- Food Ingredients & Additives

- Stabilized Starch Market

Stabilized Starch Market Size, Share, and Growth Forecast, 2026 - 2033

Stabilized Starch Market by Product Type (Cationic Stabilized Starch, Etherified Stabilized Starch, Others), Raw Material (Corn, Wheat, Cassava, Potato), Function Type (Thickeners, Stabilizers, Binders, Emulsifiers), and Regional Analysis for 2026 - 2033

Stabilized Starch Market Size and Trends Analysis

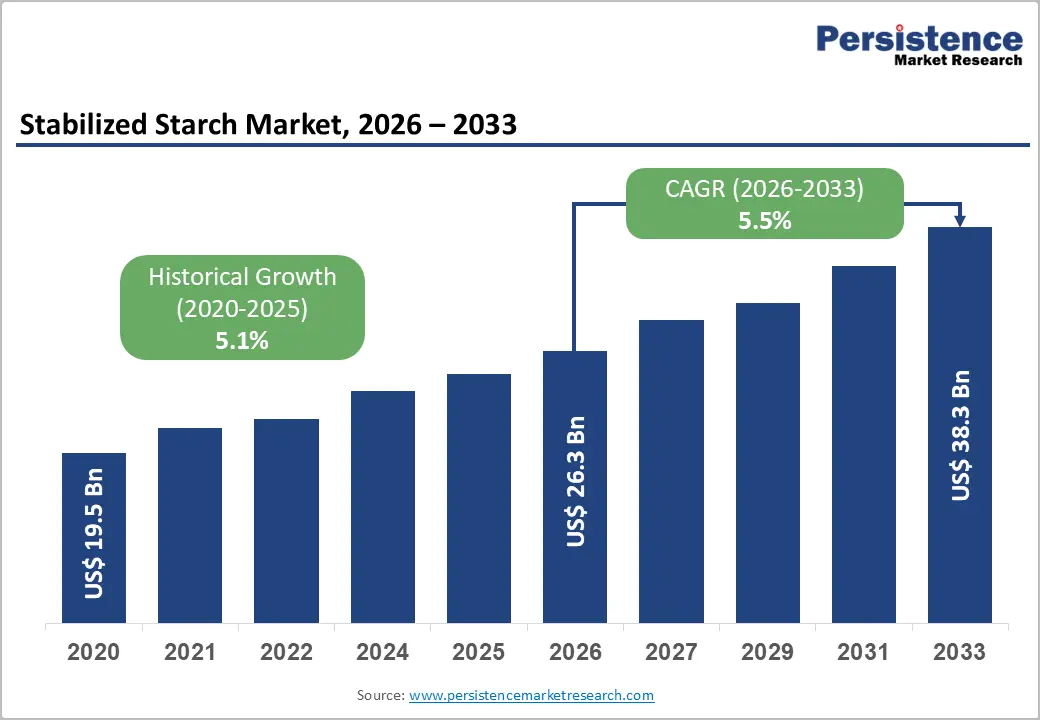

The global stabilized starch market size is likely to be valued at US$26.3 billion in 2026 and is expected to reach US$38.3 billion by 2033, growing at a CAGR of 5.5% during the forecast period from 2026 to 2033, driven by rising demand for clean-label and functional food ingredients, accelerating adoption in paper & packaging industries, and increased use in pharmaceutical applications. Regulatory emphasis from bodies such as the FDA on transparent labeling and safer food additives is accelerating the shift away from synthetic stabilizers.

According to the FDA, many stabilized starches fall under the GRAS (Generally Recognized as Safe) category, meaning they can be used in food without pre-market approval if supported by scientific consensus and historical safe use. This regulatory clarity is strengthening market growth as manufacturers increasingly adopt stabilized starch in bakery, dairy, sauces, and convenience foods to meet functional and safety standards.

