- HVAC

- Absorption Chillers Market

Absorption Chillers Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Absorption Chillers Market by Product Type (Single-Effect Absorption Chiller, Double-Effect Absorption Chiller), Source of Energy (Steam-Driven, Hot Water Driven, Direct-Fired (Gas/Oil), Waste Heat Driven), Refrigerant Type (Lithium Bromide, Ammonia), End-User (Commercial Buildings, Industrial Facilities, Residential Buildings, Hospitals & Healthcare Facilities, Miscellaneous), and Region Analysis for 2026 to 2033

Absorption Chillers Market Share and Trends Analysis

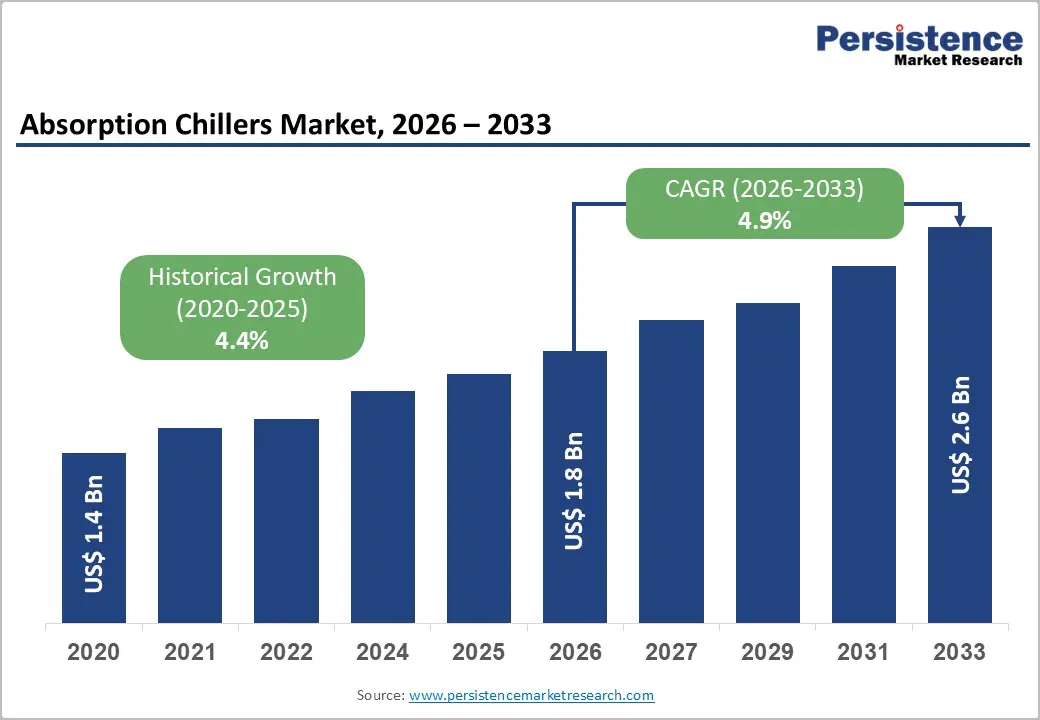

The global absorption chillers market size is anticipated at US$ 1.8 billion in 2026 and is projected to reach US$ 2.6 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

Rising industrial waste heat utilization mandates, stringent building energy efficiency regulations, and expanding district cooling infrastructure across the Asia Pacific and MENA are primary growth catalysts. The structural shift from vapor-compression systems toward thermally driven cooling, enabled by cogeneration and solar thermal integration, is expanding the addressable application base. The rise in healthcare and commercial building cooling demand in emerging economies further broadens the market's revenue foundation through 2033.

Key Industry Highlights:

- Leading Product: Double-Effect Absorption Chillers lead product type at 58.8% share; Single-Effect grows at 3.9% CAGR, driven by solar thermal compatibility and cost-sensitive emerging market deployments.

- Leading Energy Source: Steam-Driven systems dominate at 42.9% energy source share; Waste Heat Driven grows fastest at 7.0% CAGR, driven by EU EED industrial waste heat recovery mandates and cogeneration expansion.

- Leading End-user: Industrial Facilities lead end-user at 38.6% share; Miscellaneous grows fastest at 5.8% CAGR, expanding into district cooling, data centers, and net-zero campus applications.

