- Pharmaceuticals

- Fentanyl Market

Fentanyl Market Size, Share, and Growth Forecast, 2026 - 2033

Fentanyl Market by Product Type (Injectable, Lozenges & Tablets, Nasal Sprays, Patches), Route of Administration (Oral, Intravenous, Transdermal Patch, Subcutaneous, Epidural Administration), and Regional Analysis for 2026 - 2033

Fentanyl Market Size and Trends Analysis

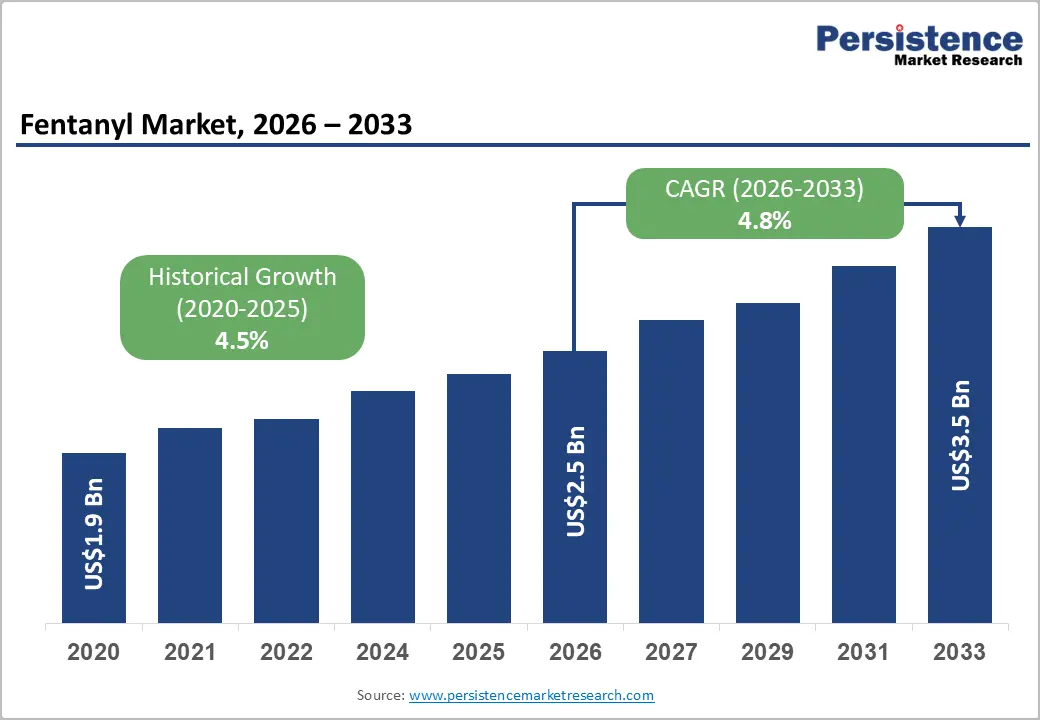

The global fentanyl market size is likely to be valued at US$2.5 billion in 2026 and is expected to reach US$3.5 billion by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033, driven by its critical role in managing severe and breakthrough pain, particularly in care and intensive care settings.

As a highly potent synthetic opioid analgesic, fentanyl remains an essential component of hospital anesthesia protocols and palliative care regimens where rapid onset and controlled dosing are clinically necessary. The NHPCO (National Hospice and Palliative Care Organization) is the biggest non-profit organization (NPO) leading palliative care programs and hospice in North America. According to NHPCO, around 36.6% out of the patients, who were admitted to palliative care centers, were experiencing disease, and the remaining (63.4%) were experiencing non-malignant conditions. Technological advancements in drug delivery systems, including transdermal patches, sublingual tablets, lozenges, and intranasal formulations, continue to enhance therapeutic precision, patient compliance, and safety in controlled environments.

