- Technology

- Border Security System Market

Border Security System Market Size, Share, and Growth Forecast 2026 - 2033

Border Security System Market by Platform (Ground, Aerial, Naval), Installation (New Installations, Upgradation), System Type (Radar Systems, Laser Systems, Camera Systems, Intelligent Fencing Systems, Unmanned Vehicles, Wide-Band Wireless Communication Systems, Command and Control Systems, Biometric Systems), and Regional Analysis for 2026 - 2033

Border Security System Market Size and Trend Analysis

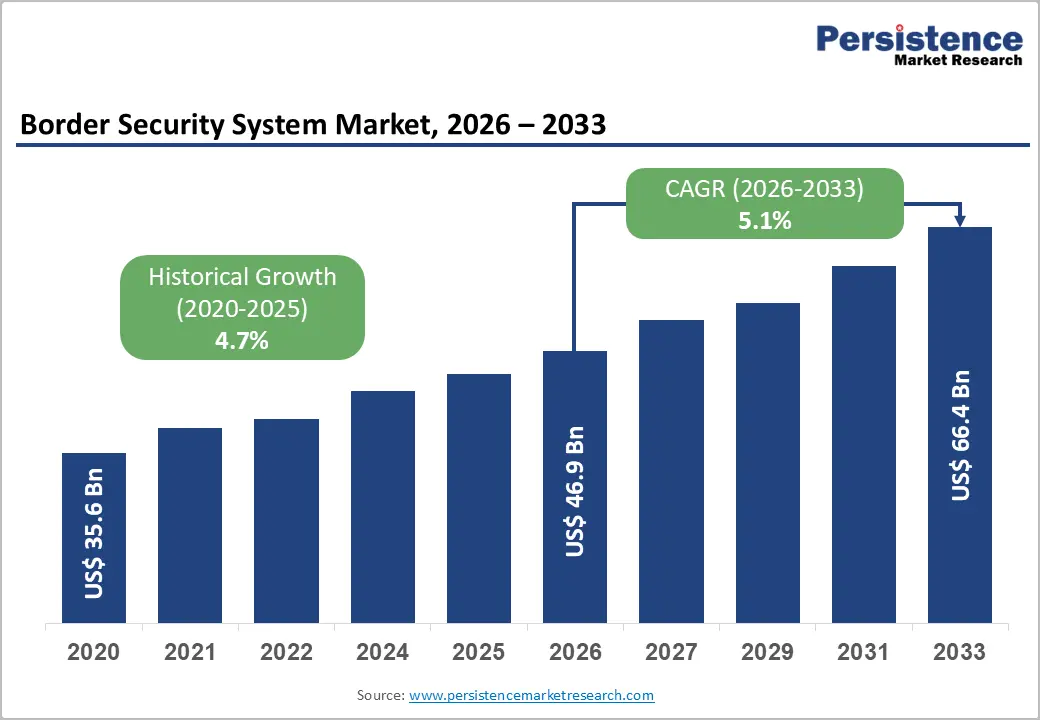

The global border security system market size is expected to be valued at approximately US$ 46.7 billion in 2026 and is projected to reach US$ 66.4 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033. This sustained growth is anchored in the intensifying geopolitical threat environment, which has prompted record-level defence budget commitments across NATO member states, Asia Pacific, and the Middle East. Governments are progressively replacing physical barrier-only approaches with integrated, multi-layer technology platforms encompassing radar, AI-powered surveillance, unmanned systems, and biometric identity verification.

