- Healthcare Services

- Bone Marrow Transplantation Market

Bone Marrow Transplantation Market Size, Share, and Growth Forecast 2026 - 2033

Bone Marrow Transplantation Market by Transplant Type (Autologous, Allogeneic, Syngeneic Transplants), Indication (Leukemia, Lymphoma, Myeloma, Aplastic Anemia, Others), End-user (Hospitals, Multispecialty Clinics, Ambulatory Surgical Centers, Cancer Research Institutes), and Regional Analysis, 2026 - 2033

Bone Marrow Transplantation Market Share and Trends Analysis

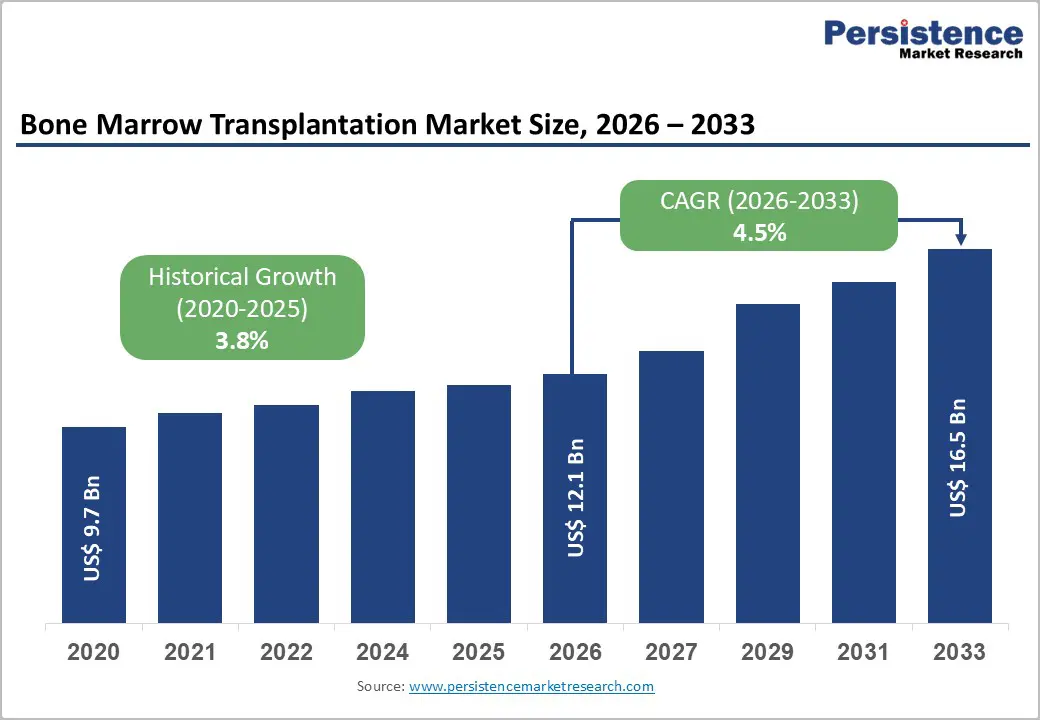

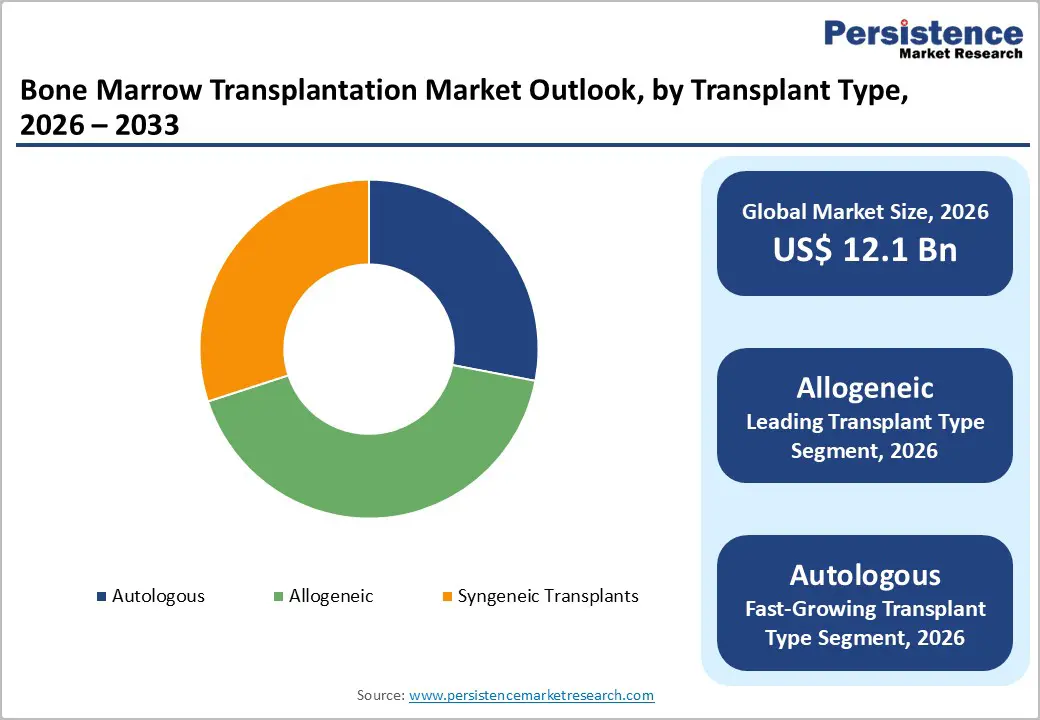

The global bone marrow transplantation market size is expected to be valued at US$ 12.1 billion in 2026 and projected to reach US$ 16.5 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033. This steady growth is primarily driven by the rising global incidence of hematological malignancies, expanding donor registries, and the increasing clinical adoption of haploidentical and cord blood transplantation techniques that have broadened the eligible patient population.

