- Pharmaceuticals

- Europe Autogenous Vaccines Market

Europe Autogenous Vaccines Market Size, Share, and Growth Forecast 2026 - 2033

Europe Autogenous Vaccines Market by Strain Type (Bacterial Strain, Virus Strain), by Animal (Poultry, Swine, Fish, Horse, Others), End-use (Veterinary Research Institutes, Livestock Farming Companies, Veterinary Clinics and Hospitals), and Country Analysis, 2026 - 2033

Europe Autogenous Vaccines Market Size and Trend Analysis

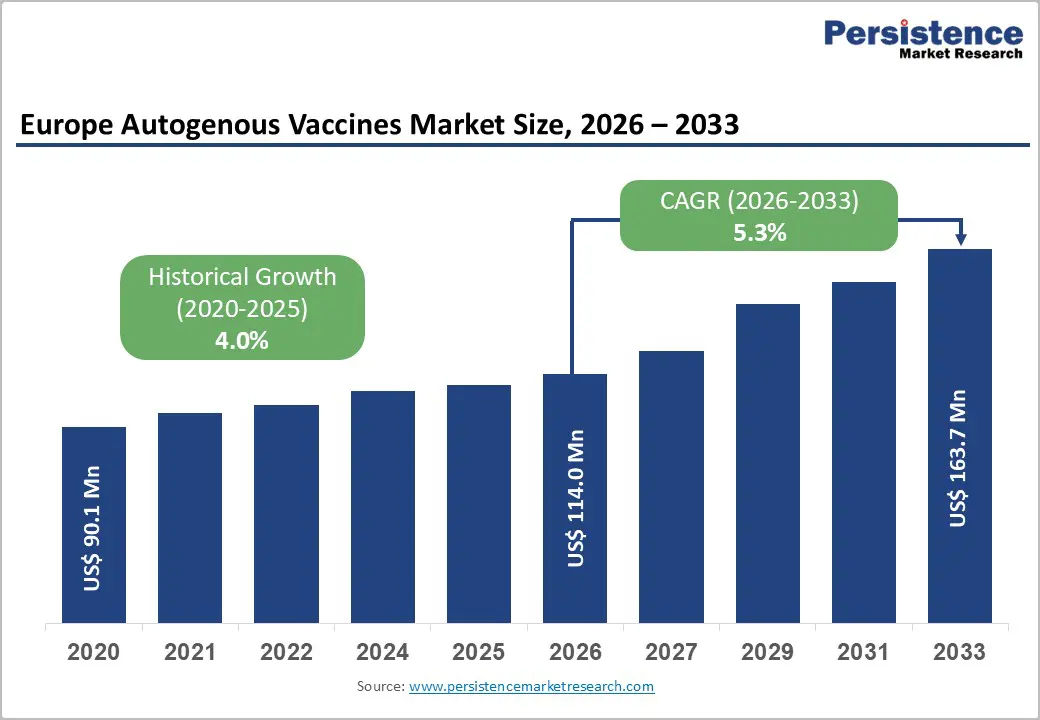

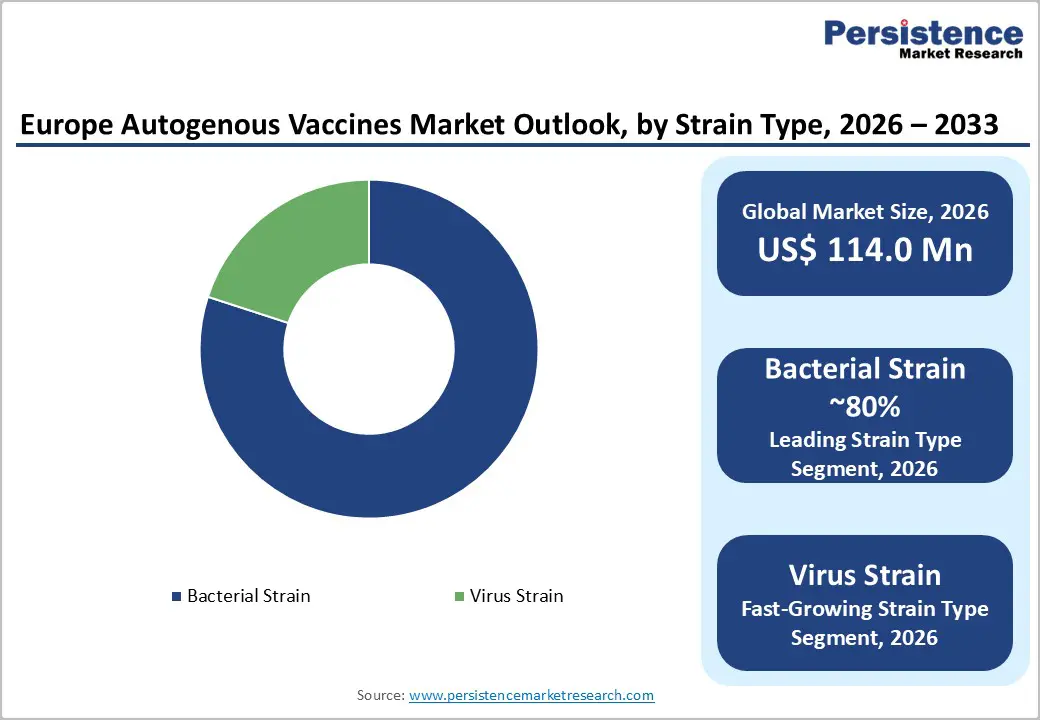

The Europe autogenous vaccines market size is expected to be valued at US$ 114.0 million in 2026 and projected to reach US$ 163.7 million by 2033, growing at a CAGR of 5.3% between 2026 and 2033. It is experiencing a steady growth driven by increasing emphasis on animal health management, disease prevention, and antimicrobial stewardship.

Autogenous vaccines, developed from pathogens isolated from specific farms or animal populations, provide targeted protection against disease outbreaks that may not be effectively addressed by commercial vaccines. The region’s advanced veterinary infrastructure, strict animal welfare standards, and expanding livestock and aquaculture industries support market growth.

Government-backed vaccination programs, improved disease surveillance, and rising investments in veterinary research are further strengthening market demand. Countries including France, Germany, Spain, and the Netherlands are promoting preventive animal healthcare to enhance biosecurity and livestock productivity. Growing awareness of the economic impact of infectious diseases and the benefits of customized vaccination strategies is accelerating the adoption of autogenous vaccines across Europe.

Key Industry Highlights:

