- Specialty & Fine Chemicals

- Calcium Hypophosphite Market

Calcium Hypophosphite Market Size, Share and Growth Forecast, 2026 - 2033

Calcium Hypophosphite Market by Grade (Industrial Grade, Pharmaceutical Grade, Food Grade), Application (Dietary Supplements, Chemical Plating, Animal Nutrition Agent, Antioxidant and Analytical Agent), and Regional Analysis 2026 - 2033

Calcium Hypophosphite Market Share and Trends Analysis

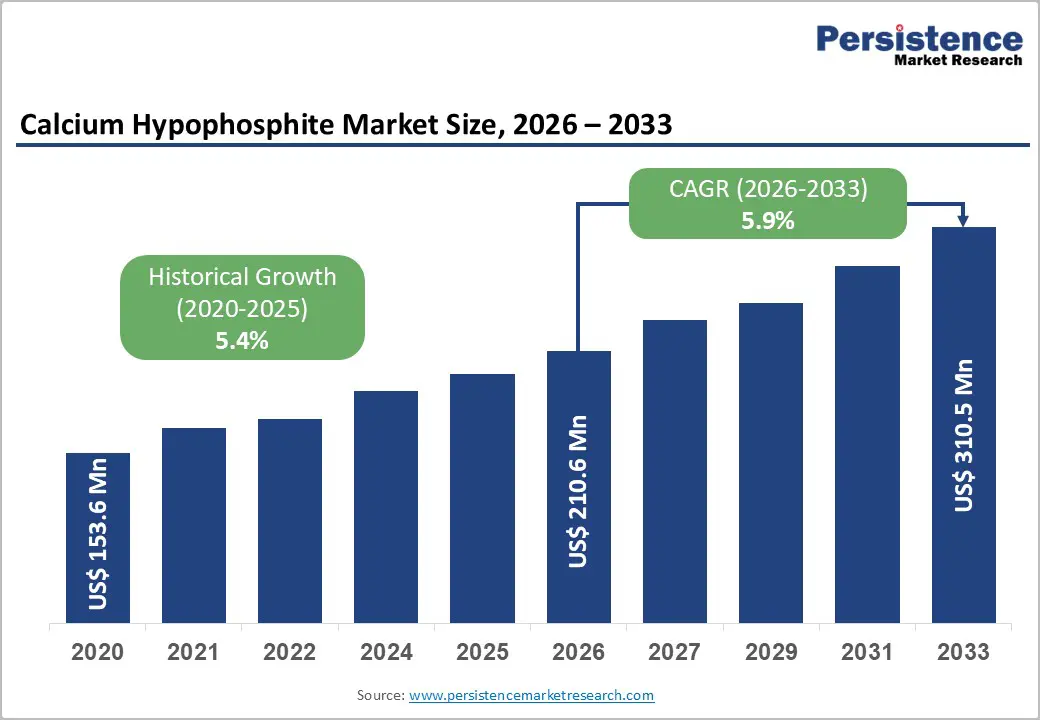

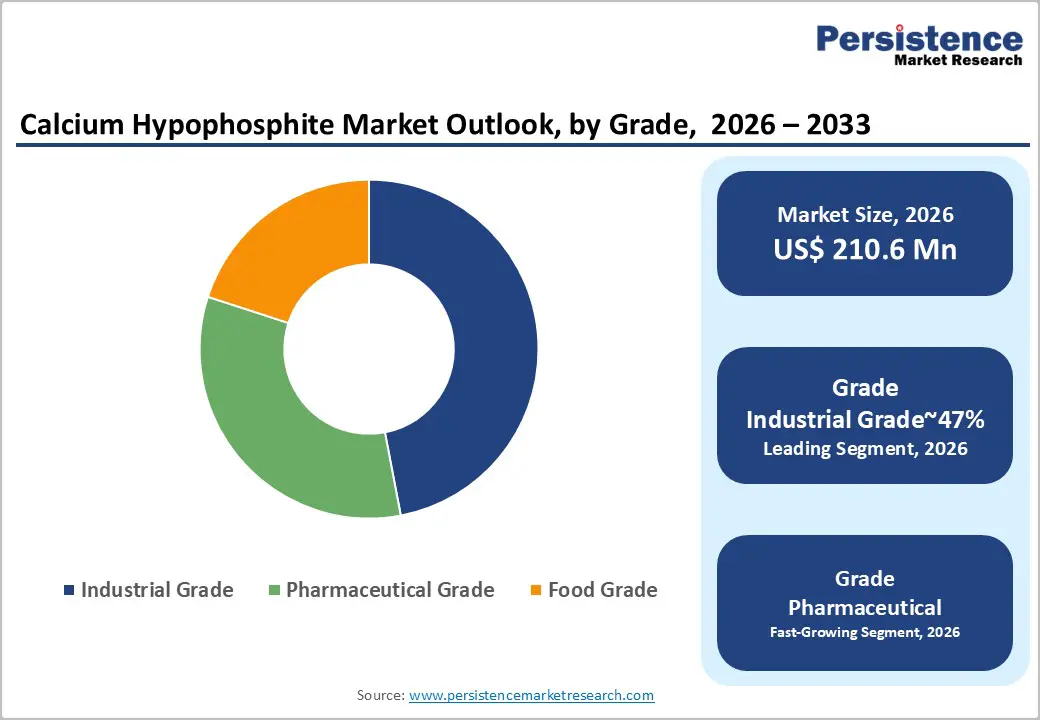

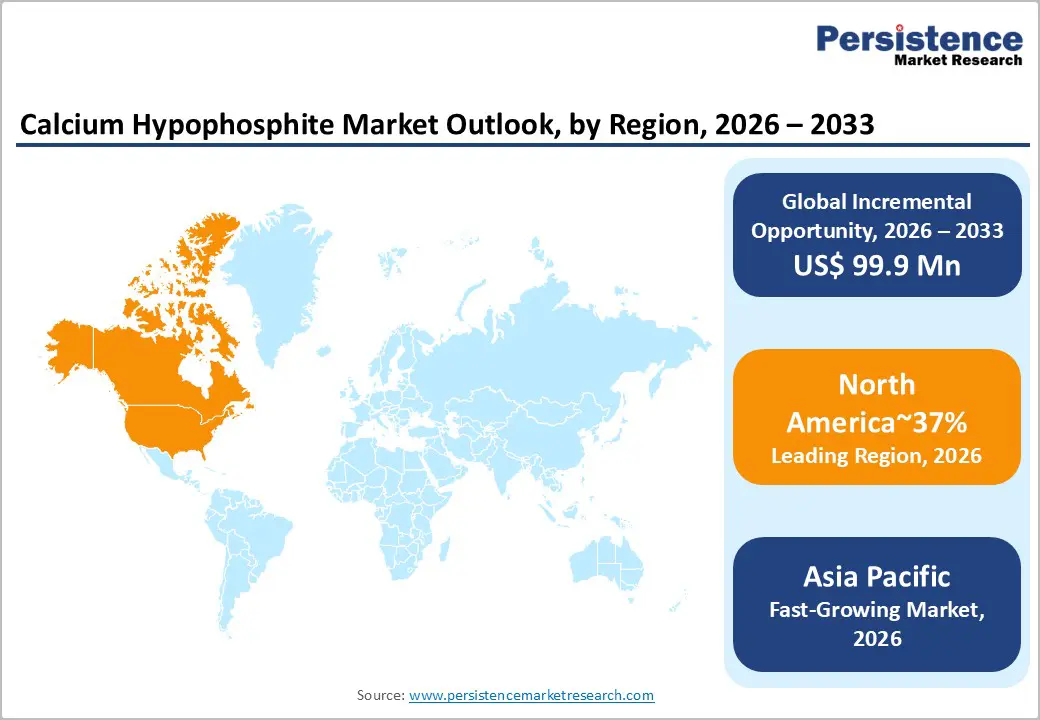

The global calcium hypophosphite market is likely to be valued at US$210.6 million in 2026 and is anticipated to reach US$310.5 million by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033, driven by its critical role as a reducing agent and nutritional additive across highly regulated industries.

