- HVAC

- Fine Bubble Diffuser Market

Fine Bubble Diffuser Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Fine Bubble Diffuser Market by Type of Diffuser (Disc Diffusers, Tube Diffusers, Plate Diffusers, Others), Material Type (EPDM Rubber, FEPDM, Silicone, Polyurethane, Viton, Ceramic, Others), Industry (Municipal Wastewater Treatment, Industrial Wastewater Treatment (Food and Beverage, Chemical, Pharmaceutical), Aquaculture, Others), and Region Analysis for 2026 to 2033

Fine Bubble Diffuser Market Trends & Analysis

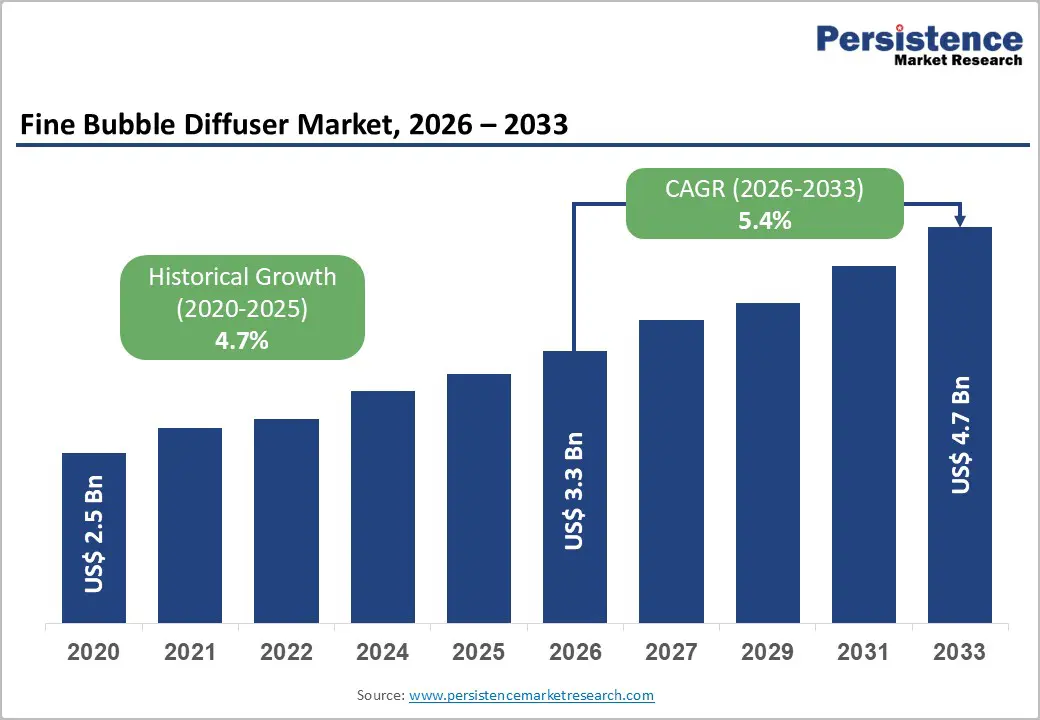

The global fine bubble diffuser market size is projected at US$ 3.3 Bn in 2026 and is projected to reach US$ 4.7 Bn by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

Global wastewater treatment infrastructure investment surpassed US$ 130 Bn annually by 2024; over 2.2 billion people lack safely managed sanitation per the WHO; EPA Clean Water Act enforcement is driving U.S. municipal plant upgrades, accelerating fine bubble diffuser procurement through 2033.

Key Industry Highlights:

- Leading Diffuser Type: Disc diffusers lead at 47.8% share; Tube diffusers grow fastest at 5.9% CAGR, driven by industrial wastewater retrofit installation advantages and food, chemical, and pharmaceutical sector treatment plant expansions globally.