Key Industry Highlights:

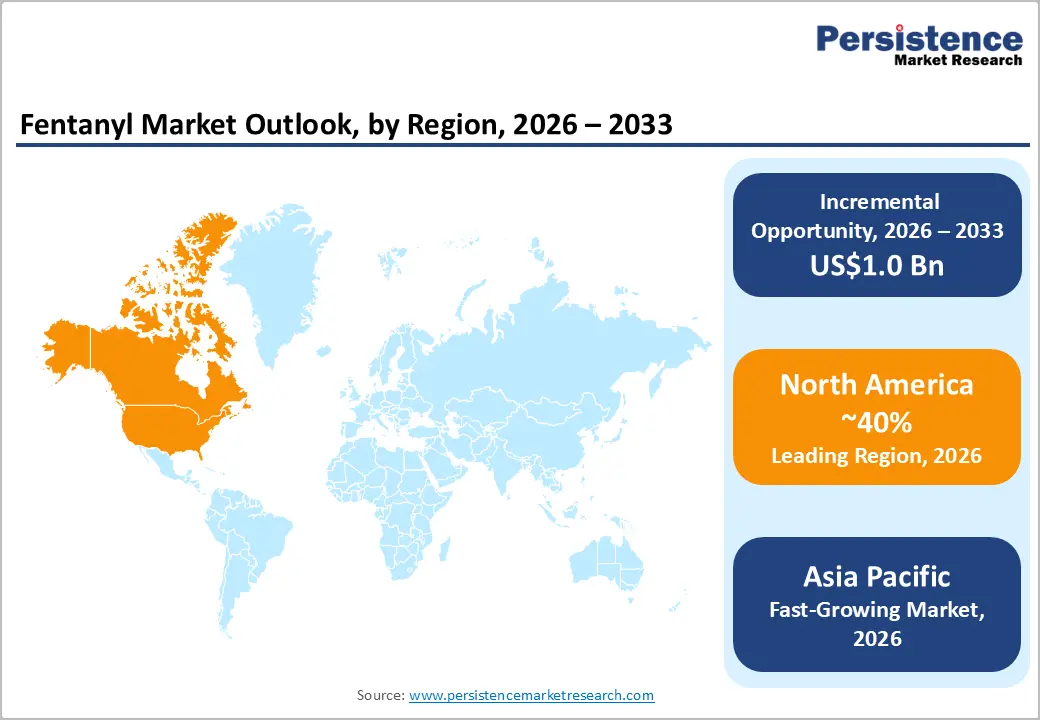

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by strong hospital infrastructure, advanced oncology care, and strict regulatory oversight supporting controlled clinical use.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region for Fentanyl in 2026, supported by expanding healthcare infrastructure, rising oncology demand, and strengthening regulated manufacturing capacity.

- Leading Product Type: Patches are projected to represent the leading product type in 2026, accounting for 45% of the revenue share, driven by strong demand for long-acting chronic pain management, improved patient compliance, and preference for controlled, non-invasive drug delivery systems.