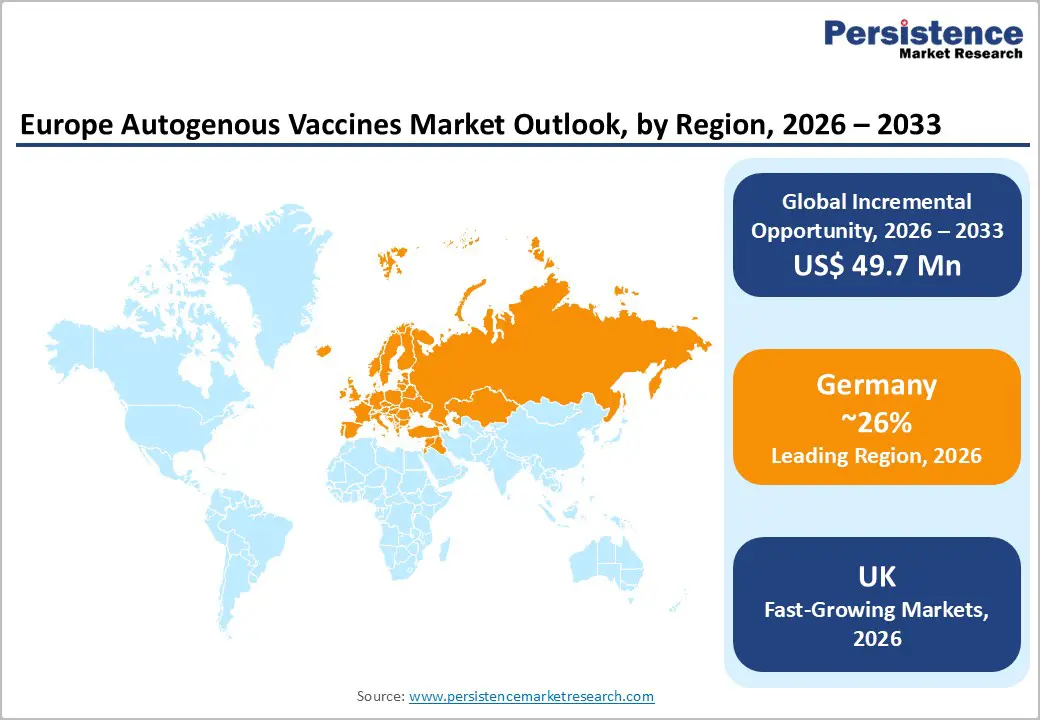

- Leading Country - Germany led Europe’s autogenous vaccines market in 2026 with ~26% share, supported by strong swine and poultry industries and favorable regulatory policies.

- Fastest Growing Country - The UK autogenous vaccines market is expected to grow at 6% CAGR by 2033, driven by aquaculture growth and veterinary regulatory modernization.

- Dominant Segment - Bacterial strain vaccines are likely to reach over 80% share in 2026 due to established approvals and widespread bacterial infections in intensive livestock farming.

- Fastest Growing Segment - Virus strain autogenous vaccines are the fastest-growing segment, fueled by avian influenza, swine fever, and emerging fish viral disease outbreaks.

- Key Opportunity - Expanding aquaculture production and limited commercial fish vaccines create strong opportunities for autogenous fish vaccine manufacturers across Europe and Asia-Pacific.

Market Dynamics

Drivers - Regulatory shifts and antimicrobial resistance concerns drive demand for herd-specific autogenous vaccines

Europe autogenous vaccines market is being driven by a growing need for targeted, farm-specific disease prevention amid rising concerns over antimicrobial resistance (AMR). With the European Union’s ban on the preventive use of antibiotics in animal feed (Regulation EU 2019/6) effective since January 2022, producers are turning to autogenous vaccines as a sustainable alternative. These vaccines offer tailored protection against pathogens not covered by commercial products, helping to enhance herd immunity and reduce reliance on broad-spectrum antimicrobials.

Regulatory support and declining antimicrobial sales down 53% between 2011 and 2022 in Europe (European Medicines Agency (EMA), 2023) are reinforcing this trend. Disease outbreaks such as bluetongue virus and epizootic haemorrhagic disease have further emphasized the importance of proactive immunization. Advances in vaccine development, including faster antigen production and approval pathways, also support market growth. As awareness among farmers and veterinarians increases, autogenous vaccines are emerging as essential tools in precision herd health management across Europe.

Restraints - Limited epidemiological understanding and research gaps restrain effective vaccine development and adoption

A key restraint in the European autogenous vaccines market is the limited understanding of veterinary disease epidemiology, particularly for region-specific and emerging pathogens. Diseases such as virulent Newcastle Disease in poultry highlight significant knowledge gaps in how pathogens evolve and spread, due to rapid genetic mutations and inadequate surveillance. These gaps hinder the development of effective, tailored vaccines.

Additionally, the complex genetic diversity of pathogens across Europe and limited insight into antigen-immunogenic structures make it difficult to identify appropriate vaccine targets. This challenge is compounded by the lack of collaboration between veterinary research institutes and vaccine manufacturers, resulting in poor knowledge of immune responses, protective mechanisms, and clinical outcomes. The absence of robust data-sharing systems further delays the creation of herd-specific formulations. To unlock the full potential of autogenous vaccines in Europe, coordinated efforts in research, diagnostics, and industry partnerships are essential to enhance precision, speed, and efficacy in vaccine development.