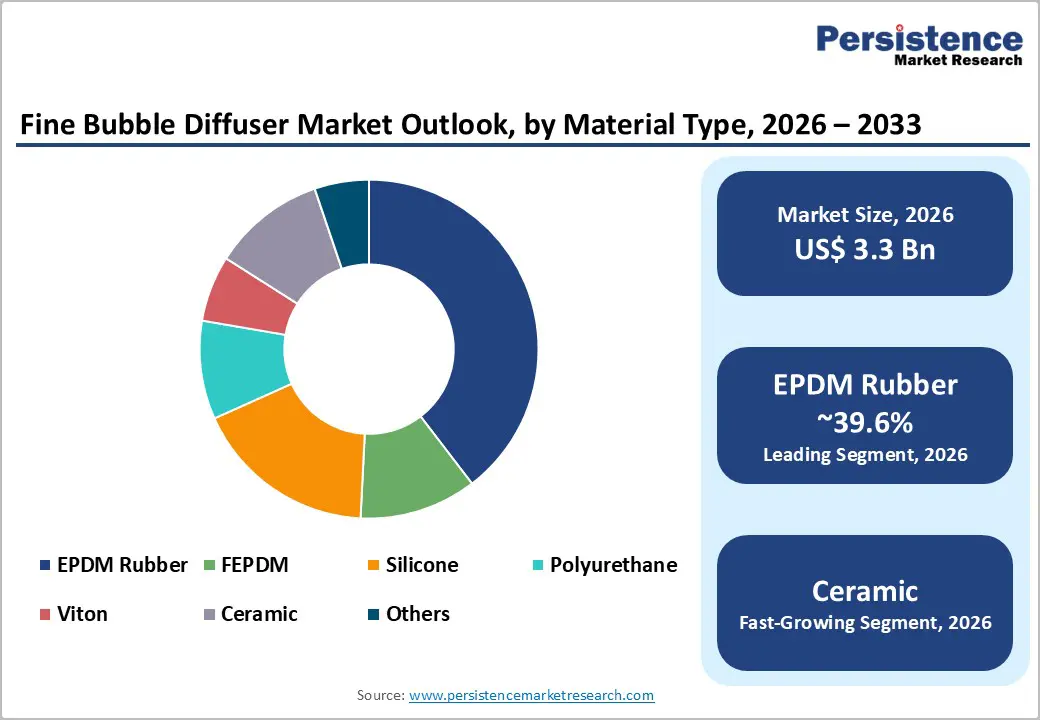

- Leading Material: EPDM rubber leads at 39.6% share; ceramic grows fastest at 6.6% CAGR, driven by pharmaceutical-grade chemical inertness requirements and aquaculture RAS biofouling-resistant surface performance specifications globally.

- Leading End-Use: Municipal Wastewater Treatment leads at 54.2% share; aquaculture is poised to achieve the fastest CAGR, driven by global RAS intensive fish and shrimp farming expansion across Norway, China, India, and Vietnam through 2033.

