- Medical Devices

- Dengue Rapid Tests Market

Dengue Rapid Tests Market Size, Share, and Growth Forecast 2026-2033

Dengue Rapid Tests Market by Test Type (NS1 Antigen Tests, IgG/IgM Antibody Tests, Combination Tests), by Technology (Lateral Flow Assay, Rapid ELISA), by End User (Hospitals & Clinics, Diagnostic Laboratories, Home Care/Self-testing, Public Health Centers), by Regional Analysis, 2026-2033

Dengue Rapid Tests Market Trends and Analysis

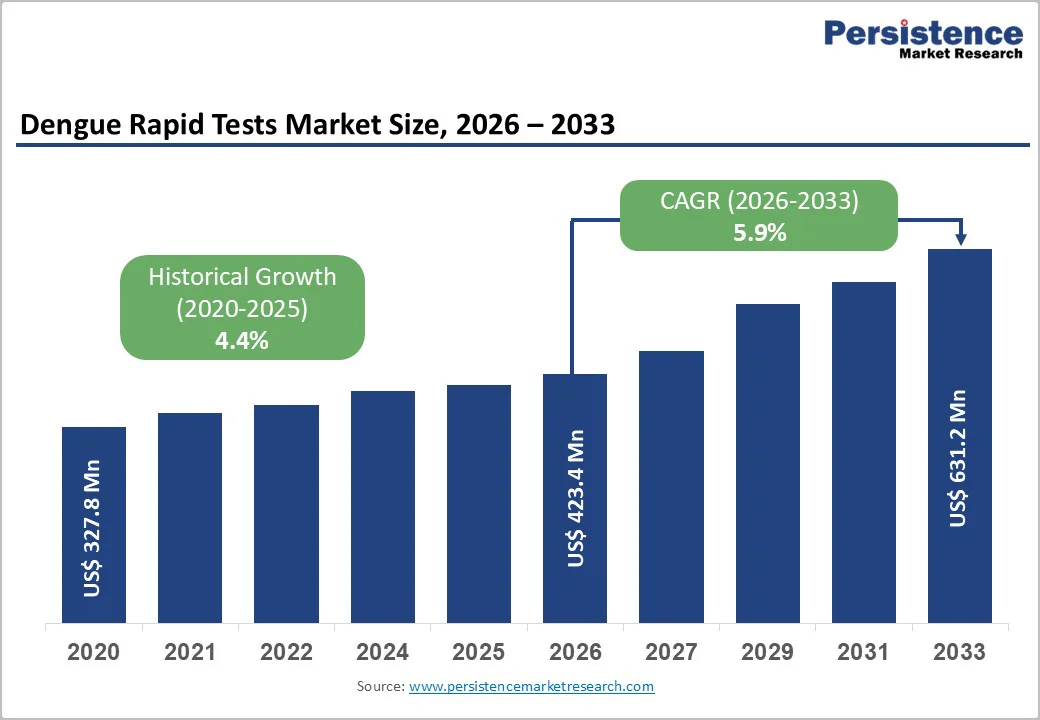

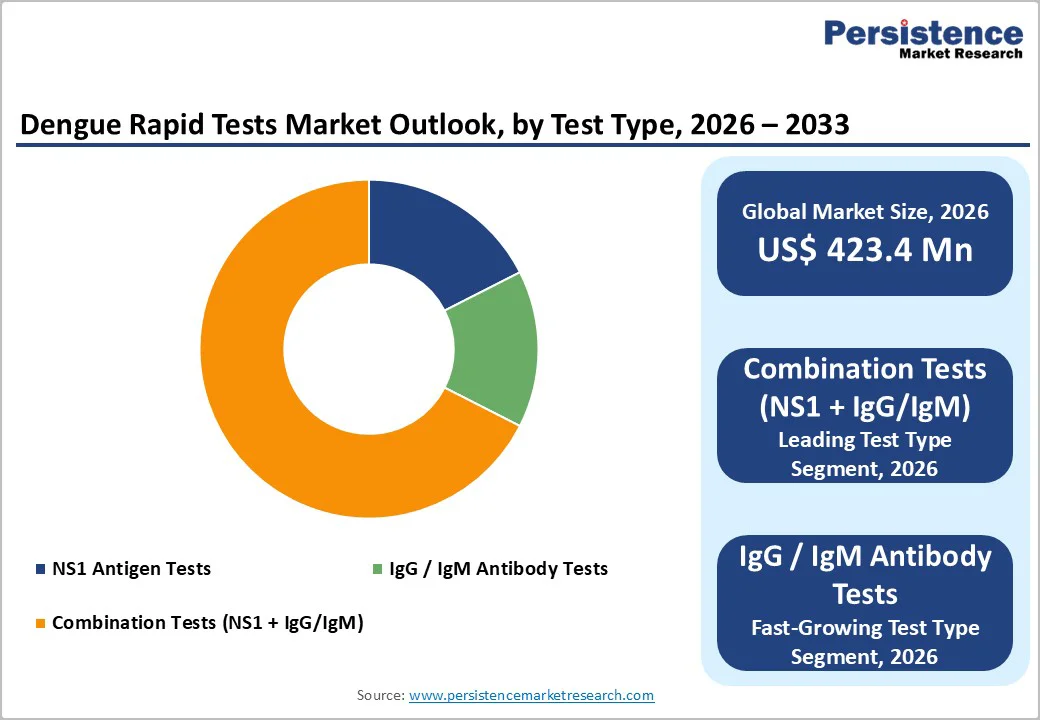

The global dengue rapid tests market is expected to be valued at US$ 423.4 million in 2026 and projected to reach US$ 631.2 million by 2033, growing at a CAGR of 5.9% between 2026 and 2033.

The market expansion is driven by unprecedented surge in dengue cases globally, with over 14.6 million cases reported in 2024 alone the highest annual record ever documented. The Americas region experienced