- Processed Food

- Cloud Kitchen Market

Cloud Kitchen Market Size, Share, and Growth Forecast 2026 - 2033

Cloud Kitchen Market by Kitchen Type (Independent Cloud Kitchen, Commissary/Shared Kitchen, Kitchen Pods), Nature (Franchised, Standalone), End-user (Individual Consumers, Corporate Offices, Educational Institutions, Healthcare Facilities, Others), and Regional Analysis, 2026 - 2033

Cloud Kitchen Market Share and Trends Analysis

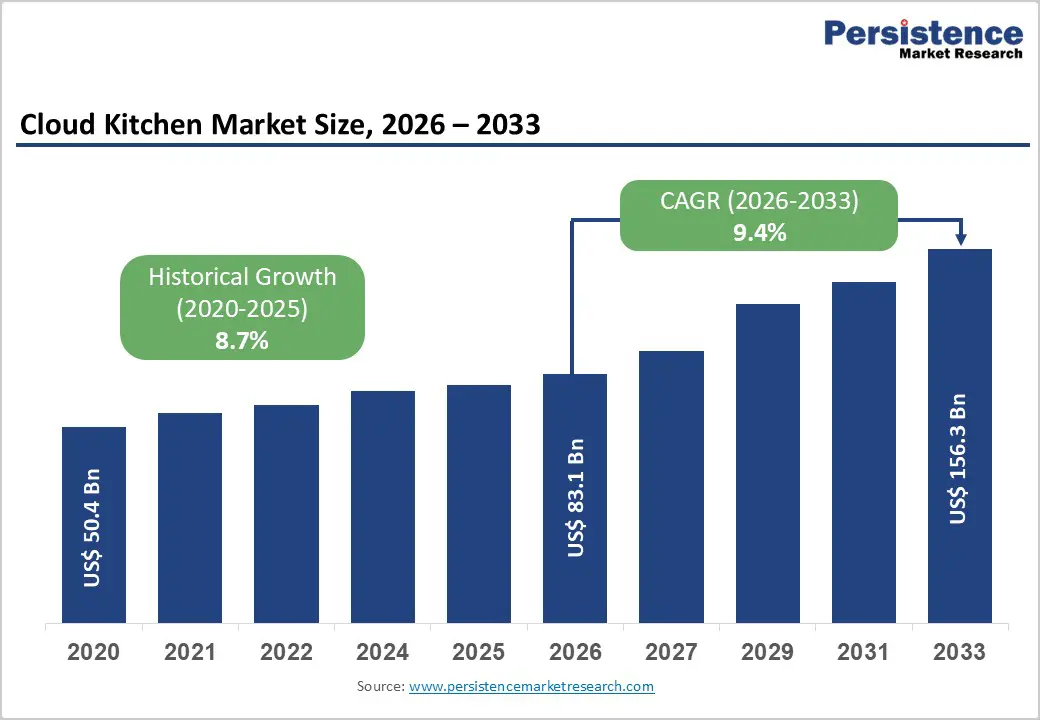

The global Cloud Kitchen market size is expected to be valued at US$ 83.1 billion in 2026 and projected to reach US$ 156.3 billion by 2033, growing at a CAGR of 9.4% between 2026 and 2033. The cloud kitchen market is rapidly expanding, driven by the rising demand for online food delivery, changing consumer lifestyles, and increasing smartphone penetration. These delivery-only kitchens operate without dine-in facilities, enabling lower operational costs, faster scalability, and efficient order management. Growth is supported by food aggregator platforms and advanced digital ordering systems that improve customer reach and delivery speed.

Urbanization, busy work schedules, and preference for convenience foods are key demand drivers. Operators are increasingly focusing on data-driven menu optimization, multiple brand kitchens, and centralized production hubs to maximize efficiency and profitability across competitive food service markets globally.