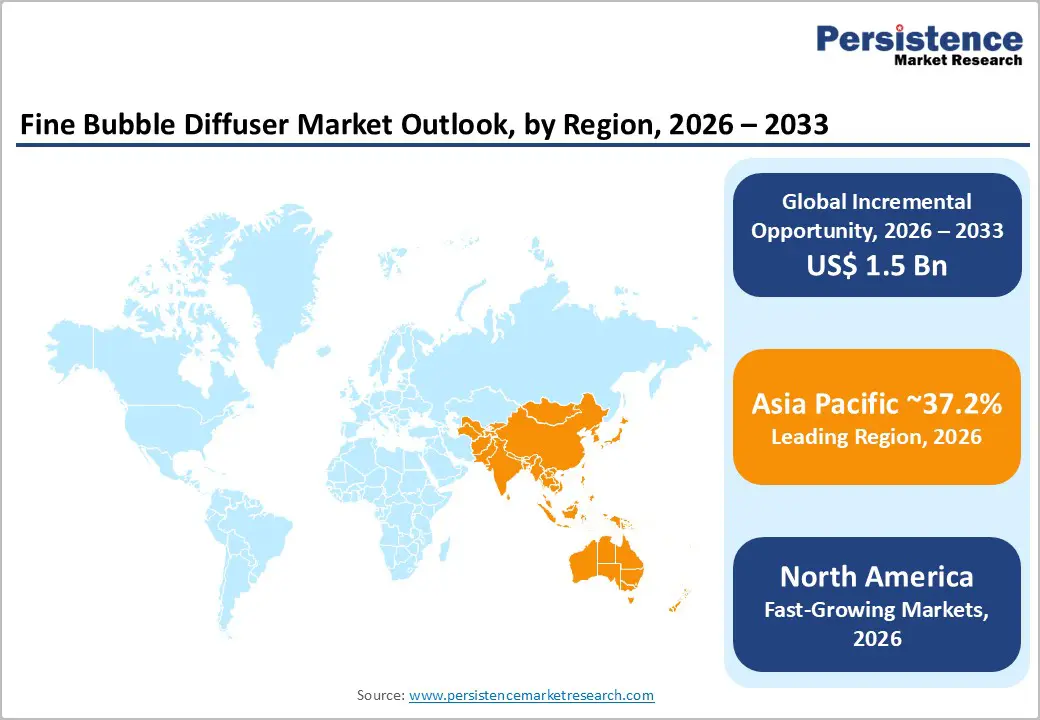

- Regional Leader: North America holds 33.5% share; Asia Pacific is likely to grow fast at 6.3% CAGR with China at US$ 427.5 Mn and India at US$ 150 Mn, anchored by NDRC wastewater mandates and AMRUT 2.0 scheme.

- Strategic Milestone: Xylem-Evoqua's BioMicrobics acquisition (January 2024) and EDI-Siemens' IoT smart aeration SCADA partnership (November 2024) signal intelligent aeration system integration as the defining competitive differentiation investment theme through 2033.

Market Dynamics Analysis

Drivers - Global Wastewater Treatment Infrastructure Modernization and Stringent Environmental Discharge Regulations

The WHO and UNICEF Joint Monitoring Programme (2023) estimates 2.2 billion people globally still lack access to safely managed drinking water and 3.5 billion lack safely managed sanitation, creating structural national policy imperatives across Asia Pacific, Latin America, and Africa to invest in new municipal wastewater treatment plant construction and upgrade programs where fine bubble diffusers are the standard aeration technology for biological treatment processes.

EPA NPDES permit tightening under the U.S. Clean Water Act, mandating nutrient removal efficiencies exceeding 85% nitrogen and phosphorus reduction at municipal plants serving populations above 10,000, is directly driving activated sludge aeration system upgrades requiring fine bubble disc and tube diffuser retrofitting programs across 16,000+ U.S. municipal wastewater treatment facilities.

The EU Urban Wastewater Treatment Directive revision (2024), expanding secondary and tertiary treatment obligations to all agglomerations above 1,000 population equivalent by 2035, is generating an estimated €35 Bn in European wastewater treatment infrastructure investment over the 2025-2035 period (EEA), with fine bubble membrane diffuser systems specified as the energy-optimal aeration technology in biological nutrient removal reactor designs across EU member state compliance programs globally. These combined regulatory and infrastructure mandates across North America, Europe, and emerging Asia Pacific create a durable, policy-anchored fine bubble diffuser procurement pipeline through 2033.

Energy Efficiency Mandates and Operational Cost Reduction Driving Fine Bubble Diffuser Adoption Over Conventional Aeration

Aeration represents 50-70% of total energy consumption in biological wastewater treatment plants (Water Environment Federation, WEF), creating powerful economic incentives for plant operators to upgrade from coarse bubble diffuser systems, with standard oxygen transfer efficiency of 8-12%, to fine bubble membrane diffuser configurations achieving 28-34% oxygen transfer efficiency and delivering 25-40% aeration energy savings per million gallons treated.

U.S. EPA Energy Star for Wastewater Plants guidelines identify fine bubble diffuser retrofitting as the single highest-ROI energy efficiency measure at activated sludge facilities, with documented payback periods of 2-4 years at US$ 0.08-0.12/kWh energy tariffs.