particularly acute epidemics, with more than 13 million suspected cases, necessitating rapid diagnostic deployment. This massive disease burden has catalyzed aggressive government procurement programs, exemplified by Brazil’s distribution of 6.5 million rapid tests in 2025, marking the first systematic deployment of rapid diagnostics in the nation’s public health system. Additionally, the rising demand for point-of-care testing in resource-constrained and remote settings continues to fuel innovation in rapid test formats, supporting market growth substantially.

Key Market Highlights

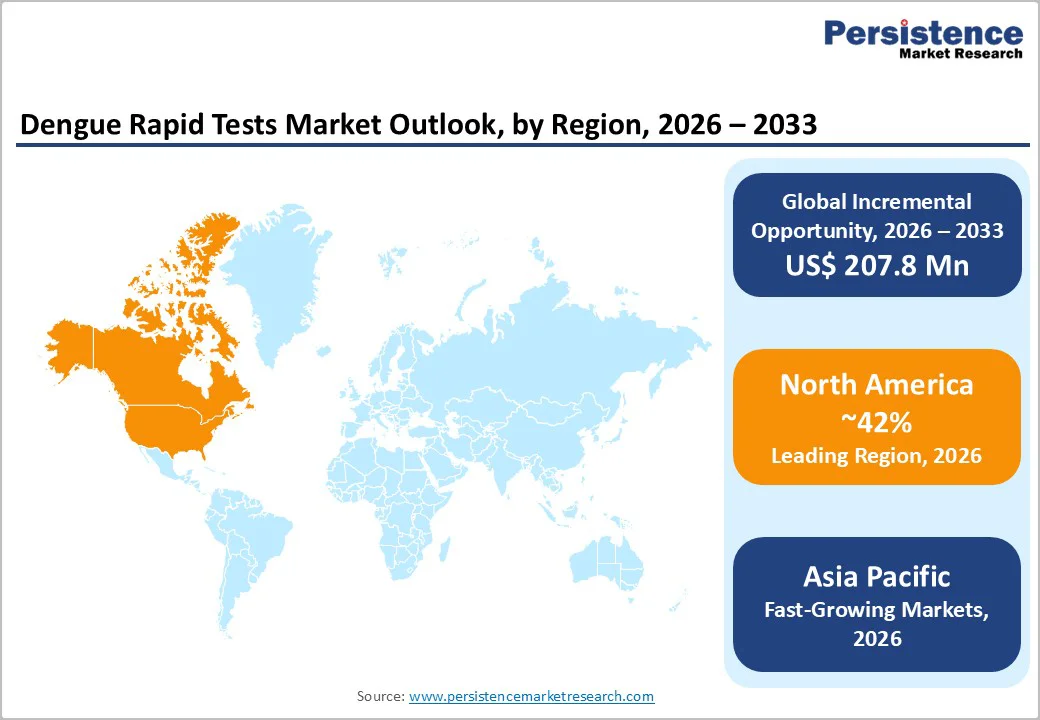

- North America dominates global market with 42% share, driven by robust diagnostic adoption in clinical settings, substantial public health investment following Puerto Rico emergency declaration with 6,291 confirmed cases in 2024, and stringent regulatory standards ensuring high-performance diagnostics.

