- Automotive Components & Materials

- Connected Tires Market

Connected Tires Market Size, Share, and Growth Forecast 2026 - 2033

Connected Tires Market by Product Type (Smart Tires, Sensor-Based Tires, RFID-Enabled Tires, TPMS-Integrated Tires, Predictive Analytics Tires), Connectivity Type (Tire-to-Vehicle (V2T), Tire-to-Cloud (T2C), Tire-to-Infrastructure (T2I), V2X Integration), Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles, Buses & Coaches), by Application, End-user, and Regional Analysis, 2026 - 2033

Connected Tires Market Size and Trend Analysis

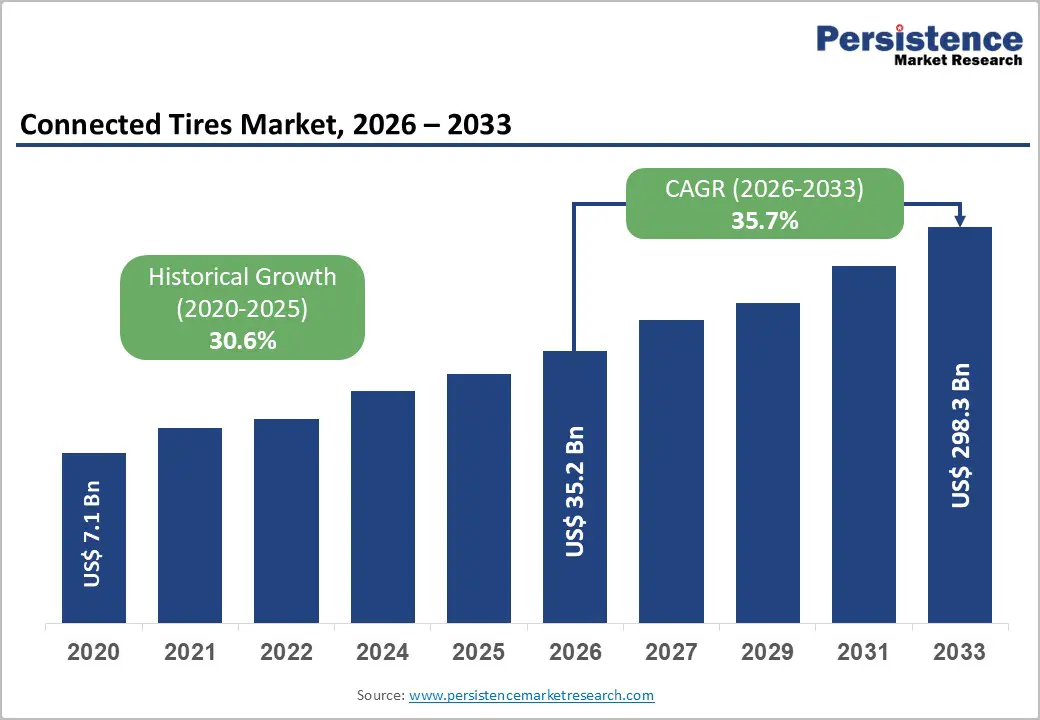

The global connected tires market is expected to reach US$35.2 billion in 2026 and US$298.3 billion by 2033, growing at an exceptional CAGR of 35.7% over the forecast period from 2026 to 2033.

The connected tires market is at the forefront of automotive technology convergence, with near-exponential growth driven by the global electrification of vehicle fleets, the proliferation of autonomous and connected driving systems, and escalating regulatory mandates for real-time tire safety monitoring.

Key Industry Highlights:

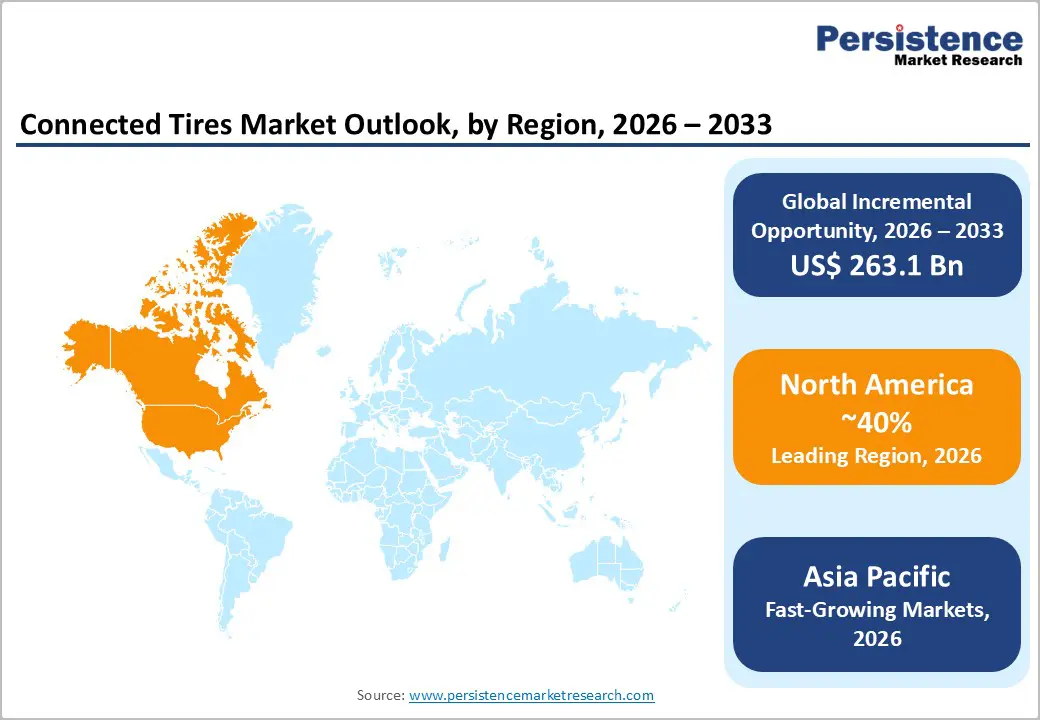

- Leading Region: North America leads the connected tires market, holding 40% share, anchored by universal U.S. NHTSA TPMS mandates since 2008, Goodyear and Bridgestone Americas' R&D leadership, the world's most advanced autonomous vehicle development ecosystem, and USDOT V2X infrastructure deployment programs stimulating T2I connected tire applications.

- Fastest-Growing Region: Asia Pacific is the fastest-growing market with a CAGR of 40%, driven by China's 9 million+ NEV sales in 2023 per CAAM, creating massive BEV-specific connected tire demand, Japan's Bridgestone and Yokohama smart tire platforms, and India's imminent commercial vehicle TPMS mandate from MoRTH.

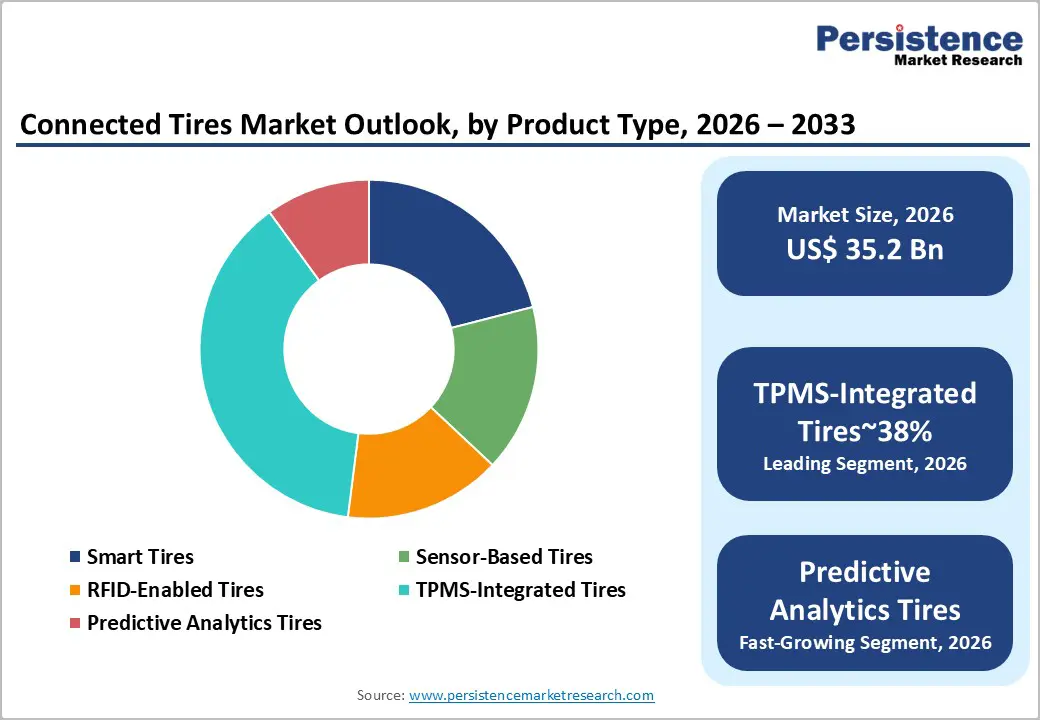

- Dominant Product: TPMS-integrated tires account for 38% of the product type category, supported by universal regulatory mandates from the U.S. NHTSA and EU Regulation 661/2009 across 85 million+ annual vehicle production units, creating the world's largest mandatory connected tire deployment platform.