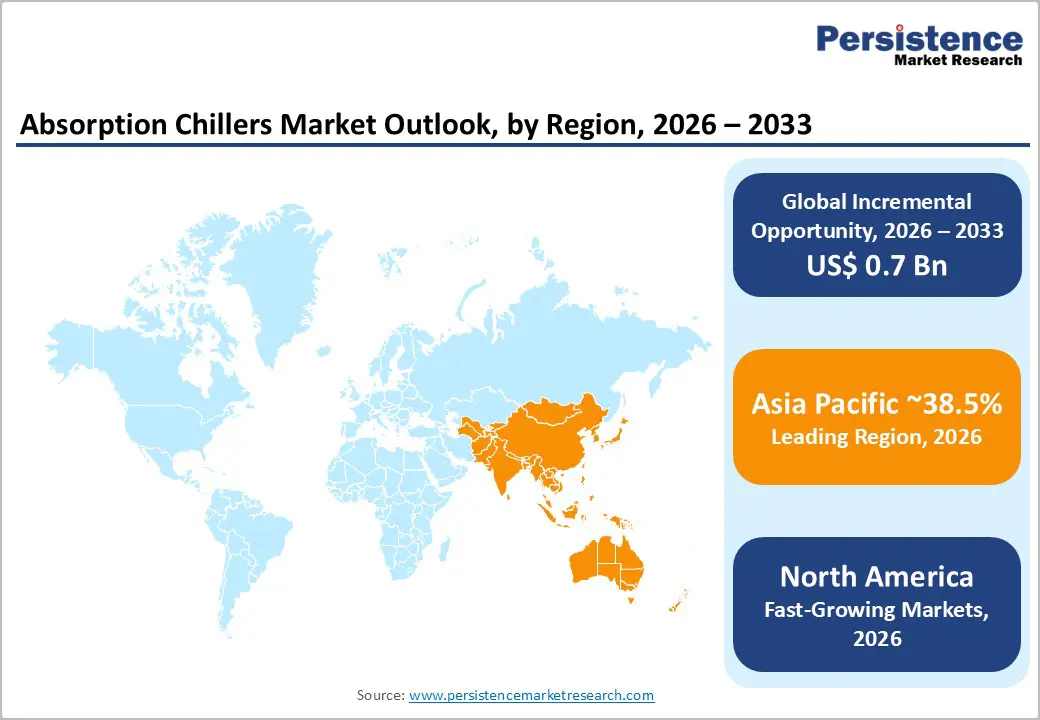

- Regional Leadership: Asia Pacific dominates at 38.5% share; China's market is estimated at US$ 318.2 Mn in 2026; North America is poised to reach at 4.9% CAGR with U.S. market at US$ 413.6 Mn.

Market Dynamics Analysis

Drivers - Energy Efficiency Regulations and Green Building Certification Mandates

Global building energy codes and green certification frameworks are directly elevating absorption chiller specifications in large commercial and institutional construction projects. The U.S. Department of Energy's Building Energy Codes Program, the EU's Energy Performance of Buildings Directive (EPBD) recast targeting near-zero energy buildings across all new constructions by 2030, and India's Energy Conservation Building Code (ECBC) collectively create regulatory pull for thermally driven cooling technologies that reduce electrical grid dependency. LEED, BREEAM, and GRIHA certification criteria, rewarding reduced electricity consumption and integration of waste or renewable heat sources, systematically favor absorption chillers over vapor-compression alternatives in project scoring frameworks.

In the Asia Pacific, China's 14th Five-Year Plan energy intensity reduction targets, requiring a 13.5% reduction in energy consumption per unit of GDP by 2025, and Japan's Top Runner Program for cooling equipment efficiency are creating structured procurement preferences for high-COP double-effect absorption systems in government-funded infrastructure. These policy frameworks directly translate into long-term specification pipelines for absorption chiller OEMs, providing multi-year revenue visibility within commercial, industrial, and institutional building sectors worldwide.

Industrial Waste Heat Recovery and Cogeneration Integration

Industrial sectors, including chemicals, refining, food processing, and power generation, produce substantial quantities of low- and medium-grade waste heat at 80°C-200°C that are structurally compatible with absorption chiller driving requirements. The U.S. EPA's Combined Heat and Power (CHP) Partnership estimates that over 6,000 CHP systems operate across U.S. industrial and commercial facilities, each representing a potential absorption chiller integration opportunity for simultaneous cooling from recovered heat. The International Energy Agency's 2023 Energy Efficiency report identifies industrial waste heat recovery as one of the top five near-term decarbonization levers globally.

