- Beauty & Personal Care

- Hair and Scalp Care Market

Hair and Scalp Care Market Size, Share, and Growth Forecast 2026 - 2033

Hair and Scalp Care Market by Product Type (Shampoos, Conditioners, Hair Masks & Packs, Scalp Treatments & Serums, Hair Oils, Others), Distribution Channel (Offline Retail, Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Pharmacies, Professional/Salon Use; Online Retail), Ingredient Type (Chemical-based, Natural, Vegan), End-user (Men, Women, Kids), by Regional Analysis, 2026 - 2033

Hair and Scalp Care Market Size and Trend Analysis

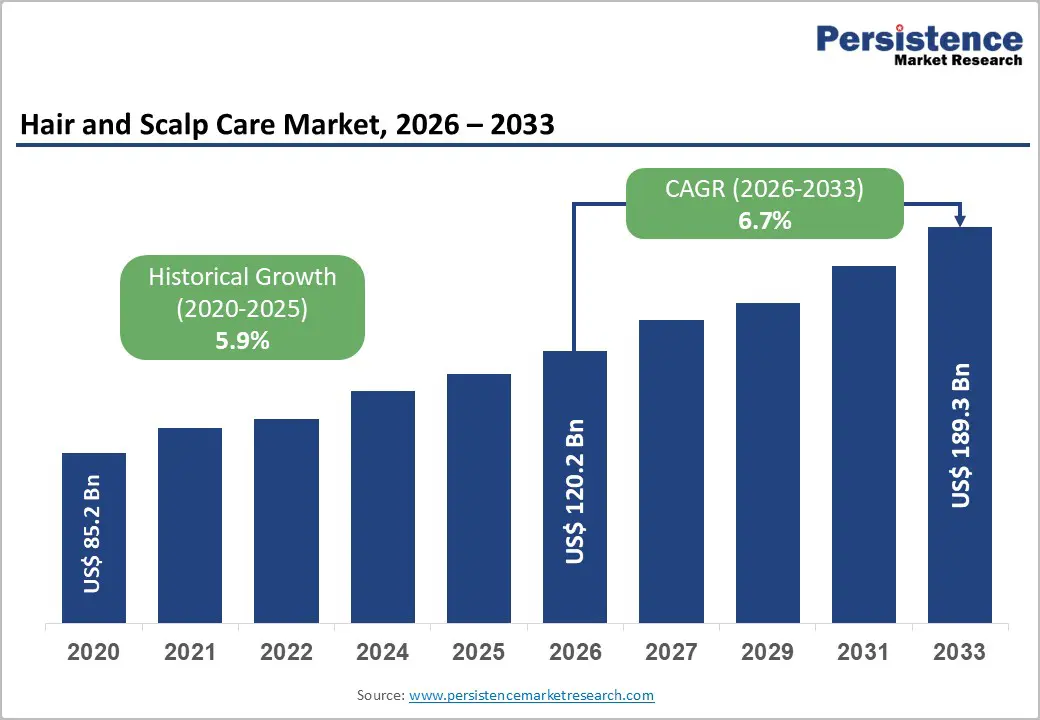

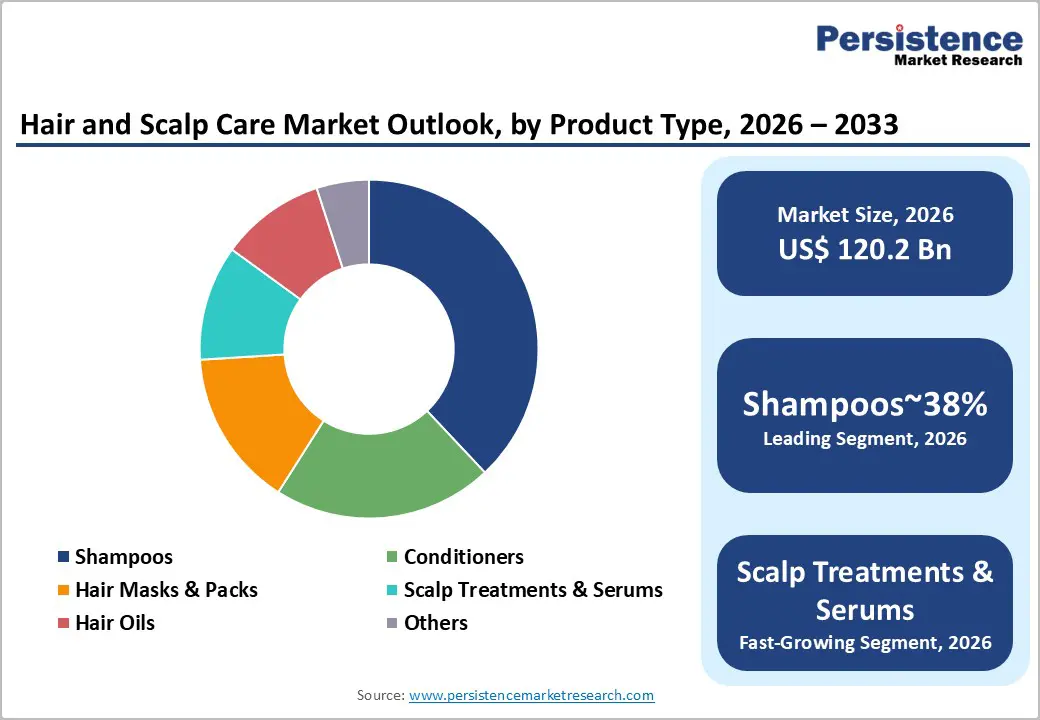

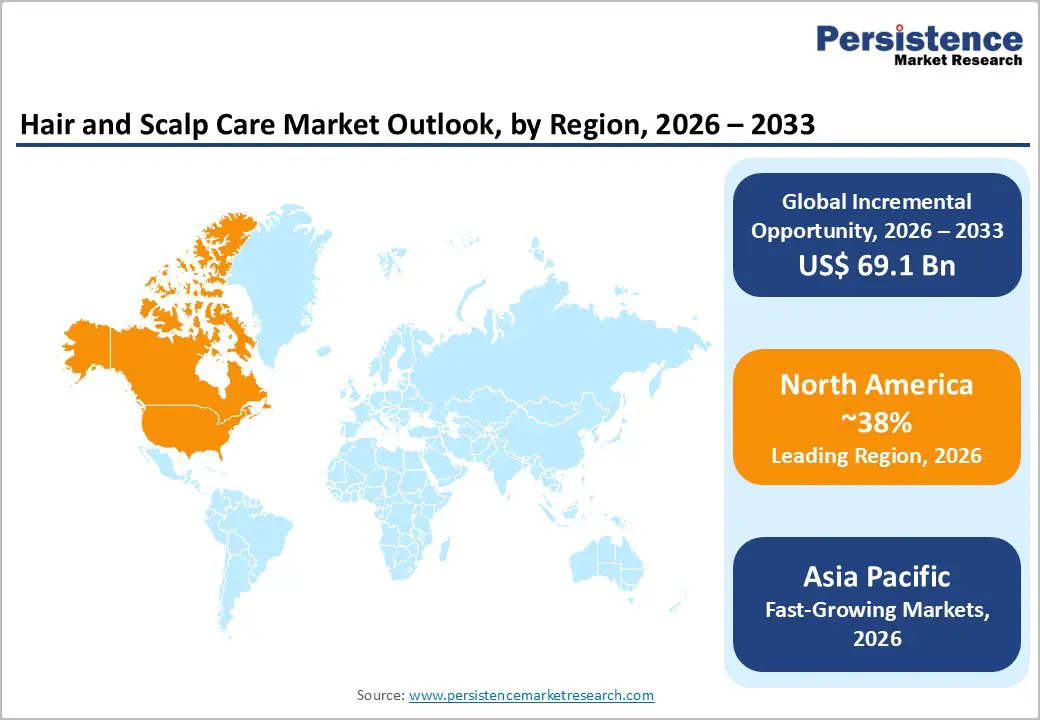

The global hair and scalp care market size is likely to be valued at US$ 120.2 billion in 2026 and is expected to reach US$ 189.3 billion by 2033, growing at a CAGR of 6.7% during the forecast period from 2026 to 2033.

The market is propelled by the convergence of rising global consumer spending on personal grooming, an accelerating shift toward scalp health awareness as a wellness priority, and the rapid proliferation of natural, vegan, and clean-label hair care formulations capturing premiumization-driven demand across developed and emerging markets alike.

Key Highlights

- Leading Region: North America, led by the United States, dominates the global Hair and Scalp Care Market holding 38% share, supported by the world's highest per-capita beauty spending, a mature salon and specialty retail ecosystem anchored by Sephora and Ulta Beauty, and a vibrant indie brand culture validated by PCPC’s reported US$ 100 Billion+ U.S. personal care industry.

