- Technology

- Security Service Edge Market

Security Service Edge Market Size, Share, and Growth Forecast, 2026 - 2033

Security Service Edge Market by Component (Solutions, Services, Others), Deployment Mode (Cloud-based, Hybrid, Others), Organization Size, End-use Industry, and Regional Analysis for 2026 - 2033

Security Service Edge Market Size and Trends Analysis

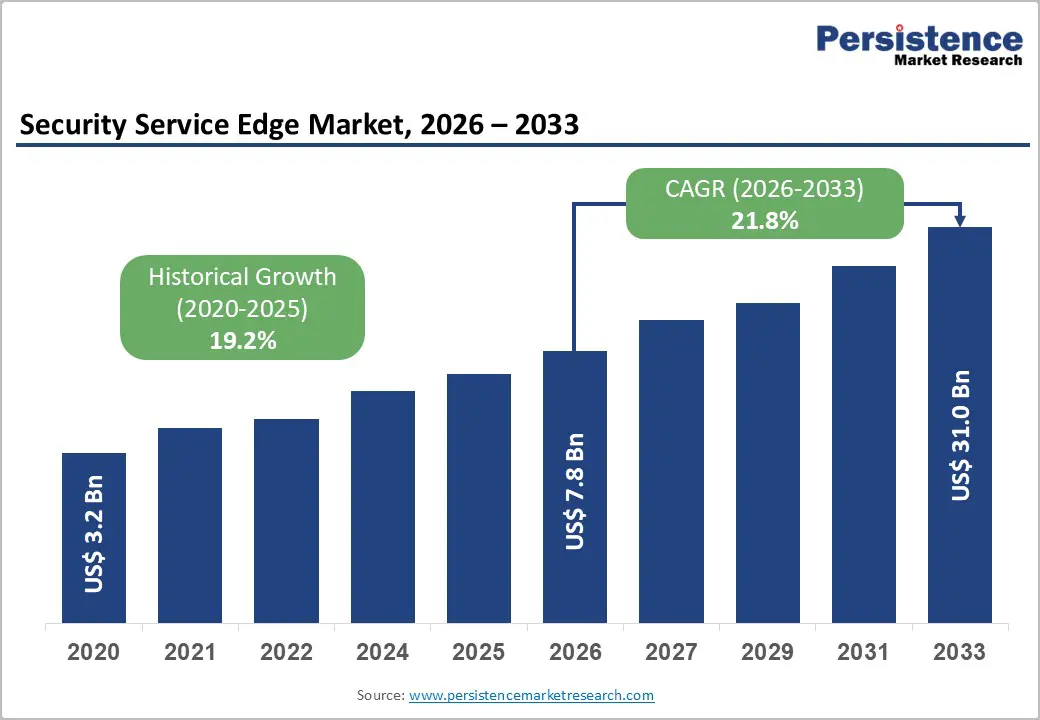

The global security service edge market size is likely to be valued at US$ 7.8 billion in 2026 and is expected to reach US$ 31.0 billion by 2033, growing at a CAGR of 21.8% between 2026 and 2033, driven by the rapid shift toward zero trust architectures, increasing cloud dependency, and the need to secure distributed workforces operating beyond traditional network perimeters.

Enterprises are replacing legacy perimeter-based models with identity-centric access control and cloud-delivered security frameworks.

Key Industry Highlights:

- Leading Region: North America is projected to account for approximately 37.4% of the market share in 2026, driven by advanced cloud adoption, strong regulatory frameworks, and the presence of major cybersecurity vendors.

- Fastest-growing Region: Asia Pacific is set to be the fastest-growing region, supported by rapid digital transformation, increasing cloud penetration, and evolving cybersecurity regulations across countries such as China, India, and Japan.