- Fastest Growing Product Segment: Predictive Analytics Tires represent the fastest growing product segment, powered by AI integration, fleet telematics adoption, and tire-as-a-service business model expansion, with Bridgestone and Michelin reporting 25% incident reduction potential from predictive maintenance connectivity for commercial fleets.

- Key Opportunity: V2X integration enabling Tire-to-Infrastructure connectivity creates a transformational new demand tier, with 70+ active global V2X deployment projects and EU C-Roads Platform funding creating infrastructure for real-time road condition data delivery from connected tire telemetry systems.

Market Dynamics

Drivers - Mandatory TPMS Regulations and Expanding Global Tire Safety Legislation

Regulatory mandates for Tire Pressure Monitoring Systems (TPMS) have established the foundational demand layer for connected tire technology and continue to expand globally. The U.S. Transportation Recall Enhancement, Accountability, and Documentation (TREAD) Act and subsequent NHTSA FMVSS No. 138 regulation mandated TPMS on all new passenger vehicles in the United States from 2008, establishing a consumer expectation baseline.

The European Parliament's Regulation (EU) 661/2009 extended TPMS mandates across the EU, and UNECE Regulation 64 has enabled adoption by over 60 contracting parties globally, including Japan, South Korea, and Australia. As these regulations evolve toward more comprehensive real-time data requirements, including tread depth and temperature monitoring, they are compelling tire manufacturers and OEMs to embed progressively more sophisticated sensor systems, expanding the addressable market for advanced connected tire solutions well beyond basic pressure monitoring.

Autonomous and Electric Vehicle Proliferation Demanding Advanced Tire Intelligence

The global transition to autonomous vehicles (AVs) and battery electric vehicles (BEVs) is a powerful structural demand driver for connected tire intelligence. AVs require real-time tire condition data, pressure, temperature, tread wear, and road friction coefficient as critical sensor inputs for autonomous navigation and safety systems. The SAE International's Level 3 and above autonomous driving specifications explicitly require comprehensive vehicle state monitoring, including tire parameters.

BEVs generate significantly higher torque loads and exhibit different wear patterns than ICE vehicles, making real-time tread wear and load monitoring particularly critical. The International Energy Agency (IEA) reports that global EV sales surpassed 14 million units in 2023, a 35% year-on-year increase, creating a rapidly expanding installed base of vehicles requiring advanced connected tire systems compatible with EV-specific performance and safety requirements.

Restraints - High System Integration Costs and OEM Adoption Complexity

Integrating advanced connected tire systems, encompassing embedded sensors, wireless communication modules, onboard data processors, and cloud connectivity, into vehicle architectures adds high per-unit costs that constrain adoption in cost-sensitive vehicle segments. The incremental cost of advanced tire sensor systems over standard TPMS can range from US$ 50 to US$ 300+ per vehicle, depending on feature complexity.

For mass-market passenger vehicle manufacturers operating on thin margins, this cost addition requires OEM-level validation, integration engineering, and consumer value proposition justification that slow adoption timelines in non-premium segments, particularly in price-sensitive markets, including India, Southeast Asia, and Latin America.

Data Privacy, Cybersecurity Vulnerabilities, and Regulatory Compliance Uncertainty

Connected tire systems generate continuous streams of vehicle location, driving behavior, and road condition data, raising significant privacy and cybersecurity concerns that create regulatory and consumer adoption barriers. The UNECE WP.29 Cybersecurity Regulation (UN R155) mandating vehicle cybersecurity management systems from 2022 creates compliance requirements for connected tire system vendors.

Data sovereignty laws, including the EU General Data Protection Regulation (GDPR) and China's Personal Information Protection Law (PIPL), impose data localization and consent requirements on tire telemetry platforms, increasing compliance costs and complicating global deployment strategies for connected tire data service providers.