The IEA projects global water sector electricity consumption will grow to 1,500 TWh annually by 2030, with wastewater treatment representing the fastest-growing sub-sector at 6.8% CAGR in energy demand as treatment capacity expands to serve urbanizing populations. Fine bubble diffuser membrane upgrades, enabling compliance with both energy efficiency targets and increasingly stringent effluent quality standards simultaneously, establish the technology as the structurally preferred aeration solution for both greenfield plant design and brownfield plant upgrade procurement programs globally through 2033.

Restraints - Membrane Fouling and Biofouling Degradation Constraining Long-Term Diffuser Performance and Replacement Cycle Reliability

Fine bubble EPDM membrane diffusers are susceptible to progressive biofouling, scaling from calcium and magnesium deposits, and grease blinding in mixed-liquor environments, causing oxygen transfer efficiency degradation of 15-30% over 18-24 months of continuous operation without cleaning maintenance interventions. Municipal plants operating under constrained maintenance budgets face 6-12 month service disruption risks when biofouled diffuser grids require complete removal for acid-wash or mechanical cleaning cycles, representing a structural operational reliability limitation that constrains fine bubble diffuser adoption at under-resourced treatment facilities in emerging market regions.

Supply Chain Concentration for Specialty EPDM and FEPDM Membrane Raw Materials

EPDM and FEPDM membrane raw material production is concentrated among five major global suppliers, including Lanxess, ExxonMobil Chemical, and Dow, with specialty grades meeting wastewater-rated chemical resistance specifications subject to lead times of 12-20 weeks during peak demand periods. Supply chain disruption events, including the 2021-2023 global elastomer shortage that extended EPDM membrane delivery times to 24+ weeks, demonstrated that raw material supply concentration creates structural production capacity constraints for fine bubble diffuser manufacturers serving time-sensitive municipal plant upgrade program procurement timelines globally.

Market Opportunities

Smart Aeration Systems and IoT-Integrated Diffuser Monitoring Expanding Fine Bubble Diffuser Value Proposition

Integration of dissolved oxygen sensors, airflow monitoring analytics, and automated blower control systems into fine bubble diffuser grid installations is enabling real-time aeration optimization platforms that reduce energy consumption by an additional 15-20% beyond baseline fine bubble diffuser efficiency gains, creating a measurable incremental ROI proposition that accelerates plant upgrade decision cycles at municipal and industrial operator levels.

The global smart water market (IDC Water Technology Tracker), encompasses IoT-enabled aeration control as a core sub-segment, with fine bubble diffuser OEMs developing sensor-integrated membrane grid systems that deliver predictive maintenance alerts and performance trend analytics to plant operators via cloud-connected SCADA platforms.

Xylem's Flygt Concertor intelligent pumping and Evoqua's aeration optimization platforms demonstrate the commercial viability of IoT-enabled fine bubble diffuser system packages, with plant operators achieving verified energy savings of US$ 180,000-350,000 annually per 10 MGD treatment capacity. IoT-enabled smart diffuser systems represent the highest-margin product development opportunity for fine bubble diffuser manufacturers through 2033, with addressable premium estimated at US$ 420-580 Mn in IoT-enabled system incremental value within the broader fine bubble diffuser market.

Aquaculture Expansion and Emerging Market Wastewater Infrastructure Investment Creating New Procurement Pools

Global aquaculture production reached 94.4 million tonnes in 2022 (FAO, State of World Fisheries and Aquaculture 2024), with intensive recirculating aquaculture system (RAS) facilities expanding across Norway, China, Vietnam, and India, where fine bubble diffusers providing dissolved oxygen levels above 7 mg/L in high-density fish tank environments are mandatory for stocking density and feed conversion optimization programs.

India's aquaculture sector, growing at 8.4% CAGR (MPEDA, 2024) and expanding shrimp and tilapia RAS capacity, represents an incremental US$ 85-120 Mn fine bubble diffuser addressable market by 2030 as domestic production modernization investment programs scale.

