- Specialty & Fine Chemicals

- Scale Inhibitors Market

Scale Inhibitors Market Size, Share and Growth Forecast, 2026 - 2033

Scale Inhibitors Market by End-use Industry (Oil & Gas, Water & Wastewater Treatment, Power Generation, Others), Formulation Type, Scale Type Controlled, and Regional Analysis for 2026 - 2033

Scale Inhibitors Market Share and Trends Analysis

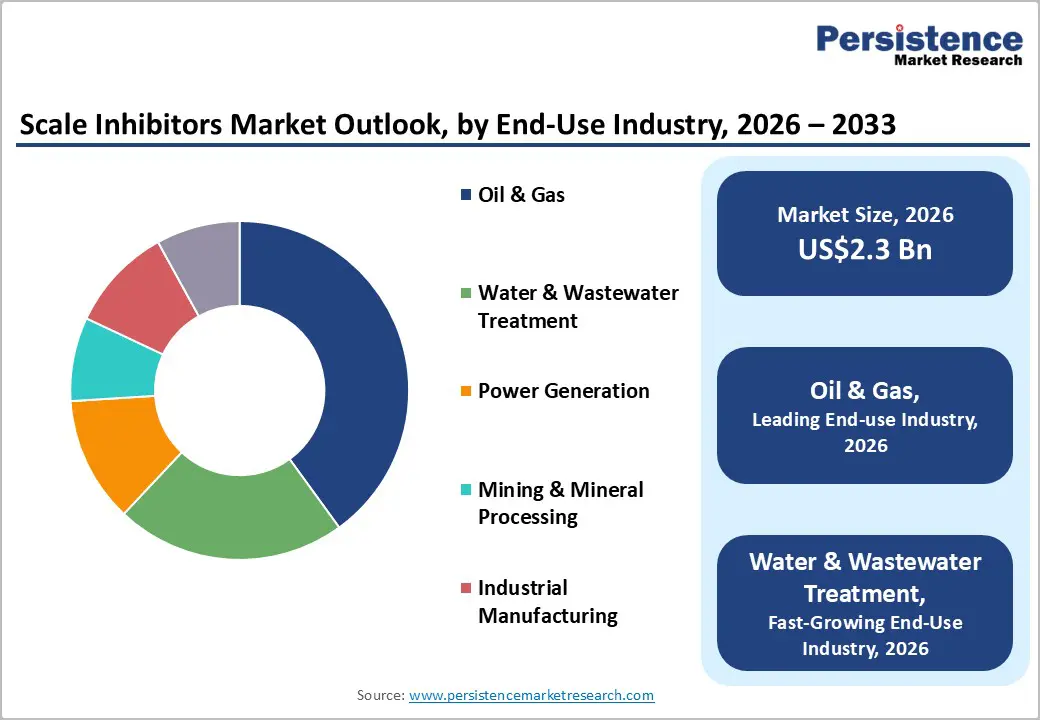

The global scale inhibitors market size is likely to be valued at US$ 2.3 billion in 2026 and is projected to reach US$ 3.2 billion by 2033, growing at a CAGR of 4.7% during 2026 - 2033, driven by rising demand for industrial water treatment chemicals, expansion of oil & gas production activities, and increasing desalination capacity worldwide.

According to data aligned with IEA energy transition insights and OECD water stress assessments, scaling-related operational inefficiencies are increasing in high-pressure systems. Additionally, stricter discharge regulations from agencies such as the U.S. EPA and the EU Water Framework Directive are accelerating the adoption of advanced scale control solutions across industries.

Key Industry Developments:

- End-use Industry Leadership: Oil & gas is set to command around 40% share in 2026, while water & wastewater treatment is projected to grow the fastest through 2033, driven by rising industrial water demand, infrastructure expansion, and stricter discharge regulations.

- Formulation Type Leadership: Liquid formulations are expected to lead with around 55% share in 2026, supported by high dosing efficiency and wide industrial adoption across oil & gas and water treatment systems.

- Scale Type Dynamics: Calcium carbonate scale is set to dominate with around 35% share in 2026, while mixed inorganic scale systems are projected to grow the fastest through 2033, driven by complex scaling conditions in deepwater and desalination systems.

