- Food Ingredients & Additives

- Dipping Sauce Market

Dipping Sauce Market Size, Share, and Growth Forecast, 2026 - 2033

Dipping Sauce Market by Product Type (Organic, Conventional), Sauce Type (Tomato-based Sauces, Mayonnaise-based Sauces, Mustard-based Sauces, Others), Distribution Channel (Online Retail Platform, Supermarkets/Hypermarkets, Others), and Regional Analysis for 2026 - 2033

Dipping Sauce Market Share and Trends Analysis

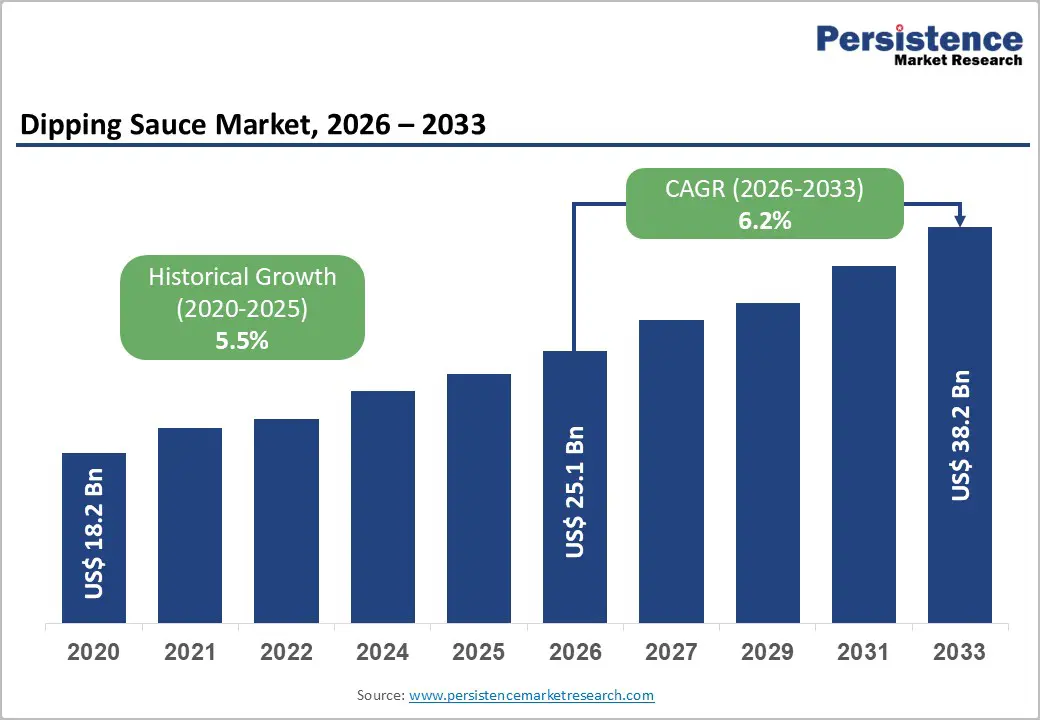

The global dipping sauce market size is likely to be valued at US$25.1 billion in 2026 and is estimated to reach US$38.2 billion by 2033, growing at a CAGR of 6.2% during the forecast period 2026−2033, driven by steady expansion in processed food consumption, urbanization, and global flavor diversification.

Rising demand for convenience foods strengthens adoption across household and food service segments. The growth of quick-service restaurants and packaged food channels supports stable demand. Regulatory standards and clean-label trends improve consumer trust. Digital retail expansion and healthier formulations further enhance market accessibility and long-term consumption.

Key Industry Highlights:

- Leading Product Type: Conventional dipping sauce is set to hold around 62% revenue share in 2026, driven by large-scale manufacturing efficiency and strong retail reach.

- Fastest-growing Product Type: Organic dipping sauce is projected as the fastest-growing segment, supported by clean-label demand and certification frameworks.