Key Industry Highlights

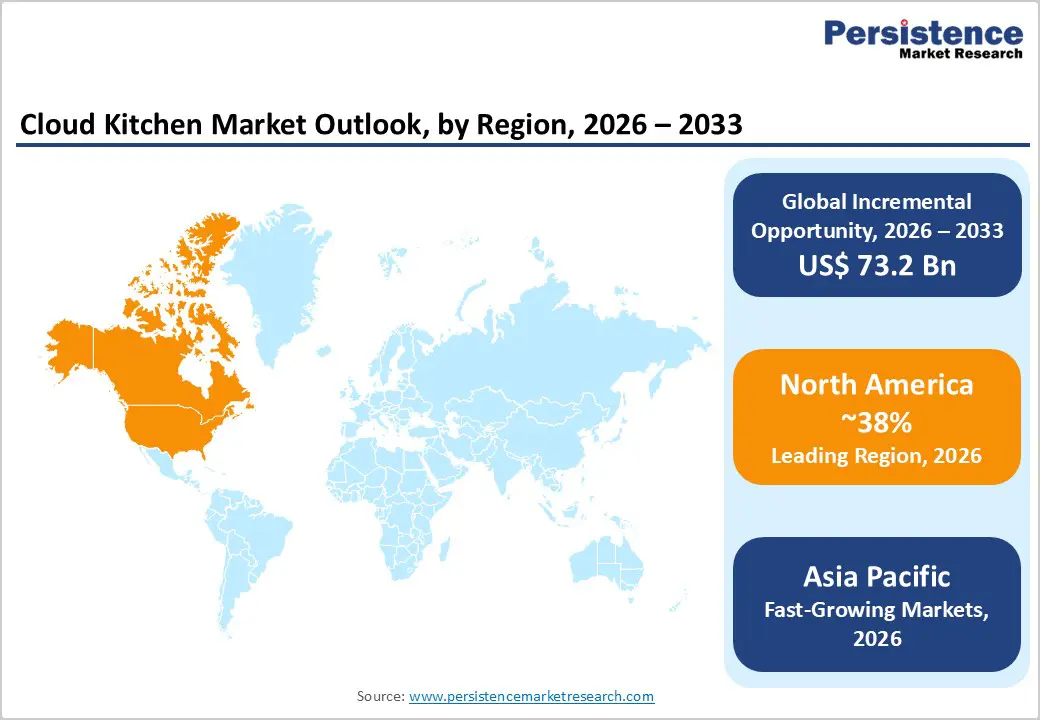

- Leading Region: North America holds approximately 38% of the global cloud kitchen market share in 2025, driven by the highest per-capita food delivery spend globally, and mature digital ordering platform infrastructure.

- Fastest Growing Market: Asia Pacific is the fastest-growing market, propelled by the world's largest food delivery user bases in China, India, and Southeast Asia.

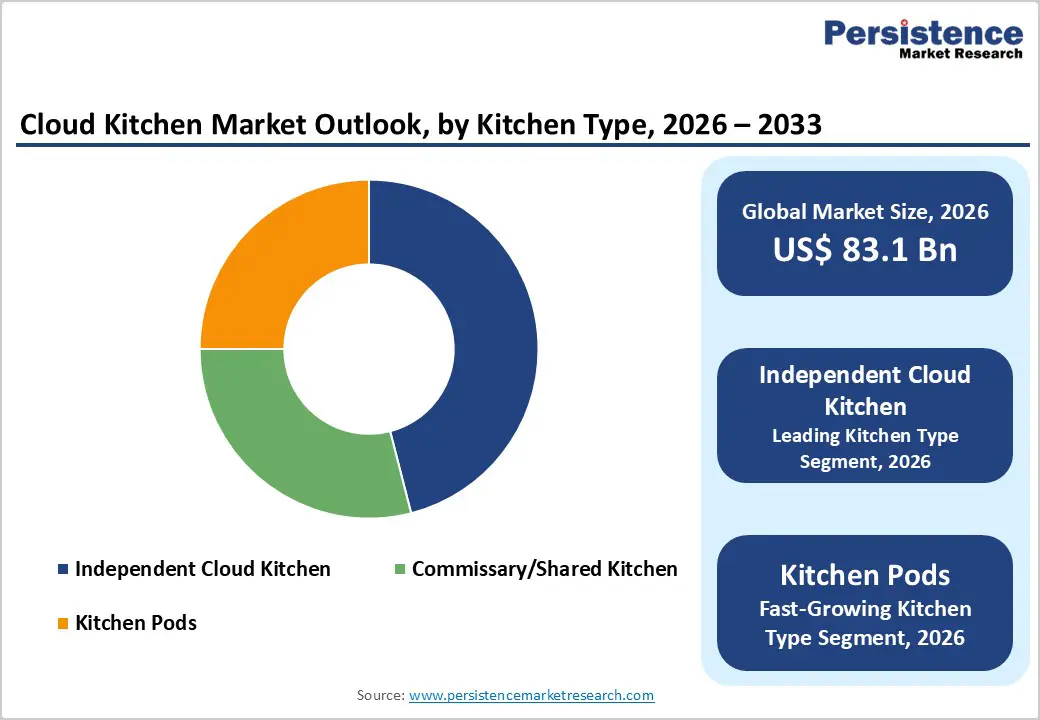

- Dominant Segment: Independent Cloud Kitchens command approximately 46% of global market share in 2025, preferred for their operational flexibility, low capital entry requirements, and maximum brand control, enabling rapid multi-cuisine virtual restaurant concept launches across major metropolitan markets.

