- Automotive Components & Materials

- Automotive Brake System Market

Automotive Brake System Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Brake System Market by Brake Type (Disc Brakes, Drum Brakes), Vehicle Type (Passenger Vehicle [Compact Car, Midsize, SUVs, Luxury], Light Commercial Vehicle, Heavy Commercial Vehicle, Electric Vehicle), Technology (Anti-lock Braking System), Electronic Stability Control, Traction Control System, Electronic Brake-force Distribution ), and Regional Analysis, 2026 - 2033

Automotive Brake System Market Size and Trend Analysis

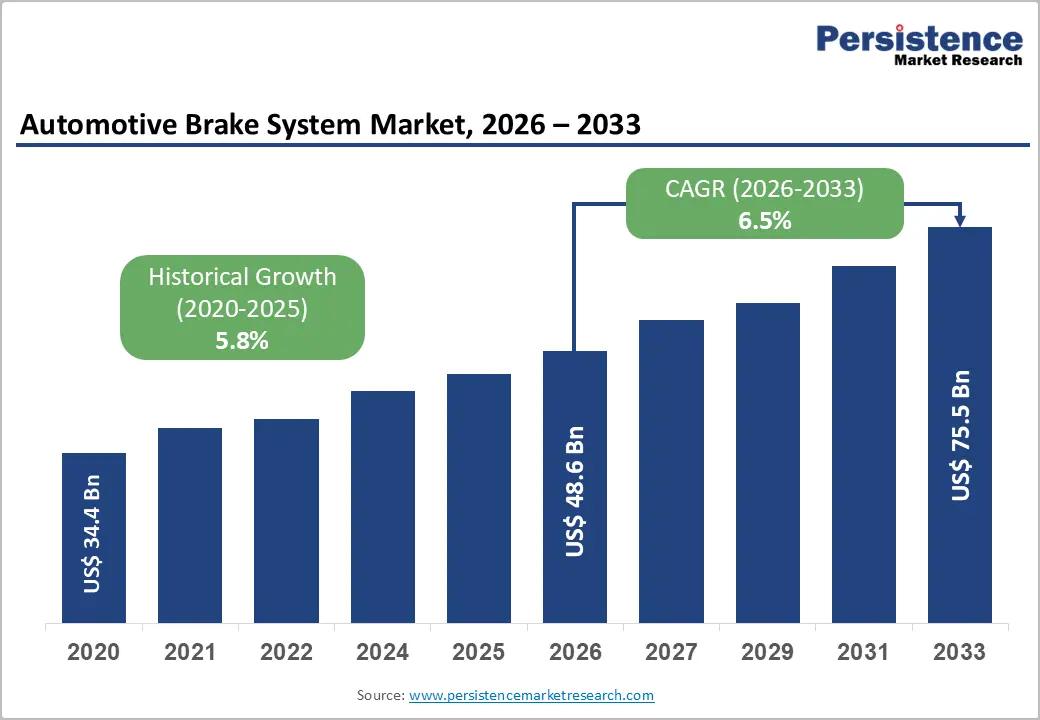

The global automotive brake system market size is expected to be valued at US$ 48.6 billion in 2026 and projected to reach US$ 75.5 billion by 2033, growing at a CAGR of 6.5% between 2026 and 2033. The market is on a firm upward trajectory, primarily propelled by record vehicle production volumes, tightening safety regulations, and accelerated electrification across major automotive economies. According to the International Organization of Motor Vehicle Manufacturers (OICA), global car manufacturing reached 75.5 million units in 2024, while car sales hit 74.6 million units, a 2.5% rise over 2023.