- Asia Pacific experiences fastest regional growth at 5.12% CAGR through 2032, supported by world’s highest dengue disease burden concentrated in Southeast Asia, India, and China, government healthcare infrastructure investment, and rising awareness among expanding middle-class populations.

- Combination Tests (NS1 + IgG/IgM) command 54% market dominance, achieving superior diagnostic performance with 78.4-88.7% sensitivity through simultaneous detection across acute and convalescent infection phases, outperforming isolated antigen or antibody testing approaches.

- IgG/IgM antibody tests represent fastest-growing segment, driven by epidemiological surveillance applications, serological status determination, and post-epidemic investigation requirements across public health systems in endemic regions.

| Key Insights | Details |

|---|---|

| Dengue Rapid Tests Market Size (2026E) | US$ 423.4 million |

| Market Value Forecast (2033F) | US$ 631.2 million |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Dynamics

Market Growth Drivers

Escalating Global Dengue Epidemics and Case Surge

The dengue pandemic has reached unprecedented proportions, creating exceptional demand for rapid diagnostic solutions. In 2024, the World Health Organization (WHO) reported over 14.6 million dengue cases globally, representing a doubling of cases from 2023 and surpassing any previous annual record. The Americas region alone reported 13 million cases, with Brazil accounting for 6.3 to 9.8 million cases establishing it as the global epicenter of dengue transmission. The Pan American Health Organization (PAHO) noted that dengue incidence has accelerated alarmingly, with 400 cases per 100,000 population in Brazil’s peak epidemic months. This exponential case increase directly translates into magnified demand for diagnostic testing, overwhelming existing laboratory capacity and necessitating deployment of rapid tests as an essential triage and case identification tool across healthcare systems.

Government Initiatives and Public Health System Expansion

Government procurement programs have emerged as critical growth catalysts for the rapid tests market. Brazil’s Ministry of Health announced the distribution of 6.5 million rapid tests in 2025, with 4.5 million in the initial distribution phase, marking the first comprehensive deployment of dengue rapid diagnostics in the nation’s Unified Health System (SUS). This initiative targets basic health units and remote municipalities lacking access to laboratory infrastructure, addressing a critical diagnostic gap. Similarly, Puerto Rico declared a public health emergency in March 2024 due to rising cases, driving expanded testing infrastructure including rapid test adoption. Japan has mandated laboratory testing for dengue at quarantine stations under its Quarantine Law, creating consistent demand for validated diagnostics. These systematic government investments signal sustained procurement momentum and establish regulatory validation standards that strengthen market expansion across endemic and non-endemic regions.

Market Restraints

Regulatory Approval Barriers and Test Performance Variability

The dengue rapid tests market faces significant regulatory constraints that limit product deployment and clinical adoption. In the United States, the FDA has approved only one NS1 antigen test (the Detect NS1 ELISA by InBios International), while all other commercial dengue NS1 rapid diagnostic tests are classified as Research Use Only (RUO), restricting their clinical application. This stringent regulatory posture reflects concerns regarding diagnostic accuracy. Heterogeneity studies demonstrate that sensitivity for dengue IgM/IgG rapid tests ranges from 17.9% to 88.7%, depending on test type and detection target, compared to RT-PCR gold standards. Isolated NS1 rapid tests achieve sensitivities between 72-76.5%, whereas combination tests performing NS1 plus IgM/IgG detection improve sensitivity to 78.4-88.7%. This performance variability creates hesitation among healthcare systems regarding test adoption and has prompted WHO and regulatory authorities to emphasize laboratory-based confirmation for clinical decision-making, constraining the addressable rapid test market in high-income healthcare systems.