- Fastest Growing Segment: Kitchen pods are the fastest-growing kitchen type, deployed by REEF Technology across 4,500+ urban locations to enable hyperlocal, sub-30-minute delivery by positioning cooking infrastructure within minutes of dense residential and commercial demand clusters.

- Key Opportunity: Expanding cloud kitchen services into B2B institutional segments, corporate offices, healthcare facilities, and educational institutions provides operators with predictable volume contracts, reduced aggregator dependency, and superior unit economics compared to volatile direct consumer ordering channels.

Market Dynamics

Drivers - Growth of Online Food Delivery and Changing Consumer Dining Behavior

The permanent behavioral shift toward online food ordering is the single most powerful structural demand driver for cloud kitchens globally. According to the National Restaurant Association, off-premises dining, including delivery and takeaway, accounted for over 60% of total U.S. restaurant sales in 2023, a dramatic increase from pre-pandemic levels.

Statista reports that global online food delivery revenue is projected to grow at approximately 10% annually through 2027, directly expanding the addressable market for delivery-optimized cloud kitchen operations. The proliferation of super-app platforms, including Grab Holdings in Southeast Asia and Zomato and Swiggy in India creates an integrated demand and logistics ecosystem that dramatically lowers order acquisition costs for cloud kitchen operators, validating the model's unit economics at scale.

Capital Efficiency Advantage and Scalable Multi-Brand Operating Model

Cloud kitchens offer food entrepreneurs and established restaurant operators a uniquely capital-efficient expansion model requiring 75–80% less upfront investment than a full-service dine-in restaurant, enabling rapid market entry and geographic scaling that traditional formats cannot match. The multi-brand kitchen model, pioneered by operators such as Rebel Foods (which operates over 45 food brands from shared cloud kitchen infrastructure) and Kitopi, demonstrates that a single kitchen facility can simultaneously operate multiple cuisine-specific virtual restaurant brands, maximize fixed cost amortization and reducing the revenue concentration risk inherent in single-brand food businesses. This model is attracting significant venture capital. CloudKitchens has raised over US$ 850 million, validating the scalability thesis and providing capitalization depth for geographic rollout.

Restraints - Customer Trust Issues Due to no Physical Dining Experience

Customer trust issues due to no physical dining experience is a major restraint in the cloud kitchen market because customers cannot directly see the kitchen environment, hygiene practices, or food preparation process before ordering. Unlike traditional restaurants, where ambiance, cleanliness, and staff interaction help build confidence, cloud kitchens operate entirely through digital platforms, making the experience intangible. This lack of transparency often creates doubts regarding food quality, freshness, and safety standards, especially among first-time users.

Negative experiences such as delayed deliveries, incorrect orders, or inconsistent taste can further reduce trust and discourage repeat purchases. Additionally, the absence of dine-in feedback or face-to-face interaction limits emotional connection with the brand, making it harder to build long-term customer loyalty. In highly competitive urban markets, customers often switch between multiple brands based on reviews and ratings rather than brand attachment. To overcome this challenge, cloud kitchens must invest heavily in strong online reputation management, transparent packaging, real-time tracking, and consistent quality assurance to gradually build consumer confidence and trust over time.

Opportunities - Partnership opportunities with aggregators and quick-commerce platforms

Partnership opportunities with food aggregators and quick-commerce platforms represent a major growth driver for the cloud kitchen market. By collaborating with established delivery apps, cloud kitchens can instantly access a large and ready customer base without heavy investment in physical infrastructure or marketing. These platforms also provide valuable data analytics, helping kitchens understand consumer preferences, peak order times, and location-based demand patterns, enabling better menu planning and pricing strategies. Quick-commerce platforms further enhance growth by ensuring faster delivery times, which improves customer satisfaction and repeat orders.