Key Industry Highlights:

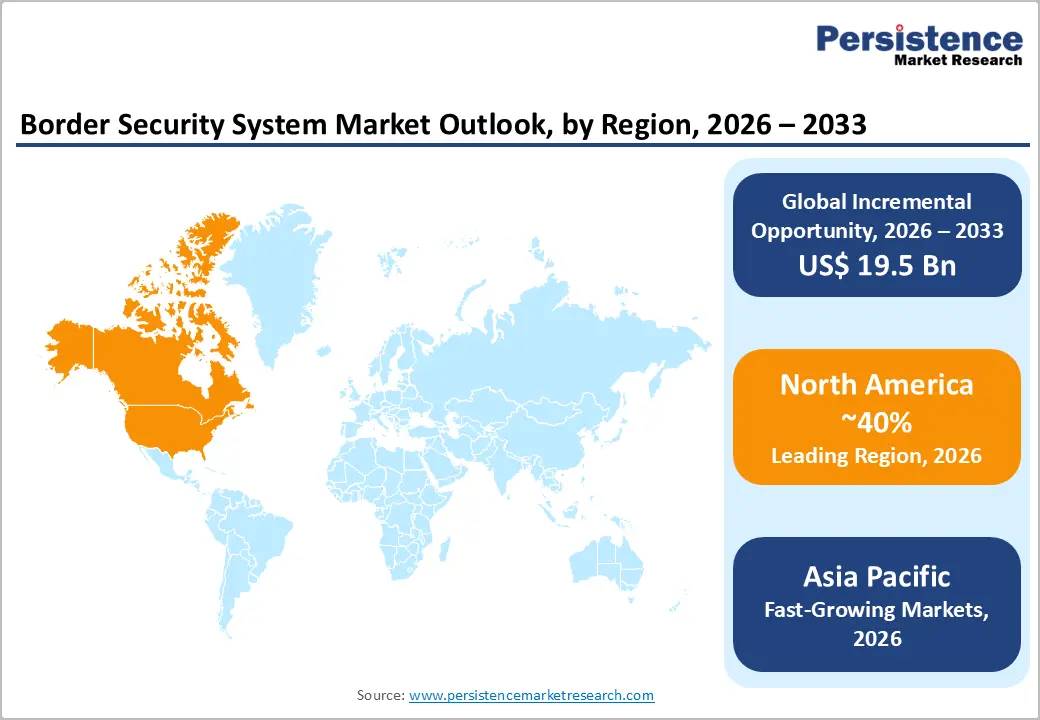

- Leading Region – North America commands the largest global share of the border security system market with approximately 40% revenue share in 2025, anchored by the U.S. CBP's USD 20+ billion annual budget and sustained southwestern border technology investment programs encompassing radar, UAV, biometric, and integrated surveillance tower systems.

- Fastest Growing Region – Asia Pacific is projected to register the highest CAGR through 2033, driven by India's CIBMS program along its 3,300 km priority border segments, SIPRI-documented record Défense budgets across the region, and China's continued border technology modernization along its 14 land border frontiers.

