- Healthcare Services

- Acupuncture Treatment Market

Acupuncture Treatment Market Size, Share, and Growth Forecast, 2026 - 2033

Acupuncture Treatment Market by Service Type (Needle Acupuncture, Electro-acupuncture, Others), Application (Musculoskeletal Conditions, Fatigue & CNS Conditions, Others), End-user (Hospitals, Wellness Centers, Clinics), and Regional Analysis for 2026 - 2033

Acupuncture Treatment Market Size and Trends Analysis

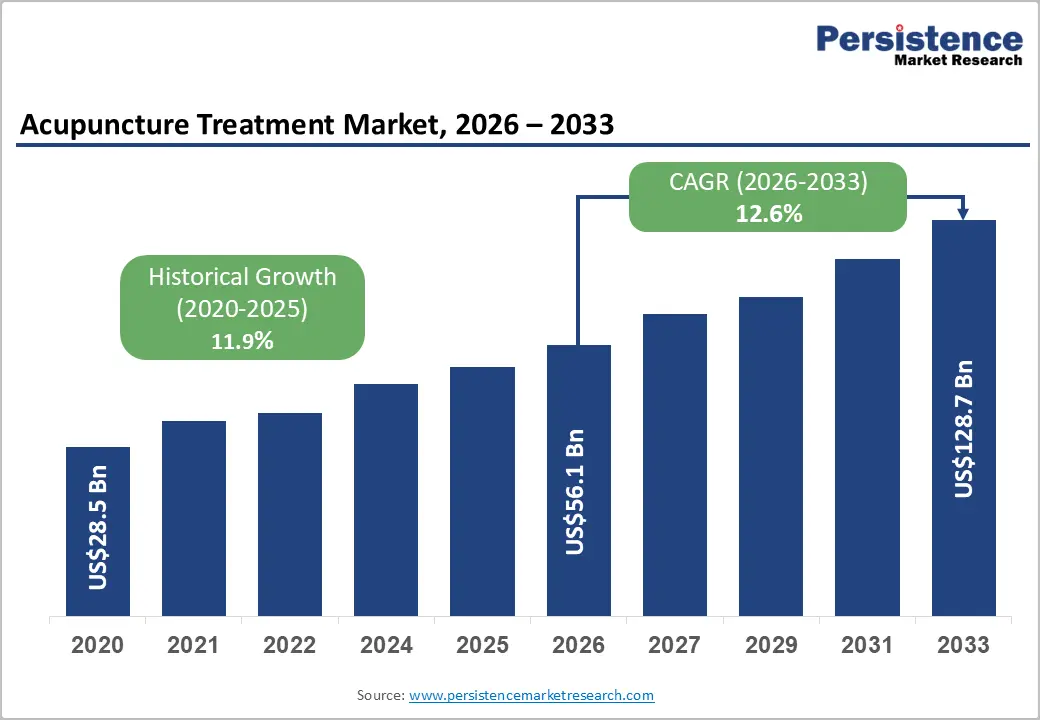

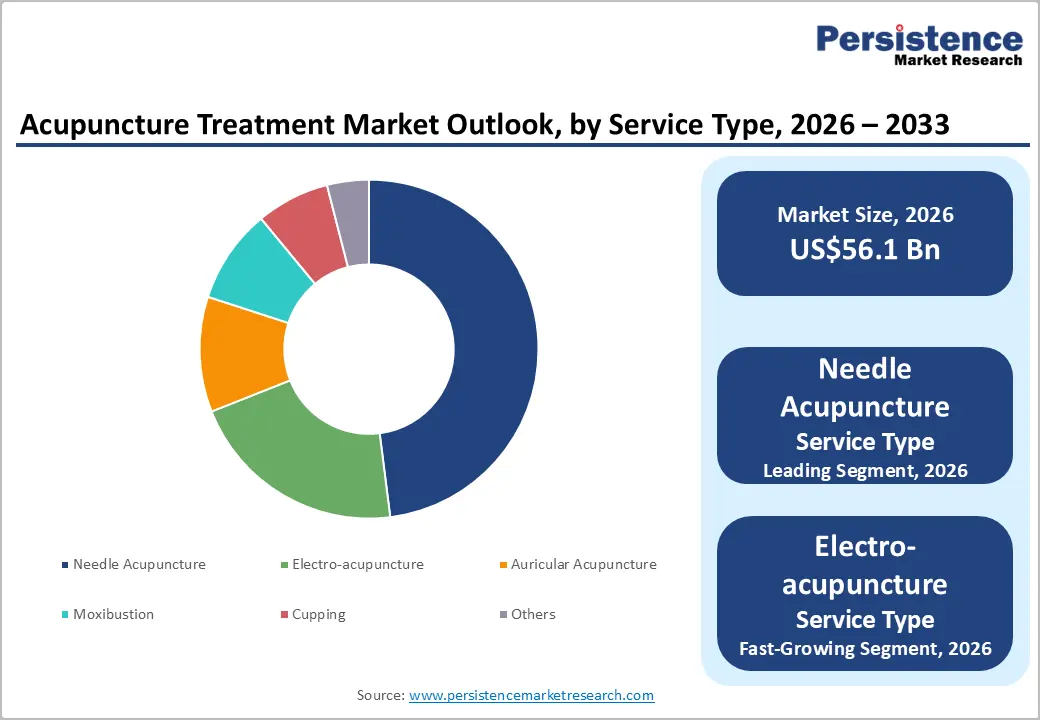

The global acupuncture treatment market size is likely to be valued at US$56.1 billion in 2026, and is expected to reach US$128.7 billion by 2033, growing at a CAGR of 12.6% during the forecast period from 2026 to 2033, driven by the rising prevalence of chronic pain, stress-related disorders, musculoskeletal conditions, and growing demand for non-pharmacological therapies.