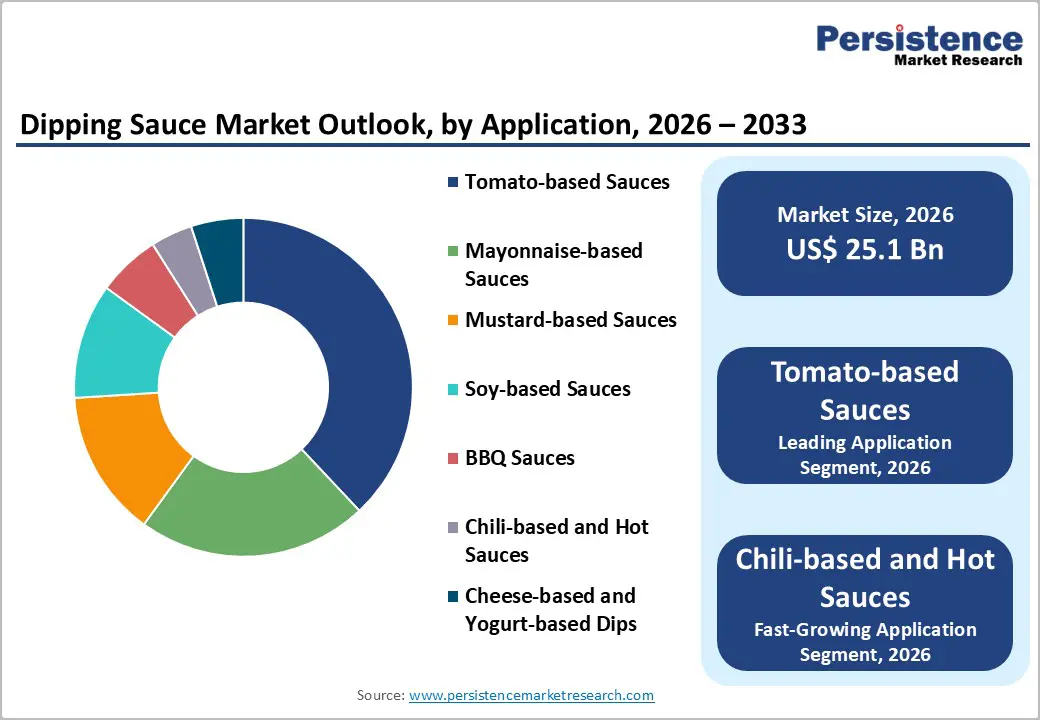

- Leading Application: Tomato-based sauces are estimated to hold roughly 38% revenue share in 2026, with wide culinary acceptance and multi-cuisine use.

- Fastest-growing Application: Chili-based and hot sauces are forecast to record the fastest growth, driven by flavor diversification and fusion food trends.

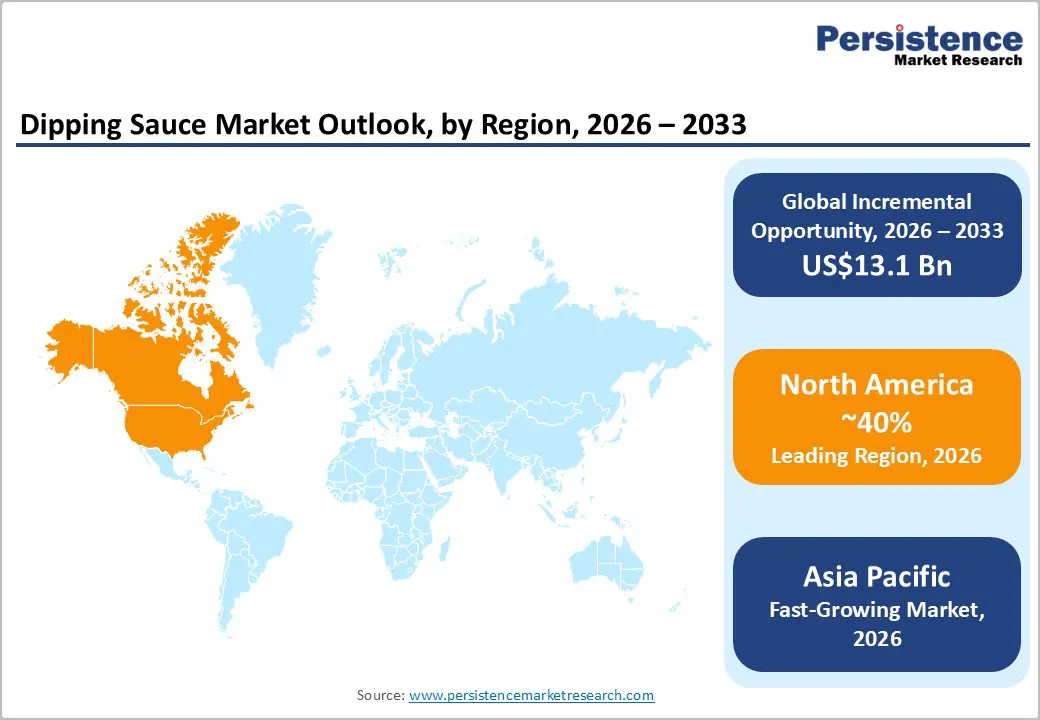

- Regional Leadership: North America is projected to capture roughly 40% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth due to urbanization and retail expansion.

- Competitive Environment: The market reflects a moderately fragmented structure, driven by strong multinational brand presence and regional manufacturer specialization, driven by retail scale advantages and pricing competitiveness across distribution channels.