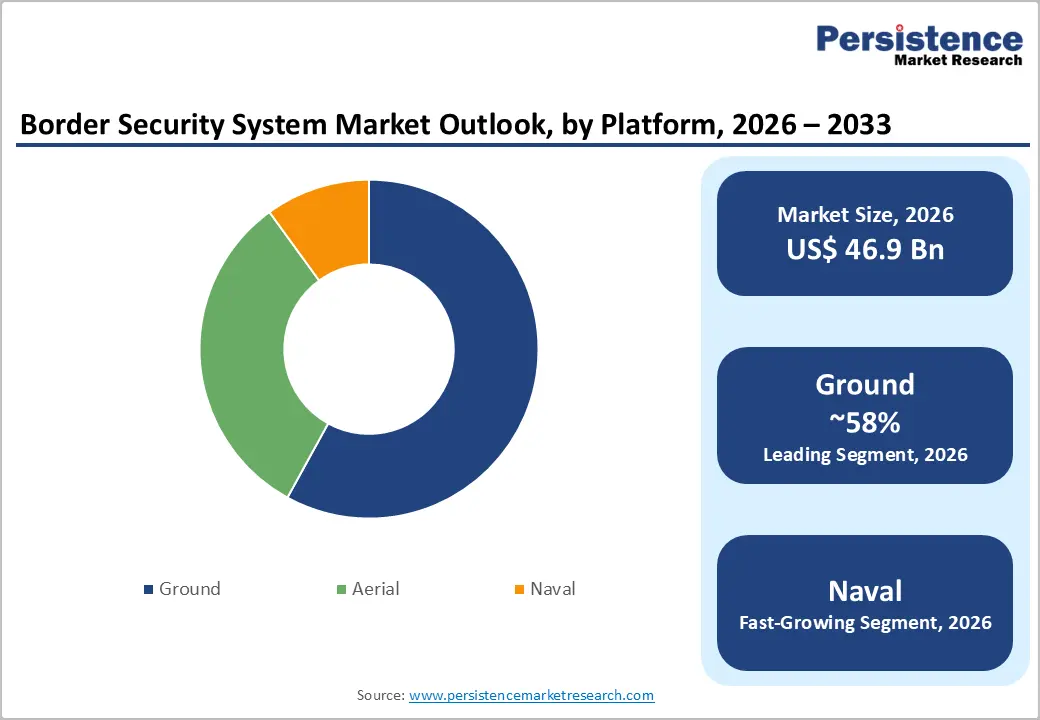

- Dominant Segment – Ground platforms led with approximately 62% share in 2025, anchored by land border surveillance systems covering the world's 250,000+ kilometers of national borders generating the largest volume and diversity of radar, camera, intelligent fencing, and biometric system procurement globally.

- Fastest Growing Segment – Unmanned aerial and ground vehicle systems are the fastest-growing border security technology category, driven by CBP's Predator B UAV programme validation of persistent coverage cost-effectiveness and Frontex's EUROSUR UAV integration expanding European border surveillance drone procurement.

- Key Opportunity: Middle East & Africa's greenfield border security investment with Saudi Arabia's Vision 2030 and the UAE's Smart Border initiative creating premium-specification procurement programs represents an underpenetrated high-value market for vendors with Interpol and ICAO biometric-compliant integrated border management platforms.

DRO Analysis

Rise in Geopolitical Tensions and Cross-Border Threat Complexity Are Driving Unprecedented Government Investment in Border Security Infrastructure

Ongoing conflicts including Russia’s full-scale invasion of Ukraine, South China Sea territorial disputes, and cross-border terrorist activity in South Asia and the Middle East have made border security a non-discretionary defence priority for national governments. NATO member states have committed to the 2% of GDP defence spending target, and the EU’s Frontex budget reached EUR 754 million in 2023 one of the largest in its history for external border surveillance operations.

These commitments are translating into multi-year procurement programmes for ground radar, thermal cameras, surveillance UAVs, and command and control platforms across eastern and southern European border segments. Eastern EU border states including Poland, the Baltic states, and Finland have received emergency budget allocations for border technology investment, generating significant new programme demand that was absent before the Russia-Ukraine conflict.

Mass Migration Crises and Irregular Border Crossing Events Are Compelling Technology-Led Surveillance System Deployment at Land and Maritime Borders

UNHCR reported that forcibly displaced persons reached a record 117 million globally in 2024, placing direct operational pressure on border agencies to deploy surveillance technology providing real-time awareness over stretches that patrol personnel cannot cover alone.

The U.S. CBP documented over 2.4 million encounters at the southwestern border in FY2023, triggering emergency procurement of thermal imaging cameras, ground-based radar towers, and autonomous surveillance platforms under the Southwest Border Technology programme.

Migration surveillance represents a legally defensible and politically sustained procurement driver for vendors, operating independently of conventional defence budget cycles and sustaining predictable long-term demand for camera, radar, and command and control systems.

High System Integration Complexity and Interoperability Challenges Create Program Delays and Cost Overruns That Suppress Procurement Velocity

Integrated border security systems spanning ground radar, aerial vehicles, camera networks, biometric databases, and command software require complex multi-vendor integration that routinely generates schedule delays and budget overruns in government procurement programmes.

The U.S. GAO has documented multiple CBP border technology programmes with slippages of 24–48 months and cost growth of 30% above original baselines, driven by the difficulty of connecting legacy sensors to new platforms without disrupting operational continuity.

