- Automotive Components & Materials

- Automotive LED Lighting Market

Automotive LED Lighting Market Size, Share, and Growth Forecast 2026 – 2033

Automotive LED Lighting Market by Application (Front, Rear, Side, Interior), Technology (Halogen, Xenon/HID, LED), Vehicle Type (Passenger Car, Light Commercial Vehicle, Heavy Commercial Vehicle), Sales Channel (OEM, Aftermarket), and Regional Analysis for 2026–2033

Automotive LED Lighting Market Size and Trend Analysis

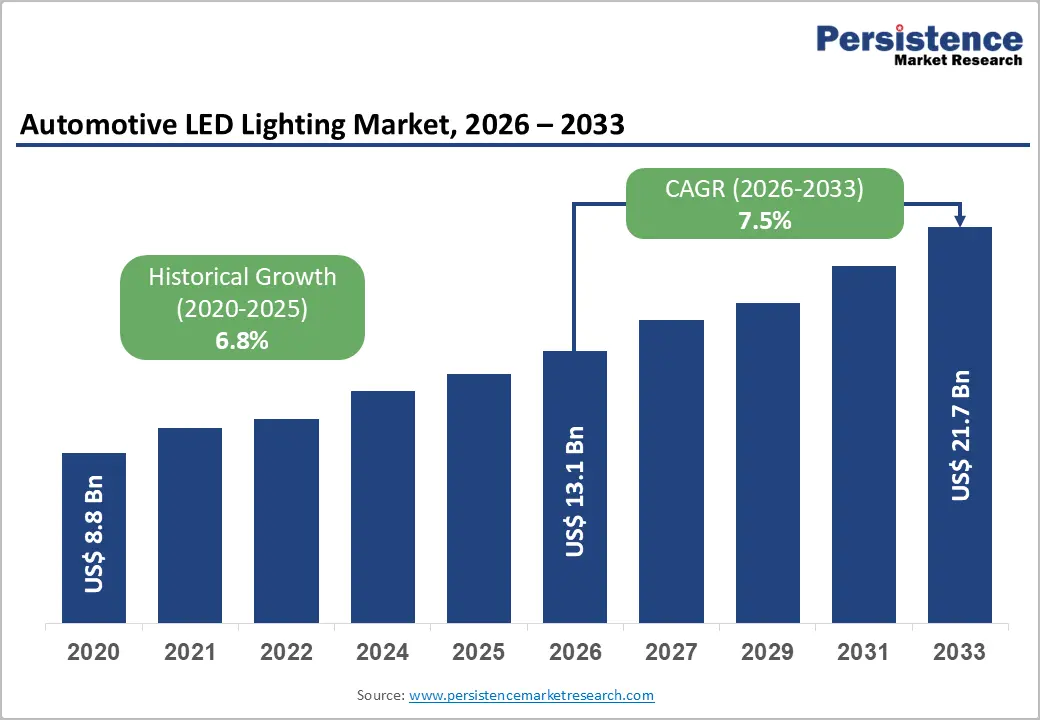

The global Automotive LED Lighting market size is valued at US$ 12.4 billion in 2026 and is projected to reach US$ 21.7 billion by 2033, growing at a CAGR of 7.5% between 2026 and 2033. Stringent global vehicle safety regulations mandating advanced lighting systems, combined with the accelerating shift toward electric vehicles, where energy-efficient LED technology reduces battery load. Regulatory mandates such as UN ECE Regulation No. 48 and FMVSS 108 require increasingly sophisticated adaptive lighting, compelling OEMs to integrate LED solutions across all vehicle segments.

Key Industry Highlights:

- Leading Region – Asia Pacific dominates the global automotive LED lighting market, driven by China's massive NEV production surge, high-volume vehicle manufacturing in Japan and South Korea, and rapidly tightening safety lighting regulations across India and Southeast Asia.

- Fast-Growing Market– North America holds a significant share of the global automotive LED lighting market, supported by a mature automotive industry, high per-capita vehicle ownership, and proactive safety regulation enforcement.