Opportunities - Commercial Fleet Telematics and Predictive Maintenance as a Service

Commercial fleet operators, trucking companies, bus operators, and logistics providers offer the highest near-term value for connected tires, supported by the strong ROI of predictive tire maintenance in high-utilization, multi-vehicle operations. The American Trucking Associations (ATA) estimates that tire-related issues are among the leading causes of commercial vehicle roadside breakdowns and accidents in the United States, and that tire maintenance costs represent a significant proportion of total fleet operating expenses.

Real-time connected tire data enabling predictive maintenance, alerting fleet managers to abnormal pressure, temperature, and wear patterns before failure, can reduce tire-related incidents by up to 25% according to industry case studies from Bridgestone Corporation and Michelin Group. Subscription-based tire-as-a-service (TaaS) models, where manufacturers retain tire ownership and charge per kilometer, embed connected monitoring as an operational necessity, creating recurring revenue streams for tire OEMs.

V2X Integration and Smart Infrastructure: Creating a New Connectivity Tier

The emergence of Vehicle-to-Everything (V2X) communication infrastructure, standardized under IEEE 802.11p (DSRC) and 3GPP C-V2X (Cellular V2X) specifications, is creating a transformational opportunity for connected tire systems to interact with road infrastructure, traffic management systems, and other vehicles in real time. When tire condition data is shared via T2I (Tire-to-Infrastructure) channels, it enables novel applications such as real-time road surface condition mapping, dynamic speed limit adjustment based on aggregate fleet tire friction data, and automated weather hazard alerts.

The European Commission's C-Roads Platform and the U.S. Department of Transportation's V2X deployment programs are actively funding infrastructure enabling these applications. As V2X-equipped road infrastructure scales, with over 70 V2X deployment projects active globally, connected tire data becomes a foundational input for intelligent transportation system optimization, creating a new demand tier for T2I-capable sensor systems.

Category-wise Analysis

By Product Type Insights

TPMS-Integrated Tires are the dominant product type, accounting for approximately 38% of the connected tire market. Their leadership reflects the near-universal regulatory mandate for TPMS across major automotive markets, established by the U.S. NHTSA since 2008 and the EU Regulation 661/2009, which has created a massive installed base of TPMS-capable tires across global passenger vehicle fleets.

The technology's maturity, proven reliability, and cost-effectiveness compared to more advanced smart tire variants sustain its segment dominance. Every new passenger vehicle sold in the U.S., EU, Japan, South Korea, and an expanding list of global markets is equipped with TPMS, with annual new-vehicle production exceeding 85 million units, according to OICA. Predictive Analytics Tires represent the fastest-growing sub-segment as AI integration matures.

By Connectivity Type Insights

Tire-to-Vehicle (V2T) is the dominant connectivity type segment, accounting for approximately 52% of the market. V2T connectivity, in which tire sensors transmit data directly to the vehicle's onboard computer or telematics unit via short-range wireless (typically 315 MHz or 433 MHz RF protocols or Bluetooth Low Energy), is the most widely adopted connected tire architecture. Its dominance reflects the existing widespread deployment of TPMS systems and direct-fit OEM integration by automotive manufacturers.

Semiconductor suppliers, including NXP Semiconductors N.V. and Infineon Technologies AG, are leading suppliers of V2T TPMS transceiver chips. While T2C (Tire-to-Cloud) connectivity is growing rapidly for fleet telematics and analytics applications, V2T remains the dominant real-time safety monitoring architecture given its established OEM integration and low latency.

By Vehicle Type Insights

Passenger Vehicles are the dominant vehicle type segment, representing approximately 55% of the connected tires market. The sheer scale of the global passenger car fleet, estimated at over 1.4 billion vehicles globally according to the International Organization of Motor Vehicle Manufacturers (OICA), combined with universal regulatory TPMS mandates in key markets, creates the largest absolute installed base for connected tire technology.

Every new passenger vehicle produced for the U.S., EU, Japanese, and Korean markets requires compliant TPMS, generating annual sensor procurement volumes in the hundreds of millions of units. However, Heavy Commercial Vehicles represent the fastest-growing and highest-value per-unit connected tire segment, as fleet operators' ROI-driven adoption of advanced predictive maintenance systems drives disproportionate revenue growth in the HCV tier.

By Application Insights

Tire pressure monitoring remains the dominant application segment, accounting for approximately 42% of connected tire market revenue. Pressure monitoring is the foundational connected tire application, mandated by law across major automotive markets and the entry point through which the connected tire ecosystem has been built.

