- Semiconductor Materials & Components

- DNA Data Storage Platform Market

DNA Data Storage Platform Market Size, Share, and Growth Forecast, 2026 - 2033

DNA Data Storage Platform Market by Deployment Mode (Cloud / On-Premises), Technology Type (Sequence-Based DNA Storage / Structure-Based DNA Storage), Application (Healthcare & Biotechnology, Government, Media & Telecommunications, Others) and Regional Analysis for 2026 - 2033

DNA Data Storage Platform Market Size and Trends Analysis

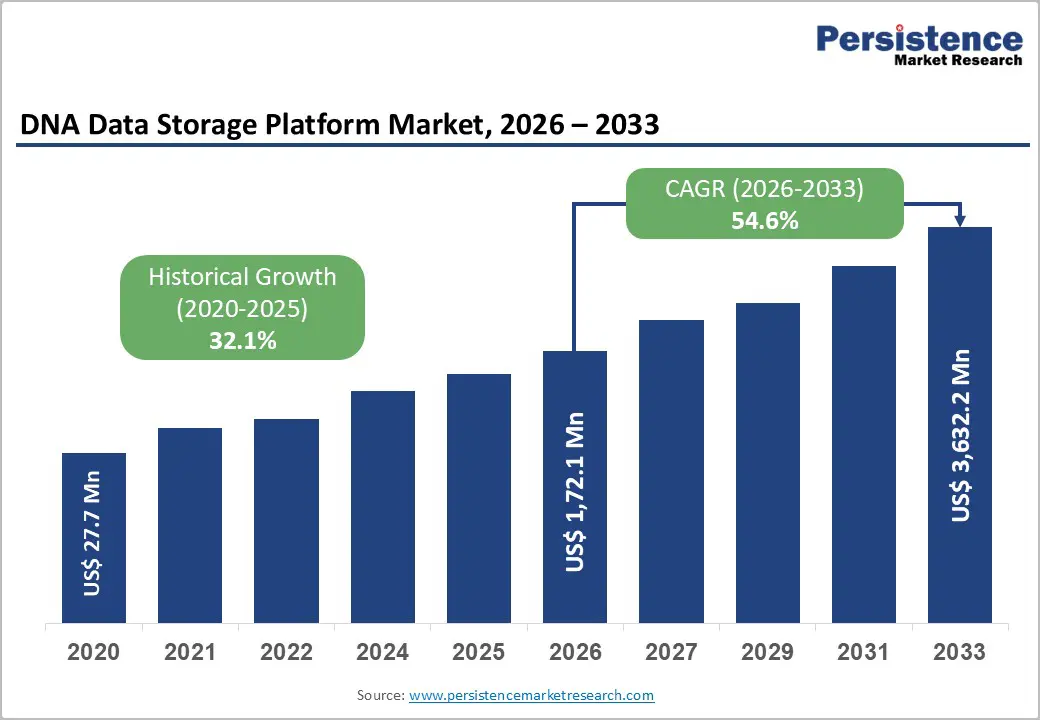

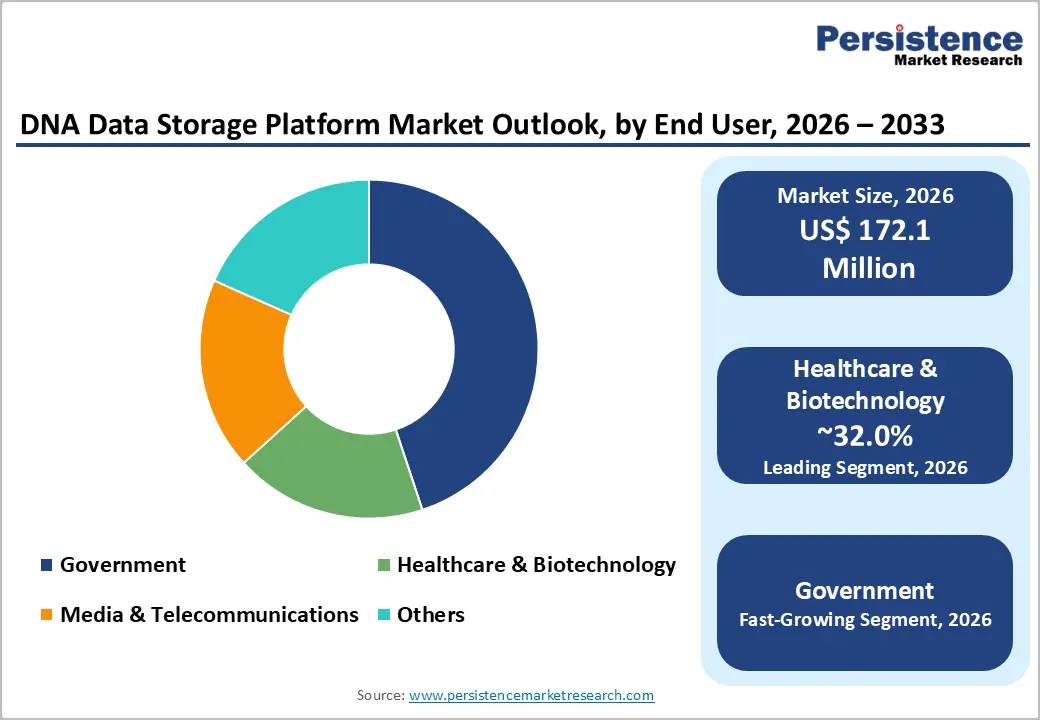

The Global DNA Data Storage Platform Market was valued at US$172.1 Million in 2026 and is projected to reach US$3,632.2 Million by 2033, growing at a CAGR of 54.6% between 2026 and 2033. This exceptionally high growth rate reflects the market's