These integration challenges suppress procurement velocity and raise total programme cost, limiting the addressable market in environments where cost overruns erode future capital allocations.

Civil Liberties and Privacy Rights Tensions Create Legal and Political Constraints on Biometric and Mass Surveillance Technology Deployment

The deployment of facial recognition systems, drone monitoring, and AI-powered behavioural analysis at national borders generates persistent legal challenges from civil liberties organizations, creating procurement delays and deployment restrictions in democratic nations.

The European Court of Human Rights has addressed member-state surveillance obligations under Article 8 of the European Convention on Human Rights, and the EU AI Act classifies certain border surveillance applications as high-risk, requiring extensive conformity assessments before deployment. These requirements add both cost and time to programme delivery, introducing compliance risk for vendors whose platforms include AI-driven biometric or behavioural analysis components.

Opportunities - Unmanned Aerial and Ground Vehicle Systems Are the Fastest-Growing Platform Category, Creating a Premium Border Surveillance Technology Opportunity

UAVs and autonomous ground vehicles provide persistent real-time coverage over border segments where fixed physical infrastructure is impractical, and patrol staffing is insufficient for continuous monitoring. CBP’s Air and Marine Operations (AMO) programme operates Predator B drones along the U.S. Mexico border, each delivering continuous multi-day surveillance over thousands of sq km using thermal and electro-optical sensor payloads.

Frontex’s EUROSUR framework is integrating UAV data from member-state assets and contracted platforms into a shared operational picture, creating growing demand for systems certified and configured specifically for border surveillance missions. This represents a high-value product opportunity for vendors with purpose-built border surveillance payload configurations and the certifications required for civil airspace operations.

Middle East & Africa's Infrastructure Investment Programs Are Creating Greenfield Border Security System Procurement Opportunities

GCC nations are modernizing border infrastructure as part of Vision-era national security commitments. Saudi Arabia’s Vision 2030 explicitly includes border security technology, and the UAE is deploying biometric, radar, and AI surveillance systems at airports and land checkpoints under its Smart Border initiative.

African nations backed by the African Union, U.S. AFRICOM, and EU border assistance missions are progressively formalizing land border management infrastructure on major cross-border smuggling and migration corridors.

These programmes represent a growing addressable market for vendors offering modular, compliant platforms adaptable to the infrastructure and budget constraints typical of emerging market procurement environments.

Category-wise Analysis

Platform Insights

Ground platform systems lead the border security market with approximately 62% market share in 2026. Land borders encompass 250,000+ km globally and represent the largest and most investment-intensive security challenge, dwarfing naval and aerial deployments in both scope and installed system density.

Ground systems span the broadest technology range: perimeter fencing with intrusion detection, ground-based surveillance radar, PTZ camera towers, biometric checkpoints, and vehicle-mounted patrol surveillance. Each generates distinct procurement events that collectively sustain the segment’s dominant revenue position.

Aerial platforms primarily surveillance UAVs are the fastest-growing platform category. Naval platforms serve coastline surveillance and maritime border monitoring, especially relevant for island nations and states with extensive coastlines.

Installation Insights

New installations lead the installation category with approximately 58% market share in 2026, driven by first-time deployments in Southeast Asia, Sub-Saharan Africa, and South Asia, where integrated border surveillance is being built for the first time under national security modernization programmes.

New installation contracts generate the highest per-programme values, covering greenfield infrastructure planning, system design, hardware procurement, and full integration. These contract structures attract Tier-1 defence and security primes including Elbit Systems, Thales, and Leonardo as prime integrators.

The upgradation segment approximately 42% of the market is driven by modernization of existing systems in mature markets, incorporating AI-powered analytics, higher-resolution sensors, and expanded connectivity into legacy surveillance infrastructure.

System Type Insights

Radar systems lead the system type segment with approximately 24% market share in 2026. Ground-based surveillance radar provides all-weather, day-and-night detection at 5–50 km range, enabling early warning of intruders, vehicles, and vessels before a perimeter breach occurs.