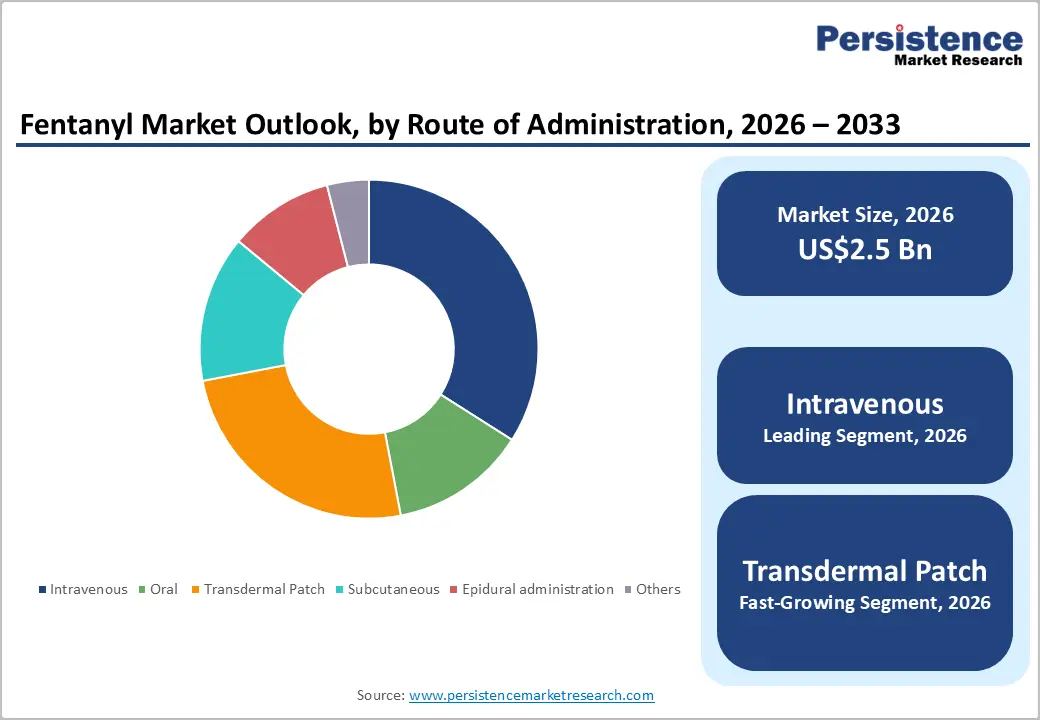

- Leading Route of Administration: Intravenous is anticipated to be the leading route of administration, accounting for over 50% of the revenue share in 2026, supported by its critical role in anesthesia induction, surgical procedures, and intensive care settings requiring rapid onset and precise titration.

| Key Insights | Details |

|---|---|

| Fentanyl Market Size (2026E) | US$2.5 Bn |

| Market Value Forecast (2033F) | US$3.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Prevalence of Chronic Pain and Cancer

Cancer patients frequently experience severe and breakthrough pain requiring potent opioid analgesics, particularly in advanced stages of disease. Fentanyl’s high potency and rapid onset make it suitable for managing refractory pain when other opioids prove insufficient. Expanding oncology treatment programs, improved diagnostic capabilities, and longer survival rates among cancer patients have collectively increased the need for structured pain management protocols. Hospitals and palliative care centers rely on regulated fentanyl formulations to ensure effective symptom relief while maintaining clinical supervision and controlled dispensing practices worldwide.

Chronic non-cancer pain conditions, including neuropathic disorders, musculoskeletal degeneration, and post-traumatic complications, support sustained demand for fentanyl in controlled medical settings. As awareness of comprehensive pain management grows, healthcare providers increasingly adopt multimodal analgesic strategies incorporating opioids for carefully selected patients. Breakthrough pain episodes, particularly among opioid-tolerant individuals, necessitate rapid-acting formulations such as injectable and transmucosal products. The expansion of specialty pain clinics and palliative care infrastructure strengthens legitimate pharmaceutical consumption.

Aging Population and Increased Surgical Procedures

Individuals aged sixty-five and older are more likely to experience chronic illnesses, degenerative joint conditions, cancer, and cardiovascular diseases that require surgical intervention and advanced pain control. Elderly patients often present complex comorbidities demanding potent, fast-acting analgesics administered under strict medical supervision. Fentanyl's pharmacokinetic profile, including rapid onset and controlled duration, makes it particularly valuable in perioperative and postoperative care. As life expectancy increases worldwide, healthcare systems are witnessing higher procedural volumes, reinforcing demand for reliable anesthesia agents.

In the context of age-related disease burden, advancements in minimally invasive surgery, organ transplantation, and interventional cardiology have broadened the range of procedures that demand precise anesthesia management. Intravenous fentanyl continues to be a key agent in both operating rooms and intensive care units due to its titratable dosing and reliable hemodynamic stability. With the growing number of procedures in ambulatory surgical centers, the demand for pharmaceuticals has strengthened. The adoption of enhanced recovery after surgery (ERAS) protocols highlights the importance of balanced analgesia, often incorporating fentanyl as part of controlled regimens.