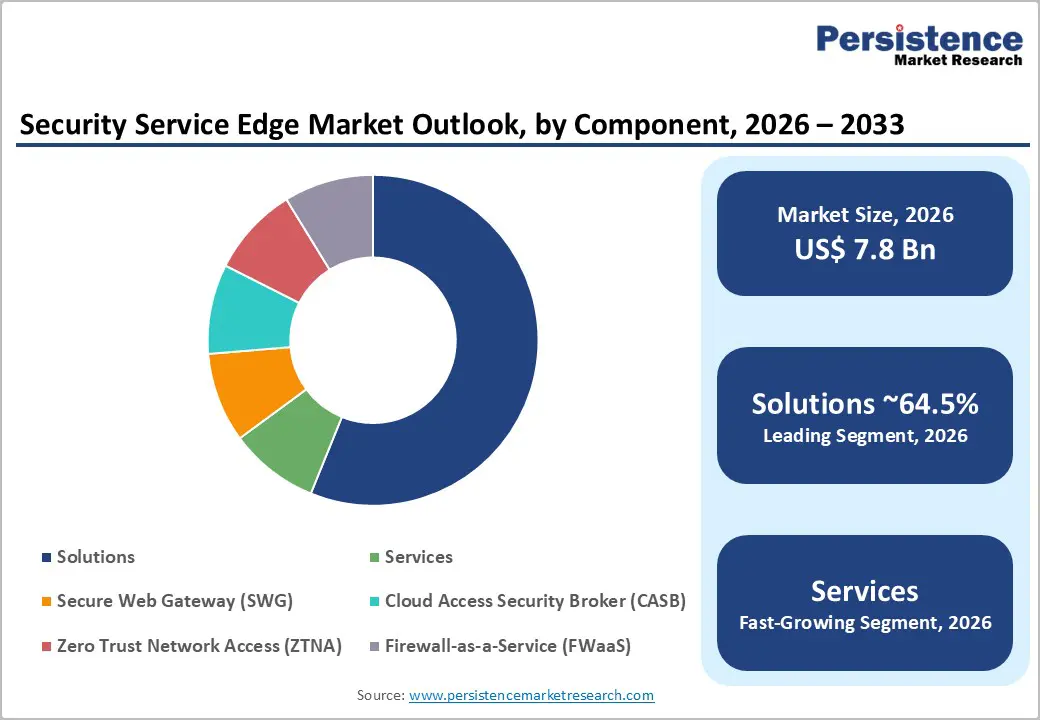

- Dominant Component: The solutions segment is expected to dominate, with an anticipated share of approximately 64.5% in 2026, as organizations prioritize integrated platforms that combine SWG, CASB, ZTNA, and FWaaS functionalities.

- Leading Deployment: The cloud-based deployment segment is expected to lead, accounting for approximately 55.7% of the market in 2026, driven by demand for scalable, centralized, and cloud-native security solutions across distributed enterprise environments.

DRO Analysis

Driver - Rising Zero Trust Adoption and Cloud Transformation Driving Core Demand

The increasing adoption of zero-trust security frameworks is fundamentally reshaping enterprise security investments. Organizations are moving away from perimeter-based models toward identity-driven architectures that verify every access request regardless of location. This shift aligns directly with SSE capabilities, which provide continuous authentication, granular access control, and centralized policy enforcement across cloud and on-premises environments.

Enterprise cloud adoption continues to accelerate, with more than half of businesses globally relying on paid cloud services and a growing proportion enabling remote access to critical applications. This expansion significantly increases the attack surface, requiring scalable and cloud-native security controls. Regulatory mandates, including cybersecurity directives in Europe and financial resilience frameworks, are further reinforcing adoption by requiring enhanced visibility, auditability, and third-party risk management. SSE is transitioning from an optional security upgrade to a foundational infrastructure component, particularly for organizations undergoing digital transformation and enabling hybrid work.

Escalating Cyber Threat Landscape and AI-Driven Security Requirements

The cybersecurity threat environment continues to evolve in complexity and scale, with enterprises facing advanced persistent threats, ransomware, and cloud-specific vulnerabilities. At the same time, the adoption of artificial intelligence and automation in enterprise workflows introduces new risk vectors, including data leakage, unauthorized access, and model exploitation.

SSE platforms are increasingly integrating AI-driven threat detection, behavioral analytics, and real-time policy enforcement to address these risks. Vendors are embedding advanced analytics into their platforms to provide continuous monitoring and adaptive security controls. This evolution allows enterprises to detect anomalies faster, enforce context-aware policies, and respond to threats in real time.