Key Industry Highlights:

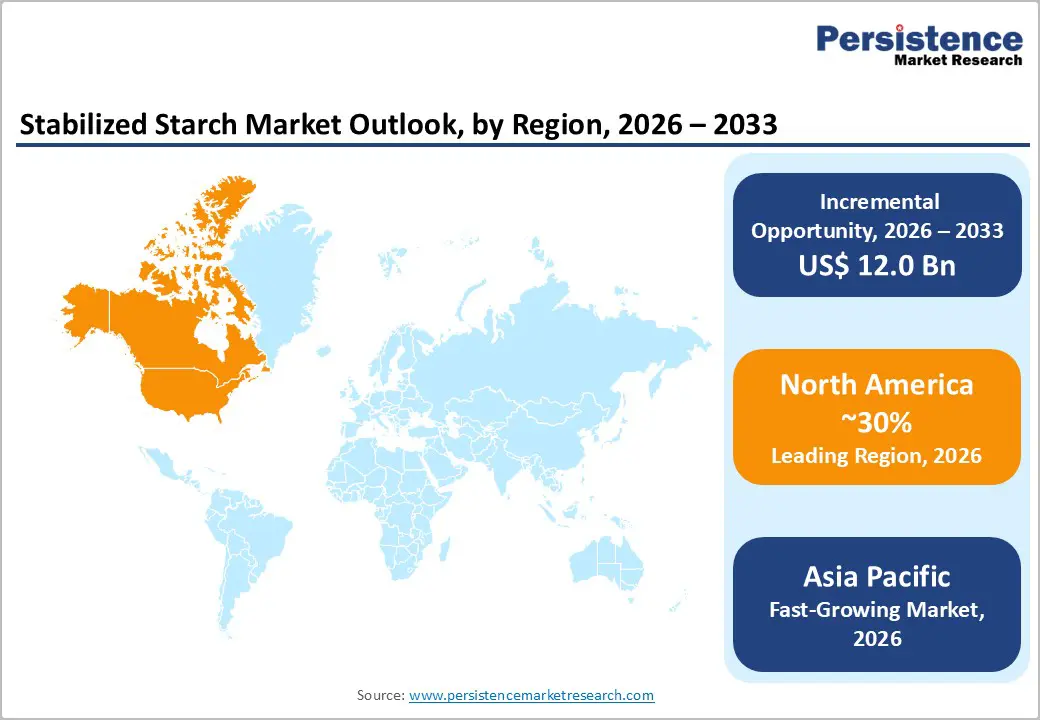

- Leading Region: North America is anticipated to be the leading region, accounting for 30% market share in 2026, driven by strong processed food demand, clean-label innovation, and adoption of FDA-regulated functional ingredients.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by rapid growth in processed foods, expanding food manufacturing bases, and strong adoption across China, India, and ASEAN economies.