transition from proof-of-concept research toward commercial deployment as DNA's unparalleled data density and multi-millennia preservation capabilities address the exponential global data growth crisis.

The convergence of advancing DNA synthesis technologies, standardisation initiatives through the DNA Data Storage Alliance, and substantial government-backed research funding catalyzes rapid commercialisation of DNA-based archival platforms for healthcare, government, and enterprise sectors requiring ultra-dense, ultra-durable long-term storage solutions.

Key Industry Highlights:

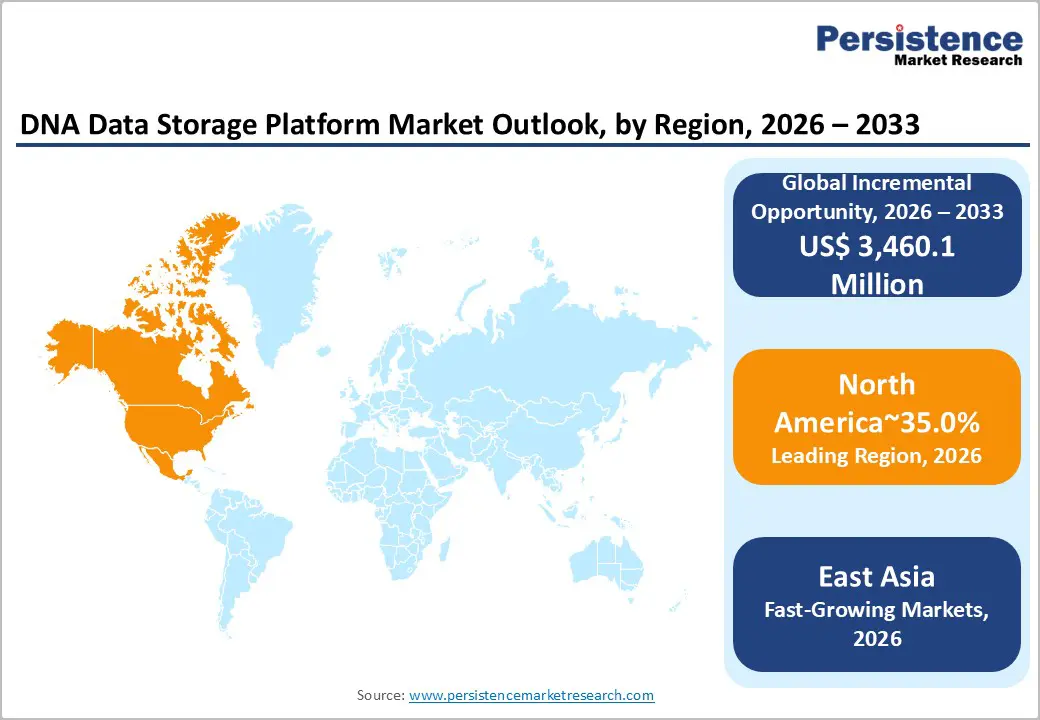

- Regional Leadership: North America leads the market with 35% share in 2025, driven by advanced research infrastructure, venture capital funding, and a concentration of genomics and healthcare data.