In Europe, the revised EU Energy Efficiency Directive (EED, 2023) mandates energy audits for large industrial enterprises and requires feasibility assessments for waste heat recovery systems in facilities consuming over 2.77 GWh annually, directly elevating waste heat-driven absorption chiller consideration in compliance roadmaps. Petrochemical complexes in China, South Korea, and the Middle East represent particularly high-density waste heat availability zones, creating concentrated demand opportunities for double-effect and triple-effect lithium bromide absorption systems with high COP values at elevated driving temperatures aligned to industrial exhaust profiles.

Restraints - Long Installation Lead Times and Complex System Integration Requirements

Absorption chiller installations require site-specific engineering for heat source integration, whether steam, hot water, or waste heat, involving extensive piping, heat exchanger design, and thermal load balancing work that extends project timelines by 6-18 months compared to plug-and-play vapor-compression alternatives. This complexity constrains adoption in retrofit markets where building downtime is commercially prohibitive. The availability of certified HVAC engineers with specialized absorption system expertise is limited globally, creating skilled labor bottlenecks that delay commissioning timelines and increase project risk exposure for building owners and EPC contractors managing tight delivery schedules.

Competition from Advancing Electric Cooling Technologies and Heat Pump Systems

High-efficiency electric vapor-compression chillers and heat pumps, benefiting from rapidly improving COP values, declining compressor costs, and growing renewable electricity availability, present intensifying competitive pressure against absorption systems in markets where electricity costs are moderate or declining. The European heat pump market grew 40% in 2022 (European Heat Pump Association), with next-generation electric heat pumps achieving COP values of 4.0-6.0 that directly challenge absorption chiller efficiency narratives in mild-climate applications. As electrical grid decarbonization accelerates, the operating emission advantage of thermally driven absorption systems narrows structurally, requiring OEMs to sharpen waste heat and solar thermal integration value propositions.

Opportunities - District Cooling Network Expansion in MENA and Southeast Asia

District cooling systems, centralized chilled water production distributed across urban building clusters, represent one of the largest structural growth opportunities for large-capacity absorption chillers, particularly in high-ambient-temperature regions where cooling loads are sustained year-round. The Middle East's district cooling market, led by Emaar, Tabreed, and Emicool in the UAE, is among the world's fastest-growing, with Abu Dhabi's district cooling capacity targeted to exceed 1.5 million refrigerant tons by 2030 under the UAE's energy efficiency strategy.

Singapore's Building and Construction Authority mandates district cooling connectivity for new developments in Marina Bay and one-north precincts, while Saudi Arabia's NEOM and Red Sea Project gigaprojects are incorporating large-scale district cooling infrastructure with waste heat and solar thermal absorption chiller integration. For absorption chiller manufacturers, district cooling projects represent high-value, large-capacity procurement events, individual projects specifying 1,000-10,000 RT systems, creating concentrated revenue opportunities that meaningfully exceed standard commercial building replacement cycles. This segment's addressable market is estimated to represent US$ 400-600 Mn in incremental absorption chiller opportunity by 2033.

Solar Thermal-Driven Absorption Cooling in Emerging Markets

Solar thermal energy, particularly concentrating solar and evacuated tube collectors generating 80°C-200°C thermal output, is structurally matched to single-effect and double-effect absorption chiller driving requirements, creating a compelling solar cooling opportunity in high-irradiation developing markets. The International Renewable Energy Agency (IRENA) identifies solar cooling as a key technology for decarbonizing space cooling in tropical and subtropical regions, particularly Sub-Saharan Africa, South Asia, and Latin America, where grid reliability is limited and cooling demand is growing at 5-8% annually.

India's Solar Cities Program and the EU-funded DESOLINATION and SOLARADSORPTION demonstration projects have validated solar-driven absorption cooling at an institutional scale. With solar thermal collector costs declining 35% over the past decade and government renewable energy subsidies in India, Morocco, and Brazil creating favorable economics, solar-absorption cooling systems are approaching commercial viability for hospitals, food storage, and educational institutions in off-grid and weak-grid environments. The addressable solar-absorption cooling market in emerging economies is estimated to reach US$ 300-450 Mn by 2033, representing a structurally new demand channel beyond traditional industrial and commercial segments.

Category-wise Analysis

Product Type Insights

Double-effect absorption chillers lead the product type segment with a commanding 58.8% market share in 2026. Their dominance reflects superior Coefficient of Performance (COP) values of 1.2-1.4 compared to 0.6-0.8 for single-effect systems, enabling significantly lower operating energy costs per ton of refrigeration in high-load industrial and district cooling applications.