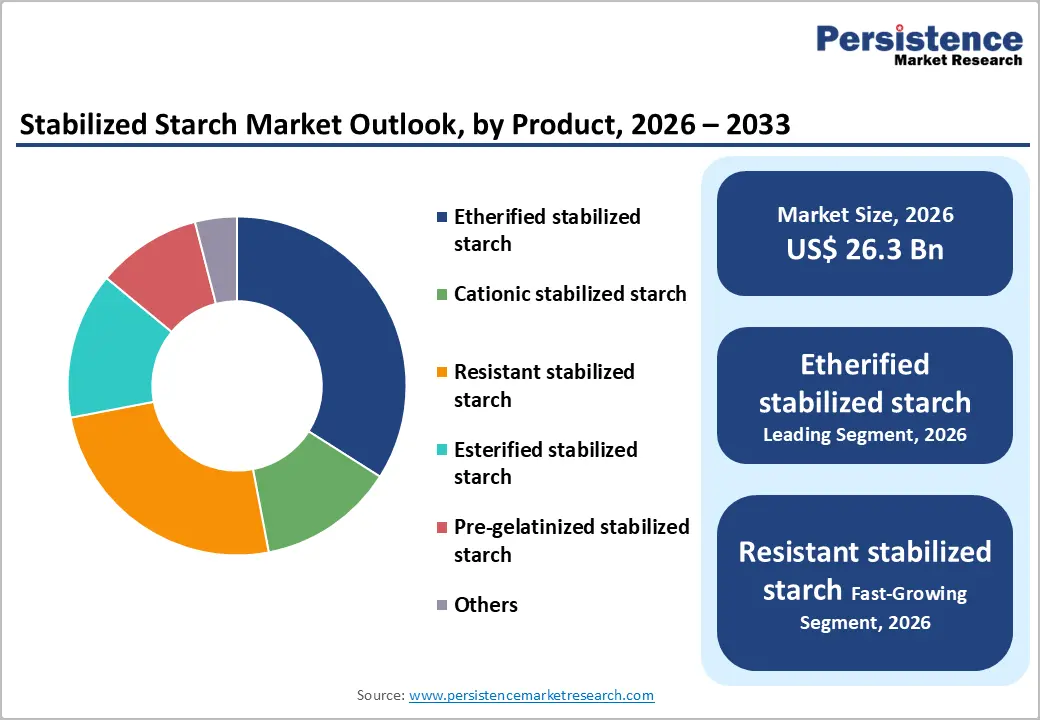

- Leading Product Type: Etherified stabilized starch is projected to represent the leading product type in 2026, accounting for 35% of the revenue share, driven by superior freeze-thaw stability and clarity in food applications.

- Leading Raw Material: Corn is anticipated to be the leading raw material, accounting for over 45% of revenue in 2026, supported by ample availability and robust processing infrastructure.

- Key Opportunity: Expanding clean-label, plant-based, and functional food innovation, combined with growing processed food demand and sustainable ingredient development, represents the key market opportunity shaping the overall stabilized starch market.

DRO Analysis

Driver - Rising Demand for Processed and Convenience Foods

Increasing urbanization, busy lifestyles, and higher workforce participation are driving demand for ready-to-eat meals, packaged snacks, and instant food products. According to the FDA and USDA food consumption trend data (2024–2025), more than 70% of calories consumed in the U.S. come from ultra-processed and packaged foods, highlighting a strong dependence on processed food systems. Stabilized starch enhances texture, viscosity, and shelf stability in sauces, soups, bakery fillings, and dairy products, ensuring consistent quality during processing, freezing, and reheating.

FDA food additive regulations under 21 CFR (updated 2024–2026) support the safe use of modified food starches in processed foods, enabling widespread industrial adoption. Large-scale food manufacturers prefer stabilized starch due to its cost efficiency and functional versatility compared to natural thickeners.

Rising disposable incomes and changing dietary habits are increasing the consumption of packaged foods. This structural shift in eating patterns is creating sustained long-term demand for stabilized starch across multiple end-use industries, particularly in high-volume processed food applications.

Restraint - Consumer Preference for Clean-Label and Minimally Processed Ingredients

Modern consumers are increasingly concerned about food transparency, ingredient origin, and chemical modification processes used in food production. Stabilized starch, especially chemically modified variants, often faces scrutiny due to perceptions of artificiality or high processing. This has led some food manufacturers to reformulate products using simpler, natural alternatives such as native starches, gums, and plant-based hydrocolloids.

Regulatory bodies and food labeling standards are pushing manufacturers to disclose more about ingredient processing methods. Clean-label trends in North America and Europe are encouraging brands to reduce reliance on chemically modified starches in favor of enzyme-treated or physically modified alternatives. Consumer awareness campaigns and rising demand for “free-from” products are also influencing purchasing behavior.

Opportunity - Clean-Label and Plant-Based Protein Formulations

Consumers shift toward healthier and more sustainable diets, and food manufacturers are reformulating products to replace synthetic additives with natural and functional ingredients. Stabilized starch is increasingly used in plant-based dairy, meat substitutes, and protein-enriched foods to improve texture, binding, and moisture retention.

According to the FDA, Global plant-based food innovation data from 2025 industry assessments show that nearly 30% of new food product launches now include plant-based or clean-label positioning, reflecting rapid consumer adoption of healthier, more sustainable diets.