From a market perspective, the demand is shifting toward integrated, intelligence-driven security platforms that can deliver visibility and protection across users, applications, and data. This trend favors vendors with strong cloud infrastructure, global presence, and advanced analytics capabilities.

Restraint - Integration Complexity and Vendor Dependency Limiting Adoption Speed

Despite strong demand, the adoption of SSE is constrained by integration challenges and dependency on third-party vendors. Most enterprises operate heterogeneous IT environments that include legacy systems, on-premises infrastructure, multiple cloud platforms, and diverse security tools. Integrating SSE into such environments requires careful planning, migration strategies, and compatibility assessments.

Vendor dependency also introduces risks related to service continuity, data control, and regulatory compliance. In highly regulated industries, organizations must evaluate vendor reliability, geographic data handling practices, and alignment with regional cybersecurity laws. These factors increase procurement cycles and slow deployment timelines.

The restraint is structural rather than demand-driven. While enterprises recognize the value of SSE, the complexity of transitioning from fragmented security architectures to unified platforms remains a key barrier to rapid adoption.

Opportunity - Asia Pacific Emerging as a High-Growth Market with Regulatory Momentum

Asia Pacific represents the most significant growth opportunity for SSE providers, supported by rapid digitalization, expanding cloud adoption, and strengthening cybersecurity regulations. Countries such as China, India, Japan, and ASEAN members are investing heavily in digital infrastructure while simultaneously tightening data protection and cybersecurity requirements. Government-led initiatives to enhance cyber resilience, combined with greater enterprise awareness of cyber risks, are driving demand for advanced security solutions. Organizations in the region are prioritizing cloud-delivered security models that can scale efficiently and comply with evolving regulatory frameworks.

This environment creates strong opportunities for SSE vendors to expand their presence through localized solutions, regional partnerships, and infrastructure investments. The ability to balance global capabilities with local compliance requirements will be a critical success factor in this market.

SME Adoption and Managed Security Services Expanding Addressable Market

Small and medium-sized enterprises (SMEs) are emerging as a high-growth segment due to increasing cyber threats and limited in-house security capabilities. Unlike large enterprises, SMEs often lack the resources to manage complex security infrastructures, making cloud-delivered, subscription-based SSE solutions highly attractive. Managed security services play a crucial role in this segment by providing implementation support, continuous monitoring, and policy management. These services reduce operational complexity and enable SMEs to adopt enterprise-grade security without significant capital investment.

The opportunity lies in delivering simplified, scalable, and cost-effective solutions tailored to mid-market needs. Vendors that offer integrated platforms and managed services are well-positioned to capture this expanding customer base.

Category-wise Analysis

Component Insights

Solutions are expected to be the leading segment, accounting for approximately 64.5% of the market in 2026, as enterprises prioritize comprehensive platforms that integrate multiple security functions into a unified framework. These solutions address critical requirements, including secure access, data protection, and threat prevention across distributed environments. The consolidation of SWG, CASB, ZTNA, and FWaaS into single platforms enables organizations to streamline operations, reduce vendor complexity, and enhance policy consistency.

For instance, platforms from Zscaler and Netskope combine secure web access, private application access, and data protection within a single cloud-native architecture. Large enterprises and regulated industries, particularly BFSI and healthcare, are the primary adopters, driven by the need for centralized control, auditability, and compliance with stringent data protection regulations.

Services represent the fastest-growing segment, fueled by the need for seamless integration and continuous management of SSE environments. The complexity of modern IT infrastructures, combined with evolving threat landscapes, necessitates continuous monitoring and optimization. Managed services, consulting, and support offerings are becoming essential components of SSE adoption strategies.

For example, Cisco and Palo Alto Networks provide managed SSE and SASE services that help enterprises transition from legacy architectures to cloud-delivered security models. This trend is particularly pronounced among SMEs and organizations undergoing digital transformation, where internal expertise may be limited, and reliance on external service providers ensures faster and more secure implementation.