This performance capability makes radar the foundational first-layer investment in any serious border security programme the non-negotiable sensing layer that no other system type can replicate across the full diversity of border terrain environments.

Unmanned vehicles are the fastest-growing system type, propelled by their cost-effectiveness over fixed sensor towers, the persistent coverage capability of long-endurance platforms, and a growing range of sensor payloads built specifically for border surveillance missions.

Regional Analysis

North America Border Security System Market Trends & Analysis

North America is the world’s largest border security system market by revenue, anchored by the United States’ large-scale CBP investment along the southwestern land border, the northern border with Canada, and maritime approaches.

CBP’s annual budget exceeds USD 20 billion, with a dedicated capital stream sustaining consistent demand for radar, integrated fixed towers, UAV platforms, and biometric verification systems across successive administrations.

Canada’s CBSA is also investing in modernized port-of-entry and remote land border surveillance technology, complementing U.S. northern border investment programmes.

U.S. Border Security System Market Size

The United States commands approximately 83% of the North American market. CBP deploys Predator B UAVs, integrated fixed tower radar-camera systems, and advanced biometric systems across its 8,000+ km southern and northern border network.

The U.S. market grows at approximately 4.9% CAGR through 2033, with AI-powered video analytics upgrades, next-generation radar systems, and autonomous surveillance vehicle procurement sustaining above-baseline investment throughout the forecast period.

Europe Border Security System Market Trends, Drivers, & Insights

Europe is the world’s most regulation-intensive border security market, defined by Schengen external border obligations, Frontex’s expanding mandate, and the EUROSUR framework integrating member-state surveillance data into a common operational picture.

The Russia-Ukraine conflict has created unprecedented political will and emergency budget allocations for border technology in previously underfunded eastern EU states Poland, the Baltic states, and Finland generating new demand for ground radar, thermal cameras, and surveillance UAVs.

Germany Border Security System Market Size

Germany accounts for approximately 20% of the European market, as the EU’s largest economy and a primary Frontex contributor. Bundespolizei is investing in surveillance technology for its eastern EU border contributions and domestic critical crossing monitoring.

Germany’s domestic defence technology industrial base including Hensoldt and Thales Deutschland further amplifies the country’s market position. The segment grows at approximately 5.3% CAGR through 2033.

U.K. Border Security System Market Size

The UK represents approximately 17% of the European market. Home Office Border Force is investing in port-of-entry biometric systems, UK–France Channel migration surveillance, and coastal maritime radar networks.

Post-Brexit, the UK has also invested in autonomous border management technology to handle increased compliance documentation requirements for EU-UK goods crossings.

France Border Security System Market Size

France accounts for approximately 14% of the European market. Police aux Frontières and DGDDI are investing in surveillance across the Mediterranean coastline, Channel approaches, and Alpine border zones.

France’s LPM 2024–2030 defence programming law commits significant capital to national security infrastructure, including border and territory surveillance technology.

Asia Pacific Border Security System Market Drivers & Analysis

Asia Pacific is the fastest-growing regional border security market, driven by the world’s most active territorial disputes the South China Sea, the India-China-Pakistan Line of Actual Control, and North Korea’s border with South Korea.

The region’s rapidly expanding defence budgets, documented by SIPRI as among the world’s fastest-growing, are translating into multi-billion-dollar procurement programmes for radar, cameras, and unmanned systems.

India’s CIBMS programme and China’s advanced border surveillance system along contested frontiers represent two of the world’s largest active border security technology investments over the forecast period.

China Border Security System Market Size

China holds approximately 35% of the APAC border security market, operating the world’s most extensive programme across land borders with 14 countries and its maritime exclusive economic zone.

Domestic manufacturers CETC, Norinco, and Hikvision supply the majority of China’s border surveillance systems, with AI-powered cameras and biometric platforms at the frontier of national border management deployment. China’s segment grows at approximately 5.8% CAGR through 2033.

India Border Security System Market Size

India represents approximately 20% of the APAC market and is among the region’s fastest growing, at approximately 6.2% CAGR through 2033.