Barrier Analysis - Stringent Regulatory Oversight and Production Quotas

National authorities enforce strict manufacturing quotas, prescription monitoring programs, and controlled substance scheduling requirements that limit production volumes and distribution channels. These safeguards, while essential for public health protection, can restrict supply flexibility and slow market expansion. Pharmaceutical manufacturers must comply with detailed reporting, storage, and transportation standards, increasing operational complexity. Regulatory audits and compliance costs also add financial burdens, particularly for smaller producers seeking to enter or expand within highly controlled opioid segments.

Prescription limitations and mandatory risk evaluation programs influence market dynamics by restricting prescribing patterns to specific clinical indications and opioid-tolerant populations. Healthcare providers often face administrative requirements, including patient education, consent documentation, and monitoring obligations. While these measures enhance patient safety, they may discourage broader utilization even in legitimate therapeutic scenarios. International trade of active pharmaceutical ingredients is similarly regulated, requiring cross-border approvals and licensing compliance.

Public Health Stigma and Prescriber Hesitancy

Heightened awareness of opioid misuse crises has led to increased scrutiny of all opioid prescriptions, including medically necessary fentanyl formulations. Media attention and policy debates often associate fentanyl with illicit abuse rather than controlled clinical application, contributing to stigma among patients and healthcare providers. This environment can result in prescriber hesitancy, with physicians opting for alternative analgesics even when fentanyl may offer appropriate therapeutic benefits under supervision.

Healthcare institutions increasingly implement conservative opioid stewardship programs to minimize liability and ensure compliance with public health directives. While these initiatives strengthen safety standards, they may also reduce prescribing frequency. Patients, particularly elderly individuals or those in chronic pain, may resist opioid therapy due to fear of dependency or social stigma. Educational efforts continue to differentiate regulated pharmaceutical use from illicit misuse, yet perception challenges remain influential.

Opportunity Analysis - Development of Next-Generation Abuse-Deterrent Formulations

Manufacturers are investing in advanced formulation science to reduce tampering, extraction, and unintended misuse while preserving therapeutic efficacy. Features such as tamper-resistant patches, unit-dose packaging, and bio-adhesive transmucosal systems enhance controlled administration and patient safety. Regulatory agencies increasingly support development pathways for products demonstrating improved risk mitigation profiles, encouraging research into safer opioid delivery technologies.

Abuse-deterrent innovation also strengthens market differentiation in a competitive environment dominated by generics. Companies that successfully integrate safety mechanisms into transdermal and intranasal systems can gain regulatory preference and institutional trust. Digital integration, including smart packaging and adherence monitoring tools, enhances responsible use in outpatient and palliative settings. As healthcare systems emphasize balanced access and safety, next-generation formulations align with policy objectives, presenting sustainable commercial opportunities while addressing societal concerns regarding opioid misuse.

Technological Convergence in Delivery

Technological convergence in drug delivery systems offers meaningful expansion prospects for the pharmaceutical fentanyl market. Advances in transdermal matrix systems, precision nasal sprays, and micro-dosing technologies improve pharmacokinetic consistency and patient adherence. Enhanced bioavailability and controlled-release mechanisms allow optimized dosing with reduced variability, supporting safer outpatient administration. Integration of device engineering with pharmaceutical science creates differentiated products that align with evolving clinical requirements.

Digital health technologies are increasingly incorporated into pain management frameworks. Smart delivery platforms capable of tracking dosage timing, adherence, and usage patterns provide valuable data for healthcare providers. Such innovations support personalized treatment strategies and strengthen regulatory compliance through improved monitoring. Telemedicine growth and home-based palliative care expansion amplify demand for convenient, technology-enabled delivery options.

Category-wise Analysis

Product Type Insights

Patches are expected to lead the fentanyl market, accounting for approximately 45% of revenue in 2026, driven by strong demand for long-acting chronic pain management, particularly among cancer and palliative care patients requiring continuous opioid delivery. Patches offer controlled release over extended durations, enhancing patient compliance by reducing the need for frequent dosing compared to short-acting formulations. A prime example is Janssen Pharmaceuticals Inc. and its renowned Duragesic brand, which helped establish transdermal fentanyl as a standard treatment option for long-term pain management in regulated medical practice.