According to the World Health Organization (WHO), blood cancers, including leukemia, lymphoma, and myeloma collectively affect millions worldwide each year, generating sustained procedural demand. The market's expansion from US$ 9.7 billion in 2020 at a historical CAGR of 3.8% underscores the consistent growth trajectory, with accelerating innovation in graft-versus-host disease (GvHD) management and conditioning regimens expected to further strengthen the outlook through 2033.

Key Industry Highlights:

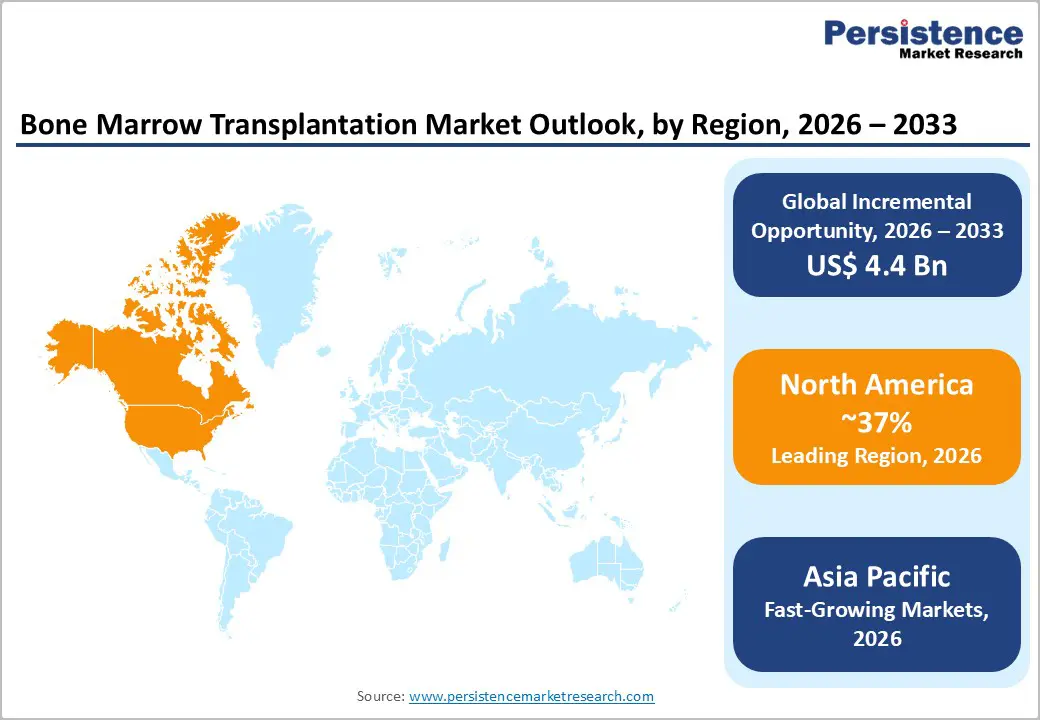

- Leading Region: North America dominates the global bone marrow transplantation market with 37% share in 2025, driven by over 22,000 annual U.S. HSCT procedures, world-renowned transplant centers, and comprehensive Medicare and private payer reimbursement frameworks.