Double-effect systems' compatibility with high-temperature steam and industrial cogeneration exhaust profiles aligns precisely with the energy characteristics of large-scale industrial facilities, power plants, and process industries that represent the market's highest-value procurement segments. While Single-Effect systems serve cost-sensitive and low-temperature-source applications, Double-Effect dominance is expected to strengthen as waste heat recovery and cogeneration deployment scale through 2033.

Single-Effect Absorption Chillers are the fastest-growing product type at a CAGR of 3.9% through 2033. Their lower capital cost, compatibility with solar thermal and low-grade waste heat sources, and suitability for smaller commercial and residential building applications are driving adoption in emerging market installations and solar cooling demonstration projects.

Source of Energy Insights

Steam-driven absorption chillers lead the source of energy segment with a 42.9% market share in 2026. Steam represents the most widely available industrial utility across refining, chemical, pharmaceutical, and power generation facilities, enabling direct absorption chiller integration into existing plant utility infrastructure without additional heat exchange equipment. Steam-driven double-effect absorption systems achieve the highest COP values in the segment, making them the preferred specification in large industrial and district cooling applications where thermal efficiency directly impacts operating cost economics.

Hot water driven and direct-fired systems address mid-range commercial applications, while waste heat driven systems are gaining traction but remain constrained by site-specific heat source availability. Steam-driven leadership is expected to remain stable through 2033. Waste heat-driven absorption chillers are the fastest-growing energy source segment at 7.0% CAGR through 2033. Tightening industrial energy efficiency regulations under the EU EED and China's 14th Five-Year Plan, combined with the expanding cogeneration installed base globally, are structurally increasing waste heat availability and driving integration investment.

Refrigerant Type Insights

Lithium bromide refrigerant systems dominate the refrigerant type segment with an overwhelming 88.6% share in 2026. Lithium bromide-water systems are the industry standard for large-capacity commercial and industrial air conditioning applications, offering non-toxic operation, zero ozone depletion potential, zero GWP, and regulatory compliance across all major markets. Their high COP values in double-effect configurations, compatibility with standard steel construction materials, and established global service and maintenance networks reinforce OEM and specifier preference.

Ammonia-water systems serve specialized industrial refrigeration applications requiring sub-zero temperatures, a fundamentally distinct application from LiBr's comfort cooling domain, ensuring that Lithium Bromide maintains a dominant revenue share without structural competitive risk from ammonia through the forecast period.

Ammonia refrigerant systems are the fastest-growing segment at a CAGR of 3.8% through 2033. Industrial refrigeration requirements in food and beverage processing, cold chain logistics, and chemical manufacturing, where sub-zero temperatures are operationally essential, are driving steady demand for ammonia-based absorption systems globally.

End-User Insights

Industrial facilities lead the end-user segment with a 38.6% market share in 2026. Industrial end-users represent the highest-value absorption chiller procurement segment, driven by dual operational imperatives of process cooling and waste heat monetization, with absorption systems enabling facilities to simultaneously reduce cooling electricity costs and recover otherwise-wasted thermal energy from manufacturing or power generation processes. Petrochemical plants, refineries, food processing facilities, and pharmaceutical manufacturers represent the core industrial procurement base. Commercial Buildings follow as the second-largest segment, while Hospitals and Residential applications are growing in share. Industrial dominance is expected to be sustained through 2033, reinforced by expanding industrial cogeneration and energy audit compliance mandates.

Miscellaneous end-users represent the fastest-growing segment at a CAGR of 5.8% through 2033. District cooling networks, data centers, and educational campuses adopting net-zero energy targets are collectively expanding absorption chiller deployment into application categories beyond traditional industrial and commercial building boundaries.

Regional Market Insights

North America Absorption Chillers Market Insights

North America holds a considerable share of the global Absorption Chillers Market, growing at a prominent 4.9% CAGR through 2033, with the U.S. market estimated at ~US$ 413.6 Mn, anchored by its industrial cogeneration base and green building regulatory framework.

U.S. Absorption Chillers Market Trends

The U.S. EPA's CHP Partnership and DOE Building Energy Codes Program create structured demand for waste heat-driven and steam-powered absorption chillers across industrial and commercial facilities. U.S. LEED certification frameworks incentivize thermally driven cooling in large commercial buildings, while growing data center and pharmaceutical manufacturing cooling requirements are expanding the addressable industrial base.

Canada Absorption Chillers Market Insights

Canada contributes to the demand from its industrial process sectors. North America's market growth is driven by industrial waste heat recovery mandates, green building certification adoption, and the expanding district cooling infrastructure in Southern U.S. urban developments requiring high-capacity thermally driven cooling systems.