Opportunities - Rising farmer awareness and Europe biosecurity policies unlock growth in customized vaccine solutions

The European autogenous vaccines market presents strong growth opportunities driven by rising awareness among farmers and veterinarians regarding targeted disease prevention and herd-specific health management. With growing concerns over antimicrobial resistance (AMR), especially in livestock production, there is a clear shift toward safer and more sustainable alternatives. Autogenous vaccines, developed from pathogens isolated within individual herds or flocks, offer tailored protection with reduced impact on microbiota and lower risk of resistance.

In November 2024, Ceva Animal Health announced a €75 million investment to build a 7,000 m² vaccine manufacturing facility in Hungary. Scheduled to open by the end of 2026, this plant is expected to produce fermentation-based multicomponent inactivated vaccines, with a capacity of over 8 billion doses annually. This expansion is anticipated to strengthen Ceva’s commitment to preventive medicine and tailored vaccine solutions for emerging diseases, supporting the growing demand for autogenous vaccines across Europe.

Additionally, veterinary outreach programs, diagnostic advancements, and EU initiatives such as the Animal Health Law (Regulation 2016/429) are promoting responsible disease control practices. Central European countries such as the Czech Republic, Hungary, and Slovakia, where autogenous vaccine use is well established, continue to drive adoption. As knowledge-sharing platforms expand and farmers increase biosecurity efforts, demand for customized vaccination strategies is expected to grow significantly.

Category-wise Analysis

Strain Type Insight

Bacterial strain segment is projected to hold a revenue share of over 80% in 2026 within the Europe autogenous vaccines market. This dominance is driven by the high prevalence of bacterial infections in livestock, such as swine dysentery, salmonellosis, and E. coli-related diseases, which are often specific to individual herds or farms.

Autogenous vaccines using bacterial strains offer a targeted approach, enabling veterinarians to develop precise formulations based on locally circulating pathogens. These vaccines are particularly valuable when commercial options are unavailable or ineffective against farm-specific bacterial variants. Additionally, the rise in antimicrobial resistance has prompted regulatory bodies and producers to favor non-antibiotic solutions, further boosting demand for customized bacterial vaccines as a proactive disease management strategy.

Animal Segment Insights

Poultry segment is expected to dominate the animal category in 2026 with nearly 42.3% of Europe autogenous vaccines market share. This is due to the high density of poultry farming across Europe and the frequent occurrence of herd-specific diseases such as Newcastle disease and infectious bronchitis, which require customized vaccination solutions. Compared to swine, fish, horse, and other animals, poultry production is more widespread, with rapid turnover and significant economic impact, driving greater vaccine demand.

Swine, however, is the most lucrative sector with a CAGR of 5.9% over the forecast period due to increasing concerns about diseases like influenza A virus and porcine reproductive and respiratory syndrome (PRRS). Swine farms often face complex, evolving pathogens, creating strong demand for tailored autogenous vaccines to improve herd health and productivity.

Country-wise Insights

Germany Autogenous Vaccines Market Size

Germany is anticipated to hold 26% share in 2026 due to its large and well-established livestock industry, especially in swine and poultry farming. The country’s strong focus on advanced animal health management, rigorous regulatory framework, and early adoption of innovative veterinary solutions support market growth. For instance, in February 2025, the Dopharma Group and its subsidiary Ripac-Labor GmbH officially broke ground on a cutting-edge autogenous vaccine production facility in Potsdam, Germany, marking a major expansion initiative.

Germany’s commitment to combating antimicrobial resistance through stringent regulations encourages the use of autogenous vaccines as sustainable alternatives. Additionally, robust veterinary infrastructure, active research collaborations, and increasing farmer awareness about targeted disease prevention further drive demand for customized vaccines in the region.

UK Autogenous Vaccines Market Size

The UK is estimated to be the most lucrative market over the forecast period, with a projected CAGR of 6.1% between 2026 and 2033, driven by its advanced livestock sector and strong emphasis on sustainable farming practices. Increasing concerns over AMR and government initiatives promoting responsible antibiotic use are accelerating demand for alternative disease prevention methods such as autogenous vaccines.