Key Industry Highlights:

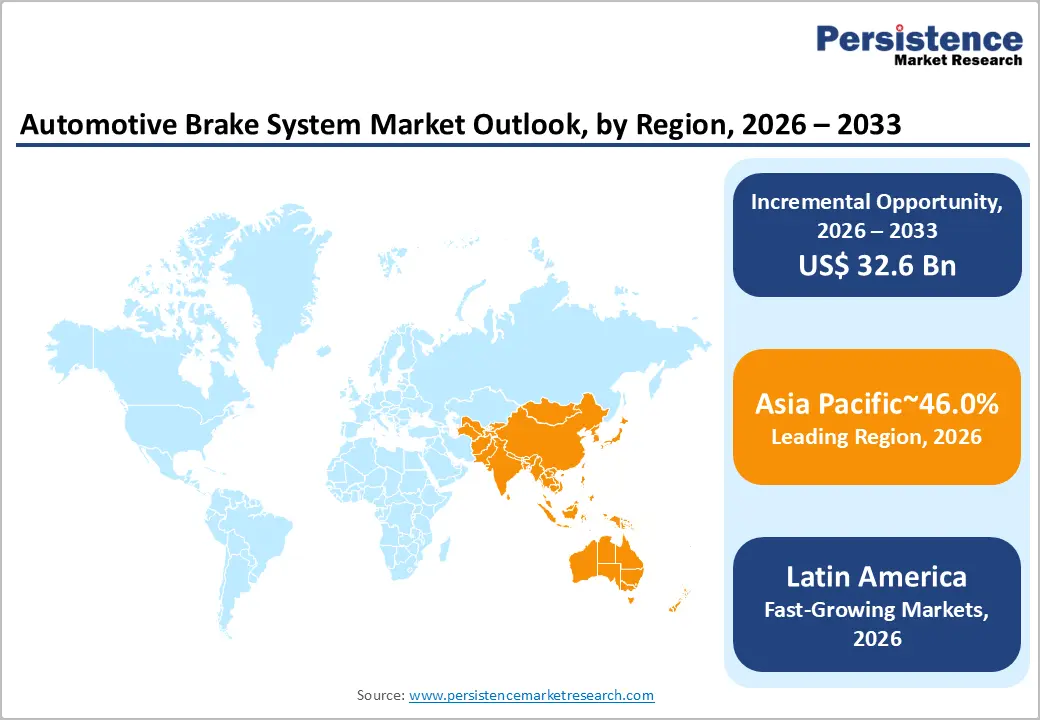

- Leading Region: Asia Pacific dominates with 46.0% market share in 2025, anchored by China's 23 million car sales and India's 4.8% production growth, supported by robust EV expansion and stringent mandatory ABS rollouts.

- Fast-Growing Market: Asia Pacific also leads in growth, propelled by India's Bharat NCAP mandate, China's NEV incentives extended through 2027, and Southeast Asia's ASEAN NCAP-driven safety upgrade cycle across passenger and commercial fleets.

- Dominant Brake Type: Disc Brakes dominate the brake-type category with approximately 70% market share in 2025, owing to superior heat dissipation, electronic-control compatibility, and near-universal adoption across passenger cars and electric vehicles globally.

- Fastest Growing Brake Type: Disc Brakes also represent the fastest-growing brake-type segment at 7% CAGR (2026-2033), driven by EV adoption, Euro 7 brake-particulate limits, and the brake-by-wire transition demanding precision-machined disc architectures.

- Opportunity: Brake-by-wire and low-particulate friction systems offer premium content exceeding US$ 1,200 per vehicle, unlocking high-margin growth as Level 3-4 autonomy, EV penetration, and Euro 7 compliance reshape global OEM sourcing strategies.

DRO Analysis

Drivers - Stringent Vehicle Safety Mandates Reshaping Braking Standards

Regulatory bodies worldwide have made advanced braking systems non-negotiable, fundamentally altering OEM procurement strategies. The European Union's General Safety Regulation (GSR) 2019/2144, fully effective from July 2024, mandates Advanced Emergency Braking Systems (AEBS), Intelligent Speed Assistance, and Electronic Stability Control on all new vehicles sold in the bloc.

The National Highway Traffic Safety Administration (NHTSA) finalized rule FMVSS No. 127 in April 2024, requiring automatic emergency braking on all U.S. light vehicles by September 2029. According to Euro NCAP, vehicles equipped with AEB show up to 38% reduction in rear-end collisions, validating the regulatory thrust and driving sustained replacement and upgrade demand across both OEM and aftermarket channels.