India's AMRUT 2.0 mission, committing INR 77,640 Cr (US$ 9.3 Bn) toward urban water and wastewater infrastructure, and Indonesia's US$ 3.8 Bn sanitation master plan through 2030, collectively create the largest emerging market fine bubble diffuser procurement expansion zone outside China.

Combined with Vietnam's Mekong Delta aquaculture zone fine bubble aeration adoption and Brazil's National Sanitation Plan (PLANASA 2033) wastewater treatment expansion programs, emerging markets represent an estimated US$ 680-820 Mn in incremental fine bubble diffuser addressable market by 2030 globally.

Category-wise Analysis

Diffuser Type Insights

Disc diffusers lead the type of diffuser segment with a 47.8% market share in 2026, estimated at approximately US$ 1.56 Bn, anchored by their high specific membrane surface area per unit, modular grid installation flexibility across rectangular activated sludge tank configurations, and established EPDM membrane replacement service economics that make disc diffuser grids the standard aeration specification at municipal wastewater treatment plants globally.

Disc diffusers' bubble uniformity across the full tank floor area, generating 2-5 mm bubble diameters with 97%+ membrane coverage, delivers superior oxygen transfer uniformity versus tube and plate alternatives, sustaining their specifier preference across new plant design and brownfield retrofit programs. Tube diffusers are growing faster in industrial wastewater settings, but disc diffusers' municipal plant standardization maintains segment dominance without material displacement risk through 2033.

Tube diffusers are the fast-growing diffuser type. Tube diffusers' installation advantage in retrofit applications, enabling parallel-to-flow lateral placement, minimizing tank drainage downtime, combined with industrial wastewater treatment plant expansion across food and beverage, chemical, and pharmaceutical manufacturing facilities, drives tube diffuser adoption acceleration through 2033 globally.

Material Type Insights

EPDM Rubber leads the material type segment with a 39.6% market share in 2026, estimated at approximately US$ 1.30 Bn, reflecting its optimal combination of chemical resistance, long-term elastomeric membrane flexibility, ozone resistance, and proven 8-12-year service life at municipal wastewater treatment operating conditions across the full pH 4-12 chemical range.

EPDM rubber membranes' cost-per-unit-area advantage over silicone and FEPDM alternatives, combined with established OEM supply chains and municipal procurement specification standardization, sustains their material segment revenue dominance. Silicone offers higher temperature resistance for industrial applications, but EPDM's municipal plant specification prevalence and service-life economics maintain its segment leadership across all global geographies through 2033.

Ceramic is the fastest-growing material type at 6.6% CAGR through 2033. Ceramic diffusers' superior chemical inertness in pharmaceutical and chemical industrial wastewater treatment environments, where organic solvents and aggressive chemical loads degrade EPDM membranes rapidly, combined with aquaculture RAS facilities preferring ceramic's biofouling-resistant surface properties, are driving ceramic diffuser adoption acceleration through 2033.

Industry Insights

Municipal wastewater treatment leads the Industry segment with a 54.2% market share in 2026, estimated at approximately US$ 1.77 Bn, reflecting the segment's scale of installed diffuser grid infrastructure across over 100,000 municipal treatment plants globally, continuous government capital funding support, and stringent biological nutrient removal compliance mandates that require high-efficiency fine bubble aeration as the baseline treatment technology.

Municipal treatment's concentration of large-scale activated sludge aeration basin installations, where single plant grid replacements generate US$ 200,000-US$ 2 Mn procurement orders, sustains the segment's revenue leadership over industrial and aquaculture end-use verticals. Industrial treatment and aquaculture are growing faster in percentage terms, but municipal wastewater treatment's sheer installed base and regulatory-mandated upgrade cycles sustain end-use dominance through 2033.