Nasal sprays are expected to be the fastest-growing segment, driven by the rising demand for rapid relief of breakthrough cancer pain in opioid-tolerant patients. Their quick onset of action and non-invasive administration make them ideal for oncology and ambulatory care settings, where immediate symptom control is essential. For instance, Instanyl Pharmaceutical Company, with its specialized portfolio that includes intranasal fentanyl products like PecFent in select markets, showcases regulatory-approved nasal fentanyl formulations already in clinical practice.

Route of Administration Insights

Intravenous is projected to lead the market, capturing around 50% of the revenue share in 2026, supported by its critical role in anesthesia induction, surgical procedures, and intensive care management, where rapid onset and precise titration are essential. Hospitals rely on intravenous fentanyl for controlled perioperative analgesia and hemodynamic stability during complex interventions. The ability to rapidly adjust dosing under clinical supervision ensures both safety and effectiveness in high-acuity settings. For example, injectable fentanyl from Hikma Pharmaceuticals PLC is commonly used in hospital anesthesia protocols within regulated healthcare systems.

Transdermal patch is likely to be the fastest-growing route of administration in 2026, driven by increasing preference for long-term pain control in outpatient and palliative settings. This method enhances convenience through reduced dosing frequency and improved adherence, particularly among elderly and chronic pain patients. Expansion of home-based healthcare services and value-based treatment models strengthens the adoption of patch-based therapies. For example, Mallinckrodt Pharmaceuticals highlights ongoing investments in patch technologies aimed at addressing chronic pain management within regulated pharmaceutical frameworks.

Regional Insights

North America Fentanyl Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by advanced hospital infrastructure and structured pain management protocols. Demand remains concentrated in regulated clinical environments such as operating rooms, intensive care units, oncology centers, and palliative care facilities. Rising surgical volumes, increasing cancer prevalence, and a growing elderly population requiring complex pain control are reinforcing stable utilization of injectable and transdermal formulations. Opioid stewardship programs and prescription monitoring systems are shaping controlled prescribing behavior.

Another notable trend is the shift toward safer formulations and hospital-focused generics, driven by established pharmaceutical companies. These companies are emphasizing high-quality manufacturing, reliable supply, and strict adherence to regulatory standards. For instance, Hikma Pharmaceuticals PLC provides injectable fentanyl products that are widely used in U.S. hospitals for anesthesia and critical care. The company's strong presence in sterile injectables ensures consistent availability within regulated healthcare systems. Additionally, the growth of outpatient surgical centers and home-based palliative care is fostering the steady adoption of controlled-release formulations, sustaining ongoing demand within legitimate pharmaceutical channels.

Europe Fentanyl Market Trends

Europe is likely to be a significant market for fentanyl in 2026, due to increasing cancer incidence, a rapidly aging population, and expanding access to specialized pain clinics. Western European countries maintain strong adoption of transdermal patches and injectable formulations for chronic and perioperative pain management under controlled prescription systems. The presence of universal healthcare systems in many countries supports stable procurement through hospital tenders, ensuring consistent supply within regulated channels. Strict pharmacovigilance policies and opioid stewardship initiatives continue to shape prescribing behavior, balancing patient access with public health safeguards.

A significant trend is the increasing focus on high-quality manufacturing and adherence to European Medicines Agency standards for controlled substances. Companies are prioritizing tamper-proof delivery systems and consistent sterile injectable production to meet the needs of hospitals. For instance, Fresenius SE & Co. KGaA, a key supplier of injectable pharmaceuticals to hospitals across Europe, plays a vital role in supporting anesthesia and critical care. Growth is further driven by the expansion of home-based palliative care services in countries like Germany, France, and the U.K., where well-established reimbursement systems ensure proper opioid use under medical supervision.

Asia Pacific Fentanyl Market Trends

The Asia Pacific region is likely to be the fastest-growing region in the fentanyl market in 2026, driven by healthcare modernization, rising cancer incidence, and growing awareness of structured pain management practices. Countries such as China, Japan, South Korea, and India are strengthening oncology infrastructure and surgical capacity, increasing the need for regulated opioid analgesics in hospital settings. Aging populations in developed economies such as Japan are contributing to higher demand for chronic pain and palliative care solutions. Governments across the region are also tightening controlled-substance regulations to align with international standards, ensuring appropriate access while limiting diversion.