Increasing demand for high-purity mineral supplements and advancements in plating technologies are reinforcing its market significance. Stringent quality standards set by global health authorities continue to influence procurement trends for pharmaceutical-grade variants. Meanwhile, ongoing innovations in electroless nickel plating are accelerating adoption across electronics and aerospace manufacturing. The market is further supported by a broader transition toward sustainable and precision-oriented chemical synthesis.

Key Industry Highlights:

- Leading Region: North America is projected to lead due to robust pharmaceutical R&D and established electronics manufacturing hubs accounting for approximately 37% share in 2026, alongside strong technology adoption and mature industrial ecosystems.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest, due to rapid industrialization in Southeast Asia, policy-backed infrastructure expansion, and increasing adoption across wastewater treatment and manufacturing sectors.

- Leading Application: Dietary supplements are expected to lead, accounting for approximately 43% in 2026, through strong industrial adoption, high-volume throughput, quality standardization, and integration into high-value health applications.

- Leading Grade: The industrial grade segment is projected to dominate for simplicity, cost efficiency, widespread adoption, and functional use across chemical plating and flame retardant sectors, holding approximately 47% in 2026.

- Competitive Environment: Manufacturers are prioritizing capacity expansions and high-purity refinement technologies to meet evolving semiconductor standards. Recent strategic moves include vertical integration by major phosphorus producers to secure raw material supply chains amidst global trade volatility.

DRO Analysis

Driver - Nutritional Fortification Mandates

The global push for eradicating micronutrient deficiencies serves as a fundamental pillar for market expansion. The World Health Organization (WHO) continues to advocate for mineral fortification in staple foods and supplements to combat osteoporosis and skeletal disorders. Such global health initiatives encourage manufacturers to procure high-purity calcium sources that offer superior bioavailability and stability. The demand for Ca(H2PO2)2 as a functional ingredient in bone-health formulations continues to rise.

The trend is evident in offerings from American Elements, which supplies high-purity calcium hypophosphite crystals suitable for clinical applications. This emphasis on chemical consistency enables pharmaceutical manufacturers to comply with stringent safety standards set by the U.S. Food and Drug Administration. Looking ahead, market growth is expected to align with the expansion of the wellness industry, where mineral-based ingredients play a central role in developing next-generation dietary formulations.

Animal Nutrition Efficiency Standards

Livestock productivity is increasingly dependent on the precision delivery of essential minerals to improve feed conversion ratios. The Food and Agriculture Organization (FAO) projects that global meat production must increase significantly by 2050, intensifying the need for high-quality feed additives. Calcium hypophosphite serves as a dual-source supplement, providing both phosphorus and calcium in a form that is easily absorbed by poultry and swine.

Market momentum is further evidenced by Sichuan Chuanlin Chemical with Feed Grade Hypophosphite, which targets the expanding agricultural sectors in emerging economies. These products bolster the immune systems of livestock, reducing the reliance on traditional antibiotics in commercial farming. Enhanced regulatory scrutiny over feed safety continues to strengthen the transition toward certified mineral supplements across global supply chains.

Restraint - Competition from Alternate Calcium Sources

The availability of more affordable calcium alternatives, such as calcium carbonate and calcium phosphate, poses a significant threat to the hypophosphite segment. In price-sensitive applications such as basic food fortification or low-end animal feed, buyers often prioritize cost over the specialized functional benefits of hypophosphites. This substitution effect limits the penetration of the calcium hypophosphite market in developing regions, where cost-efficiency is paramount.

Evidence of this competitive pressure is seen in Guanhao High-Tech's product positioning, which must differentiate its specialty offerings from bulk mineral commodities. The challenge lies in justifying the premium price of hypophosphites through superior solubility and reactivity. Without clear technical advantages, the uptake of this compound is poised to remain restricted to niche, high-performance applications.