- Dominant Technology Segment – LED technology commands the largest technology segment share, supported by its superior energy efficiency, longer operational lifespan exceeding 25,000 hours, and near-universal adoption by EV OEMs as the default lighting architecture globally.

- Fast-Growing Application Segment – Matrix and adaptive driving beam LED systems are the fastest-growing application sub-segment, mandated by EU GSR II from 2024 and rapidly migrating from luxury to mid-range vehicle segments across Europe and North America.

- Key Opportunity – The aging global vehicle fleet averaging 12+ years in the U.S. and SEMA's US$ 50 Bn North American aftermarket underscores a vast LED retrofit opportunity, amplified by plug-and-play kit innovations lowering installation complexity for consumers.

DRO Analysis

Drivers - Stringent Vehicle Safety Regulations Driving LED Adoption

Government-mandated lighting standards are a primary accelerant for the automotive LED lighting market. The United Nations Economic Commission for Europe (UNECE) Regulation No. 48 and its amendments allows the automakers to integrate adaptive front-lighting systems (AFS) and daytime running lights (DRL) across vehicle categories. In the European Union, DRLs have been mandatory for all new passenger cars since 2011 and for light commercial vehicles since 2012.

The U.S. National Highway Traffic Safety Administration (NHTSA) reports that advanced headlighting systems reduce nighttime pedestrian fatalities by up to 26%. As safety mandates expand into emerging economies with India's AIS-008 regulation and China's GB 4785 standard both undergoing stricter revisions automakers are standardizing LED technology across their global platforms to ensure regulatory compliance and reduce development complexity.

Rapid Electrification of the Automotive Sector

The global transition toward electric vehicles (EVs) is creating a powerful structural tailwind for LED lighting adoption. According to the International Energy Agency (IEA), global EV sales reached 17 million units in 2024, representing 20% of total new car sales globally. LED lighting consumes up to 75% less energy compared to halogen equivalents, a critical advantage for EV range optimization.

Major EV manufacturers including Tesla, BYD, and Volkswagen Group have standardized full-LED lighting across their entire EV portfolios. The Society of Automotive Engineers (SAE) has also published technical benchmarks correlating energy-efficient lighting with extended driving range, reinforcing OEM procurement decisions. As EV penetration accelerates, the baseline demand for LED lighting systems is poised to expand commensurately.

Restraints - High Initial Cost of LED Systems Relative to Halogen Alternatives

Despite their long-term cost efficiency, LED automotive lighting systems carry substantially higher upfront costs, creating adoption resistance particularly in price-sensitive emerging markets. A complete LED headlamp assembly typically costs 3 to 5 times more than a comparable halogen unit.

According to the International Council on Clean Transportation (ICCT), in markets such as India, Indonesia, and Brazil, the average vehicle transaction price remains a significant barrier to premium feature uptake. This cost disparity limits LED penetration in the entry-level and mid-range vehicle segments, which collectively account for over 55% of global vehicle sales, constraining overall market volume growth in the near term.

Thermal Management Challenges and Complex Integration Requirements

LED systems generate concentrated heat at the junction, requiring sophisticated thermal management architectures heat sinks, thermal interface materials, and active cooling that add weight and engineering complexity. The Institute of Electrical and Electronics Engineers (IEEE) have documented that improper thermal dissipation can reduce LED luminous efficacy by up to 30% and shorten operational lifespan significantly.

Integrating these systems into compact modern vehicle designs, particularly in front fascias shared with sensor arrays for ADAS, presents compounding engineering challenges. Smaller suppliers and Tier-2 manufacturers without advanced thermal simulation capabilities face barriers to entry, limiting competitive diversity and creating supply concentration risks within the value chain.

Opportunities - Expansion of Matrix and Adaptive LED Headlamp Systems in Premium Vehicles

The proliferation of matrix LED and adaptive driving beam (ADB) technologies represents a high-value growth frontier. These systems use individually controllable LED segments to precisely shape the light beam, eliminating glare for oncoming traffic without switching to low beam improving nighttime visibility by up to 50% compared to static LED headlamps, per the Insurance Institute for Highway Safety (IIHS).