Manufacturing capacity and domestic pharmaceutical development are additional defining trends in the region. Local producers are investing in high-quality active pharmaceutical ingredient production and finished dosage capabilities to meet both domestic and export demand. For example, Humanwell Healthcare (Group) Co., Ltd., a major producer of anesthetic and opioid formulations, supplies regulated hospital markets in China and internationally. Growth opportunities are supported by expanding palliative care programs in emerging Southeast Asian economies, where improving hospital access and reimbursement frameworks are strengthening legitimate pharmaceutical consumption.

Competitive Landscape

The global fentanyl market exhibits a moderately fragmented structure, driven by the coexistence of large multinational pharmaceutical firms and regional manufacturers supplying regulated hospital and palliative care channels. Unlike illicit supply chains that dominate public headlines, the legitimate market centers on controlled, prescription-based products used in anesthesia, severe pain management, and oncology care. Companies must navigate stringent regulatory frameworks, production quotas, and distribution controls enforced by agencies such as the U.S. FDA, European Medicines Agency, and national health authorities across Asia.

With key leaders including Pfizer Inc., Hikma Pharmaceuticals PLC, Fresenius SE & Co. KGaA, Sun Pharmaceutical Industries Ltd., and Humanwell Healthcare (Group) Co., Ltd., the competitive landscape reflects both branded and generic portfolio strategies. These players compete through ongoing investments in abuse-deterrent technologies, expansion of manufacturing capacity, and enhancements in drug delivery systems to meet evolving clinical needs.

Key Industry Developments:

- In January 2026, AltaPointe Health announced findings from a clinical study published in Addiction Science & Clinical Practice demonstrating that a low intramuscular dose of ketamine can significantly reduce fentanyl withdrawal symptoms and enable patients to begin buprenorphine treatment without severe discomfort. The study, conducted at a behavioral health crisis center in Alabama, involved patients experiencing fentanyl withdrawal and showed rapid symptom relief with no reported adverse effects. Most participants were able to initiate buprenorphine therapy shortly after ketamine administration, improving stabilization timelines and discharge readiness.

- In January 2025, Alvogen announced a voluntary nationwide recall of one lot of its Fentanyl Transdermal System 25 mcg/h patches due to a defective delivery system that could result in multiple patches being accidentally stacked together in a single pouch. The lot affected (Lot 108319, expiry April 2027) was distributed to pharmacies and patients across the United States. The multi-stacked patches posed a risk of delivering a higher than intended dose, potentially causing serious, life-threatening, or fatal respiratory depression, particularly among first-time users, children, and the elderly.

Companies Covered in Fentanyl Market

- Alvogen

- Apotex Inc.

- Biesterfeld SE

- Daiichi Sankyo Company, Limited

- Fresenius SE & Co. KGaA

- Hikma Pharmaceuticals PLC

- Humanwell Healthcare (Group) Co., Ltd.

- Sun Pharmaceutical Industries Ltd.

- Mallinckrodt Pharmaceuticals

- Endo Pharmaceuticals Inc.

- Pfizer Inc.

- Boehringer Ingelheim

- Janssen Pharmaceuticals Inc.

- Zyla Life Sciences

- Actavis Plc.

- Sanofi SA

- Assertio Therapeutics Inc.

Frequently Asked Questions

The global fentanyl market is projected to reach US$2.5 billion in 2026.

The fentanyl market is driven by the rising prevalence of severe chronic pain and cancer, increasing surgical procedures, and growing demand for effective anesthesia and palliative care management in regulated clinical settings.

The fentanyl market is expected to grow at a CAGR of 4.8% from 2026 to 2033.

Key market opportunities lie in the development of abuse-deterrent formulations, advanced drug delivery technologies, and the expansion of hospital and home-based palliative care services under regulated frameworks.

Alvogen, Apotex Inc., Biesterfeld SE, Daiichi Sankyo Company, Limited, and Fresenius SE & Co. KGaA are the leading players.