Opportunity - High-Purity Semiconductor Manufacturing

The global expansion of semiconductor fabrication facilities, particularly in the U.S. and Europe, presents a lucrative growth avenue. High-purity calcium hypophosphite is required for specialized cleaning and etching processes in the production of advanced microchips. As the electronics industry moves toward more complex 3D NAND and logic architectures, the demand for ultrapure chemical reagents is expected to surge.

Projects such as American Elements' ultra-high purity grades target this sophisticated manufacturing niche. This technological inflection point allows chemical providers to capture higher value-added margins compared to traditional industrial sales. Continued investment in domestic chip production through government funding programs reinforces the long-term stability of this high-tech application segment.

Category-wise Analysis

Grade Insights

The industrial grade segment is projected to lead the calcium hypophosphite market, accounting for approximately 47% share in 2026, anchored by its widespread application as a versatile chemical intermediate. This grade is essential for the production of flame retardants and water treatment chemicals, where volume and cost-effectiveness are prioritized over extreme purity. Industrial participants frequently utilize Sichuan Chuanlin Chemical's Industrial Hypophosphite to stabilize polymers and prevent thermal degradation in plastic components. The massive scale of the construction and automotive industries ensures a steady baseline demand for these industrial-grade variants.

The pharmaceutical grade segment is anticipated to be the fastest-growing segment in the calcium hypophosphite market, driven by tightening regulatory oversight and the surge in clinical-grade supplement production. Health authorities in Europe and North America are mandating lower heavy metal limits for mineral ingredients, pushing buyers toward high-purity hypophosphites. Vendors are responding with specialized products like Jiangxi Fuerxin's Pharmaceutical Calcium Hypophosphite, which undergoes multi-stage refinement to ensure safety. This shift toward "clean-label" and GMP-certified minerals represents a significant value-added opportunity for advanced chemical processors.

Application Insights

Dietary supplements are expected to dominate the calcium hypophosphite market, accounting for approximately 43% share in 2026, supported by the global rise in geriatric populations requiring skeletal support. This segment relies on the compound's high elemental calcium content and favorable solubility profile compared to traditional carbonates. Leading vendors such as American Elements provide the necessary purity levels to satisfy international pharmacopeia standards. These high-grade inputs ensure that supplement manufacturers can claim superior bioavailability, which is a key differentiator in the crowded wellness market.

Chemical plating is anticipated to be the fastest-growing segment, driven by the rapid expansion of the electric vehicle (EV) and telecommunications infrastructure. The need for precise, corrosion-resistant nickel layers on sensitive electronic components makes hypophosphites the preferred reducing agent. Manufacturers are increasingly adopting Hubei Furui Chemical's Industrial Calcium Hypophosphite to achieve consistent plating rates and high-phosphorus alloy deposits. This trend is further accelerated by the 5G rollout, which necessitates advanced electromagnetic shielding on high-frequency circuit boards.

Regional Analysis

North America Calcium Hypophosphite Market Trends

North America is expected to be the leading market region, accounting for approximately 37% share in 2026, supported by a highly developed healthcare sector and a resurgence in domestic semiconductor fabrication. The regional market benefits from the presence of major pharmaceutical companies that prioritize high-stability mineral inputs for chronic disease treatments.

U.S. Calcium Hypophosphite Market Trends

The U.S. is expected to dominate, driven by policy support for domestic chemical and semiconductor production. American Elements expands output of electronics-grade phosphorus derivatives to meet industrial demand. Growth in high-potency supplement formulations strengthens pharmaceutical procurement of calcium hypophosphite. Industrial alignment between electronics and healthcare sectors reinforces sustained material consumption.

Canada Calcium Hypophosphite Market Trends

Canada is anticipated to support regional growth driven by strict regulatory frameworks for natural health products. Emphasis on high-purity mineral processing enhances export compatibility with major pharmaceutical markets. Focus on sustainable mining and phosphorus recycling strengthens domestic supply chain resilience. Market trends reflect alignment between environmental standards and specialty chemical production.