- Fastest Growing Region: Asia Pacific, led by India and China, is the fastest-growing regional market, driven by India’s 600 Million+ under-25 population, Ayurvedic natural brand momentum, China’s premiumizing Gen Z consumers, and booming social commerce platforms Douyin, Tmall, and JD.com enabling rapid hair care brand scaling.

- Dominant Segment: Shampoos lead the Product Type category with approximately 38% market share, underpinned by universal purchase frequency averaging every 4-6 weeks per consumer, the broadest geographic penetration across all income levels, and continuous premiumization through clinically formulated anti-dandruff, scalp health, and color-protection variants.

- Fastest Growing Segment: Scalp treatments & serums are the fastest-growing product type, driven by the AAD’s reported 50 Million Americans experiencing alopecia, scalp microbiome science elevation to mainstream consumer awareness, and dermatologist-partnered launches from L'Oréal, The Ordinary, and Briogeo validating the clinical scalp care premium segment.

- Key Opportunity: The men’s hair and scalp care segment, targeting the 50 Million American men with pattern baldness per the AAD, combined with the global natural and Ayurvedic hair care boom validated by brands including Mamaearth and WOW Skin Science achieving international scale, represents the highest-growth dual opportunity for brand portfolio expansion by 2033.

Market Dynamics

Drivers - Rising Scalp Health Awareness and Dermatology-Backed Product Innovation

Growing consumer recognition of the scalp as an extension of facial skin requiring dedicated dermatological care is fundamentally reshaping the Hair and Scalp Care Market, driving robust demand for scalp treatment serums, pre-shampoo scalp exfoliants, and microbiome-balancing formulations. According to the American Academy of Dermatology (AAD), approximately 50 million Americans experience androgenetic alopecia (pattern hair loss), and conditions including seborrheic dermatitis and psoriasis of the scalp are among the most common dermatological presentations globally.

This clinical prevalence is creating a large and growing consumer segment seeking evidence-backed, dermatologist-recommended scalp care solutions beyond conventional shampoos. Brands including The Ordinary (DECIEM), Briogeo Hair Care, and Kérastase (a division of L'Oréal Group) have launched clinically formulated scalp serums featuring ingredients such as niacinamide, salicylic acid, and hyaluronic acid, achieving strong sell-through rates that validate the scalp health premium segment's commercial momentum.

Rapid E-Commerce Growth and Social Media-Driven Discovery of Hair Care Brands

The global acceleration of e-commerce adoption across beauty and personal care categories is dramatically expanding consumer access to specialized, direct-to-consumer, and international hair care brands, creating a structurally larger and more competitive addressable market. According to the U.S. Department of Commerce, e-commerce's share of total U.S. retail sales has grown consistently since a decade, with beauty and personal care among the fastest-growing categories online.

Social media platforms, including TikTok, Instagram, and YouTube, have become the dominant products and purchase channels for hair care, particularly among millennial and Gen Z consumers, enabling indie brands to achieve viral scale without traditional retail shelf access. The #HairCare hashtag on TikTok has accumulated billions of views, with scalp care, curly hair routines, and ingredient education content driving discovery and trial for both established brands and emerging specialized brands across global markets.

Restraints

Growing Regulatory Scrutiny of Synthetic Ingredients and Chemical Formulations

Increasing regulatory pressure on synthetic ingredients commonly used in hair care formulations, including sulfates, parabens, formaldehyde-releasing preservatives, and certain silicones, is creating reformulation costs and product development complexity for manufacturers. The European Commission's Regulation (EC) No. 1223/2009 on cosmetic products maintains a continuously updated list of restricted and prohibited substances, with hair care ingredients subject to periodic review.

In the U.S., the Modernization of Cosmetics Regulation Act (MoCRA) 2022 introduced strengthened FDA oversight requirements for cosmetic safety substantiation. These evolving regulatory requirements compel manufacturers to invest in alternative ingredient research and safety dossier development, increasing time-to-market and reformulation expenditure.

Counterfeit and Low-Quality Products Undermining Brand Equity in Online Channels

The rapid growth of online retail channels for hair care products has simultaneously enabled a proliferation of counterfeit, mislabeled, and substandard products that undermine consumer trust and brand equity for legitimate manufacturers.