- Fastest-Growing Region: East Asia captures 25% share and is the fastest-growing region, supported by China’s government-backed synthetic biology initiatives and South Korea and Japan’s biotech and nanofabrication capabilities.

- Leading Technology Segment: Sequence-based DNA storage dominates with 70% market share in 2026, reflecting superior maturity, cost trajectory, and regulatory validation compared to structure-based approaches.

- Top End-User Segment: Healthcare & Biotechnology accounts for 32% share and is the fastest-growing end-user segment, driven by exponential genomic and clinical data generation and long-term preservation mandates.

- Key Growth Driver: Exponential global data growth and storage capacity constraints propel DNA storage adoption, offering multi-century durability and zero-energy cold storage advantages over conventional magnetic and solid-state media.

| Key Insights | Details |

|---|---|

|

DNA Data Storage Platform Market Size (2026E) |

US$ 172.1Million |

|

Market Value Forecast (2033F) |

US$ 3,632.2 Million |

|

Projected Growth (CAGR 2026 to 2033) |

54.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

32.1% |

Market Dynamics

Growth Drivers

Exponential Global Data Growth and Storage Capacity Constraints

The DNA Data Storage Platform Market responds to the fundamental challenge that global digital data production has exceeded traditional storage infrastructure capacity for over a decade. Global data volumes are projected to reach approximately 175-181 zettabytes by 2025, demonstrating the exponential trajectory that conventional magnetic tape, solid-state, and optical storage technologies cannot sustain sustainably.

This data growth crisis directly drives the Market as organizations recognize traditional storage media's physical limitations, magnetic hard drives degrade within 5-10 years, solid-state drives within 10-20 years, and even premium magnetic tape within 30 years.

DNA molecules, when stored in appropriate conditions like room-temperature dry powder or silicon-based encapsulation, maintain information integrity for thousands of years, providing multi-century preservation capability unmatched by any electronic storage medium. The data accumulation problem particularly affects sectors with massive dataset volumes, such as healthcare organisations generating genomic sequencing data, clinical trial datasets, electronic health records, and medical imaging that collectively constitute the most rapidly expanding data category globally, driving healthcare's 32% market share within the DNA Data Storage Platform Market.

The cost of storage itself motivates DNA adoption, while current synthesis costs remain elevated at approximately $1 per gigabyte. This approach approaches competitiveness with premium long-term archival solutions, and technology learning curves suggest costs will decline substantially through 2033. For cold storage applications, data accessed infrequently or never post-archival, DNA's zero-energy requirement after encoding provides substantial operational cost advantages compared to continuously powered traditional storage systems consuming terawatts annually.

Regulatory Mandates for Extended Data Retention and Preservation Compliance

Government and healthcare sector regulatory frameworks establish mandatory data retention periods that create an institutional obligation to deploy long-term storage solutions, thereby driving the DNA Data Storage Platform Market.

The United Kingdom's National Health Service mandates medical record retention for 10 years following patient death, establishing multi-decade obligations that require archival solutions with proven durability beyond current electronic storage warranties. India's health data management policies and ABDM (Ayushman Bharat Digital Mission) mandate compliance require healthcare organisations to maintain patient records for extended periods, creating institutional pressure to adopt durable storage platforms.

Government agencies globally maintain permanent archives of national records, census data, legal documents, and classified materials requiring protection against data degradation and unauthorised access requirements that the DNA Data Storage Platform Market addresses through encrypted DNA storage mechanisms offering physical immutability. These regulatory mandates create non-discretionary demand for storage infrastructure upgrades; organisations cannot defer compliance with government-mandated retention periods.

The Market specifically serves these regulatory use cases because traditional magnetic archives require periodic migration and equipment replacement to prevent data loss, while DNA archives require no such intervention once properly sealed and stored. Government cultural heritage preservation initiatives, such as national libraries, archives, and museums further drive regulatory demand for institutional recognition that digital collections represent irreplaceable cultural assets requiring permanent preservation has accelerated the adoption of DNA storage for preserving digital museum collections, historical documents, and multimedia archives.

Market Restraining Factors

Prohibitive Current Synthesis and Sequencing Costs Versus Competing Storage Modalities

Despite technological advances, DNA storage synthesis and sequencing costs remain substantially elevated compared to established archival alternatives, limiting adoption to high-value datasets where cost justifies deployment.