- Fast-Growing Region: Asia Pacific is the fast-growing market led by China's 15,000+ annual transplants and India's rapidly expanding HSCT infrastructure at centers like Apollo Hospitals, supported by government registry development and rising medical tourism.

- Dominant Transplant Type: Allogeneic transplants lead with approximately 42% market share in 2025, underpinned by their curative potential across acute leukemias and aplastic anemia, supported by a 40 million+ global donor registry and advances in haploidentical transplantation protocols.

- Fast-Growing Transplant Type Segment: Autologous transplantation is the fastest-growing transplant type, driven by rising multiple myeloma incidence affecting 176,000 patients annually and the integration of novel induction agents improving pre-transplant remission depth and post-transplant outcomes.

Market Dynamics

Does the Rise in Global Incidence of Hematological Malignancies Propel Growth?

The growing burden of blood cancers constitutes the most powerful structural driver of bone marrow transplantation demand. The American Cancer Society estimates that over 186,000 new cases of leukemia, lymphoma, and myeloma will be diagnosed in the United States in 2024 alone. Globally, the International Agency for Research on Cancer (IARC) reported approximately 1.3 million new non-Hodgkin lymphoma and leukemia cases in 2022.

As hematopoietic stem cell transplantation (HSCT) remains one of the few potentially curative options for many of these conditions, increasing cancer incidence directly translates into elevated transplant volumes across major treatment centers worldwide, underpinning sustained market growth.

Does Expanding Unrelated Donor Registries Improve HLA Matching Technologies?

Access to matched unrelated donors has historically been the principal barrier to allogeneic transplantation. However, global bone marrow registry expansion is substantially improving match rates. The World Marrow Donor Association (WMDA) reports that the global stem cell donor pool has surpassed 40 million registered donors and cord blood units across member registries worldwide. Advances in next-generation sequencing (NGS)-based HLA typing have improved allele-level matching resolution, reducing transplant-related mortality. In parallel, the clinical validation of haploidentical transplantation using half-matched family donors has dramatically expanded donor availability, with post-transplant cyclophosphamide (PTCy) protocols achieving outcomes comparable to those of matched unrelated donors, thereby opening transplant eligibility to previously excluded patient populations.

Do the High Procedural Cost Limits Healthcare Access in Emerging Economies?

Bone marrow transplantation remains among the most expensive medical procedures globally, with total treatment costs in the United States ranging from US$ 100,000 to over US$ 300,000 depending on transplant type and post-procedure care. Allogeneic transplants typically exceed autologous procedures in cost due to extended hospitalization, immunosuppression, and GvHD management requirements. In low- and middle-income countries, where hematological malignancy burdens are increasing, limited insurance coverage and underdeveloped transplant infrastructure constrain procedural access, creating a significant disparity between disease prevalence and treatment uptake.

Risk of Graft-Vs-Host Disease (GvHD) and Treatment-Related Mortality

Graft-versus-host disease remains a serious complication of allogeneic transplantation, affecting up to 50% of recipients in its acute form and representing a leading cause of transplant-related mortality and morbidity. According to the National Bone Marrow Transplant Link, chronic GvHD affects approximately 30–70% of long-term allogeneic transplant survivors, significantly impacting quality of life and long-term outcomes. The complexity of managing GvHD requires specialized multidisciplinary teams and contributes to extended inpatient stays, increasing the total cost burden and deterring referrals to transplantation in cases where alternative therapies exist.

How do the Advancements in Multiple Myeloma Treatment Drive Autologous Transplantation Growth?

Autologous hematopoietic stem cell transplantation (auto-HSCT) is experiencing renewed growth momentum, particularly in multiple myeloma treatment protocols. The International Myeloma Foundation (IMF) reports that multiple myeloma affects over 176,000 people annually worldwide, with incidence rising in aging populations. Auto-HSCT remains the standard of care consolidation strategy for transplant-eligible myeloma patients following induction therapy. The integration of novel agents, including proteasome inhibitors, immunomodulatory drugs, and anti-CD38 monoclonal antibodies as pre-transplant induction, is improving the depth of remission and post-transplant outcomes. Investigational tandem transplant approaches and combination strategies with CAR-T therapies represent an expanding clinical frontier that is expected to sustain and amplify auto-HSCT volumes through the forecast period.

How do Expansions in Emerging Markets and Medical Tourism in the Asia Pacific Pump Novel Opportunities?

