- Food Ingredients & Additives

- Commercial Food Dehydrators Market

Commercial Food Dehydrators Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Commercial Food Dehydrators Market by Source (Vertical Airflow, Horizontal Airflow), Application (Small-Scale, Medium-Scale, Large-Scale), Composition & Flavor (Fruits and Vegetable, Meats and Seafood, Herbs and Spices, Pet Food, Others), and Regional Analysis from 2026 - 2033

Commercial Food Dehydrators Market Share and Trends Analysis

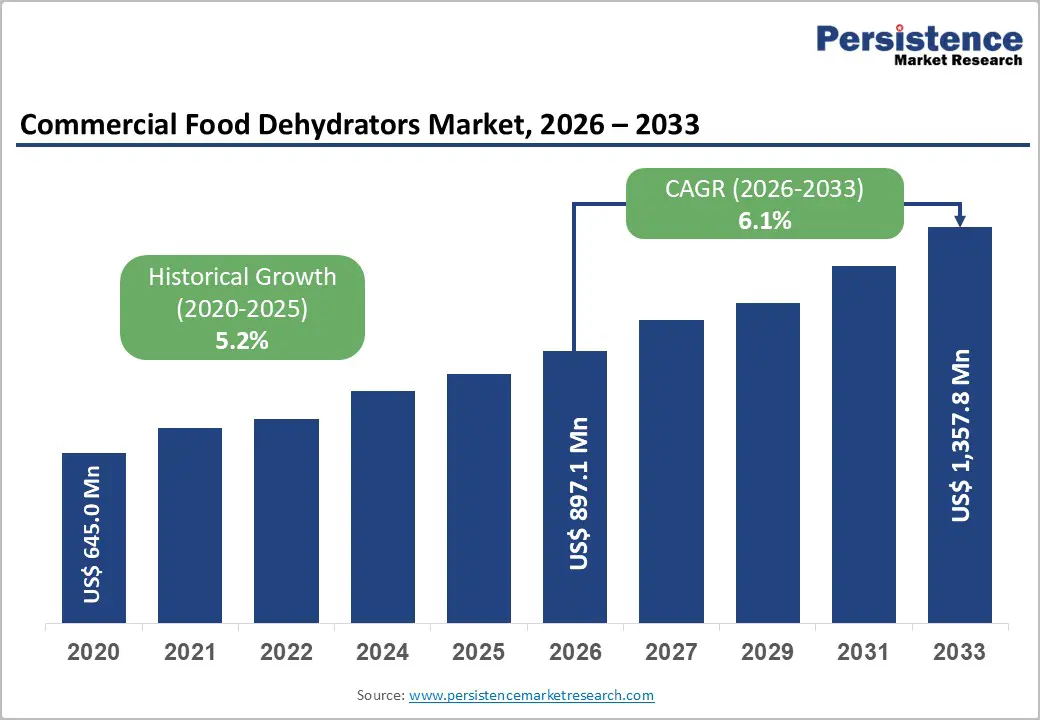

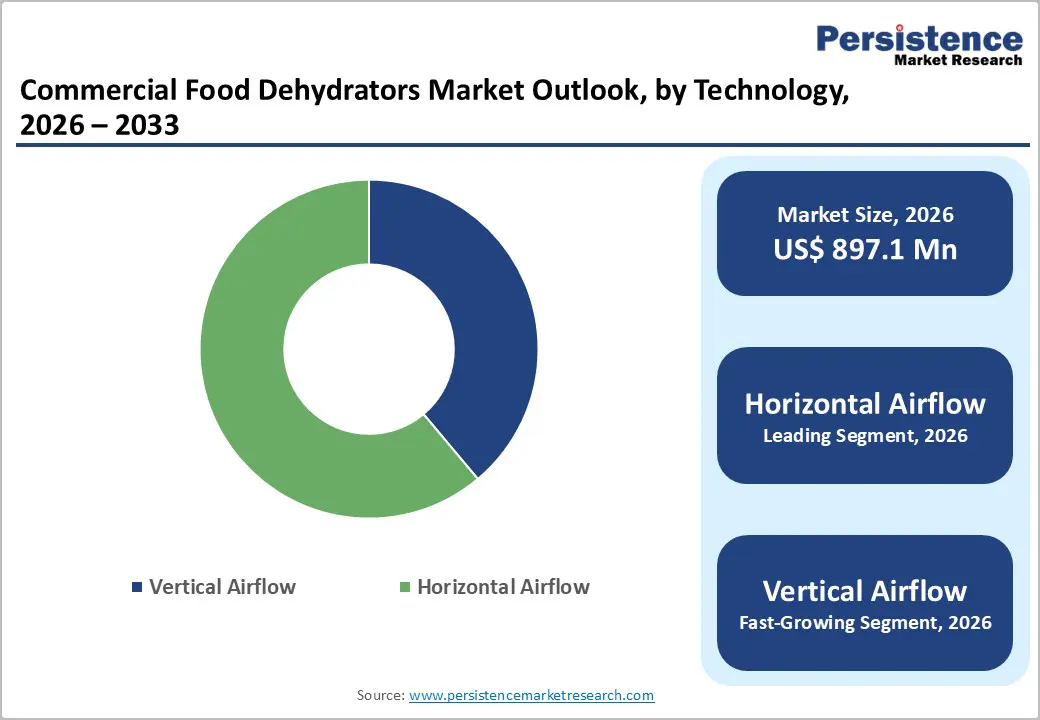

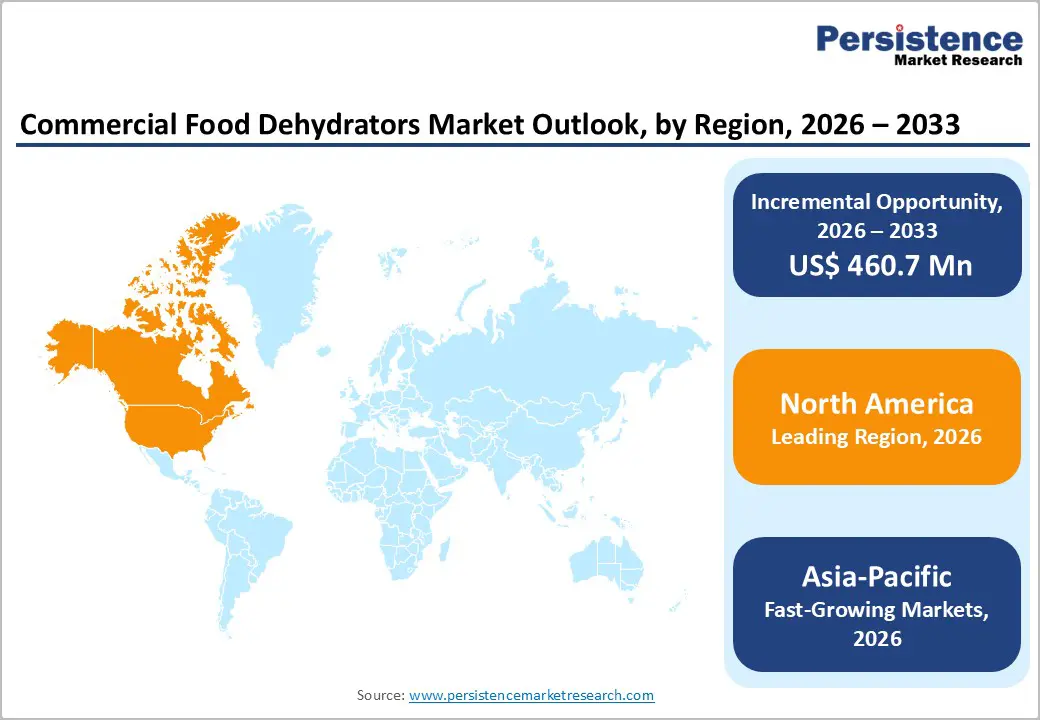

The global commercial food dehydrators market is estimated to grow from US$ 897.1 million in 2026 to US$ 1,357.8 million by 2033. The market is projected to record a CAGR of 6.1% during the forecast period from 2026 to 2033 and is expected to experience steady growth driven by rising demand for processed foods, longer shelf life, and reduced food waste.

North America leads due to advanced food processing infrastructure, while Asia-Pacific is the fastest-growing region. Europe shows stable growth, supported by clean-label trends and efficient food preservation technologies.

Key Industry Highlights

- Dominant Segment: Medium-scale dehydrators held the largest share in 2025 at 46.5%, driven by strong adoption among SMEs, food processors, and contract manufacturers requiring balanced capacity and cost efficiency.

- Dominant Region: North America led in 2025 with 34.0% share, supported by advanced food processing infrastructure, high demand for preserved foods, and widespread adoption of commercial drying technologies.

- Market Drivers: Growth is driven by increasing demand for extended shelf life, reduced food waste, rising consumption of processed foods, expansion of agro-processing industries, and a growing focus on clean-label and natural preservation methods.

- Market Opportunity: Opportunities exist in energy-efficient and solar dehydrators, expansion in Asia-Pacific, integration of smart/automated systems, rising demand for organic dried products, and increasing applications across nutraceutical, pet food, and functional food industries.