Electric Vehicle Adoption Catalyzing Brake System Reengineering

The shift toward electrified powertrains is reshaping brake architecture demand toward regenerative-compatible, brake-by-wire, and lightweight disc systems. The International Energy Agency (IEA) reported that global electric car sales surpassed 17 million units in 2024, representing more than 20% of total car sales, with China alone accounting for nearly 11 million of those.

EVs require sophisticated brake-blending controls, low-drag calipers, and dust-reducing rotors to address particulate emissions under the Euro 7 standard finalized in March 2024, which for the first time regulates brake-particle emissions at 3 mg/km for ICE/HEV passenger cars. This regulatory and technological convergence is generating substantial new revenue streams for Continental AG, Brembo S.p.A., and ZF Friedrichshafen AG.

Restraints - Volatility in Raw Material and Friction Material Costs

Brake systems rely heavily on cast iron, steel, copper, and friction composites, all of which have experienced sustained price volatility. According to the World Bank Commodity Markets Outlook (April 2025), iron ore prices fluctuated within a 22% band during 2024, while copper averaged US$ 9,150 per metric ton, near multi-year highs.

Compounding this, U.S. Environmental Protection Agency restrictions and California's SB 346 mandate copper content below 0.5% in friction materials by 2025, forcing costly reformulation. Smaller Tier-2 suppliers face margin compression, delayed product validation cycles, and capital-intensive material substitution, slowing capacity additions across the brake friction segment.

Counterfeit Aftermarket Components Undermining Brand Integrity

The proliferation of counterfeit brake pads, rotors, and hydraulic components in the aftermarket continues to erode consumer trust and OEM revenues. The European Union Intellectual Property Office (EUIPO) estimated counterfeit auto parts cost the legitimate industry approximately EUR 2.2 billion annually, with brake components ranking among the top three most-counterfeited categories.

Inferior friction materials can extend stopping distances by up to 25%, according to testing by TUV Rheinland, posing serious safety risks. This black-market activity dilutes pricing discipline, diverts replacement-cycle revenue from authorized channels, and forces legitimate suppliers to invest heavily in anti-counterfeit packaging, blockchain tracking, and customs enforcement.

Opportunities - Brake-by-Wire Systems Unlocking Premium Value Pockets

The transition from hydraulic to electromechanical brake-by-wire (EMB) architectures represents a high-margin frontier, particularly for premium EVs and autonomous-ready platforms. Brembo S.p.A. launched its Sensify intelligent braking platform in 2024, integrating software-driven, wheel-independent control, while Continental AG announced volume production of its Future Brake System (FBS) dry brake-by-wire from 2026 with a confirmed Asian OEM.

According to the United Nations Economic Commission for Europe (UNECE) WP.29 framework, Level 3 and 4 autonomous vehicles require redundant electronic braking, making EMB virtually mandatory. With EV passenger vehicle production projected to exceed 30 million units annually by 2030, suppliers establishing early intellectual property and validation footprints in brake-by-wire stand to capture premium content per vehicle exceeding US$ 1,200, more than double conventional hydraulic systems.

Particulate-Reducing and Regenerative Brake Innovations Gaining Traction

The introduction of Euro 7 brake-particulate limits and the U.S. EPA's ongoing review of non-exhaust emissions have created a strategic opening for low-dust, ceramic-coated, and tungsten-carbide rotor technologies. Bosch Mobility unveiled its iDisc coated rotor in collaboration with Buderus Guss, which the company claims reduces brake dust by up to 90%.

Regenerative braking integration in EVs and hybrids reduces friction-brake wear by 40-60%, according to data from the U.S. Department of Energy's Argonne National Laboratory. With more than 45 countries having announced ICE phase-out targets, suppliers offering integrated regenerative-plus-low-emission friction packages are positioned to capture significant share, particularly in Europe and China, where regulatory pressure is most acute.