The 2024–2026 food innovation trend reports from FDA-aligned labeling frameworks and industry associations highlight strong growth in non-GMO, enzyme-treated, and physically modified starch solutions aligned with clean-label expectations. The expansion of plant-based food startups and food manufacturers investing in alternative proteins is accelerating demand. Stabilized starch is increasingly used in high-protein beverages, nutritional bars, and functional foods, where texture stability and mouthfeel are critical.

Category-wise Analysis

Product Type Insights

Etherified stabilized starch is expected to lead the stabilized starch market, accounting for approximately 35% of revenue in 2026, driven by its superior functional performance in food systems. It offers excellent freeze–thaw stability, high clarity, and strong resistance to acidic conditions, making it highly suitable for modern processed food formulations. For example, it is widely used in yogurt-based desserts and creamy salad dressings to maintain stability and visual appeal across shelf life.

Resistant stabilized starch is likely to represent the fastest-growing segment, supported by rising health awareness and demand for high-fiber, low-glycemic food products. It functions as a dietary fiber and fat replacer, supporting digestive health and weight management trends. Its compatibility with clean-label and nutritional formulations is increasing its adoption in functional foods. For instance, it is commonly used in high-fiber breakfast cereals and protein bars to improve texture while enhancing nutritional value.

Raw Material Insights

Corn-based stabilized starch is projected to lead the market, capturing around 45% of the revenue share in 2026, supported by its high availability, cost efficiency, and strong industrial processing infrastructure. Corn provides high starch yield and is widely cultivated across major producing regions, supporting large-scale modified starch manufacturing. A notable example includes corn-based stabilized starch, which is extensively used in instant soup mixes and canned gravies to maintain consistent thickness and texture during storage and reheating.

Cassava-based stabilized starch is likely to be the fastest-growing raw material, driven by increasing demand in emerging markets and clean-label food applications. Cassava is widely cultivated in tropical regions and offers a cost-effective, gluten-free alternative to traditional starch sources. Its neutral taste and smooth texture make it highly suitable for modern processed food formulations. For example, it is commonly used in instant noodles and bakery fillings to improve elasticity and consistency.

Function Type Insights

Thickeners are expected to lead the stabilized starch market, accounting for approximately 40% of revenue in 2026, driven by their essential role in controlling viscosity and improving texture in food products. They are widely used in sauces, soups, gravies, and dairy-based items where consistent mouthfeel and stability are critical. For instance, they are extensively used in canned pasta sauces to maintain uniform thickness and prevent separation during heating and storage.

Stabilizers are likely to represent the fastest-growing segment, supported by increasing demand for frozen foods, plant-based alternatives, and ready-to-eat meals. They help maintain texture, prevent phase separation, and improve product stability during freezing and thawing cycles. For example, they are used in plant-based yogurt drinks to maintain smooth consistency and prevent ingredient separation over shelf life.

Regional Insights

North America Stabilized Starch Market Trends

North America is anticipated to be the leading regional market, accounting for a market share of 30% in 2026, driven by strong demand from processed food, clean-label reformulation, and industrial applications. High consumption of ready-to-eat foods, advanced food processing infrastructure, and increasing adoption of functional ingredients in bakery, dairy, and sauces increase the demand. For example, Ingredion Incorporated has expanded its clean-label starch portfolio to support plant-based formulations and texture solutions.

U.S. Stabilized Starch Market Trends

The U.S dominates the regional market, contributing approximately 69% share, driven by its large-scale food processing industry, strong R&D capabilities, and rapid adoption of functional and fortified food products. Recent developments include increased demand for clean-label starch in plant-based dairy and high-protein foods.

Canada Stabilized Starch Market Trends

Canada holds a smaller but growing share of approximately 20%, supported by rising demand for organic, gluten-free, and sustainable food ingredients, along with government-backed food innovation initiatives. Food safety authorities such as Health Canada and the Canadian Food Inspection Agency promote safe use, clear labeling, and quality standards for food ingredients, including modified starches.

Europe Stabilized Starch Market Trends

Europe is likely to be a significant market for stabilized starch in 2026, growing at a CAGR of 3.7% due to advanced food processing, high demand for clean-label ingredients, and strict EU regulations promoting non-GMO and enzyme-modified starch solutions. The EU’s Farm to Fork strategy is driving sustainable sourcing and innovation in functional starch solutions. Companies such as Roquette Frères have expanded their plant-based and clean-label starch portfolio.