Infrastructure and Cost Barriers in Endemic-Country Healthcare Systems

Dengue rapid tests face deployment challenges in the very regions with the highest disease burden—tropical and subtropical developing nations with limited healthcare infrastructure. Many endemic countries lack sufficient laboratory technicians, equipment, cold chain logistics, and training capacity to optimize diagnostic utilization. The WHO explicitly noted that global shortages of high-quality dengue diagnostic kits, combined with inadequate trained clinical staff and vector control specialists, significantly constrain effective outbreak response. While rapid tests are more affordable than molecular diagnostics (typically US$ 1-3 per rapid test versus US$ 20-50 for RT-PCR), bulk procurement during epidemics strains budgets of already resource-constrained public health systems. Additionally, the lack of standardized testing protocols across endemic countries creates fragmented purchasing patterns, limiting economies of scale that would reduce per-unit costs and expanding market penetration.

Market Opportunities

Emerging Multiplex and Serotype-Specific Diagnostic Technologies

Advanced diagnostic technologies represent substantial market opportunities for companies developing next-generation dengue tests. Serotype-specific rapid testing emerged as an innovation frontier—VisGene Ltd launched the VisCheck™ Dengue NS1 Rapid Antigen Serotyping Test in Thailand in January 2025 following regulatory approval, offering the world’s first rapid test capable of identifying all four dengue serotypes while predicting severe disease risk in 15 minutes. Multiplex assay development enabling simultaneous detection of dengue with co-circulating arboviruses (chikungunya, Zika) addresses critical clinical needs, particularly given the 2024 emergence of dengue serotype 3 in Brazil after 16-year dormancy. Alternative molecular platforms, including RT-LAMP (reverse transcription loop-mediated isothermal amplification) and RT-RPA (reverse transcription recombinase polymerase amplification) demonstrate 96%+ sensitivity with 15-35 minute turnaround times, minimal equipment requirements, and cost-effectiveness suitable for field deployment. These emerging technologies are capturing significant research funding and regulatory attention, with substantial commercial potential as public health systems seek comprehensive diagnostic solutions during concurrent pathogen surges.

Category-wise Insights

Test Type Analysis

Combination Tests (NS1 + IgG/IgM) represent the dominant segment in the dengue rapid tests market, commanding approximately 54% market share in 2025. This leadership position reflects the clinical superiority of combination testing approaches simultaneous NS1 antigen detection combined with IgG/IgM antibody capture enables detection across the full diagnostic window of dengue infection, from acute phase (0-7 days) through convalescent phase. Clinical validation studies demonstrate that combination tests achieve sensitivity of 78.4-88.7% compared to RT-PCR reference standards, substantially outperforming isolated NS1 tests (72-76.5% sensitivity) or IgM/IgG-only tests. Standard Diagnostics’ Bioline Dengue Duo and Abbott’s SD Bioline products exemplify this category, with reported sensitivities of 92.8% for NS1 antigen and 99.4% for IgM/IgG detection. IgG/IgM antibody tests represent the fastest-growing segment within this category, driven by their utility in identifying recent infections and establishing serological status for epidemiological surveillance, particularly valuable in post-epidemic investigation and seroprevalence studies.

End User Analysis

Diagnostic Laboratories emerge as the leading end-user segment, accounting for approximately 44% market share in 2025. This dominance reflects the laboratory network’s centrality in dengue surveillance systems, referral testing for complex cases, and outbreak investigation requiring serotype confirmation. Clinical laboratories have substantially upgraded testing capacity through investments in high-throughput ELISA platforms and RT-PCR systems, enabling same-day turnaround and integration of dengue testing into comprehensive infectious disease panels. LabCorp and Quest Diagnostics in North America exemplify this trend, integrating dengue RT-PCR into their service offerings. Home Care/Self-testing represents the fastest-growing end-user category, with India’s first home-use dengue test launched in August 2024 by J Mitra & Company demonstrating substantial market potential. Self-testing adoption is particularly pronounced in Asia Pacific and Latin America, where patient-initiated testing during symptomatic episodes reduces clinic burden and enables early clinical intervention, addressing critical gaps in outbreak response capacity.