Asia Pacific presents a transformational market opportunity, with rapidly developing transplant infrastructure in India, China, South Korea, and Thailand, attracting both domestic patients and international medical tourists. India's National Health Policy and initiatives under the Ayushman Bharat scheme are expanding oncology care access to economically disadvantaged populations, while JCI-accredited centers such as Apollo Hospitals offer internationally competitive transplant programs at a fraction of Western costs. The Asia Pacific Blood and Marrow Transplantation Group (APBMT) has reported a consistent year-on-year increase in HSCT activity across the region, with over 20,000 annual transplants now performed. Government investment in cord blood banking and donor registry expansion across the region is further enabling broader allogeneic transplant access.

Category-wise Analysis

Transplant Type Insights

Allogeneic transplants represent the leading segment within the transplant type category, commanding approximately 42% of global market share in 2025. This dominance is attributable to the curative potential of allogeneic HSCT across a broader spectrum of hematological conditions including acute leukemias, myelodysplastic syndromes, and aplastic anemia, where the graft-versus-tumor effect provides a therapeutic advantage beyond simple hematopoietic reconstitution. The Center for International Blood and Marrow Transplant Research (CIBMTR) reports that allogeneic transplant volumes in North America have grown steadily, with over 9,000 allogeneic procedures performed annually in the United States. Expanding haploidentical platforms and reduced-intensity conditioning regimens have extended eligibility to older patients, further reinforcing the segment's leading position.

Indication Insights

Leukemia represents the dominant indication segment, accounting for approximately 38% of global bone marrow transplantation market share in 2025. Acute myeloid leukemia (AML) and acute lymphoblastic leukemia (ALL) together constitute the primary indications for allogeneic HSCT, as transplantation offers the most viable curative pathway for high-risk and relapsed/refractory disease. According to the Leukemia & Lymphoma Society (LLS), leukemia represents the most common blood cancer in children and one of the top five most frequent cancers in adults in the United States, ensuring a large and sustained transplant-eligible patient population. Ongoing advances in minimal residual disease (MRD) monitoring and targeted conditioning are improving leukemia transplant outcomes, further solidifying the indication's market leadership.

End-user Insights

Hospitals dominate the end-user landscape for bone marrow transplantation, representing approximately 60% of total global market share in 2025. Tertiary care and academic medical centers serve as the primary sites for HSCT procedures, given the requirement for specialized bone marrow transplant units, dedicated negative-pressure isolation rooms, and multi-disciplinary teams encompassing hematologists, infectious disease specialists, and transplant nurses. Major transplant centers—including Dana-Farber Cancer Institute, MD Anderson Cancer Center, and Fred Hutchinson Cancer Center—perform hundreds of procedures annually and lead clinical trials advancing transplant protocols. The Joint Accreditation Committee ISCT-Europe & EBMT (JACIE) accreditation framework ensures that hospital-based programs maintain internationally standardized quality benchmarks, further reinforcing hospital segment dominance.

Regional Insights

North America Bone Marrow Transplantation Market Trends and Insights

North America leads the global bone marrow transplantation market with approximately 37% of revenue share in 2025, underpinned by a high concentration of FACT- and JACIE-accredited transplant centers, comprehensive insurance coverage for HSCT under Medicare and private payers, and the presence of leading research institutions driving clinical protocol innovation. Increasing adoption of outpatient and reduced-toxicity conditioning regimens is expanding procedural volumes.

U.S. Bone Marrow Transplantation Market Size

The United States accounts for over 85% of the North American market. With over 22,000 HSCT procedures performed annually according to the CIBMTR, and the presence of world-renowned centers such as Memorial Sloan Kettering, City of Hope, and Cleveland Clinic, the U.S. market demonstrates consistently high procedural volumes supported by robust NIH-funded clinical research programs.

Europe Bone Marrow Transplantation Market Trends and Insights

Europe is the second-largest regional market, benefiting from a well-established transplant network coordinated by the European Bone Marrow Transplantation (EBMT) registry the world's largest HSCT outcomes database with data from over 700 transplant centers. Universal healthcare systems across major European economies ensure patient access, while pan-European clinical trial networks and the EBMT Annual Congress drive continuous protocol refinement and standardization across member countries.

Germany Bone Marrow Transplantation Market Size

Germany is the largest European market for bone marrow transplantation, representing approximately 20% of regional revenue. The Deutsche Knochenmarkspenderdatei (DKMS), headquartered in Tübingen, is the world's largest stem cell donor registry with over 10 million registered donors, giving German transplant centers unparalleled donor access and reinforcing the country's market leadership.

U.K. Bone Marrow Transplantation Market Size

The United Kingdom contributes approximately 13% of European BMT market revenue. NHS England funds HSCT as a commissioned specialized service, ensuring nationally consistent access. The Anthony Nolan registry with over 800,000 donors and the British Society of Blood and Marrow Transplantation (BSBMT) network support robust annual transplant activity across leading UK centers.