Current DNA synthesis costs remain approximately US$1 per gigabyte, whereas magnetic tape archival solutions cost less than US$0.01 per gigabyte when amortised over a 30-year lifespan, representing a 100-fold cost disadvantage that constrains DNA Data Storage Platform Market adoption to premium-value use cases. Error correction requirements add significant overhead. DNA molecules require redundancy encoding to achieve acceptable error rates, effectively increasing storage costs by 10-100% depending on desired reliability levels.

This cost structure restricts the DNA Data Storage Platform Market to applications where durability and density advantages justify the cost premium: national archives, genomic databases, medical records, and long-term government repositories rather than routine commercial backup and recovery operations. The cost differential compels organisations to evaluate the total cost of ownership across decades-long timescales, requiring financial analysis sophistication that may exceed the decision-making capacity of smaller organisations. Until DNA synthesis costs decline through manufacturing scale-up and process improvements, the DNA Data Storage Platform Market will remain limited to institutional customers with sophisticated financial analysis capabilities and multi-decade planning horizons.

Key Market Opportunities

Genomic Data Archival and Healthcare Digital Transformation

The DNA Data Storage Platform Market addresses an unprecedented accumulation of genomic and clinical data that healthcare institutions must preserve indefinitely for patient care, research, regulatory compliance, and future medical discovery. The healthcare sector's explosive data generation reflects multiple converging trends: genomic sequencing costs have declined from US$100 million (2000) to approximately US$100-500 (2025), enabling routine clinical sequencing in diagnostic pathways and personalised medicine applications, generating multi-petabyte institutional datasets. Clinical trial data similarly comprises massive datasets from thousands of patients tracked across years or decades, with regulatory requirements mandating permanent preservation for regulatory compliance and post-marketing safety monitoring. Emerging personalised medicine approaches require preservation of individual genomic profiles linked to medical outcomes across patient lifetimes for precision treatment optimisation.

The Market presents compelling value in this context because genomic data remains medically relevant for decades or centuries, justifying long-term preservation infrastructure investment. Healthcare institutions already operate genomic sequencing facilities with technical staff capable of managing DNA-based workflows, reducing adoption barriers compared to non-technical sectors.

DNA's unparalleled density directly addresses healthcare's space constraints. Storing 1 petabyte of genomic data in conventional magnetic storage requires approximately 500 square meters of facility space, whereas the equivalent DNA storage requires less than a single cubic centimetre, enabling healthcare systems to maintain comprehensive genomic databases without proportional facility expansion. Government-backed initiatives like India's genomic research programs and emerging healthcare AI applications requiring massive historical datasets to train machine learning models create institutional demand for comprehensive archival solutions that the DNA Data Storage Platform Market uniquely addresses.

Government and Institutional Long-Term Record Preservation

Government agencies, national archives, and cultural institutions increasingly recognise that digital content represents irreplaceable national assets requiring preservation against technological obsolescence, natural disasters, and intentional destruction a recognition creating substantial demand for the DNA Data Storage Platform Market.

The Arch Mission Foundation's initiatives to preserve human knowledge on lunar and orbital platforms demonstrate institutional recognition that DNA's multi-millennium stability offers unprecedented preservation assurance compared to electronic media vulnerable to electromagnetic interference, solar radiation, and terrestrial physical damage. Government archives of legal records, census data, immigration documentation, and classified materials represent invaluable national resources whose loss would be catastrophic; DNA storage provides immutable, tamper-evident preservation immune to hacking, ransomware, and physical degradation.

Cultural heritage preservation represents another substantial opportunity for museums, libraries, and media institutions to maintain digital collections of digitised manuscripts, photographs, film archives, and artwork documentation. Increasingly, they recognise that traditional storage systems lack adequate durability for institutional timescale preservation requirements. UNESCO World Memory initiatives and similar global programs documenting endangered cultural heritage increasingly adopt DNA storage approaches due to DNA's incomparable longevity.

Recent developments, including the DNA Palette coding scheme enabling brain MRI data encoding to demonstrate how DNA storage expands beyond simple file preservation to enable complex medical data preservation with capacity for future reprocessing and analysis as technologies advance. These government and institutional use cases create contractual multi-year revenue streams independent of commercial market cycles, providing stable demand for specialised DNA Data Storage Platform providers contracting directly with government procurement organisations.