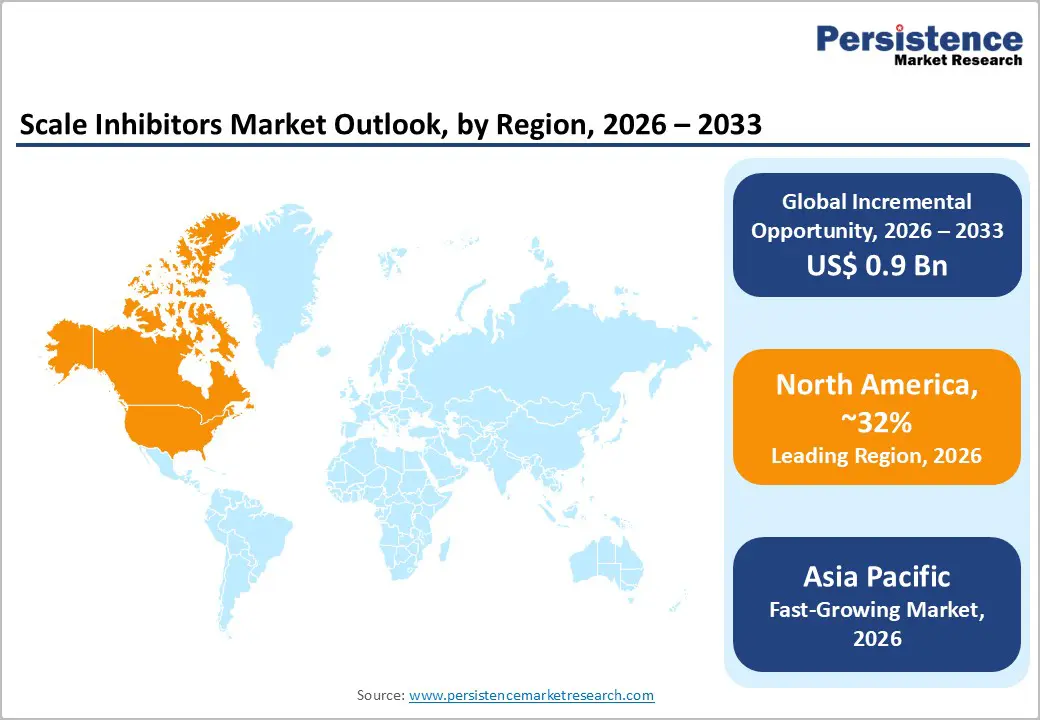

- Regional Leadership: North America is expected to lead with around 32% share in 2026, while Asia Pacific is projected to grow the fastest through 2033, driven by rapid industrialization, urbanization, and rising demand for industrial water treatment solutions.

- Competitive Environment: Market competition is increasingly driven by innovation in sustainable scale inhibitors, along with digital dosing technologies and integrated water treatment solutions across industrial applications.

DRO Analysis

Driver - Rising Demand from Oil & Gas Production and Enhanced Recovery Operations

The oil & gas sector remains the largest consumer of scale inhibitors, driven by increasing deepwater exploration and enhanced oil recovery (EOR) techniques. According to the U.S. Energy Information Administration (EIA), global upstream investment is steadily recovering post-2020 volatility, strengthening demand for production chemicals. Scale formation in pipelines, wells, and separators continues to reduce efficiency and raise operating costs by 5-7% of total production expenses. As unconventional reserves expand across North America and the Middle East, operators are increasingly relying on chemical scale inhibition programs to maintain flow assurance and protect asset integrity.

The adoption has accelerated with oilfield operators deploying AI-based monitoring and real-time chemical dosing systems to manage scaling in mature and deepwater fields. Projects in regions such as the Permian Basin are increasingly using predictive water management tools to optimize chemical usage and improve production reliability. At the same time, stricter environmental controls on produced water reuse are pushing operators toward advanced treatment chemistries. This is further increasing demand for high-performance, thermally stable, low-toxicity scale inhibitors, especially in high-salinity and ultra-deep reservoirs, reinforcing steady market expansion.

Restraint - Environmental Regulations and Supply Chain Volatility in Chemical Production

The use of phosphonate and phosphate-based inhibitors is increasingly restricted due to environmental concerns such as eutrophication and aquatic toxicity. Regulatory frameworks from the European Chemicals Agency (ECHA) and the U.S. EPA Toxic Substances Control Act (TSCA) are tightening allowable chemical thresholds. This is raising compliance costs, extending approval timelines, and limiting flexibility in new product development. As a result, smaller manufacturers face higher entry barriers, slowing innovation and market expansion.

In 2025-2026, regulatory pressure has intensified further with stricter enforcement under REACH in Europe and deeper chemical safety reviews under TSCA in the U.S., increasing testing and documentation requirements across the industry. The global crackdown on water contaminants such as PFAS is accelerating restrictions on industrial water treatment chemicals, adding further compliance complexity. On the supply side, petrochemical-linked raw material volatility and intermittent disruptions in major manufacturing hubs continue to create cost instability. These factors are tightening margins and limiting pricing predictability across the scale inhibitors value chain.