According to the Organisation for Economic Co-operation and Development (OECD), counterfeit cosmetics and personal care products represent a multi-billion dollar global issue, with online marketplaces identified as primary distribution vectors. Counterfeit hair care products, particularly those replicating premium brands such as Moroccanoil, Olaplex, and Kérastase, have been documented to contain harmful undisclosed ingredients, generating consumer safety incidents and litigation risks for platform operators and brand owners.

Opportunities - Booming Men's Hair and Scalp Care Segment Driven by Grooming Normalization

The rapid expansion of the men's grooming and personal care market is creating a substantial and underserved growth opportunity for specialized hair and scalp care products targeting male consumers. According to the Personal Care Products Council (PCPC), the men's personal care segment has demonstrated consistent above-average growth rates compared to the overall personal care market, driven by generational shifts in male grooming attitudes and celebrity-driven normalization of skincare and hair care routines among men.

According to the American Academy of Dermatology (AAD), male pattern baldness affects approximately 50 million American men, creating a strong demand for clinically formulated anti-hair loss shampoos, scalp serums, and DHT-blocking topical treatments. Brands including Hims, Keeps, and Dove Men+Care (Unilever) are growing rapidly in the men's hair care segment, and mainstream brands including Procter & Gamble and L'Oréal Group are actively expanding their male-specific hair care portfolios to capture this high-growth demographic.

Rising Demand for Ayurvedic, Natural, and Clean-Label Hair Care in Asian and Global Markets

The global consumer shift toward natural, plant-based, and Ayurvedic hair care formulations, driven by ingredient transparency demands, clean beauty movement momentum, and cultural heritage reconnection particularly in South Asian and Southeast Asian markets, represents a compelling growth opportunity for brands investing in authentically sourced, naturally derived hair care.

According to the Ministry of Ayush of India, Ayurvedic and natural personal care products have experienced double-digit annual revenue growth, with traditional ingredients including amla, bhringraj, neem, and brahmi gaining global consumer recognition. The European Union's evolving natural cosmetics certification frameworks and consumer demand for COSMOS-certified organic formulations are similarly driving European brand innovation in natural hair care. Brands including Mamaearth, WOW Skin Science, and Forest Essentials have achieved rapid international expansion on the back of Ayurvedic and natural positioning, demonstrating the global commercial viability of this formulation approach.

Category-wise Analysis

Product Type Insights

Shampoos represent the dominant product type segment, accounting for approximately 38% of total hair and scalp care market revenue. Shampoos are the universal entry point and most frequently repurchased product in the hair care routine across all consumer demographics, geographies, and income levels, providing a large, stable, and continuously regenerating revenue base. According to the Personal Care Products Council (PCPC), shampoo is among the most widely purchased personal care products globally, with purchase frequency averaging every 4-6 weeks per consumer.

The shampoo segment is experiencing robust innovation-driven premiumization, with clinically formulated anti-dandruff, color-protection, keratin-strengthening, and scalp microbiome-balancing variants commanding significant price premiums over mass-market offerings. Scalp Treatments & Serums represent the fastest-growing product sub-segment, reflecting the escalating consumer investment in targeted scalp health solutions beyond cleansing.

Distribution Channel Insights

Offline retail represents the dominant distribution channel, accounting for approximately 62% of total hair and scalp care market revenue. Within offline retail, supermarkets and hypermarkets account for the largest sub-segment, serving as the primary hair care purchase venue for the majority of global consumers through their combination of broad product range, competitive pricing, and convenient co-purchasing with other household groceries.

According to the Food Marketing Institute (FMI), supermarkets remain the highest-traffic consumer retail format globally, sustaining high-volume hair care product sales for mass and mass-premium brands. Professional and salon channels, while representing a smaller revenue share, carry significant influence in driving consumer awareness of premium professional-grade formulations, including Wella Company and L'Oréal Professionnel products. Online Retail is the fastest-growing distribution channel, with e-commerce penetration in hair care accelerating across all regions.

Ingredient Type Insights

Chemical-based formulations retain the dominant position in the Ingredient Type segment, accounting for approximately 54% of total market revenue. Chemical-based hair care products, formulated with synthetic surfactants, conditioning polymers, silicones, and synthetic fragrances, deliver consistent, scientifically validated performance attributes, including lather quality, detangling efficacy, and color protection that natural alternatives have historically struggled to replicate at comparable price points for mass-market consumers.