Europe Absorption Chillers Market Insights

Europe holds a 24.6% share of the global absorption chillers Market in 2025, anchored by regulatory leadership under the EU Energy Efficiency Directive and the European Green Deal, positioning the region as a premium absorption chiller innovation and specification hub globally.

Germany Absorption Chillers Market

Germany accounts for approximately US$ 120.3 Mn, underpinned by its dense industrial base of chemical, automotive, and manufacturing facilities generating high-grade waste heat compatible with double-effect absorption systems, alongside Continental European OEM leadership from EAW Energieanlagenbau.

The EU's revised Energy Efficiency Directive (2023) mandates waste heat recovery feasibility assessments for large industrial consumers, directly embedding absorption chiller evaluation into regulatory compliance workflows across Germany, France, Spain, and the U.K. Europe's growth is anchored by Spain and France's solar-absorption cooling demonstration investments, EU carbon border adjustment mechanisms raising fossil cooling operating costs, and circular energy economy policy driving industrial waste heat utilization programs across member states.

Asia Pacific Absorption Chillers Market Insights

Asia Pacific commands the dominant 38.5% share of the global Absorption Chillers Market in 2025 and is the fastest-growing region, driven by the world's largest industrial manufacturing base, accelerating district cooling infrastructure, and government energy intensity reduction mandates.

China & India Absorption Chillers Market: Expansion

China is the single largest national market, estimated at US$ 318.2 Mn in 2026, anchored by its mass-scale industrial cogeneration base, 14th Five-Year Plan energy intensity targets, and domestic OEM leadership from Broad Group and Shuangliang. Japan leads in high-efficiency double-effect and triple-effect absorption system R&D with Mitsubishi Heavy Industries, Hitachi, and Kawasaki Thermal Engineering, while India represents a high-growth sub-market driven by industrial park expansion, pharmaceutical manufacturing cooling requirements, and solar cooling demonstration programs.

Asia Pacific's manufacturing scale advantages, government energy efficiency incentive programs, and rapidly expanding district cooling infrastructure make it the most strategically critical region for absorption chiller volume and investment through 2033.

Competitive Landscape

The global absorption chillers market is moderately fragmented, with leading players, Thermax, Johnson Controls, Broad Group, Shuangliang, and Trane, collectively holding approximately 40% of global revenue in 2025. Regional OEMs in Japan, China, and India command significant domestic share alongside global HVAC conglomerates. Market leaders differentiate through high-COP double-effect system portfolios, integrated waste heat engineering capabilities, and long-term service agreement models that generate recurring maintenance revenues.

Technology innovation in triple-effect systems and IoT-integrated chiller controls, geographic expansion into MENA district cooling and South Asian industrial markets, and service contract bundling as a lifecycle revenue strategy define the dominant competitive themes shaping the absorption chiller industry landscape through 2033.

Strategic Developments

- In September 2024, Broad Group advanced its direct-fired natural gas absorption chiller deployment across ASEAN district cooling projects in Thailand and Vietnam, investing in regional service infrastructure to support post-commissioning long-term maintenance contracts for multi-MW cooling installations.

- In March 2024, Johnson Controls integrated IoT-enabled remote performance monitoring across its YORK absorption chiller product line, enabling predictive maintenance algorithms that reduce unplanned downtime by up to 30% for industrial and commercial facility operators.

Companies Covered in Absorption Chillers Market

- Thermax Limited

- Johnson Controls International plc

- Broad Group

- Shuangliang Eco-Energy Systems

- Trane Technologies plc

- Carrier Global Corporation

- Mitsubishi Heavy Industries Ltd.

- Hitachi Appliances Inc.

- LG Electronics Inc.

- Yazaki Corporation

- EAW Energieanlagenbau GmbH

- Kawasaki Thermal Engineering Co. Ltd.

- Robur S.p.A.

- Ebara Corporation

- Century Corporation

Frequently Asked Questions

The absorption chillers market is valued at US$ 1.8 Bn in 2026, projected to reach US$ 2.6 Bn by 2033.

Industrial waste heat recovery mandates, building energy efficiency regulations, and expanding district cooling infrastructure in MENA and Asia Pacific are the primary growth drivers.

The market is projected to grow at a CAGR of 4.9% from 2026 to 2033.

District cooling network expansion in MENA and Southeast Asia and solar thermal-driven absorption cooling commercialization in emerging markets represent the most actionable near-term growth opportunities.

Thermax, Johnson Controls, Broad Group, Shuangliang, Trane Technologies, Carrier, Mitsubishi Heavy Industries, Hitachi, LG Electronics, and Yazaki Corporation are the leading global participants.