DRO Analysis

Driver - Rising Demand for Convenience-based Food Consumption Patterns

Convenience-oriented eating patterns strengthen the dipping sauce market growth across urban food systems. Packaged meals and ready-to-eat formats increase reliance on quick flavor enhancers during daily consumption. Expansion of fast-food outlets and cloud kitchens elevates product integration in menu offerings. In 2025, data from the Food Safety and Standards Authority of India indicates a sustained increase in processed food consumption across urban India, reinforcing institutional demand trends, expanding market visibility, and supporting overall category growth.

Digital grocery ecosystems accelerate the accessibility of condiments across diverse consumer segments. Rapid delivery networks and e-commerce platforms streamline purchase frequency for impulse-driven consumption. Product innovation in low-sodium and clean-label formulations aligns with evolving nutritional expectations. Food service operators integrate standardized sachets to optimize cost efficiency and portion control. Distribution scalability enhances shelf presence in both developed and emerging market channels.

Restraint - Stringent Food Safety Compliance and Ingredient Regulation Complexity

Complex regulatory frameworks elevate compliance burden across formulation, labeling, and packaging processes. Frequent updates in permissible additives and allergen disclosure rules increase operational complexity for manufacturers. Ingredient sourcing becomes constrained under multiple jurisdictional standards, limiting formulation flexibility. In 2025, FSSAI official compliance surveillance indicates increased inspection intensity across packaged food facilities, reinforcing stricter enforcement expectations and higher documentation requirements across production systems.

Diverse international safety standards across the Food and Drug Administration (FDA) and European Food Safety Authority (EFSA) frameworks create fragmentation in approval pathways, extending product development cycles. Testing protocols for preservatives, emulsifiers, and flavor enhancers raise production costs and delay commercialization timelines. Small and mid-scale producers face higher entry barriers due to certification expenses. Retail listing approvals become more selective, reducing shelf penetration. Continuous reformulation requirements disrupt supply stability and slow innovation cycles across product portfolios.

Opportunity - Expansion of Clean-label and Health-oriented Condiment Innovation

Clean-label and health-oriented innovation creates strong value opportunities through reformulation of sauces with minimal additives, recognizable ingredients, and reduced artificial preservatives. Rising consumer scrutiny of ingredient transparency supports premium positioning and brand differentiation. Food manufacturers gain pricing power through healthier variants. Retail channels expand shelf space allocation for simplified formulations, strengthening demand visibility across multiple consumption occasions in global markets.

Regulatory alignment and health-driven consumption patterns accelerate the development of reduced-sodium and sugar-free formulations across condiment portfolios. Digital retail expansion improves access to healthier variants across urban and semi-urban markets. In 2025, FSSAI updates set a 30% sodium reduction target in selected packaged foods. This drives reformulation and supports wider adoption of healthier condiment choices.

Category-wise Analysis

Product Type Insights

Conventional products are the leading segment, projected to hold around 62% market share in 2026 due to a strong production infrastructure that supports large-scale output and cost efficiency. Established retail penetration ensures wide availability across supermarkets and foodservice networks, such as McDonald’s, sourcing standardized ketchup and mayonnaise. Standardized taste profiles, regulatory compliance, and product familiarity drive consistent demand and repeat household consumption.

Organic products are expected to be the fastest-growing segment during the forecast period. Rising consumer preference for ingredient transparency and pesticide-free sourcing supports higher adoption. Certification systems strengthen trust and premium positioning in retail channels, such as Annie’s organic ketchup, gaining shelf space in premium stores. Demand is further supported by health-focused dietary guidelines and sustainability priorities.

Sauce Type Insights

Tomato-based sauces are the leading segment, projected to hold around 38% market share in 2026. Universal culinary acceptance supports strong household and foodservice demand. Stable agricultural sourcing ensures consistent supply and pricing efficiency. Integration in fast food chains and home cooking strengthens repeat consumption across multiple regions and meal applications, such as Heinz tomato ketchup, widely used in burger and fry offerings.

Chili-based and hot sauces are the fastest-growing segment during the forecast period. Rising exposure to spicy and fusion cuisines supports stronger adoption among urban consumers. Digital platforms improve the discovery of niche products. An example includes Sriracha gaining global traction across restaurants and retail shelves. Tabasco is expanding usage across packaged meals. Continuous innovation in flavor intensity and regional variants accelerates category expansion across developed and emerging markets.

Regional Insights

North America Dipping Sauce Market Trends

North America is expected to lead with an estimated 40% of the dipping sauce market share in 2026, supported by the high penetration of convenience food culture and advanced food processing infrastructure across the U.S. and Canada. Mature quick-service restaurant networks create stable institutional demand for standardized condiments, including ketchup and mayonnaise used in burger meals at McDonald’s outlets. Strong product innovation cycles sustain category expansion.