Opportunity - Expansion of Desalination, Water Reuse, and Green Chemistry Solutions

The global desalination capacity is expanding rapidly, particularly in Saudi Arabia, the UAE, and China. According to International Desalination Association (IDA) estimates, global installed capacity continues to grow at over 5% annually. Scale formation remains one of the most critical operational challenges in reverse osmosis (RO) systems. This creates strong demand for specialty scale inhibitors for membrane protection, opening a high-value opportunity segment worth an estimated US$ 600-800 million by 2033.

Alongside infrastructure growth, the shift toward sustainable water management is unlocking strong momentum for green and bio-based scale inhibitors. Companies are increasingly investing in biodegradable, low-toxicity, and non-phosphorus chemistries to align with stricter environmental expectations. Supportive regulatory direction under clean water initiatives and sustainability-focused policies is accelerating adoption in municipal systems. This transition is particularly strong in food-grade industries and urban water treatment, where eco-compliance is becoming a key procurement criterion, creating a fast-scaling premium niche within the market.

Category-wise Analysis

End-use Industry Insights

The oil & gas segment remains the leading end-use industry in the scale inhibitors market, accounting for an estimated 40% share in 2026, driven by widespread use in upstream and midstream operations where scaling impacts flow efficiency. High-pressure drilling, deepwater exploration, and reservoir complexity continue to require advanced chemical treatment for operational stability. The offshore expansion projects under Norway’s Continental Shelf development and stricter produced water management norms introduced by the U.S. BSEE are further reinforcing demand for high-efficiency, low-dosage inhibitor systems.

The water & wastewater treatment segment is projected to be the fastest-growing, supported by urbanization, stricter discharge standards, and rising adoption of membrane-based filtration systems. In 2025-2026, desalination expansion in China under national water conservation initiatives and capacity upgrades by Singapore’s PUB (NEWater program) are accelerating demand for advanced anti-scaling solutions, strengthening adoption across municipal and industrial water treatment infrastructure.

Formulation Type Insights

Liquid formulations dominate the scale inhibitors market, accounting for around 55% share in 2026, driven by easy dosing, high solubility, and strong compatibility with automated chemical injection systems. Their widespread use across oilfield production programs and industrial water systems reinforces their leadership position. Adoption has further strengthened with digital chemical injection upgrades in the Middle Eastern offshore assets and refinery modernization projects in Asia, where precision dosing and operational efficiency are critical.

Emulsion formulations are the fastest-growing segment, supported by improved stability and controlled-release performance under extreme operating conditions. Usage has expanded in ultra-high temperature geothermal projects in Iceland and high-salinity offshore systems in Brazil’s pre-salt fields, where conventional formulations face performance limitations. These applications are accelerating demand for more durable and longer-acting chemical solutions.

Scale Type Controlled Insights

Calcium carbonate scale remains the leading segment, contributing around 35% share in 2026, as it is the most common scaling issue across industrial water systems and oilfield operations. Its predictable formation behavior ensures strong compatibility with conventional inhibitor chemistries. Rising scaling incidents in thermal power cooling systems in China and ongoing maintenance programs in U.S. municipal water networks continue to sustain steady demand for calcium carbonate control solutions.

Mixed inorganic scale systems are emerging as the fastest-growing category, driven by increasingly complex scaling environments involving multiple mineral deposits. This challenge has become more prominent in Saudi Arabia’s Red Sea desalination mega-projects and offshore deepwater developments in West Africa, where mixed-scale deposition is becoming harder to manage. These conditions are pushing operators toward more advanced, multi-functional scale inhibition technologies.

Regional Analysis

North America Scale Inhibitors Market Trends

North America is expected to account for approximately 32% of the global market share in 2026, supported by strong oil & gas production activity, shale development, and advanced industrial water treatment systems. The region benefits from mature infrastructure, high chemical adoption rates, and continuous modernization of pipeline and water reuse systems. Strong regulatory oversight and rapid digitalization of chemical dosing further strengthen market maturity and technology integration.

U.S. Scale Inhibitors Market Trends

The U.S. is projected to dominate, holding around 65% of the regional share in 2026, driven by large-scale shale gas production, offshore operations, and extensive wastewater treatment infrastructure. Continuous investments in pipeline integrity, digital oilfield systems, and produced water management are sustaining strong demand for oilfield production chemicals, including scale inhibitors. Ongoing shale modernization across major basins is reinforcing the adoption of advanced flow assurance solutions.

Canada Scale Inhibitors Market Trends

Canada is expected to contribute around 10% of the regional share in 2026, supported by oil sands production, mining operations, and cold-climate industrial water systems. Increasing focus on environmental compliance and water recycling in resource extraction industries is driving the adoption of advanced scale control solutions. Recent efficiency upgrades in Alberta’s oil sands operations aimed at reducing water intensity and improving extraction efficiency are strengthening demand for high-performance chemical treatment systems.