U.K. Stabilized Starch Market Trends

The U.K. holds an estimated 18% share, supported by rising demand for convenience foods, clean-label reformulation, and expansion of plant-based food production. Increasing focus on reducing artificial additives and improving ingredient transparency is driving starch innovation in the U.K.

Germany Stabilized Starch Market Trends

Germany dominates the regional market with approximately 21% share, driven by its strong food processing industry, advanced starch manufacturing capabilities, and increasing use of bio-based materials in industrial applications. Recent developments include growing investments in sustainable and biodegradable starch-based materials aligned with energy transition policies.

Asia Pacific Stabilized Starch Market Trends

The Asia Pacific region is likely to be the fastest-growing regional market, expanding at a CAGR of 6%, driven by rapid urbanization, strong food processing growth, and abundant agricultural raw materials. The region benefits from rising consumption of convenience foods, packaged snacks, and ready-to-eat meals across emerging economies. For example, Tate & Lyle PLC has expanded its specialty starch solutions in Asia to support clean-label and texture innovation in processed foods.

China Stabilized Starch Market Trends

China dominates the regional market with approximately 40% share, driven by its large-scale starch production, strong food processing industry, and expanding export-oriented manufacturing base. Recent developments include increased investment in corn and cassava processing facilities and rising demand from the convenience food and textile sectors.

India Stabilized Starch Market Trends

India holds approximately 25% share, supported by rapid growth in packaged foods, government-led food processing initiatives, and rising consumption of instant and ready-to-eat products. The country is witnessing expansion in starch manufacturing capacity and increasing use of stabilized starch in bakery, dairy, and snack applications.

Competitive Landscape

The global stabilized starch market exhibits a moderately fragmented structure, driven by the presence of large multinational ingredient companies alongside regional and niche producers specializing in customized starch solutions. The market is characterized by continuous innovation, expanding applications, and increasing demand for clean-label and functional ingredients.

With key leaders including Cargill, Incorporated, Ingredion Incorporated, Archer Daniels Midland Company, Tate & Lyle PLC, and Roquette Frères, the market is highly competitive and innovation-driven. These players compete through product innovation, clean-label starch development, strategic partnerships, and capacity expansions to meet evolving consumer and industrial demand.

Key Industry Developments:

- In October 2025, Roquette Frères launched AMYSTA™ L 123, a new label-friendly soluble pea starch developed through a chemical- and enzyme-free process to support clean-label food formulations.

- In April 2025, ingredient supplier Ulrick & Short launched its Synergie A range of clean-label stabilizing starches designed to enhance texture and stability in food products while enabling simpler and more transparent ingredient labeling.

- In March 2025, Cargill, Incorporated, inaugurated a new corn milling plant in Gwalior, India, in partnership with Saatvik Agro Processors to meet rising demand for starch derivatives used in confectionery, dairy, and infant nutrition applications.

Companies Covered in Stabilized Starch Market

- Cargill, Incorporated

- Ingredion Incorporated

- Tate & Lyle PLC

- Archer Daniels Midland Company

- Roquette Frères

- AGRANA Beteiligungs-AG

- Avebe U.A.

- BENEO GmbH

- Grain Processing Corporation

- Emsland Group

- Global Bio-Chem Technology Group Company Limited

- Tereos S.A.

- Penford Corporation

- Universal Starch Chem Allied Ltd.

Frequently Asked Questions

The global stabilized starch market is projected to reach US$26.3 billion in 2026.

Rising demand for processed and convenience foods, along with increasing adoption of clean-label and functional ingredients, drives the stabilized starch market.

The stabilized starch market is expected to grow at a CAGR of 5.5% from 2026 to 2033.

Growing demand for clean-label, plant-based, and functional food formulations presents key opportunities for the stabilized starch market.

Cargill, Incorporated, Ingredion Incorporated, Tate & Lyle PLC, Archer Daniels Midland Company, and Roquette Frères are the leading players.