High consumer willingness to pay for differentiated taste profiles strengthens premium product adoption across the U.S. and Canada. Advanced cold chain logistics and organized retail systems ensure consistent product availability across urban and suburban outlets. Regulatory alignment under FDA standards reinforces product safety and brand trust. Digital grocery platforms accelerate purchasing frequency, while flavor customization, such as Chipotle mayo in Subway menus, supports sustained consumption across diverse meal occasions.

Europe Dipping Sauce Market Trends

The Europe market shows strong maturity driven by premiumization and clean-label demand. High preference for organic and reduced additive sauces supports steady growth. Germany, France, and the U.K. demonstrate strong uptake of mayonnaise and herb-based sauces. Regulatory standards under the European Food Safety Authority strengthen quality compliance and consumer trust.

Innovation in flavor profiles supports product differentiation across retail shelves. Italy shows strong demand for tomato and olive oil-based sauces, while Spain favors aioli and spicy variants. Digital grocery growth and sustainable packaging improve accessibility. Expansion of quick-service restaurant menus reinforces consistent consumption across urban and suburban areas.

Asia Pacific Dipping Sauce Market Trends

Asia Pacific is forecast to be the fastest-growing market for dipping sauce, stimulated by rapid urbanization, expanding quick service restaurant penetration, and rising packaged food consumption. China shows strong demand growth through large-scale e-commerce grocery expansion and increasing adoption of Western-style fast food menus, such as McDonald’s Sichuan sauce offerings. India reflects rising intake of packaged condiments supported by food delivery platform growth, such as Zomato-linked restaurant delivery meals using packaged ketchup and mayo.

Japan and South Korea demonstrate strong innovation-led consumption, supported by premium flavor development and high convenience food integration in retail channels, such as Kewpie mayonnaise in Japanese convenience meals and bulgogi-style dipping sauces in Korean ready-to-eat kits. Dense urban populations across Southeast Asia further strengthen demand for ready-to-use sauces in street food ecosystems, such as Thai sweet chili sauce used in fried snacks. Expanding cold chain infrastructure improves availability across modern retail formats.

Competitive Landscape

The global dipping sauce market is moderately fragmented, with the presence of multinational food conglomerates and regional condiment manufacturers. Nestlé S.A., Unilever PLC, The Kraft Heinz Company, McCormick & Company, Kikkoman Corporation, and General Mills maintain diversified portfolios across sauces and condiments. Market balance is supported by strong regional brand loyalty and continuous product differentiation across global retail and foodservice channels.

The global dipping sauce market is shaped by distribution strength, flavor innovation, and pricing alignment across multiple channels. Strong retail partnerships and foodservice contracts enhance brand visibility in urban consumption hubs. Private label expansion from large retailers intensifies competition in mid-tier pricing segments. Continuous investment in reformulation, packaging innovation, and localized taste adaptation supports sustained competitive positioning across established and emerging markets.

Key Industry Developments:

- In April 2026, Domino’s launched Slice Sauce with a free promotional offer, introducing a new pizza dipping sauce to enhance customer dipping experience and boost engagement through digital ordering channels.

- In June 2025, Chipotle introduced Adobo Ranch as its first new dipping sauce in five years, a smoky ranch-style condiment made with adobo peppers and herbs to enhance customization across bowls, burritos, and tacos in North American outlets.

- In April 2025, McDonald’s introduced McCrispy Strips alongside a new Creamy Chili Dip, a savory, sweet, and tangy dipping sauce designed to enhance chicken offerings and expand its permanent menu lineup across U.S. outlets, reflecting growing consumer demand for flavorful chicken-based meals and innovation in dipping sauces across quick service restaurant formats.

Companies Covered in Dipping Sauce Market

- Nestlé S.A.

- Unilever PLC

- The Kraft Heinz Company

- McCormick & Company

- Kikkoman Corporation

- General Mills Inc.

- Conagra Brands

- Ajinomoto Co., Inc.

- Hormel Foods Corporation

- Kraft Heinz India

- Lee Kum Kee

- Del Monte Foods

- Oetker Group

- Associated British Foods

- Kraft Foods International

Frequently Asked Questions

The dipping sauce market is projected to reach US$25.1 billion in 2026.

Rising demand for convenience foods, expanding quick service restaurant networks, and growing preference for diverse global flavors drive the dipping sauce market.

The dipping sauce market is poised to witness a CAGR of 6.2% from 2026 to 2033.

Expansion of clean-label formulations, flavor innovation, and growth in digital grocery and quick service restaurant channels create key market opportunities.

Some of the key market players include Nestlé S.A., Unilever PLC, The Kraft Heinz Company, McCormick & Company, Kikkoman Corporation, and General Mills.