The European Commission's General Safety Regulation (EU) 2019/2144, effective from July 2024, mandates advanced lighting systems including ADB for all new vehicle types in the EU. BMW's Iconic Glow grille illumination and Mercedes-Benz's Digital Light system projecting road markings at 84 LED chips per headlamp illustrate the premium technology trajectory. As these features migrate from luxury to mid-range segments, the addressable market for high-value LED assemblies is set to expand substantially.

Rising Demand for LED Lighting in the Aftermarket Segment

The automotive aftermarket presents a compelling growth avenue as vehicle owners seek to retrofit and upgrade legacy lighting systems. The Specialty Equipment Market Association (SEMA) estimates the North American automotive aftermarket at over US$ 50 billion, with lighting upgrades among the top five most popular modification categories.

The global average vehicle age reached 12.2 years in 2023 (S&P Global Mobility), ensuring a large installed base eligible for LED retrofitting. Growing consumer awareness of LED benefits longer lifespan exceeding 25,000 hours, lower energy consumption, and superior luminous output is driving upgrade adoption. Additionally, the emergence of plug-and-play LED conversion kits compatible with existing vehicle harnesses, combined with expanding e-commerce distribution channels, is lowering barriers to aftermarket LED adoption across both developed and developing markets.

Category-wise Analysis

Application Insights

Among all application segments, the front lighting segment holds the dominant position, accounting for approximately 45% of the global Automotive LED Lighting market in 2026. This leadership is driven by front headlamp systems being the first and most regulated lighting assembly on any vehicle, where LED adoption is both mandated and commercially prioritized. According to the UNECE and NHTSA, front lighting directly influences collision avoidance and pedestrian safety outcomes, prompting OEMs to invest disproportionately in front-end LED technology.

The rising deployment of adaptive front-lighting systems (AFS) and matrix LED headlamps in C-segment and above vehicles further consolidates front lighting's market share dominance. Consumer expectations for premium aesthetic styling at the front fascia additionally reinforce LED penetration in this application category across both OEM and aftermarket channels.

Technology Insights

The LED technology segment is unequivocally the leading and fastest-growing technology in the Automotive LED Lighting market, commanding a share of approximately 62% in 2026, and steadily displacing both Halogen and Xenon/HID alternatives. The U.S. Department of Energy (DOE) reports LED automotive lamps deliver luminous efficacy of up to 150 lumens per watt, compared to 25 lm/W for halogen and 90 lm/W for HID systems.

LED's extended operational life of over 25,000 hours versus 1,000 hours for halogen reduces lifecycle ownership costs significantly. Phased-out regulations in the EU on halogen lamp production (with several member states encouraging transition plans) are further accelerating LED adoption. Ongoing semiconductor advancements, including micro-LED and chip-on-board (COB) LED architectures, continue to push performance boundaries while reducing unit costs.

