing machines, positioning GMP as one of the first U.S.-manufactured cable blowing equipment brands eligible for procurement preference under the BEAD Program's domestic content preference provisions.

Cable Blowing Equipment Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 102.7 Bn |

| Current Market Value (2026) | US$ 127.0 Bn |

| Projected Market Value (2033) | US$ 177.6 Bn |

| CAGR (2026 - 2033) | 4.9% |

| Leading Region | Asia Pacific, 40% share |

| Dominant Application | Micro Duct, 58% share |

| Top-ranking Product | 12-63 mm, 48% |

| Incremental Opportunity | US$ 50.5 Bn |

Companies Covered in Cable Blowing Equipment Market

- Plumettaz SA

- Fremco A/S

- General Machine Products Co. (GMP)

- Condux International

- Lancier Kabeltechnik GmbH

- ZECK GmbH

- Durable Devices (DuraPull)

- GALIS

- Hexatronic Group

- UFI Filters

Frequently Asked Questions

The global cable blowing equipment market is valued at approximately US$ 127.0 billion in 2026. The market is projected to reach US$ 177.6 billion by 2033, expanding at an accelerated CAGR of 4.9% through the forecast period driven by the BEAD Program, EU Gigabit Society funding, and Asia Pacific broadband infrastructure investment programs.

The primary demand drivers are national broadband program investments including the U.S. BEAD Program's USD 42.45 billion fiber deployment funding and the EU Digital Decade's EUR 135 billion connectivity investment that mandate fiber optic infrastructure buildout at unprecedented scale, combined with 5G network densification requiring 10-15 times more fiber connections per square kilometre than 4G per the 5G Infrastructure Association (5GIA), directly driving cable blowing equipment demand as the standard fiber installation method for pre-installed micro duct networks.

Hydraulically Powered machines lead the power type segment with approximately 42% market share in 2025. Their dominance reflects their industry-validated superiority for long-haul backbone fiber installation applications requiring 500-3,000 meter single-pass cable blowing distances performance specifications that pneumatic and electric alternatives cannot match in comparable equipment form factors.

Asia Pacific leads the global cable blowing equipment market with approximately 44% market share in 2025. China is the dominant country within the region, having deployed the world's largest FTTH network connecting over 560 million households per MIIT data, with ongoing 5G backhaul densification and F5G infrastructure upgrade programs sustaining consistent cable blowing equipment procurement.

The leading companies in the global cable blowing equipment market include Plumettaz SA, Fremco A/S, General Machine Products Co. (GMP), Condux International, Lancier Kabeltechnik GmbH, ZECK GmbH, Hexatronic Group, and GALIS.