According to the Society of Cosmetic Chemists (SCC), synthetic formulations remain the technical foundation of most mass and mass-premium hair care products globally due to their formulation stability, scalable manufacturing economics, and broad consumer acceptability. However, the Natural sub-segment is growing fastest, driven by clean beauty trends, ingredient transparency demand, and the rapidly expanding organic and Ayurvedic hair care brand ecosystem in South Asia, Southeast Asia, and Europe.

End-user Insights

Women represent the dominant end-user segment, accounting for approximately 65% of the total hair and scalp care market revenue. Women's hair care consumption reflects higher average product expenditure per capita, greater product category breadth, encompassing shampoos, conditioners, hair masks, oils, heat protectants, and scalp serums within a single consumer routine, and a stronger willingness to invest in premium formulations validated by dermatological or professional endorsements.

According to the U.S. Bureau of Labor Statistics (BLS) Consumer Expenditure Survey, women consistently outspend men on personal care products, including hair care, by a substantial margin across all income brackets. The Women segment spans the widest range of product innovation, including color-treated hair care, curl-defining systems, keratin treatments, and biotin-enriched growth formulations, sustaining continuous premium product pipeline investment from leading brands, including L'Oréal Group, Shiseido Company, and Unilever.

Regional Insights

North America Hair and Scalp Care Market Trends & Analysis

North America represents a mature yet innovation-led market, driven by premiumization, diverse hair type needs, and strong brand ecosystems. The region benefits from high per-capita spending and regulatory strengthening under MoCRA. Clean-label, dermatologically tested, and textured hair solutions continue to drive growth, supported by omnichannel retail expansion.

- U.S. Hair and Scalp Care Market Size

The U.S. is a dominant market, accounting for approximately US$ 35.5 billion by 2026, growing at ~5.6% CAGR. Growth is fueled by premium product adoption, multicultural hair care demand, and strong innovation pipelines from both legacy and indie brands.

Europe Hair and Scalp Care Market Trends, Drivers & Insights

Europe’s market is highly regulated and quality-focused, with strong demand for organic, sustainable, and salon-grade products. EU cosmetic regulations and sustainability mandates are reshaping formulations and packaging. Premium brands and professional hair care segments remain key growth drivers across major economies.

- Germany Hair and Scalp Care Market Size

Germany leads Europe with an estimated US$ 6.8 billion market by 2026, driven by strong domestic brands, high consumer awareness, and a well-established retail and salon ecosystem emphasizing quality and performance.

- U.K. Hair and Scalp Care Market Size

The U.K. market is projected to reach US$ 5.4 billion by 2026, supported by premium product penetration, e-commerce growth, and rising demand for personalized and scalp-focused treatments.

- France Hair and Scalp Care Market Size

France, a hub for beauty innovation, is estimated at US$ 5.9 billion by 2026, driven by luxury hair care brands, strong R&D capabilities, and global influence in formulation science.

Asia Pacific Hair and Scalp Care Market Drivers & Analysis

Asia Pacific is the largest and fastest-growing region, driven by population scale, rising incomes, and cultural emphasis on hair care rituals. Rapid digitalization, e-commerce penetration, and increasing demand for natural and functional products are accelerating market expansion across key countries.

- China Hair and Scalp Care Market Size

China leads the region with an estimated US$ 15.4 Billion market by 2026, growing at ~7.8% CAGR. Premiumization, social commerce platforms, and demand for scalp health solutions are major growth drivers.

- India Hair and Scalp Care Market Size

India is the fastest-growing major market, projected at US$ 8.2 Billion by 2026, with ~8.9% CAGR. Growth is driven by a young population, increasing urbanization, and strong demand for herbal and Ayurvedic formulations.

- Japan Hair and Scalp Care Market Size

Japan’s market is estimated at US$ 7.1 billion by 2026, characterized by high product sophistication, aging population needs, and strong demand for scalp care and anti-hair loss solutions.

Competitive Landscape

The global hair and scalp care market is moderately consolidated at the premium and mass-premium tiers, dominated by multinational FMCG and beauty conglomerates including L'Oréal Group, Procter & Gamble (P&G), Unilever, Henkel AG, Kao Corporation, and Shiseido Company. Key competitive differentiators include R&D investment in clinically validated formulations, portfolio breadth spanning mass to professional salon segments, digital marketing sophistication on social commerce platforms, and supply chain sustainability credentials.

Emerging business model trends include subscription-based personalized hair care platforms, such as Function of Beauty, direct-to-consumer brand scaling via TikTok Shop and Instagram, and clinical dermatologist partnership programs for scalp treatment product validation. Mid-tier specialist brands, including Moroccanoil, Briogeo, and The Ordinary, are disrupting the market through ingredient transparency and community-driven brand equity.