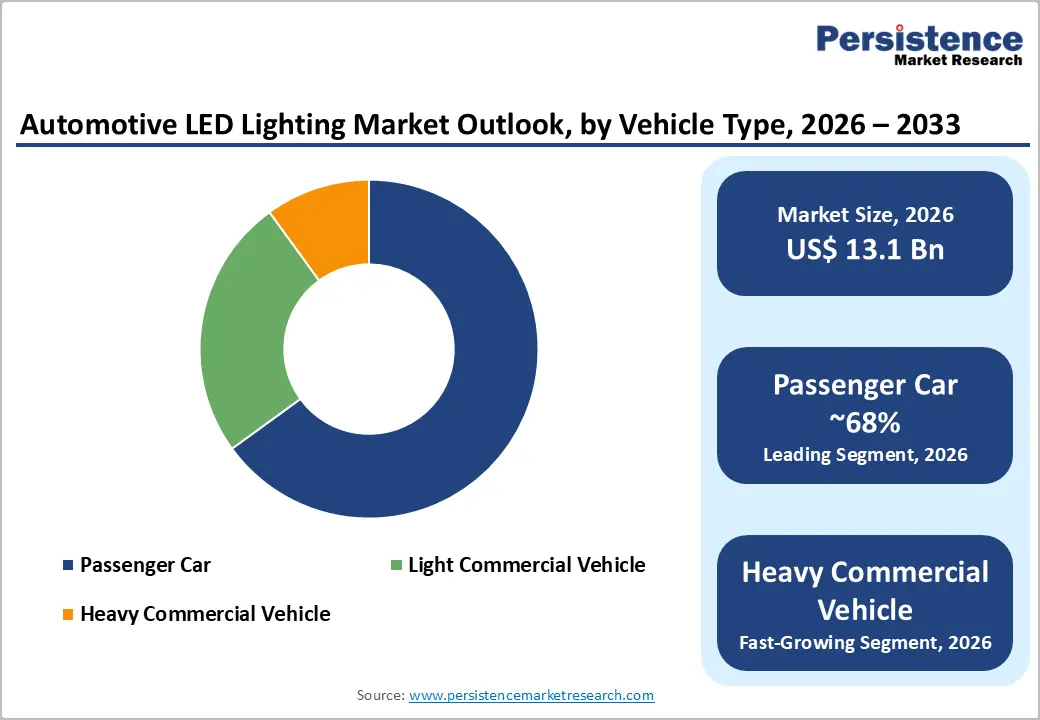

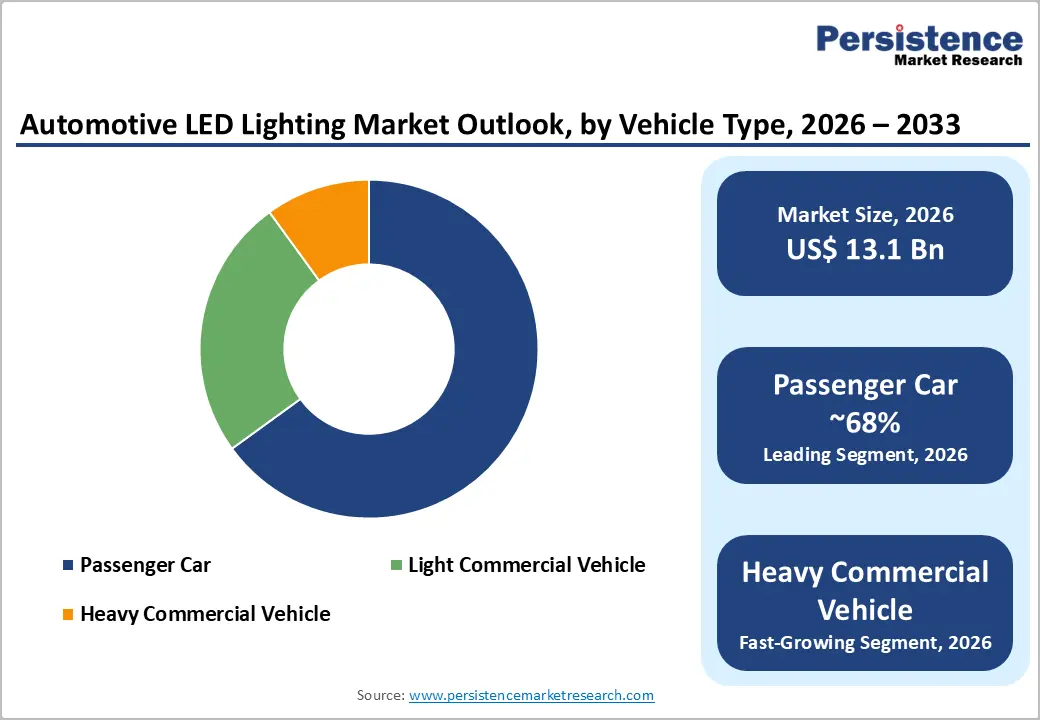

Vehicle Type Insights

The passenger car dominates the vehicle type category, representing approximately 68% of the global Automotive LED Lighting market in 2026. This dominance is underpinned by the sheer scale of global passenger car production the International Organization of Motor Vehicle Manufacturers (OICA) reported global passenger car production at approximately 67 million units in 2023and the accelerating shift toward premium and electric passenger vehicles where LED is the de facto standard.