Deployment Mode Insights

Cloud-based deployments are expected to dominate the market, accounting for approximately 55.7% in 2026, reflecting SSE's inherent cloud-delivered security model. This approach enables organizations to enforce consistent policies across users and locations while reducing reliance on physical infrastructure.

Cloud deployment supports scalability, rapid implementation, and centralized management, making it the preferred choice for enterprises with distributed workforces and SaaS-heavy environments. For instance, Cloudflare leverages its global edge network to deliver secure access and traffic inspection close to users, while Zscaler enables direct-to-cloud connectivity without relying on traditional VPNs.

Hybrid deployment is likely to be the fastest-growing segment, as organizations adopt phased migration strategies. Hybrid models allow enterprises to retain certain on-premises controls while leveraging cloud-based security for broader coverage. This approach is particularly relevant for industries with strict regulatory requirements or latency-sensitive applications.

For example, Fortinet integrates on-premises firewalls with cloud-delivered SSE services, enabling organizations to maintain control over critical workloads while extending protection to remote users. Similarly, Check Point Software Technologies supports hybrid architectures that combine gateway-based security with cloud-managed policies. The ability to integrate legacy systems with modern cloud security frameworks positions hybrid deployment as a critical transitional strategy for large-scale enterprises.

Regional Insights

North America Security Service Edge Market Trends

North America is expected to lead the market, accounting for approximately 37.4% of market share in 2026, supported by advanced cloud adoption, strong cybersecurity awareness, and a mature technology ecosystem. The region is projected to grow at a CAGR of approximately 21.5%, reflecting sustained enterprise investment in zero trust and cloud-native security architectures.

U.S. Security Service Edge Market Trends

The U.S. dominates the regional landscape, accounting for the majority of North America’s revenue, supported by large-scale enterprise deployments and strong regulatory oversight. Federal initiatives promoting zero trust architectures have accelerated adoption across government agencies and critical infrastructure sectors. This policy environment has translated directly into enterprise procurement strategies.

Recent developments highlight the pace of innovation. Cisco partnered with AT&T in 2025 to deliver integrated SASE solutions, expanding SSE adoption through telecom-led distribution channels. At the same time, Zscaler introduced AI-driven security enhancements in 2025-2026, reinforcing the shift toward intelligent, cloud-native security platforms. These developments are strengthening the U.S. market by enabling enterprises to adopt scalable, integrated solutions with reduced operational complexity.

Canada Security Service Edge Market Trends

Canada is emerging as a steady-growth market, supported by increasing enterprise cloud adoption and public-sector digital transformation initiatives. Organizations are prioritizing secure access solutions to protect distributed workforces and sensitive data. Vendors such as Palo Alto Networks and Fortinet are expanding their presence through regional partnerships and managed service offerings.

The region benefits from strong alignment with North American cybersecurity standards, which facilitates cross-border technology adoption. Investment trends in Canada focus on hybrid deployment models and managed security services, particularly among mid-sized enterprises. This contributes to the broader regional trend of platform consolidation and cloud-first security strategies.

Overall, North America’s leadership is reinforced by continuous innovation, strong vendor presence, and regulatory alignment, making it the most mature SSE market globally.

Europe Security Service Edge Market Trends

Europe represents a significant market, characterized by strong regulatory frameworks and increasing cloud adoption. The region is expected to grow at a CAGR of approximately 20.9% through 2033, driven by compliance requirements and enterprise digital transformation.

Germany Security Service Edge Market Trends

Germany leads SSE adoption in continental Europe, driven by its strong industrial base and emphasis on cybersecurity in manufacturing and critical infrastructure. Enterprises are increasingly deploying SSE solutions to secure remote access for industrial operations and supply chain partners. Vendors such as Check Point Software Technologies and Fortinet are actively supporting these use cases through integrated network and cloud security platforms.

The country’s focus on compliance and data protection is accelerating the transition toward unified security architectures, particularly in sectors such as automotive and engineering.