Such partnerships also allow cloud kitchens to scale rapidly across multiple locations and test new food concepts with minimal risk. Additionally, promotional visibility on aggregator apps increases brand recognition and order frequency. As digital ordering continues to dominate food consumption behavior, these collaborations are becoming essential for improving operational efficiency, expanding market reach, and strengthening competitive positioning in the evolving food service industry.

Category-wise Analysis

Kitchen Type Insights

Independent Cloud Kitchens command the leading kitchen type share of approximately 46% of the global cloud kitchen market in 2025, reflecting their status as the preferred entry model for both restaurant brand owners launching delivery-only concepts and tech-enabled operators building multi-brand food businesses from dedicated leased facilities. Independent cloud kitchens offer operators maximum operational control over food quality, brand identity, and menu design advantages that commissary/shared models constrain. The low capital requirement and flexibility of the independent model has enabled rapid proliferation of virtual restaurant brands globally, particularly in major metropolitan markets. Rebel Foods' global expansion across 10+ countries using independent cloud kitchen infrastructure exemplifies the scalability of this model. Kitchen Pods are the fastest-growing segment, driven by hyperlocal deployment economics.

Nature Insights

Standalone cloud kitchens lead the nature segment with approximately 62% of global market share in 2025, driven by the dominance of independent restaurant entrepreneurs, virtual food brand startups, and established restaurant groups launching delivery-exclusive concepts without franchise obligations. The standalone model offers greater agility in menu experimentation, pricing strategy, and brand positioning critical advantages in the rapidly evolving delivery food landscape where consumer preferences shift quickly. Franchised cloud kitchens are the fastest-growing nature segment, as established quick-service restaurant (QSR) brands, including global chains, leverage franchise frameworks to rapidly expand their delivery-only presence in new geographies through third-party licensed operators, using Ghost Kitchen Brands and similar white-label models to scale efficiently.

End-user Insights

Individual Consumers represent the dominant end-user segment with approximately 71% of global cloud kitchen revenue in 2025, anchored by the mass-market scale of food delivery platforms serving hundreds of millions of households globally. The direct-to-consumer ordering channel powered by aggregators and cloud kitchen operators' own apps constitutes the foundational revenue base of the cloud kitchen industry. According to Statista, there were over 2 billion online food delivery users globally in 2024, with the consumer segment showing the broadest geographic penetration. Corporate Offices are the fastest-growing end-user segment, as hybrid work models create structured daily meal demand during in-office days, with companies investing in curated cloud kitchen meal programs as employee welfare benefits to encourage office attendance.

Regional Insights

North America Cloud Kitchen Market Trends and Insights

North America leads the global cloud kitchen market with approximately 38% of global share in 2025, driven by the highest per-capita food delivery spending globally, dense urban markets ideal for cloud kitchen economics, and a mature venture capital ecosystem that has funded operators including CloudKitchens and REEF Technology. The region's regulatory frameworks are evolving to accommodate the cloud kitchen model, with growing city-level policy attention on commissary licensing and food safety compliance.

U.S. Cloud Kitchen Market Size

The United States accounts for approximately 82% of North American cloud kitchen market revenue, supported by over 150,000 estimated virtual restaurant listings across major delivery platforms per Bloomberg reporting. The post-pandemic permanence of delivery behavior, DoorDash's dominant platform scale, and the proliferation of multi-brand operators sustain the U.S. as the world's single largest national cloud kitchen market.

Europe Cloud Kitchen Market Trends and Insights

Europe represents the second-largest cloud kitchen market, holding approximately 22% of global share in 2025, with strong demand across the U.K., Germany, France, and the Netherlands. Deliveroo's and Just Eat Takeaway's strong European platform presence provides cloud kitchen operators with broad consumer reach, while growing urban density and rising commercial rental costs are making the cloud kitchen model increasingly attractive versus traditional restaurant formats.

Germany Cloud Kitchen Market Size

Germany accounts for approximately 16–18% of the European cloud kitchen market, with strong online food ordering adoption in Berlin, Munich, and Hamburg. Lieferando (Just Eat Takeaway) dominates the platform layer. Rising urban delivery demand and growing immigrant cuisine preferences are expanding virtual restaurant brand diversity, supporting sustained cloud kitchen infrastructure investment through 2033.