Category-wise Analysis

Technology Type Insights

Sequence-based DNA storage dominates the DNA Data Storage Platform Market with 70% market share in 2026 and simultaneously represents the fastest-growing technology segment, reflecting superior maturity, reliability, and cost trajectory of sequence-based approaches. Sequence-based methods leverage established DNA sequencing and synthesis technologies widely available through Illumina, BGI, 10X Genomics, and emerging sequencing vendors. Reliability advantages stem from sequence-based approaches' reliance on well-understood DNA synthesis chemistry and NGS technologies deployed at scale across global research institutions, diagnostic laboratories, and biotechnology companies for over two decades.

Technology’s dominance reflects regulatory and validation advantages, healthcare institutions and government archivists demonstrate greater confidence in sequence-based technologies with proven clinical and research deployment histories compared to novel structure-based approaches lacking equivalent operational validation.

Continuous improvements in NGS technology cost and throughput create compounding advantages for the sequence-based segment as Illumina and competing sequencing vendors reduce per-read costs and increase throughput through competitive product development, sequence-based DNA storage achieves proportional cost reductions automatically without requiring proprietary research investment by DNA storage companies. Recent breakthrough innovations like the Technion DNAformer method, demonstrating 3,200-fold retrieval speed improvements, specifically address sequence-based storage limitations, suggesting the segment's continuous maturation will extend its market dominance throughout the forecast period

Application Insights

Healthcare and biotechnology sectors command 32% of the DNA Data Storage Platform Market and simultaneously represent the fastest-growing end-user segment, reflecting healthcare's unique convergence of data growth explosiveness, regulatory preservation mandates, long retention requirements, and sophisticated technical infrastructure capable of managing DNA-based workflows.

The healthcare sector generates the highest-volume, highest-value datasets globally. Genomic sequencing volumes have expanded from millions of sequences annually in 2010 to billions annually by 2025, creating petabyte-scale institutional repositories that traditional storage systems struggle to manage cost-effectively. Clinical trials, electronic health records, medical imaging, and emerging real-world evidence datasets collectively constitute healthcare's most rapidly expanding data category, with regulatory requirements mandating retention of most clinical data for patient care durations plus extended post-mortem periods typically 10-20 years.

The combination of massive data volume, decades-long retention requirements, and critical data importance creates compelling DNA storage economics where durable long-term preservation justifies premium storage costs. Healthcare organisations possess the necessary technical sophistication to operate DNA storage systems. Genomic laboratories already operate next-generation sequencing instruments, maintain bioinformatics expertise, and manage molecular data workflows, reducing adoption barriers compared to sectors requiring de novo technical capability development. Regulatory compliance represents another healthcare advantage, as standards development by genomics organisations such as Illumina and BGI, regulatory bodies establish validation pathways for DNA storage in clinical contexts, reducing uncertainty about regulatory approval that might otherwise constrain adoption.

Regional Insights and Trends

North America Market Trend

North America commands 35% of the Global DNA Data Storage Platform Market, establishing the region as the dominant market through a combination of advanced research infrastructure, an established biotechnology ecosystem, substantial venture capital funding, and government research investment concentration. The United States hosts the majority of DNA data storage research institutions such as the University of Washington, MIT, Caltech, UC Berkeley, that conduct foundational innovations and commercialise breakthrough technologies through affiliated startups.

Major technology companies headquartered in North America invest substantially in DNA storage research, viewing the technology as addressing existential data infrastructure challenges facing hyperscale cloud providers. Government research agencies, including IARPA (Intelligence Advanced Research Projects Activity), fund DNA storage research with multi-million-dollar programs recognising military and intelligence applications of DNA-based archival systems, thereby catalysing technology development and accelerating commercialisation pathways.

The venture capital ecosystem concentrating in North America, particularly Silicon Valley, Boston, and Seattle, provides capital for DNA storage startups, including Catalogue (US$60 million plus raised), Biomemory (US$18 million Series A, December 2024), and numerous emerging ventures developing specialised components and applications. Healthcare and research data volumes concentrate in North America, with leading genomic research institutions and pharmaceutical companies generating massive genomic datasets requiring preservation. This data concentration creates a local customer base for DNA storage platform vendors.

Regulatory frameworks, including HIPAA (healthcare data) and state-specific data protection laws, create institutional pressure for robust long-term preservation mechanisms, supporting DNA storage adoption in regulated sectors. The region's dominant position reflects cumulative advantages in research infrastructure, capital availability, technical expertise, and anchor customer concentration that compound over time.