Key Developments:

- February 2025: L'Oréal Group launched its L'Oréal Dermatologist Solutions scalp serum range, developed in clinical collaboration with dermatologists and featuring microbiome-balancing prebiotics and salicylic acid, targeting the premium scalp health category across Europe and North America.

- October 2024: Procter & Gamble expanded its Head & Shoulders portfolio with a new premium scalp microbiome collection featuring clinically tested probiotic-derived ingredients, targeting the growing consumer segment seeking dermatologist-recommended scalp care beyond anti-dandruff treatment.

- May 2024: Unilever announced the expansion of its TRESemmé brand with a new vegan-certified, sulfate-free product line targeting Gen Z consumers across Asia Pacific and Latin America, reflecting the brand’s strategy to capture the rapidly growing clean-label and natural hair care consumer segment.

Hair and Scalp Care Market- Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 85.2 Bn |

| Current Market Value (2026) | US$ 120.2 Bn |

| Projected Market Value (2033) | US$ 189.3 Bn |

| CAGR (2026 - 2033) | 6.7% |

| Leading Region | North America, 38% share |

| Dominant Product Type | Shampoos, 38% share |

| Top-ranking End User | Women, 65% |

| Incremental Opportunity | US$ 69.1 Bn |

Companies Covered in Hair and Scalp Care Market

- Procter & Gamble (P&G)

- Unilever

- L'Oréal Group

- Johnson & Johnson

- Henkel AG

- Kao Corporation

- Shiseido Company

- Amorepacific Corporation

- Wella Company

- Revlon, Inc.

- Estée Lauder Companies

- Moroccanoil

- Oriflame Cosmetics

- Briogeo Hair Care

- The Ordinary

- Dabur India Ltd.

- Mamaearth

- Olaplex Holdings, Inc.

Frequently Asked Questions

The global Hair and Scalp Care Market is projected to reach US$ 189.3 Billion by 2033, growing at a CAGR of 6.7% during the forecast period 2026 - 2033, from an estimated US$ 120.2 Billion in 2026. The market recorded a historical CAGR of 5.9% between 2020 and 2025, driven by rising scalp health awareness, natural ingredient demand, and e-commerce-enabled brand democratization across global markets.

The primary drivers are rising scalp health awareness, with the American Academy of Dermatology (AAD) reporting approximately 50 Million Americans experiencing hair loss and scalp conditions driving demand for clinical formulations, and accelerating e-commerce adoption and social media discovery, with the U.S. Department of Commerce documenting consistent e-commerce beauty category growth and TikTok accumulating billions of hair care content views accelerating product trial.

Shampoos dominate the product type with approximately 38% share, reflecting universal consumer adoption, high repurchase frequency averaging 4-6 weeks per consumer, and continuous premiumization across anti-dandruff, scalp health, and color-protection variants. The PCPC identifies hair care, led by shampoos, as a consistently top-three U.S. personal care expenditure category, with leading brands Procter & Gamble, Unilever, and L'Oréal Group maintaining dominant positions through continuous shampoo innovation.

North America, led by the United States, is the dominant regional market supported by the world's highest per-capita beauty spending, a mature omnichannel retail ecosystem anchored by Sephora and Ulta Beauty, and the PCPC’s reported US$ 100 Billion+ U.S. personal care industry. Asia Pacific is the largest market by volume and fastest growing, with India and China driving incremental demand through youthful demographics, Ayurvedic brand momentum, and social commerce acceleration.

The men's hair and scalp care segment, targeting 50 Million American men with androgenetic alopecia per the AAD, supported by rapid growth of brands including Hims, Dove Men+Care (Unilever), and Keeps, combined with global natural and Ayurvedic hair care expansion driven by brands including Mamaearth and the Ministry of Ayush’s reported double-digit Ayurvedic personal care growth in India, represents the highest-return dual growth opportunity by 2033.

Key market participants include L'Oréal Group, Procter & Gamble (P&G), Unilever, Henkel AG (Schwarzkopf), Kao Corporation, Shiseido Company, Amorepacific Corporation, Wella Company, Johnson & Johnson, Estée Lauder Companies, Moroccanoil, Revlon, Inc., Oriflame Cosmetics, Briogeo Hair Care, and The Ordinary (DECIEM), alongside fast-growing challengers Olaplex Holdings, Mamaearth, and Dabur India Ltd.