U.K. Cloud Kitchen Market Size

The United Kingdom is Europe's most mature cloud kitchen market, contributing approximately 28–30% of regional revenue. Deliveroo and Uber Eats provide a deep delivery platform infrastructure. The Food Standards Agency (FSA) has developed specific cloud kitchen registration frameworks. High urban restaurant rental costs relative to cloud kitchen fees make the economics particularly compelling for London-based operators.

Asia Pacific Cloud Kitchen Market Trends and Insights

Asia Pacific is the fastest-growing regional cloud kitchen market, propelled by the world's largest food delivery user bases in China, India, and Southeast Asia. China's Meituan platform processed over 50 million daily food delivery orders in 2023, creating a massive demand base for cloud kitchen operators. The region's young, digitally native urban population and deep super-app food-ordering ecosystems create unparalleled growth conditions by 2033.

India Cloud Kitchen Market Size

India represents approximately 20% of the Asia Pacific cloud kitchen market revenue one of the highest growth markets globally, driven by Swiggy and Zomato's combined 600+ million registered user base. Rebel Foods and Curefoods are headquartered in India, validating the country as both a major demand market and a global cloud kitchen innovation hub. Rapid urbanization sustains double-digit demand growth.

Japan Cloud Kitchen Market Size

Japan accounts for approximately 12% of Asia Pacific cloud kitchen market value, with growth driven by increasing acceptance of food delivery among urban working professionals and the expansion of Uber Eats Japan and the Demae-can platform reach. Japan's high urban density, premium food quality expectations, and strong food safety regulatory compliance culture are shaping a distinctive premium-tier cloud kitchen segment targeting quality-conscious consumers.

Competitive Landscape

The cloud kitchen market is highly competitive, driven by rapid digital adoption, food delivery platform expansion, and changing consumer dining preferences. Companies are focusing on multi-brand operations, technology-enabled kitchen management, and strategic partnerships with delivery aggregators to strengthen market presence. Investment in AI-based demand forecasting, smart inventory systems, and data-driven menu optimization is improving operational efficiency and profitability. Expansion through franchising, shared kitchen spaces, and modular kitchen pods is accelerating market penetration.

Key Developments

- In March 2025, Actor Akkineni Naga Chaitanya launched the cloud kitchen brand Shoyu through an exclusive collaboration with Swiggy. It provides Pan-Asian cuisine, including a wide variety of delectable Japanese dishes available to customers in Hyderabad through Swiggy.

- In February 2025, BIGGUYS announced its entry into India’s cloud kitchen market. It aims to open around 150 cloud kitchens by 2030, highlighting its dedication to widespread availability and quick scalability.

Global Cloud Kitchen Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 50.4 billion |

|

Current Market Value (2026) |

US$ 83.1 billion |

|

Projected Market Value (2033) |

US$ 156.3 billion |

|

CAGR (2026–2033) |

9.4% |

|

Leading Region |

North America, ~38% market share (2025) |

|

Dominant Kitchen Type |

Independent Cloud Kitchen, ~46% market share (2025) |

|

Top-Ranking Nature Segment |

Standalone, ~62% market share (2025) |

|

Incremental Opportunity |

US$ 73.2 billion (Absolute Dollar Opportunity, 2026–2033) |

Companies Covered in Cloud Kitchen Market

- Rebel Foods

- Kitopi

- CloudKitchens

- DoorDash

- Zomato

- Swiggy

- REEF Technology

- Deliveroo

- Grab Holdings

- Wonder Group

- Kitchen United

- Ghost Kitchen Brands

- Curefoods

Frequently Asked Questions

The global Cloud Kitchen market is valued at US$ 83.1 billion in 2026.

The primary demand drivers are the structural permanence of online food delivery behavior, with the National Restaurant Association reporting off-premises dining exceeding 60% of U.S. restaurant sales, and the compelling capital efficiency of cloud kitchens requiring 75–80% less investment than traditional restaurants, enabling rapid multi-brand scaling across metropolitan markets by operators like Rebel Foods and Kitopi.

North America leads the global Cloud Kitchen market with approximately 38% of global share in 2025.

The most significant near-term opportunities are the deployment of Kitchen Pods for hyperlocal delivery optimization in high-density urban locations, enabling sub-30-minute delivery windows that are becoming the new consumer expectation and expansion into B2B institutional markets, including corporate catering, healthcare meal services, and educational institution food programs, which offer predictable volumes and reduced aggregator dependency.

The leading companies in the global Cloud Kitchen market include Rebel Foods, Kitopi, CloudKitchens, REEF Technology, Wonder Group, and Kitchen United.