Category-wise Analysis

Brake Type Insights

Disc Brakes dominate the global automotive brake system market, commanding approximately 70% market share in 2025 and projected to expand at a 7% CAGR through 2033. Their leadership is underpinned by superior heat dissipation, consistent stopping power under repeated use, and compatibility with electronic control modules essential for ABS, ESC, and brake-by-wire integration.

According to vehicle homologation data from the European Automobile Manufacturers' Association (ACEA), virtually 100% of new passenger cars sold in the EU in 2024 were equipped with disc brakes on at least the front axle, with four-wheel disc adoption exceeding 85%. The proliferation of larger SUVs, performance-oriented EVs, and stricter braking-distance norms under UNECE R13-H continues to displace drum technology even in budget segments across emerging markets.

Vehicle Type Insights

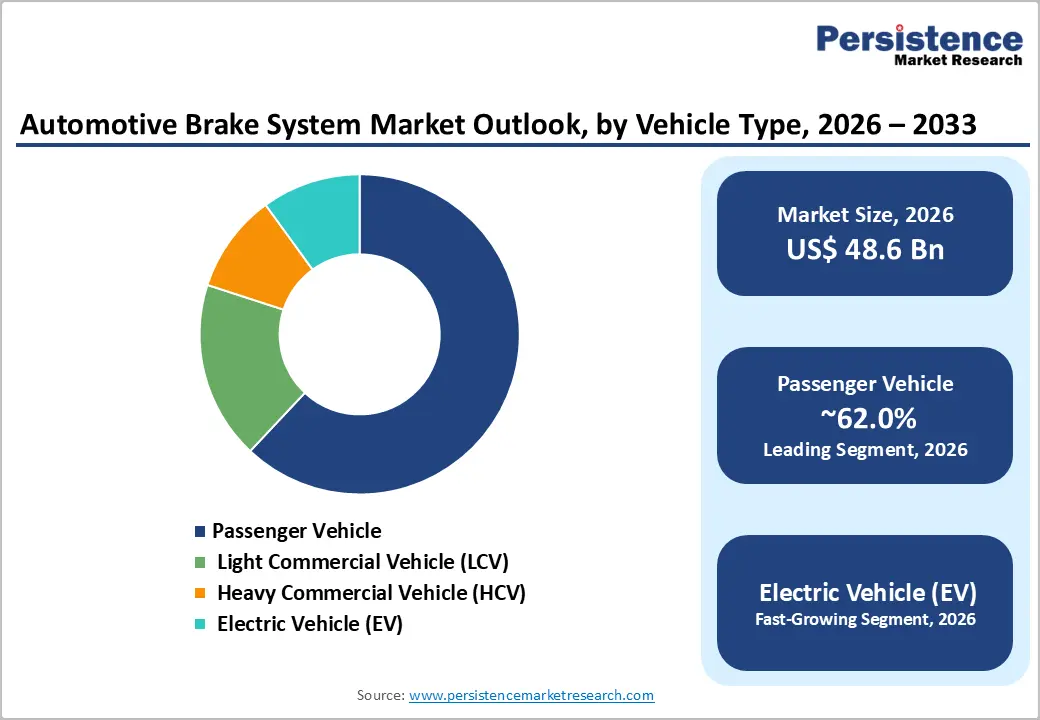

Passenger Vehicles lead the vehicle-type segment, holding an estimated 62% market share in 2025, supported by sheer volume and rising content per vehicle. OICA data shows passenger car production reached approximately 68 million units globally in 2024, with SUVs alone representing more than 48% of new passenger vehicle sales according to the IEA Global EV Outlook 2025. SUVs and luxury segments command higher-value brake systems with larger rotors, multi-piston calipers, and advanced electronics, lifting average selling prices

Electric passenger vehicles are emerging as the fastest-growing sub-segment, with the IEA confirming 17 million-plus EV sales in 2024, each requiring sophisticated regenerative-friendly brake architectures, blended control units, and lower-dust friction materials to comply with Euro 7 particulate norms.