Asia Pacific Bone Marrow Transplantation Market Trends and Insights

Asia Pacific is the fastest-growing regional market, driven by rapidly expanding transplant infrastructure, increasing cancer awareness, and government initiatives to develop national donor registries. China has emerged as the second-largest HSCT market globally by volume, with over 15,000 annual procedures reported by the Chinese Hematopoietic Stem Cell Transplantation Group. Regional growth is further supported by medical tourism corridors across Southeast Asia.

India Bone Marrow Transplantation Market Size

India holds approximately 10% of the Asia Pacific bone marrow transplantation market. Annual HSCT volumes have grown to over 2,500 procedures, driven by centers such as Apollo Hospitals and Tata Memorial Centre. The DATRI Blood Stem Cell Donors Registry and government initiatives under the National Health Mission are improving donor access and affordability for economically disadvantaged patients.

Competitive Landscape

The global bone marrow transplantation market is moderately concentrated among leading academic medical centers and specialized cancer institutes, with the top institutions collectively accounting for a significant share of global transplant volumes. Key competitive differentiators include JACIE/FACT accreditation status, outcomes data transparency, clinical trial pipeline depth, and donor registry access. Strategic trends include the development of dedicated outpatient transplant programs to reduce costs, integration of CAR-T cell therapy suites alongside transplant units, and cross-border telemedicine consultation models. Emerging business model trends encompass value-based care contracts with insurers linking reimbursement to one-year post-transplant survival outcomes.

Key Developments

- In March 2025, Zydus Lifesciences introduced ANVIMO (Letermovir), a novel and advanced therapy designed to prevent Cytomegalovirus (CMV) infections in patients undergoing hematopoietic stem cell transplants (HSCT) and kidney transplants.

- In June 2024, Apollo Cancer Centres (ACC), Hyderabad, launched the first Outpatient Bone Marrow Transplant (BMT) service in Andhra Pradesh and Telangana, marking a significant advancement in the treatment of lymphoma, multiple myeloma, and other hematologic conditions. This service provided patients with the life-saving benefits of bone marrow transplantation while significantly reducing the need for extended hospital stays and cutting treatment costs by 50 percent.

Global Bone Marrow Transplantation Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 9.7 billion |

|

Current Market Value (2026) |

US$ 12.1 billion |

|

Projected Market Value (2033) |

US$ 16.5 billion |

|

CAGR (2026–2033) |

4.5% |

|

Leading Region |

North America, 37% market share (2025) |

|

Dominant Category (Transplant Type) |

Allogeneic Transplants, ~42% market share (2025) |

|

Top-ranking Category (Indication) |

Leukemia, ~38% market share (2025) |

|

Incremental Opportunity (2026–2033) |

US$ 4.4 billion |

Companies Covered in Bone Marrow Transplantation Market

- Dana-Farber Cancer Institute

- MD Anderson Cancer Center

- Fred Hutchinson Cancer Center

- City of Hope National Medical Center

- Memorial Sloan Kettering Cancer Center

- Cleveland Clinic

- Apollo Hospitals

- King Faisal Specialist Hospital & Research Centre

- Singapore General Hospital

- Zydus Lifesciences

Frequently Asked Questions

The global bone marrow transplantation market size is valued at US$ 12.1 billion in 2026.

The primary drivers are the rising global incidence of hematological cancers, with over 1.3 million new leukemia and lymphoma cases reported by IARC in 2022 alongside a global donor registry surpassing 40 million registered donors (WMDA).

North America is the leading region with approximately 37% of global market share in 2025.

The most significant growth opportunity lies in Asia Pacific's rapidly developing transplant infrastructure and the concurrent expansion of autologous HSCT for multiple myeloma. With the APBMT recording over 20,000 annual transplants across the region and India's Ayushman Bharat scheme extending oncology coverage to millions, market participants with an established regional presence and cost-competitive transplant programs are best positioned to capture this incremental demand through 2033.

The bone marrow transplantation market is led by specialized academic medical centers and cancer institutes, including Dana-Farber Cancer Institute, MD Anderson Cancer Center, Fred Hutchinson Cancer Center, City of Hope National Medical Center, Memorial Sloan Kettering Cancer Center, Cleveland Clinic, Apollo Hospitals, King Faisal Specialist Hospital & Research Centre, and Singapore General Hospital. These institutions compete on outcomes data, accreditation standards, clinical trial depth, and donor registry access.