East Asia Market Trend

East Asia holds 25% of the Global DNA Data Storage Platform Market and exhibits a rapid growth trajectory reflecting the emergence of competitive DNA storage research ecosystems in China, South Korea, and Japan. China's government research investments in synthetic biology and biotechnology create institutional support for DNA storage research, with breakthrough innovations including the Tianjin University DNA Palette coding scheme, enabling brain MRI data encoding, demonstrating technological leadership alongside North American competitors. Chinese government archive requirements for massive datasets create domestic demand for advanced storage platforms compatible with DNA-based approaches.

South Korea's advanced semiconductor and biotechnology sectors position the region for leading DNA storage hardware development, with potential for integration of DNA storage into consumer electronics and IoT devices following technology maturation.

Japan's robotics and precision manufacturing capabilities enable potential leadership in DNA storage hardware production and integration, particularly for structure-based approaches requiring specialised nanofabrication. Academic research excellence in Chinese universities and Japanese institutions ensures continued technology contributions, competing with North American research output.

Europe Market Trend

Europe accounts for 22% of the Global DNA Data Storage Platform Market, with growth driven by comprehensive data protection regulations (GDPR) creating institutional preferences for data sovereignty and long-term preservation assurance, combined with government-backed research initiatives.

The EU's Horizon Europe research funding program explicitly supports DNA storage research through initiatives, including the MI-DNA Disc project (April 2025), developing living bacterial DNA storage systems, demonstrating institutional commitment to DNA storage technology development at the supranational level. The European regulatory environment emphasising data protection and citizen rights, creates customer demand for durable archival solutions preserving sensitive personal and health data in formats resistant to unauthorised access or modification. DNA's physical immutability addresses these regulatory concerns.

Competitive Landscape

The Global DNA Data Storage Platform market is moderately consolidated, driven by a mix of established technology giants and innovative biotech startups. Leading players such as Microsoft Corporation, Twist Bioscience / Atlas Data Storage, Illumina Inc., IBM Corporation, Thermo Fisher Scientific, and DNA Script dominate the market through strategic partnerships, R&D investments, and technological advancements in DNA synthesis, encoding, and storage.

While companies like Microsoft and IBM focus on integrating DNA storage with cloud infrastructure, Atlas Data Storage and Illumina specialise in commercialising dedicated DNA storage platforms and sequencing-based solutions. The market also benefits from standardisation initiatives by alliances and collaborations to improve interoperability and scalability. High entry barriers, such as production costs and technical complexity, limit fragmentation, but emerging startups continue to contribute niche innovations in DNA encoding and automated synthesis.

Key Industry Developments

- May 05, 2025 – Twist Bioscience Corporation: Twist Bioscience spun out its DNA-based data storage platform into an independent company, Atlas Data Storage, to accelerate the commercialisation of DNA data storage technologies. Atlas launched with USD 155 million in seed financing and a pure-play focus on DNA data storage platforms, while Twist retained a minority stake and ongoing royalty-linked participation in future platform revenues.

- March 12, 2024 – DNA Data Storage Alliance: The DNA Data Storage Alliance released its first industry specifications (Sector Zero and Sector One) to standardise how digital data, vendor details, and CODEC information are stored and accessed in DNA-based data storage archives. This development marks a key step toward interoperability and commercialisation of DNA data storage platforms by enabling consistent archive “boot-up” and data retrieval mechanisms.

Companies Covered in DNA Data Storage Platform Market

- Illumina Inc.

- Twist Bioscience

- Micron Technology Inc.

- Beckman Coulter

- Microsoft

- Catalog

- Helixworks Technologies Ltd

- Eurofins Scientific

- Iridia Inc.

- Thermo Fisher Scientific Inc.

- Agilent Technologies Inc.

- Siemens

Frequently Asked Questions

The global DNA Data Storage Platform Market is projected to be valued at US$ 172.1 Million in 2026.

The Sequence-Based DNA Storage Segment is expected to account for approximately 70% of the global DNA Data Storage Platform Market by Technology in 2026.

The market is expected to witness a CAGR of 54.6% from 2026 to 2033.

The DNA Data Storage Platform Market is driven by exponential global data growth, limitations of traditional storage media, long-term preservation needs, and regulatory mandates for extended data retention across healthcare, government, and archival sectors.

The DNA Data Storage Platform Market presents key opportunities in genomic and clinical data archival for healthcare digital transformation, long-term government record preservation, and safeguarding cultural heritage through ultra-dense, durable, and tamper-evident DNA storage solutions.

The key players in the DNA Data Storage Platform Market include Illumina Inc., Twist Bioscience, Micron Technology Inc., Microsoft, Thermo Fisher Scientific Inc., and Agilent Technologies Inc.