Aquaculture is the fastest-growing end-user industry. Global RAS aquaculture expansion in Norway, China, India, and Vietnam, with intensive fish and shrimp stocking densities requiring precise dissolved oxygen management above 7 mg/L, is driving fine bubble diffuser adoption in aquaculture at structurally accelerating rates beyond conventional pond aeration volumes through 2033 globally.

Regional Market Insights

North America Fine Bubble Diffuser Market Trends

North America holds a 33.5% share of the global Fine Bubble Diffuser Market in 2026, estimated at approximately US$ 1.10 Bn, anchored by U.S. Clean Water Act NPDES compliance-driven municipal treatment plant upgrades, EPA energy efficiency mandates, and sustained federal infrastructure investment through the US$ 55 Bn Clean Water and Drinking Water infrastructure allocation under the Infrastructure Investment and Jobs Act across U.S. and Canadian wastewater utility capital programs.

U.S. Fine Bubble Diffuser Market: Clean Water Act Compliance, IIJA Funding, and Smart Aeration Technology Leadership

The United States holds approximately US$ 896.4 Mn in 2026, driven by 16,000+ NPDES-permitted municipal facilities facing biological nutrient removal upgrade mandates and EPA Energy Star wastewater plant guidelines promoting fine bubble diffuser retrofitting as the highest-ROI aeration upgrade measure. Xylem, Evoqua, and SSI Aeration dominate U.S. supply, with IIJA-funded state revolving fund disbursements accelerating municipal upgrade procurement. Canada contributes through municipal wastewater secondary treatment compliance programs under the Wastewater Systems Effluent Regulations (WSER).

North America's growth is reinforced by IIJA Clean Water SRF-funded treatment plant upgrades, EPA nutrient removal compliance mandates, and IoT-enabled smart aeration system adoption across major U.S. municipal wastewater utility capital investment programs through 2033.

Europe Bubble Diffuser Market Trends

Europe is likely to achieve a steady growth 3.6% CAGR through 2033, holding approximately 24.8% of global market in 2026, estimated at approximately US$ 812 Mn, driven by EU Urban Wastewater Treatment Directive revision compliance investments, Germany and France municipal plant tertiary treatment upgrade programs, and REPowerEU energy efficiency mandates reducing aeration energy consumption across the EU wastewater treatment infrastructure.

Germany Fine Bubble Diffuser Market: Regulatory Compliance and Tertiary Treatment Upgrade Programs

Germany leads Europe at approximately US$ 175.6 Mn in 2026, anchored by WABAG, Huber SE, and SSI Aeration municipal plant upgrade programs across Bavarian and North Rhine-Westphalian wastewater authorities. The U.K. drives fine bubble diffuser demand through Water Industry National Environment Programme (WINEP) compliance programs at Anglian Water, Thames Water, and Severn Trent facilities. France contributes through Grand Paris Seine Ouest treatment upgrade programs, while Spain expands under Confederaciones Hidrográficas wastewater compliance investment mandates.

Europe's EU UWWTD revision compliance programs, REPowerEU aeration energy efficiency mandates, and Germany-France-anchored tertiary treatment upgrade cycles sustain structured premium fine bubble diffuser procurement demand across European municipal wastewater utility programs.

Asia Pacific Bubble Diffuser Market Trends

Asia Pacific is the fastest-growing market at 6.3% CAGR by 2033, commanding approximately 34.2% of the global Fine bubble diffuser market share in 2025, driven by China's massive sewage treatment capacity expansion, India's AMRUT 2.0 urban water infrastructure investment, and ASEAN aquaculture sector RAS facility growth generating the world's largest incremental fine bubble diffuser procurement expansion zone.

China & India Fine Bubble Diffuser Market: Infrastructure Scale, Aquaculture Growth, and Policy-Driven Wastewater Investment

China accounts for US$ 427.5 million in 2026, driven by National Development and Reform Commission (NDRC) wastewater treatment capacity expansion programs targeting 95% urban sewage treatment rate by 2030, with SIIC Environment and Guangzhou Longji leading domestic fine bubble diffuser supply. India at US$ 150 Mn expands through AMRUT 2.0's US$ 9.3 Bn urban wastewater investment and shrimp aquaculture RAS adoption. Japan sustains Kubota and Meidensha precision fine bubble diffuser leadership, while Vietnam and Indonesia drive ASEAN aquaculture and industrial wastewater aeration demand.