Technology Insights

Anti-lock Braking System (ABS) remains the dominant technology segment, accounting for nearly 55% market share in 2025, owing to universal regulatory mandates across virtually all major automotive markets. Under UNECE Regulation 13/13-H, U.S. FMVSS 126, India's AIS-150, and China's GB 21670, ABS is compulsory on essentially all new four-wheelers and most two-wheelers above 125cc.

The Insurance Institute for Highway Safety (IIHS) has documented that ABS-equipped vehicles experience 35% fewer fatal run-off-road crashes on wet roads. Beyond standalone ABS, the technology forms the foundational hardware on which ESC, TCS, and EBD are layered, ensuring its dominance even as more advanced electronic stability and brake-by-wire systems gain traction across premium and EV platforms.

Regional Insights

North America Automotive Brake System Market Trends and Insights

North America holds a share of 21.0% in 2025, supported by mature replacement cycles, stringent NHTSA safety mandates, and robust SUV and pickup truck demand. The region benefits from the April 2024 finalization of FMVSS No. 127, which mandates automatic emergency braking on all light vehicles by 2029, accelerating supplier R&D and aftermarket retrofit activity across the United States, Canada, and Mexico.

U.S. Automotive Brake System Market Size

The U.S. automotive brake system market is valued at US$ 7.9 billion in 2025, driven by 12.7 million new vehicle sales reported by the U.S. Bureau of Economic Analysis for 2024, a 3.1% rise year-on-year. Demand is anchored by light-truck and SUV dominance (over 80% of sales), the NHTSA AEB mandate, and a vehicle parc exceeding 283 million units per the Federal Highway Administration, sustaining strong aftermarket pad and rotor replacement.

Europe Automotive Brake System Market Trends and Insights

Europe holds a share of 25.0% in 2025, anchored by the EU General Safety Regulation 2019/2144, Euro 7 brake-particulate limits, and the world's most concentrated luxury vehicle production base. The ACEA reported 10.6 million new EU registrations in 2024, with battery-electric share reaching 13.6%, fueling demand for advanced regenerative and low-dust brake systems across Germany, France, Italy, and the Nordics.

Germany Automotive Brake System Market Size

Germany automotive brake system market is valued at US$ 3.2 billion in 2025, driven by its position as Europe's largest vehicle producer with 4.07 million units manufactured in 2024 per VDA data. The presence of premium OEMs, including BMW Group, Mercedes-Benz Group AG, Volkswagen AG, and Porsche AG, combined with global Tier-1 suppliers Continental AG and ZF Friedrichshafen AG, sustains exceptional content-per-vehicle and export-led demand.

France Automotive Brake System Market Size

France automotive brake system market is valued at US$ 1.3 billion in 2025, supported by domestic production from Stellantis N.V. and Renault Group, alongside the French Ecological Bonus that drove EV penetration to roughly 17% of new registrations in 2024, according to Plateforme Automobile (PFA). Investment in low-emission friction materials and brake-by-wire R&D anchored at the Saclay technology cluster reinforces market depth.

U.K. Automotive Brake System Market Size

The U.K. automotive brake system market is estimated at approximately US$ 1.1 billion in 2025, underpinned by 1.95 million new car registrations in 2024 per the Society of Motor Manufacturers and Traders (SMMT), a 2.6% rise.

Asia Pacific Automotive Brake System Market Trends and Insights

Asia Pacific held 46.0% share in 2025, making it the largest regional market, driven overwhelmingly by China's manufacturing scale and India's rapid motorization. The region produced nearly 46 million vehicles in 2024 per OICA, with China growing 5.2% and India growing 4.7% in production. Expanding middle-class vehicle ownership, mandatory ABS rollouts, and accelerating EV penetration are fundamentally reshaping demand patterns across the region.

China Automotive Brake System Market Size

The China automotive brake system market is valued at US$ 9.4 billion in 2025, anchored by 23 million car sales in 2024 representing 31% of global volume. Growth is driven by domestic NEV champions BYD Company Ltd. and Geely Holding Group, government tax incentives extended through 2027, and a 6.49 million km national road network supporting one of the world's largest vehicle parcs at roughly 440 million units.