Additionally, the UK’s well-developed veterinary services, growing adoption of precision livestock farming, and rising awareness among farmers about herd-specific health management contribute significantly to market growth. Ongoing investments in research and development further support innovation and the adoption of customized vaccines across various livestock and aquaculture sectors.

In February 2025, Mowi Scotland reported a 35% reduction in overall biomass mortality across all seawater farms in 2024, attributed to enhanced biosecurity, improved vaccination programs, including autogenous vaccines developed in collaboration with Ridgeway Biologicals, and favourable environmental conditions. This success highlights the increasing role of autogenous vaccines in improving animal health outcomes in the UK, reinforcing their potential as a key tool in sustainable animal disease management.

Spain Autogenous Vaccines Market Analysis

Spain represents a key market within the European autogenous vaccines industry, supported by one of the region's largest livestock populations and its strong position in swine and poultry production. Growing concerns regarding infectious disease outbreaks, pathogen evolution, and antimicrobial resistance are encouraging livestock producers to adopt customized vaccination strategies. The increasing need for farm-specific disease prevention solutions, particularly intensive livestock operations, continues to support market expansion across the country.

The market is further benefiting from rising investments in biosecurity, veterinary diagnostics, and preventive animal healthcare. As conventional vaccines may not always provide adequate protection against localized pathogen strains, demand for autogenous vaccines is increasing among commercial producers seeking targeted disease management solutions. Continued modernization of livestock farming practices and strengthening animal health programs are expected to support steady growth of the Spain autogenous vaccines market during the forecast period.

Competitive Landscape

The global autogenous vaccines market exhibits a moderately fragmented structure, with a mix of large multinational animal health companies and specialized regional manufacturers. Leading multinationals including Boehringer Ingelheim, Ceva Santé Animale, HIPRA, and Elanco Animal Health, compete alongside dedicated autogenous specialists such as Vaxxinova and AniCon Labor GmbH.

Key competitive differentiators include proprietary rapid diagnostic and antigen isolation technologies, regulatory expertise across multiple jurisdictions, and the ability to deliver short production lead times. Strategic investments in genomic pathogen characterization and digitalized farm health management platforms are emerging as important business model innovations across the competitive landscape.

Key Developments:

- In April 2025, HIPRA launched ICHTIOVAC® ERM, its first inactivated vaccine for Atlantic salmon against Yersiniosis, which was designed to be administered by immersion to combat the disease during the freshwater phase.

- In March 2025, Bimeda’s AquaTactics entered the autogenous fish vaccine market after receiving USDA approval for aquaculture autogenous vaccines.

- In January 2023, Ridgeway Biologicals Ltd. (UK) received Veterinary Medicines Directorate (VMD) approval for its upgraded autogenous vaccine production protocol, enabling faster release of farm-specific vaccines while maintaining full regulatory compliance.

Companies Covered in Europe Autogenous Vaccines Market

- Ceva

- HIPRA

- Vaxxinova

- Phibro Animal Health Corporation

- Dopharma International B.V

- RB Vac sp. z o.o.

- Dyntec

- Hygieia Biological Laboratories

- Boehringer Ingelheim International GmbH

- Elanco Animal Health

- Bimeda® Biologicals

- AniCon Labor GmbH (SAN Group GmbH)

- INVAC International GmbH

- AgriLabs (Huvepharma, Inc.)

- Others

Frequently Asked Questions

The global autogenous vaccines market is expected to reach US$ 114.0 million in 2026.

Growing demand for tailored autogenous vaccines in aquaculture and livestock, decline in antimicrobial use, and increasing focus on preventative measures for herd health are the key driving factors for the market growth.

Germany leads the global autogenous vaccines market, commanding ~26% of total market share in 2025.

Major growth opportunities in the autogenous vaccines market are driven by aquaculture expansion, rising viral disease outbreaks, unmet vaccine needs, and supportive evolving regulatory frameworks.

Ceva, HIPRA, Vaxxinova, Phibro Animal Health Corporation, Boehringer Ingelheim International GmbH, and Elanco Animal Health are a few leading players.