India’s CIBMS programme covers approximately 3,300 km of India-Pakistan and India-Bangladesh border segments, generating multi-year demand for integrated radar, ground sensors, thermal cameras, and C2 systems. BSF and ITBP modernization programmes supplement CIBMS for high-altitude and coastal segments.

Japan Border Security System Market Size

Japan accounts for approximately 12% of the APAC market. Japan Coast Guard and JMSDF are investing in maritime radar and UAV systems in response to Chinese and North Korean activity in Japan’s EEZ and territorial waters.

Japan’s National Security Strategy targets 2% of GDP defence spending, creating above-historical procurement momentum. Japan’s market grows at approximately 5.5% CAGR through 2033.

Competitive Landscape

The global border security system market is moderately consolidated at the prime integrator level. Elbit Systems, Thales Group, Leonardo S.p.A., L3Harris Technologies, Lockheed Martin, and Airbus Defence & Space collectively hold an estimated 35–40% of global revenue through national border security infrastructure programmes.

Their competitive advantages certified defence system architectures, government security clearances, and long-term programme management relationships are structural barriers that new entrants cannot quickly replicate.

Market leadership rewards scale, security clearance depth, and multi-domain integration capability. Strategic priorities across leading players include AI-driven autonomous detection, persistent UAV surveillance platforms, and biometric database integration.

Key Market Developments

- In March 2025, Elbit Systems was awarded a USD 150 million contract by a European NATO member for a multi-year integrated border surveillance system encompassing ground radar, thermal camera towers, and command and control software one of the largest European border security system awards of the year.

- In August 2024, Canadian border authorities introduced a new app designed to assist in tracking individuals who have been ordered to leave the country. The Canada Border Services Agency (CBSA) will use facial biometrics to verify identities and employ the app to monitor their locations.

- In October 2024, Thales Group delivered the first phase of India's CIBMS Laser Intrusion Detection System along the India-Pakistan border under a contract with India's Ministry of Home Affairs, marking a significant milestone in India's comprehensive integrated border management programme.

Companies Covered in Border Security System Market

- Elbit Systems Ltd.

- Thales Group

- L3Harris Technologies

- Lockheed Martin Corporation

- Leonardo S.p.A.

- Airbus Defence & Space

- Northrop Grumman Corporation

- Raytheon Technologies (RTX)

- General Dynamics Corporation

- Saab AB

- Hensoldt AG

- Israel Aerospace Industries (IAI)

- UFI Filters

Frequently Asked Questions

The global border security system market is valued at approximately US$ 46.7 billion in 2026. The market is projected to reach US$ 66.4 billion by 2033, expanding at a CAGR of 5.1% representing an incremental opportunity of US$ 19.7 billion driven by record global Défense budgets, migration surveillance investment, and geopolitical border security modernization programs.

The primary demand drivers are record-level global Défense spending with SIPRI reporting USD 2.44 trillion in 2023 military expenditure combined with unprecedented irregular migration pressure, evidenced by U.S. CBP's documentation of over 2.4 million southwestern border encounters in FY2023.

Radar Systems lead the system type segment with approximately 24% market share in 2025. Ground-based surveillance radar provides all-weather, day-and-night detection coverage of 5–50 kilometers a performance capability that establishes radar as the foundational first-layer investment in every comprehensive integrated border security architecture globally.

North America leads the global border security system market with approximately 40% revenue share in 2025. The United States commands approximately 83% of the North American market, underpinned by the U.S. CBP's annual budget exceeding USD 20 billion and sustained multi-program investment in Integrated Fixed Towers, Predator B UAV surveillance, biometric verification, and next-generation radar systems along the 8,000+ kilometer U.S. southern and northern border network.

The leading companies in the global border security system market include Elbit Systems, Thales Group, L3Harris Technologies, Lockheed Martin, Leonardo S.p.A., Airbus Defence & Space, Northrop Grumman, Raytheon Technologies (RTX), Saab AB, Hensoldt AG, and Israel Aerospace Industries (IAI).