U.K. Security Service Edge Market Trends

The U.K. is a key SSE market, supported by its strong financial services sector and advanced digital economy. Adoption is being driven by the need to secure remote access and ensure regulatory compliance. A notable development includes Palo Alto Networks collaborating with the U.K. Ministry of Justice in 2025 to enhance digital resilience using integrated security platforms.

This type of public-sector engagement demonstrates how SSE solutions are being deployed in high-compliance environments, reinforcing trust and accelerating adoption across other industries.

Asia Pacific Security Service Edge Market Trends

Asia Pacific is expected to be the fastest-growing SSE market, with a CAGR of approximately 22.8% over the forecast period, driven by rapid digital transformation, increasing cloud adoption, and evolving cybersecurity regulations.

China Security Service Edge Market Trends

China represents a significant SSE market, where adoption is heavily influenced by stringent cybersecurity and data protection regulations. Enterprises are prioritizing localized security solutions that comply with national data governance requirements.

Global vendors such as Fortinet and Cisco are adapting their offerings to align with regional regulations, while domestic providers are also strengthening their capabilities. This regulatory environment is shaping a market that emphasizes compliance, data localization, and hybrid deployment models.

Japan Security Service Edge Market Trends

Japan is characterized by a high demand for reliable and low-latency security solutions, driven by its advanced technological infrastructure and strong enterprise IT adoption. Organizations are increasingly adopting SSE platforms to secure remote work and cloud applications.

Companies such as Zscaler and Netskope have expanded their presence in Japan through partnerships and infrastructure investments, enabling improved performance and service delivery. This supports the country’s focus on secure digital transformation and operational efficiency.

Vendors such as Cloudflare and Cato Networks are expanding their regional footprint by establishing new points of presence and forming partnerships with local service providers. These developments improve network performance and accessibility, making SSE solutions more viable for a broader range of organizations. Southeast Asian countries are also witnessing increased adoption across sectors such as finance, e-commerce, and manufacturing. Organizations are leveraging SSE platforms to support digital transformation while addressing rising cyber threats.

Competitive Landscape

The global security service edge market is fragmented, with multiple global and regional players competing across different segments. Leading vendors differentiate themselves through platform capabilities, global infrastructure, and integration with broader security ecosystems. Competition is centered on innovation, scalability, and the ability to deliver unified security solutions.

Key strategies include platform consolidation, AI integration, and global expansion. Vendors are focusing on unified security architectures, strategic partnerships, and managed service offerings to differentiate their solutions and capture market share.

Key Industry Developments:

- In October 2025, Palo Alto Networks launched Cortex Cloud 2.0 and introduced new AI-driven security capabilities, including Prisma AIRS, to secure AI applications and strengthen cloud-delivered security platforms aligned with SSE architectures.

- In December 2025, Palo Alto Networks formed a strategic partnership with Google Cloud to help enterprises secure cloud and AI initiatives, reinforcing its position in cloud-delivered SSE and SASE ecosystems.

- In August 2025, Cisco partnered with AT&T to launch an integrated Secure Access Service Edge (SASE) solution, expanding enterprise access to cloud-delivered security services through telecom infrastructure.

Companies Covered in Security Service Edge Market

- Zscaler

- Palo Alto Networks

- Cisco

- Cloudflare

- Netskope

- Fortinet

- Check Point Software Technologies

- Broadcom

- Forcepoint

- Cato Networks

- Akamai Technologies

- Imperva

- Trellix

- McAfee Enterprise

- Symantec

- Versa Networks

Frequently Asked Questions

The global security service edge market is estimated to be valued at US$7.8 billion in 2026.

The security service edge market is expected to reach approximately US$31.0 billion by 2033.

Key trends include the adoption of zero trust architectures, consolidation of security functions (SWG, CASB, ZTNA, FWaaS) into unified platforms, and the growing integration of AI-driven threat detection and analytics.

The solutions segment is the leading component category, holding an anticipated share of 64.5%, as organizations prioritize integrated platforms for secure access, data protection, and threat prevention.

The security service edge market is projected to grow at a CAGR of 21.8% from 2026 to 2033.

Major players include Zscaler, Palo Alto Networks, Cisco, Cloudflare, and Netskope.