Regional Insights

North America Dengue Rapid Tests Market Trends

North America commands approximately 42% of the global dengue rapid tests market in 2025, establishing it as the dominant regional market despite significantly lower endemic disease burden compared to tropical regions. This market leadership reflects robust regulatory frameworks, high diagnostic adoption rates in clinical settings, and substantial public health investments. Puerto Rico, a U.S. territory, declared a public health emergency in March 2024 due to rapidly escalating dengue cases, with 6,291 confirmed cases reported during 2024, representing a dramatic increase from prior years. This emergency declaration catalyzed accelerated diagnostic infrastructure expansion, including expanded adoption of rapid diagnostic tests and molecular assays across healthcare facilities. Point-of-care testing (POCT) adoption has significantly expanded in U.S. hospitals and clinics, supported by the availability of FDA-cleared and CE-marked diagnostics that meet stringent performance standards. Roche Diagnostics, Abbott Laboratories, and Bio-Rad Laboratories maintain substantial market presence in North America, with regular product innovations and regulatory approvals. The region’s mature healthcare infrastructure, combined with heightened clinical awareness of dengue risk from imported cases and international travel, ensures sustained demand for reliable, rapid diagnostics, supporting continued market expansion at rates exceeding global growth averages.

Asia Pacific Dengue Rapid Tests Market Trends

Asia Pacific represents the fastest-growing regional market for dengue rapid tests, projected to achieve 5.12% CAGR from 2025-2032 outpacing global growth rates substantially. This regional leadership reflects the world’s highest dengue disease burden concentrated in Southeast Asia, India, China, and Japan, combined with rapid healthcare infrastructure modernization and expanding public health investment. China maintains a substantial Asia Pacific market share, with southern regions, including Guangzhou, reporting 69.2% of mainland China’s dengue cases, driving sustained diagnostic demand. India experiences endemic dengue transmission across tropical regions with peak seasonal epidemics, supporting growing adoption of rapid tests in public health centers, diagnostic laboratories, and increasingly in home testing following the August 2024 launch of India’s first self-test kit by J Mitra & Company. Japan, despite its non-endemic dengue status, mandates laboratory testing at quarantine stations under its Quarantine Law, creating consistent demand for validated diagnostics among international travelers. Southeast Asian countries, including Malaysia, the Philippines, Vietnam, Thailand, and Indonesia, have implemented enhanced dengue surveillance programs with government funding for improved healthcare facility infrastructure, laboratory automation, and rapid test deployment. This regional expansion of healthcare investment, combined with rising middle-class awareness and demand for convenient diagnostics, establishes Asia Pacific as the highest-growth market for dengue rapid tests globally.

Competitive Landscape

Market Structure Analysis

The Dengue Rapid Tests Market is highly competitive, dominated by global players like Abbott Laboratories, Roche Diagnostics, Bio-Rad, Thermo Fisher, and SD Biosensor. Companies compete on product innovation, test accuracy, speed, and cost-effectiveness, with increasing focus on combination NS1 + IgG/IgM tests that offer comprehensive detection. Regional players such as J. Mitra & Co. and GenBody also capture market share in Asia and Latin America. Strategic initiatives include new product launches, partnerships, and distribution expansion to reach hospitals, diagnostic labs, and home users.

Key Market Developments

- In August 2024, J. Mitra & Company launched the Dengue NS1 Antigen self-test kit, marking the first such self-test/home-test kit in India. The kit allowed users to conduct the test independently at any location. It provided results within 20 minutes, with a rapid visual test for easy interpretation.

Companies Covered in Dengue Rapid Tests Market

- Abbott Laboratories

- Roche Diagnostics

- Bio-Rad Laboratories

- Thermo Fisher Scientific

- SD Biosensor

- InBios International

- QuidelOrtho

- bioMérieux

- CTK Biotech

- GenBody

- J Mitra & Company

- VisGene Ltd

Frequently Asked Questions

The global dengue rapid tests market is expected to reach US$ 423.4 million in 2026.

Increasing outbreaks and endemic prevalence in tropical and subtropical regions drive demand for quick and reliable diagnostics.

North America maintains market leadership with approximately 42% share in 2025, driven by substantial healthcare infrastructure investment, regulatory stringency ensuring high-performance diagnostics.

Rapid tests in clinics, community health centers, and mobile screening units.

Abbott Laboratories, Roche Diagnostics, Bio-Rad Laboratories, SD Biosensor, and Thermo Fisher Scientific maintain dominant market positions through comprehensive product portfolios and global distribution networks.