Europe Calcium Hypophosphite Market Trends

Europe is expected to remain structurally stable, supported by industrial plating demand and regulated pharmaceutical applications. Strict compliance frameworks under regional health authorities sustain the use of high-purity calcium hypophosphite. Demand remains anchored in electronics plating and controlled pharmaceutical formulations. Market dynamics reflect alignment between regulatory standards and specialty chemical utilization across industrial and healthcare sectors.

Germany Calcium Hypophosphite Market Trends

Germany is expected to dominate, driven by stringent pharmaceutical standards and a strong industrial manufacturing base. Hubei Xingfa Chemicals Group strengthens supply through expanded exports, supporting plating applications. Growth in automotive electronics manufacturing increases demand for high-performance chemical inputs. Industrial integration of precision materials reinforces sustained consumption across key sectors.

U.K. Calcium Hypophosphite Market Trends

The U.K. is anticipated to support regional demand driven by regulatory oversight on supplements and pharmaceutical usage. GFS Chemicals Inc. advances high-purity formulations supporting dietary and industrial applications. Recovery in manufacturing activity strengthens demand for specialty chemical grades. Market trends emphasize regulatory compliance and diversified applications across healthcare and industrial segments.

Asia Pacific Calcium Hypophosphite Market Trends

Asia Pacific is anticipated to be the fastest-growing region, driven by the massive expansion of the Chinese electronics industry and rising middle-class spending on nutritional supplements in India. Government-led infrastructure projects in Southeast Asia also contribute to the heightened demand for industrial-grade plating chemicals.

China Calcium Hypophosphite Market Trends

China is expected to dominate, supported by large-scale production capacity and advanced materials policy frameworks. Hubei Furui Chemical Co., Ltd. strengthens global supply through extensive hypophosphite salt production capabilities. Expansion in water treatment and chemical waste management drives additional demand. Industrial growth reinforces China’s role as a key export hub.

India Calcium Hypophosphite Market Trends

India is anticipated to lead growth, supported by pharmaceutical manufacturing incentives and expanding domestic demand. Increasing investments in high-purity chemical production reduce reliance on imports. Growth in health supplement consumption strengthens demand for calcium hypophosphite across formulations.

Key Industry Developments:

- In January 2026, 'Minapharm' acquired the global rights for Praxilene® from Merck to expand its pharmaceutical portfolio. This acquisition will strengthen the pharmaceutical segment's demand for high-purity reducing agents like calcium hypophosphite, used in synthesizing advanced cardiovascular drug formulations.

- In February 2026, 'Solvay' announced the completion of its largest GHG emission reduction project at the Green River facility. By phasing out coal and integrating renewable energy, Solvay has lowered the carbon footprint of its phosphorus-adjacent production, appealing to eco-conscious industrial buyers.

Companies Covered in Calcium Hypophosphite Market

- American Elements

- Hubei Xingfa Chemicals Group Co., Ltd.

- Hubei Furui Chemical

- Jiangxi Fuerxin Medicine Chemical

- Sichuan Chuanlin Chemical

- Henan Yinghua Biotechnology

- Merck Group (Sigma-Aldrich)

- GFS Chemicals

- Triveni Chemicals

- Thermo Fisher Scientific

- Tokyo Chemical Industry Co., Ltd.

- Alfa Aesar (Thermo Fisher Scientific)

- Loba Chemie Pvt. Ltd.

- Central Drug House (CDH)

- MP Biomedicals

- Spectrum Chemical Manufacturing Corp.

Frequently Asked Questions

The global calcium hypophosphite market is likely to be valued at US$210.6 million in 2026 and is anticipated to reach US$310.5 million by 2033.

Primary drivers include the rising demand for bone-health dietary supplements and innovations in electroless nickel plating for the electronics sector.

The global market is projected to grow at a CAGR of 5.9% from 2026 to 2033, sustained by industrial-grade demand.

Key opportunities lie in the expansion of high-purity semiconductor manufacturing and the adoption of precision agriculture nutrient delivery systems.

Prominent players include American Elements, Hubei Furui Chemical, Jiangxi Fuerxin Medicine Chemical, and Sichuan Chuanlin Chemical.