Asia Pacific's China NDRC wastewater treatment expansion mandates, India AMRUT 2.0 infrastructure investment, and ASEAN aquaculture RAS sector growth position the region as the dominant global fine bubble diffuser volume and revenue growth engine.

Competitive Landscape

The global fine bubble diffuser market is moderately fragmented, with Xylem, Evoqua (Xylem), SUEZ Water Technologies, Pentair, and SSI Aeration collectively holding approximately 40-45% of global revenue share, while mid-tier and regional players including Environmental Dynamics International, Sanitaire, and KLa Systems serve geographic niche procurement programs. Proprietary EPDM membrane formulation, diffuser grid engineering design services, and long-term service agreements are primary competitive differentiation tools.

Smart IoT-enabled aeration system integration, ceramic and FEPDM specialty membrane development, emerging market geographic expansion into India and ASEAN, and municipal plant lifecycle service contract models define the dominant competitive strategic themes across all major Fine Bubble Diffuser market participants through 2033.

Strategic Developments

- In May 2023, Evoqua Water Technologies (now Xylem) acquired BioMicrobics Inc., a decentralized wastewater treatment solution provider, expanding its fine bubble diffuser-enabled biological treatment system portfolio for small-to-mid-scale municipal and onsite industrial wastewater treatment facilities across North American and international markets.

- In March 2025, Xylem Inc. expanded its Sanitaire fine bubble diffuser manufacturing capacity at its Milwaukee, Wisconsin facility, investing in automated EPDM membrane assembly lines targeting growing U.S. municipal wastewater treatment plant upgrade program demand driven by IIJA Clean Water State Revolving Fund disbursements by 2030.

- In June 2024, Fluence Corporation signed an EPC contract for a 15 MLD fine bubble aeration-equipped MABR wastewater treatment plant in Saudi Arabia, expanding its Middle East and Africa emerging market footprint as national water utility modernization investment programs under Saudi Vision 2030 generate new fine bubble diffuser procurement demand across Gulf Cooperation Council member states.

Companies Covered in Fine Bubble Diffuser Market

- Xylem Inc.

- Evoqua Water Technologies LLC

- SUEZ Water Technologies & Solutions

- Pentair PLC

- SSI Aeration Inc.

- Environmental Dynamics International (EDI)

- Aqua-Aerobic Systems Inc.

- KLa Systems Inc.

- Veolia Water Technologies

- Kubota Corporation

- Huber SE

- Sanitaire

- Fluence Corporation Limited

- VA Tech WABAG Ltd.

- Guangzhou Longji Environmental Technology Co.

Frequently Asked Questions

The fine bubble diffuser market is likely to be valued at US$ 3.3 billion in 2026, projected to reach US$ 4.7 Bn by 2033, delivering an incremental opportunity of US$ 1.4 billion by 2033.

Municipal wastewater infrastructure upgrade mandates under EPA and EU UWWTD regulations, energy-efficiency imperatives reducing aeration energy by 25-40%, and global aquaculture RAS sector expansion are the primary structural growth drivers.

The fine bubble diffuser market is likely to achieve a CAGR of 5.4% from 2026 to 2033, building on a historical CAGR of 4.7% from 2020 to 2026.

IoT-enabled smart aeration system integration delivering US$ 180,000-350,000 annual energy savings per 10 MGD plant and India AMRUT 2.0 and ASEAN emerging market wastewater infrastructure investment represent the highest-value actionable growth opportunity pools.

Xylem, Evoqua (Xylem), SUEZ Water Technologies, Pentair, SSI Aeration, EDI, Aqua-Aerobic Systems, KLa Systems, Veolia, Kubota, Huber SE, Sanitaire, Fluence, WABAG, and Guangzhou Longji are the leading global market participants.