The U.S. National Highway Traffic Safety Administration (NHTSA) estimates that tire underinflation contributes to approximately 11,000 tire-related crashes annually in the United States alone, providing a compelling safety justification for mandated monitoring. Despite its maturity, pressure monitoring is evolving, with next-generation systems capable of detecting micro-leaks, predicting valve failures, and integrating with vehicle ADAS systems, sustaining ongoing technology investment and hardware upgrade cycles that preserve the segment's revenue leadership.

By End-User Insights

The Automotive end-use segment dominates the connected tires market, accounting for approximately 58% of total market revenue. Automotive OEMs, including Toyota Motor Corporation, Volkswagen AG, General Motors, and Stellantis, are the primary integrators of TPMS and connected tire technologies into new vehicle architectures.

The OICA reports that global vehicle production exceeds 85 million units annually, with TPMS-mandated markets accounting for the majority of that volume. The transition to electrified and autonomous vehicles is compelling automotive OEMs to integrate increasingly sophisticated tire telemetry, positioning the automotive end-use as the innovation frontier and primary volume driver for connected tire hardware, software, and data services throughout the forecast period.

Regional Insights

North America Connected Tires Market Trends & Analysis

North America represents a mature yet innovation-driven connected tires market, supported by early TPMS mandates and strong V2X infrastructure investments. The region accounts for approximately 40% of the global market in 2026, driven by autonomous vehicle development, fleet telematics adoption, and the strong presence of leading tire manufacturers and mobility tech firms.

- U.S. Connected Tires Market Size

The U.S. dominates North America with nearly 80% regional share. Growth is fueled by regulatory mandates, advanced autonomous vehicle programs, and large commercial fleet penetration. Increasing integration of predictive tire analytics in logistics and mobility platforms continues to expand the addressable market.

Europe Connected Tires Market Trends, Drivers & Insights

Europe is a regulatory-led market, accounting for around 28% of the global share. Strong safety regulations, OEM integration, and connected mobility initiatives drive adoption. The region benefits from established automotive supply chains and leadership in smart tire innovation and deployment across passenger and commercial vehicles.

- Germany Connected Tires Market Size

Germany leads Europe with approximately 30% regional share. Its dominance is supported by strong OEM presence, engineering excellence, and integration of connected tire technologies into premium vehicles and industrial transport systems.

- U.K. Connected Tires Market Size

The U.K. contributes around 18% of the European market. Growth is driven by smart mobility initiatives, insurance telematics adoption, and increasing deployment in fleet and logistics sectors.

- France Connected Tires Market Size

France holds approximately 15% share, supported by strong domestic tire manufacturing and innovation ecosystems. Connected tire adoption is growing across motorsports, passenger vehicles, and fleet management applications.

Asia Pacific Connected Tires Market Drivers & Analysis

Asia Pacific is the fastest-growing region, accounting for 30% of the global market. Growth is driven by EV expansion, regulatory developments, and increasing vehicle production. The region offers significant opportunities due to large-scale adoption potential and evolving smart mobility ecosystems.

- China Connected Tires Market Size

China dominates Asia Pacific with nearly 50% regional share. Strong EV adoption, government digitalization initiatives, and large automotive production volumes position China as the primary growth engine for connected tire technologies.

- India Connected Tires Market Size

India is an emerging market, accounting for around 10% of the share. Growth is supported by upcoming TPMS regulations, expanding commercial vehicle fleets, and increasing focus on road safety and fleet efficiency.

- Japan Connected Tires Market Size

Japan accounts for approximately 20% of the Asia Pacific market. Advanced automotive technologies, a strong OEM ecosystem, and early adoption of smart mobility solutions support steady growth in connected tire deployment.

Competitive Landscape

The Connected Tires Market exhibits a moderately fragmented structure, combining global tire majors, Bridgestone Corporation, Michelin Group, Goodyear Tire & Rubber Company, and Continental AG, with semiconductor and sensor specialists including NXP Semiconductors N.V. and Infineon Technologies AG.

Market leaders differentiate through proprietary embedded sensor platforms, cloud analytics ecosystems, fleet telematics integration, and OEM supply agreements with premium vehicle manufacturers. Key strategies include tire-as-a-service (TaaS) business model development, strategic partnerships with autonomous vehicle developers and logistics technology platforms, and investment in AI-based predictive tire analytics. Emerging trends include digital twin tire platforms, blockchain-based tire lifecycle traceability, and integration of connected tire data into vehicle insurance telematics programs, reflecting the market's evolution from hardware to data service value models.