Europe Scale Inhibitors Market Trends

Europe is expected to account for approximately 25% share of the global market share in 2026, supported by strict environmental regulations, a strong industrial base, and a growing emphasis on sustainable chemical usage. The region is characterized by regulatory-driven demand for low-phosphate and biodegradable inhibitors, alongside increasing adoption in industrial water reuse and energy efficiency programs. Continuous modernization of manufacturing and water infrastructure is further supporting steady market expansion.

Germany Scale Inhibitors Market Trends

Germany holds around 30% share of the regional market share, driven by its strong chemical processing industry, advanced manufacturing base, and high industrial water treatment adoption. Demand is reinforced by efficiency-focused upgrades across automotive, power, and industrial sectors, where scale control is critical for operational reliability. Ongoing industrial water optimization programs are further strengthening the use of advanced inhibitor systems.

U.K. Scale Inhibitors Market Trends

The U.K. is expected to contribute approximately 15% of the regional share, supported by offshore oil & gas operations, aging water infrastructure upgrades, and expanding wastewater treatment modernization. Continued investment in North Sea asset maintenance and industrial water efficiency improvements is driving steady demand for scale control solutions. Recent upgrades in municipal water treatment systems are further supporting the adoption of advanced chemical formulations.

Asia Pacific Scale Inhibitors Market Trends

Asia Pacific is set to be the fastest-expanding regional market, accounting for approximately 28% share of the global scale inhibitors market, driven by rapid industrialization, urban growth, and large-scale infrastructure expansion in power generation and water treatment. Rising water stress and strong manufacturing activity are significantly increasing demand for industrial water treatment solutions and chemical scale control technologies.

China Scale Inhibitors Market Trends

China is expected to lead, accounting for 50% share of the Asia Pacific market share, supported by large-scale petrochemical complexes, desalination projects, and industrial wastewater treatment expansion. Strong government-led water conservation and industrial efficiency programs are accelerating the adoption of advanced scale inhibition technologies. Recent coastal desalination capacity expansions are further reinforcing chemical demand.

India Scale Inhibitors Market Trends

India is projected to hold approximately 20% market share within Asia Pacific, driven by expanding thermal power generation, rapid urban water infrastructure development, and growing industrial manufacturing. Increasing focus on water reuse and pipeline efficiency is boosting demand for cost-effective scale control solutions. Large-scale municipal water treatment upgrades are further strengthening market penetration.

Competitive Landscape

The global scale inhibitors market is moderately consolidated, led by key players such as BASF SE, Ecolab, Solenis, Kemira, and SNF Group, which together account for a significant share of global revenue. These companies leverage strong customer networks across oil & gas, water treatment, and power industries, supported by integrated service offerings and long-term contracts. Continuous investment in advanced water treatment chemicals and scale control technologies strengthens their competitive positioning.

Regional and niche players are expanding through specialized solutions for desalination, high-salinity oilfields, and industrial cooling systems. Companies such as Italmatch Chemicals and Nouryon focus on differentiated formulations, while oilfield-linked firms such as Baker Hughes and SLB integrate scale inhibitors into broader production chemical portfolios. High entry barriers due to regulatory compliance and technical complexity limit new entrants, but partnerships and targeted acquisitions are gradually reshaping competition and supporting market consolidation.

Key Industry Developments:

- In October 2025, BASF sold its Brazilian decorative paints business for US$ 1.15 billion and its automotive coatings unit for €7.7 billion (US$8.24 billion) under its “Winning Ways” strategy. The move reflects a sharper focus on core specialty chemicals, including industrial and water treatment-related solutions.

- In September 2025, SLB acquired RESMAN to enhance its reservoir monitoring and production optimization capabilities, completing the deal in early 2026.

The integration improves real-time tracking of fluid movement and strengthens scale control and flow assurance in oilfield operations.

Companies Covered in Scale Inhibitors Market

- BASF SE

- Ecolab Inc.

- Solenis LLC

- Kemira Oyj

- SNF Group

- Clariant AG

- Dow Inc.

- Baker Hughes Company

- Halliburton Company

- Schlumberger Limited

- AkzoNobel N.V.

- Lubrizol Corporation

- Nouryon

- Italmatch Chemicals

- Cortec Corporation

Frequently Asked Questions

The global scale inhibitors market is valued at approximately US$2.3 billion in 2026.

The scale inhibitors market is driven by rising oil & gas production, expanding water treatment infrastructure, and increasing industrial scaling challenges.

The scale inhibitors market is expected to grow at a CAGR of 4.7% from 2026 to 2033.

Key opportunities include desalination expansion, industrial water reuse projects, and development of sustainable scale inhibitor formulations.

Key players include BASF SE, Ecolab, Solenis, Kemira, SNF Group, Baker Hughes, SLB, and Italmatch Chemicals.