The growing penetration of LED in B-segment and C-segment passenger cars, driven by competitive OEM pricing strategies and consumer demand for advanced styling, is continuously expanding the addressable volume. Meanwhile, the electrification wavered by China, Europe, and North America reinforces LED dominance within this vehicle category as EV architecture inherently Favors energy-efficient lighting.

Sales Channel Insights

The OEM (Original Equipment Manufacturer) channel leads the Sales Channel category, capturing approximately 72% of the Automotive LED Lighting market in 2026. OEM dominance reflects the fundamental integration of LED lighting into vehicle design from the manufacturing stage, where automakers specify LED systems as standard or optional equipment through long-term supply contracts with Tier-1 lighting suppliers.

The Automotive Industry Action Group (AIAG) notes that OEM supply agreements typically span 4 to 7 years aligned with vehicle platform lifecycles, providing sustained volume predictability. The global rollout of LED-standard platforms by Stellantis, Toyota, Hyundai-Kia Group, and Volkswagen Group is structurally reinforcing OEM channel primacy. The aftermarket channel, while smaller, is growing faster and remains a critical revenue diversification avenue for lighting manufacturers.

Regional Analysis

North America Automotive LED Lighting Market Trends & Analysis

North America holds a significant share of the global Automotive LED Lighting market, supported by a mature automotive industry, high per-capita vehicle ownership, and proactive safety regulation enforcement. The U.S. NHTSA's Federal Motor Vehicle Safety Standard (FMVSS) 108 and the Insurance Institute for Highway Safety (IIHS) headlight evaluation program which rates headlamp performance across a fleet of new vehicles have been instrumental in pushing automakers toward LED and adaptive lighting adoption.

U.S. Automotive LED Lighting Market

The United States is estimated to account for over 85% of the North American market, driven by its large vehicle parc exceeding 280 million registered vehicles and a rapidly growing EV market led by Tesla, General Motors, and Ford. The aftermarket opportunity is particularly large given the aging U.S. vehicle fleet.

Europe Automotive LED Lighting Market Trends, Drivers, & Insights

Europe is the most advanced regional market for automotive LED lighting, characterized by stringent regulatory mandates and a high concentration of premium vehicle manufacturers. The European Union's General Safety Regulation (GSR II) effective from July 2024 mandates intelligent speed assistance, advanced emergency braking, and enhanced lighting systems including ADB as standard in all new vehicles. Euro NCAP assessment protocols award safety points for advanced lighting performance, incentivizing OEM investment.

Germany Automotive LED Lighting Market Trends

Germany, home to BMW, Mercedes-Benz, Audi, and Volkswagen, is the largest European market. The country accounts for roughly 22% of European automotive LED demand, underpinned by high-value vehicle production and leading-edge lighting R&D investment.

U.K. Automotive LED Lighting Market Trends

The U.K. market benefits from the ZEV Mandate requiring 22% of automaker sales to be zero-emission vehicles by 2024, rising to 100% by 2035, driving accelerated LED adoption aligned with EV platform development.

France Automotive LED Lighting Market Trends

France, led by Stellantis and Renault Group, is investing heavily in LED integration across entry-level EV platforms such as the Renault 5 E-Tech and Citroën ë-C3, democratizing LED lighting access to the mass market.

Asia Pacific Automotive LED Lighting Market Trends

Asia Pacific is both the largest and fastest-growing regional market for Automotive LED Lighting, driven by the world's highest vehicle production volumes, rapid EV adoption particularly in China and evolving safety regulations across the region. The OICA attributes over 55% of global vehicle production to the Asia Pacific region. China's NEV (New Energy Vehicle) Policy supported by substantial government subsidies and a nationwide charging infrastructure rollout, has made China the world's largest EV market.