Key Developments:

- February, 2025: Bridgestone Corporation launched its Tire Data ID™ 2.0 platform, featuring AI-powered predictive tread wear analytics and Tire-to-Cloud (T2C) connectivity targeting commercial fleet operators in North America and Europe, with real-time alerts integrated into fleet management systems.

- October, 2024: Michelin Group announced a strategic partnership with Stellantis N.V. to develop next-generation embedded smart tire sensors for Stellantis' upcoming BEV platforms, integrating real-time load monitoring, road condition detection, and autonomous driving data feeds across multiple Stellantis brands.

- May, 2024: Continental AG introduced its ContiSense Pro tire sensing technology incorporating compound-embedded electronic sensors capable of detecting road surface temperature and friction coefficient, supplying real-time data to ADAS and autonomous driving systems in partnership with multiple European OEMs.

Connected Tires Market- Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 7.1 Bn |

| Current Market Value (2026) | US$ 35.2 Bn |

| Projected Market Value (2033) | US$ 298.3 Bn |

| CAGR (2026 - 2033) | 35.7% |

| Leading Region | North America, 40% share |

| Dominant Application | TPMS-Integrated Tires, 38% share |

| Top-ranking Product | Automotive, 58% |

| Incremental Opportunity | US$ 263.1 Bn |

Companies Covered in Connected Tires Market

- Bridgestone Corporation

- Michelin Group

- Goodyear Tire & Rubber Company

- Continental AG

- Pirelli & C. S.p.A.

- Sumitomo Rubber Industries Ltd.

- Hankook Tire & Technology Co., Ltd.

- Yokohama Rubber Co., Ltd.

- Nokian Tyres plc

- Apollo Tyres Ltd.

- Toyo Tire Corporation

- NXP Semiconductors N.V.

- Infineon Technologies AG

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- Sensata Technologies

- Pacific Industrial Co., Ltd.

- Schrader International

Frequently Asked Questions

The global Connected Tires Market is estimated at US$ 35.2 billion in 2026 and is projected to reach US$ 298.3 billion by 2033, at an exceptional CAGR of 35.7%. This represents an acceleration from the already high historical CAGR of 30.6% from 2020 to 2025, reflecting the compounding effect of regulatory mandates, EV proliferation, and autonomous vehicle development on connected tire technology demand.

Key drivers include NHTSA FMVSS No. 138 and EU Regulation 661/2009 establishing universal TPMS mandates, the IEA-reported 14 million global EV sales in 2023 (35% YoY growth) creating BEV-specific tire monitoring demand, and SAE International Level 3+ autonomous driving specifications requiring real-time tire condition data as essential vehicle state inputs for navigation and safety systems.

TPMS-Integrated Tires dominate with approximately 38% market share, driven by universal regulatory mandates enforced by U.S. NHTSA and EU regulations across the majority of global passenger vehicle markets. With global vehicle production exceeding 85 million units annually per OICA, the mandatory TPMS deployment creates an unmatched volume foundation that sustains TPMS-integrated tires' market leadership.

North America is the leading regional market, anchored by the United States' world-first TPMS mandate since 2008, the USDOT's V2X infrastructure programs advancing T2I connectivity, and the presence of global connected tire leaders including Goodyear Tire & Rubber Company and Bridgestone Americas. The region's advanced AV development ecosystem, including Tesla, Waymo, and multiple OEM programs, creates the most technically demanding connected tire specification environment globally.

The highest-value opportunities are commercial fleet predictive maintenance as a service, where Bridgestone and Michelin report up to 25% incident reduction potential for fleet operators, and V2X Tire-to-Infrastructure integration, with 70+ active global V2X deployment projects and the EU C-Roads Platform creating a new tier of connected tire data value for road safety and traffic management applications.

Leading companies include Bridgestone Corporation, Michelin Group, Goodyear Tire & Rubber Company, Continental AG, Pirelli & C. S.p.A., NXP Semiconductors N.V., Infineon Technologies AG, Robert Bosch GmbH, and ZF Friedrichshafen AG. These companies compete on sensor miniaturization capability, cloud analytics platform depth, OEM integration relationships, tire-as-a-service business model maturity, and the ability to deliver real-time predictive intelligence from embedded tire sensor data.