India Automotive Brake System Market Size

India automotive brake system market is valued at US$ 3.6 billion in 2025, propelled by 4.8% growth in car sales in 2024 per SIAM and the Bharat NCAP safety rating program launched in October 2023, which incentivizes ABS, ESC, and EBD adoption. The PM GatiShakti infrastructure program and national highway expansion to 146,204 km are catalyzing commercial vehicle brake demand.

Japan Automotive Brake System Market Size

The Japan automotive brake system market is estimated at approximately US$ 2.7 billion in 2025, despite a 7% decline in car sales in 2024. Demand is sustained by globally exported production from Toyota Motor Corporation, Honda Motor Co., Ltd., and Nissan Motor Co., Ltd., alongside domestic Tier-1 leadership from Akebono Brake Industry Co., Ltd. and Advics Co., Ltd. in advanced brake calipers and regenerative systems.

Competitive Landscape

The global automotive brake system market is moderately consolidated, with the top five suppliers controlling an estimated 55-60% of global revenues. Tier-1 leaders including Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Brembo S.p.A., and Aisin Corporation compete on integrated electronic braking platforms, regenerative blending, and brake-by-wire IP.

Differentiation increasingly hinges on software-defined control units, low-dust friction formulations compliant with Euro 7, and OEM co-development partnerships for EV platforms. Emerging business models include subscription-based brake software updates, predictive maintenance via connected diagnostics, and joint ventures with Chinese NEV makers to localize content under regional sourcing mandates.

Key Developments:

- In Dec, 2025, ADVICS announced the adoption of its new Cooperative Regenerative Braking System in Toyota’s newly launched sixth-generation RAV4 SUV, marking a significant advancement in electrified automotive brake system technology. The system is integrated into Toyota’s hybrid platform, which combines electrification and intelligent vehicle control under a next-generation mobility architecture.

- In Jan 2025, ZF announced a major global business win in brake-by-wire and electro-mechanical braking systems for light vehicles, reinforcing its leadership in advanced automotive brake system technologies. Under a long-term agreement with a global OEM, ZF will equip nearly 5 million vehicles with its Electro-Mechanical Brake (EMB) technology, marking one of the largest commercial deployments of brake-by-wire systems in the industry.

Global Automotive Brake System Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 34.4 Billion |

|

Current Market Value (2026) |

US$ 48.6 Billion |

|

Projected Market Value (2033) |

US$ 75.5 Billion |

|

CAGR (2026-2033) |

6.5% |

|

Leading Region |

Asia Pacific, 46.0% |

|

Dominant Brake Type |

Disc Brakes, 70% share |

|

Top-ranking Vehicle Type |

Passenger Vehicle, 62% share |

|

Incremental Opportunity |

US$ 26.9 Billion (2026-2033) |

Companies Covered in Automotive Brake System Market

- Advics Co, Ltd.

- Akebono Brake Industry Co., Ltd.

- Zf Friedrichshafen Ag

- The Web Co

- Nissin Kogyo Co., Ltd Robert Bosch Gmbh

- Aisin Corporation

- Haldex

- Hitachi Astemo, Ltd.

- Brembo S.P.A

Frequently Asked Questions

The global automotive brake system market is valued at US$ 48.6 billion in 2026 and is projected to reach US$ 75.5 billion by 2033, expanding at a CAGR of 6.5% during the forecast period.

Stringent safety mandates such as the EU GSR 2019/2144, U.S. FMVSS No. 127, and rapid EV adoption surpassing 17 million units in 2024 per the IEA are the principal demand drivers globally.

Asia Pacific leads the global market with a 46.0% share in 2025, anchored by China's 23 million annual car sales, India's 4.8% production growth, and the region's expanding EV manufacturing footprint.

The transition to brake-by-wire systems and low-particulate friction materials compliant with Euro 7 norms offers premium content exceeding US$ 1,200 per vehicle, especially for EVs and Level 3-4 autonomous platforms.

Leading players include Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Brembo S.p.A., Aisin Corporation, Akebono Brake Industry Co., Ltd., Knorr-Bremse AG, Hyundai Mobis Co., Ltd., and Mando Corporation.