China Automotive LED Lighting Market Insights

China dominates Asia Pacific LED lighting demand, accounting for an estimated 48% of regional market revenue in 2026. BYD, NIO, Li Auto, and SAIC are deploying full-LED and matrix LED systems as standard across their NEV fleets, creating massive volume demand for domestic and international Tier-1 lighting suppliers.

India Automotive LED Lighting Market

India is the fastest-growing country market for automotive LED lighting in Asia Pacific, supported by rising income levels, increasing passenger car penetration, and the Automotive Industry Standards (AIS) regulatory upgrade trajectory. The government's FAME II (Faster Adoption and Manufacturing of Electric Vehicles) scheme is accelerating EV adoption, expanding the LED lighting addressable market.

Japan Automotive LED Lighting Market Trends

Japan remains a technology leader in automotive lighting innovation, home to Koito Manufacturing, Stanley Electric, and Ichikoh Industries. Japanese OEMs Toyota, Honda, Mazdaare integrating advanced LED and laser lighting systems globally from their domestic R&D centres, sustaining Japan's role as a premium LED lighting innovation hub.

Competitive Landscape

The global automotive LED lighting market exhibits a moderately consolidated competitive structure, with a handful of large Tier-1 automotive lighting suppliers including Koito Manufacturing, Valeo, Marelli, Hella (FORVIA), and Stanley Electric commanding significant combined market share through long-term OEM supply agreements and vertically integrated manufacturing.

Key competitive differentiators include proprietary LED module design, advanced thermal management IP, software-defined adaptive beam control, and global manufacturing footprint enabling regional supply chain resilience. Strategic M&A activity is intensifying, as incumbents acquire semiconductor and software capabilities to address the growing demand for digitally integrated lighting systems.

Key Developments:

- In June 2025, Car Mate launched the GIGA LED position bulb S400T and C4500 headlight series, featuring a stealth design and enhanced aluminum heat sinks.

- In May 2025, Car Mate unveiled EC-exclusive E8 and D9 LED headlight ranges offering up to 9,000-lumen output for halogen and HID replacements.

Companies Covered in Automotive LED Lighting Market

- UFI Filters

- Koito Manufacturing Co., Ltd.

- Valeo SE

- FORVIA HELLA

- Stanley Electric Co., Ltd.

- Marelli Holdings Co., Ltd.

- Osram Automotive (ams-OSRAM)

- Lumileds Holding B.V.

- Nichia Corporation

- Gentex Corporation

- Ichikoh Industries, Ltd.

- ZKW Group (LG Electronics)

Frequently Asked Questions

The global LED Chips market is projected to reach a value of US$ 36.8 billion in 2026 and is expected to grow to US$ 63.9 billion by 2033, expanding at a CAGR of 8.2% during the forecast period.

Key demand drivers include stringent energy-efficiency mandates such as the EU Ecodesign Directive, accelerating Mini-LED and Micro-LED adoption in premium displays by Apple Inc. and Samsung Electronics, and rising automotive matrix headlamp deployment under NHTSA FMVSS No. 108.

Asia Pacific leads the global LED Chips market with a commanding 58% revenue share in 2025, supported by China's dominant chip manufacturing ecosystem, Taiwan's display fabrication strength, and rapidly expanding electronics production capacity across India and Southeast Asia.

Automotive lighting electrification, adaptive driving beam systems, and specialty horticulture and UV-C disinfection LED chips represent the most significant opportunities, supported by 17 million annual electric vehicle sales and rapid vertical farming expansion globally.

Key market players include Nichia Corporation, OSRAM Licht AG (ams OSRAM), Cree LED, Seoul Semiconductor, Samsung Electronics, LG Innotek, Epistar Corporation, Sanan Optoelectronics, HC SemiTek, and Lumileds Holding B.V., among others.