Market Dynamics

Driver: Rising Demand for Extended Shelf-Life Food Products

The demand for extended shelf-life food products is a major driver of the commercial food dehydrators market, as dehydration significantly reduces moisture content and inhibits microbial growth. Food typically contains 50-95% water, making it highly perishable; removing this moisture slows spoilage and enables long-term storage without chemical preservatives. Governments and global agencies emphasize preservation as a critical strategy for food security, especially with a rising global population and supply chain inefficiencies. Dehydrated foods such as fruits, vegetables, and meats are increasingly used in packaged foods, ready meals, and emergency food supplies due to their stability and reduced storage costs.

From a statistical standpoint, food loss and waste remain a global concern, strongly reinforcing the need for preservation technologies. According to the Food and Agriculture Organization and United Nations Environment Program, around 13.2% of food is lost post-harvest, and an additional 19% is wasted at retail and consumer levels. Extending shelf life directly reduces this loss. Studies show that increasing shelf life by even 20-40% can reduce food waste by 5-7%, alongside reductions in water and carbon footprints. This creates strong economic and environmental incentives for industries to adopt dehydration technologies.

Restraint: Energy-Intensive Operations Increasing Operating Costs

One of the most critical constraints in the commercial food dehydrators market is the high energy consumption associated with drying. Food dehydration relies on heat transfer and evaporation, which are inherently energy-intensive because of the thermodynamic requirement to remove water. Industrial drying processes account for approximately 12-25% of total industrial energy consumption in developed economies, making them among the most energy-intensive operations in food processing. Additionally, the typical thermal efficiency of drying systems remains relatively low (around 25-50%), meaning a large portion of energy input is lost during operation.

This high energy demand directly translates into elevated operating costs, particularly in regions with expensive electricity or fuel. Energy losses linked to food systems are already substantial—global food waste alone accounts for nearly 4 trillion megajoules of wasted energy annually, highlighting inefficiencies across the supply chain. Since most commercial dehydrators rely on conventional hot-air or fossil-fuel-based systems, operational expenditure becomes a major barrier for SMEs and emerging markets. As energy prices fluctuate globally, this constraint limits widespread adoption, especially for large-scale industrial dehydration systems.

Opportunity: Adoption of Energy-Efficient and Solar-Based Dehydration Systems

The shift toward energy-efficient and solar-based dehydration systems presents a strong opportunity in the commercial food dehydrators market. Solar dehydration eliminates dependence on grid electricity, offering near-zero operating costs while maintaining food quality. Innovations in solar-conduction drying and hybrid systems enable efficient moisture removal with minimal energy input, making them highly suitable for rural and agro-based economies. These systems also help preserve nutrients and improve product quality compared to traditional open-air drying, supporting demand for high-quality dried foods in both domestic and export markets.

From a data perspective, the opportunity is reinforced by global food waste and energy challenges. The United Nations Environment Program estimates that 931 million tonnes of food are wasted annually, much of which could be preserved through technologies such as dehydration. Additionally, around 40% of food losses in developing countries occur during post-harvest and processing stages, where solar dehydration can play a crucial role. By combining sustainability with cost efficiency, energy-efficient dehydrators are gaining traction, particularly in Asia-Pacific and Africa, where energy access and food preservation remain critical challenges.

Category-wise Analysis

By Technology, Horizontal Airflow Dominates the Commercial Food Dehydrators Market

Horizontal airflow systems dominate the commercial food dehydrators market with 61.1% share in 2025, due to their ability to provide uniform heat distribution and consistent drying across multiple trays. This ensures better product quality, reduced contamination risk, and shorter drying cycles, making them highly suitable for commercial food processing. Their efficiency is critical since industrial drying processes consume approximately 12-25% of total industrial energy use, according to energy studies, making optimized airflow essential for cost control. Horizontal systems are therefore widely adopted in large-scale operations handling fruits, vegetables, and meat products.

The fastest-growing segment is advanced and hybrid drying technologies, including heat pump and solar-assisted systems. These technologies can reduce energy consumption by 30-50% while improving nutrient retention and operational efficiency. With increasing regulatory and sustainability pressures, industries are rapidly shifting toward energy-efficient, automated dehydration solutions.

By Capacity, Medium-Scale Dominates the Commercial Food Dehydrators Market

Medium-scale dehydrators dominate the market as they provide an ideal balance between processing capacity, investment cost, and operational flexibility. They are widely used by SMEs and agro-processing units, which form a significant portion of the global food industry. These systems are particularly important in reducing post-harvest losses, which account for a substantial share of global food inefficiencies. Medium-scale units enable efficient batch processing without the high capital and energy requirements of large industrial systems.

The fastest-growing segment is large-scale dehydrators, driven by increasing industrialization of food processing and demand for bulk production. Industrial drying already consumes around 12-25% of total industrial energy, reflecting the scale of operations. Large manufacturers are investing in automated, continuous drying systems to meet growing demand for packaged and export-quality food products, especially in the rapidly growing Asia Pacific.

Regional Insights

North America Commercial Food Dehydrators Market Trends

North America dominates the commercial food dehydrators market due to its highly developed food processing ecosystem and strong focus on minimizing food waste. The United States leads the region, supported by one of the world’s largest food supply chains, as highlighted by the United States Department of Agriculture. The U.S. processes large volumes of perishable food, where preservation technologies like dehydration are essential to extend shelf life and reduce losses. With increasing demand for packaged and shelf-stable foods, the U.S. market is expected to reach US$ 1,200 Mn, driven by automation and industrial-scale adoption.

Canada is the fastest-growing country, expected to grow at 6.5% CAGR, supported by investments in food processing and sustainability initiatives. Government-backed efforts to reduce food waste and improve supply chain efficiency are encouraging the adoption of energy-efficient dehydration systems across the agro-processing and food manufacturing sectors.

Europe Commercial Food Dehydrators Market Trends

Europe plays a critical role in the commercial food dehydrators market due to strict food safety regulations and strong sustainability goals. Germany leads the region with a well-established food processing industry and high adoption of efficient preservation technologies. According to the Food and Agriculture Organization, around 13.2% of food is lost post-harvest globally, reinforcing the importance of dehydration in reducing waste. Germany’s focus on industrial automation and energy-efficient systems supports its leadership, and the market is expected to reach US$ 700 Mn.

The United Kingdom is the fastest-growing country, expected to grow at 6.8% CAGR, driven by rising consumption of packaged and convenience foods. Sustainability policies and food waste reduction programs are accelerating the adoption of advanced dehydration technologies across the food processing and retail sectors.

Asia Pacific Commercial Food Dehydrators Market Trends

Asia-Pacific is the fastest-growing region in the commercial food dehydrators market, driven by rapid agro-processing expansion and high post-harvest losses. China leads the region, supported by its massive agricultural output and growing food processing sector. Data from the Food and Agriculture Organization indicates that a significant share of food losses occurs during post-harvest and processing stages, especially in developing economies. To address this, China is increasingly adopting dehydration technologies, and its market is expected to reach US$ 900 Mn.

India is the fastest-growing country, expected to grow at 7.5% CAGR, driven by government initiatives promoting food processing and infrastructure development. Rising demand for shelf-stable foods and efforts to reduce post-harvest losses are accelerating the adoption of commercial dehydration systems.

Competitive Landscape

The commercial food dehydrators market is moderately competitive, led by players such as Excalibur Dehydrator, LEM Products Holding LLC, Tribest Corporation, Harvest Right, and Hamilton Beach Brands, Inc.. Companies focus on energy-efficient technologies, automation, product durability, and expanding applications across food processing, nutraceutical, and agro-industrial sectors.

Key Industry Developments:

- In June 2024, Mitchell & Cooper announced the launch of new digital dehydrators under the Excalibur Performance range. The newly introduced models featured a glass top design, allowing users to monitor the drying process without opening the unit.

Commercial Food Dehydrators Market - Key Insights & Scope

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 645.0 Mn |

| Projected Market Value (2026) | US$ 897.1 Mn |

| Projected Market Value (2033) | US$ 1,357.8 Mn |

| CAGR (2026 - 2033) | 6.1% |

| Leading Region | North America, 34.0% share |

| Dominant Technology | Horizontal Airflow, 61.1% share |

| Top-ranking Capacity | Medium-Scale, 46.5% |

| Incremental Opportunity | US$ 460.7 Mn |

Companies Covered in Commercial Food Dehydrators Market

- Excalibur Dehydrator

- LEM Products Holding LLC

- Harvest Right

- Tribest Corporation

- Koolatron Corporation

- Hamilton Beach Brands, Inc.

- National Presto Industries, Inc.

- Aroma Housewares

- COSORI

- Magic Chef

- Presto

- Magic Mill

- Others

Frequently Asked Questions

The global commercial food dehydrators market is projected to be valued at US$ 897.1 Mn in 2026.

Rising demand for shelf-life extension, food waste reduction, processed foods, and efficient preservation technologies drives growth.

The global commercial food dehydrators market is poised to witness a CAGR of 6.1% between 2026 and 2033.

Energy-efficient technologies, solar dehydrators, Asia-Pacific expansion, automation, and growing demand for dried functional foods.

Excalibur Dehydrator, LEM Products Holding LLC, Harvest Right, Tribest Corporation, Koolatron Corporation, Hamilton Beach Brands, Inc.