Increasing acceptance of integrative and holistic healthcare practices, along with supportive reimbursement policies in several countries, is further accelerating adoption. The expansion of electroacupuncture therapies, integration of digital health technologies such as telehealth and wearable stimulation devices, and rising incorporation of acupuncture into wellness centers, rehabilitation facilities, and hospital-based integrative medicine programs.

Key Industry Highlights:

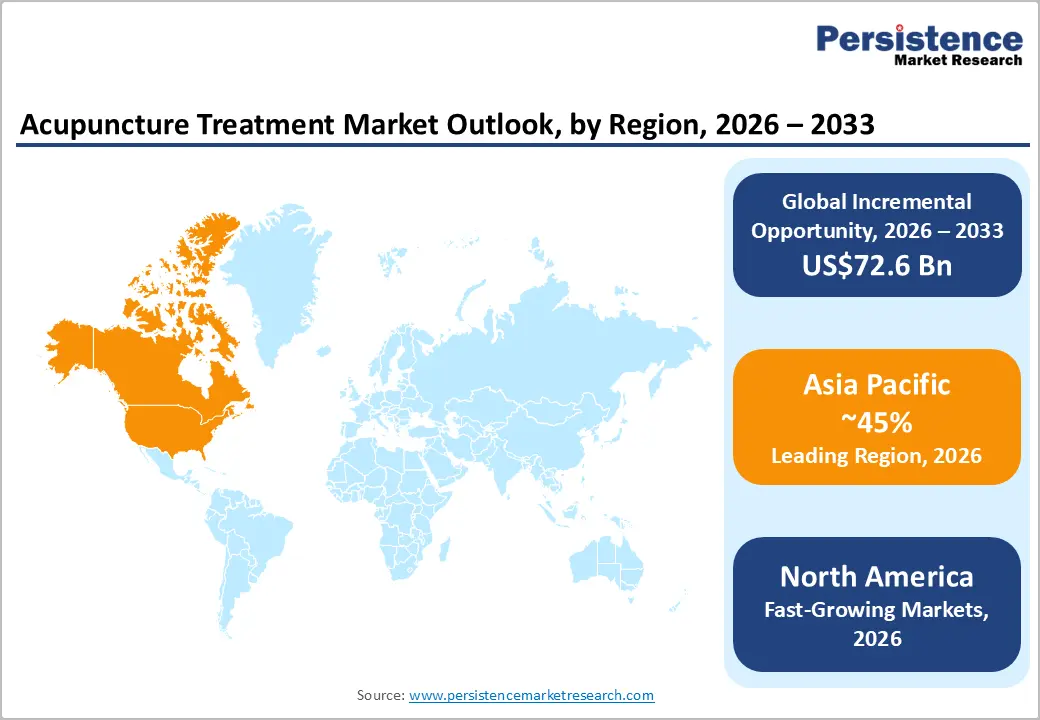

- Dominant Region: Asia Pacific is expected to dominate the market with an estimated 45% revenue share in 2026, anchored by China's millennia-long TCM cultural integration, government-mandated TCM service provision within national healthcare systems, and the world's highest density of licensed acupuncture practitioners.

- Fastest-growing Region: North America is likely to be the fastest-growing regional market, fueled by expanding insurance coverage, surging chronic pain patient volumes, and growing integrative medicine adoption across hospital and outpatient clinical settings.

- Leading Service Type: Needle acupuncture is anticipated to dominate with approximately 48% share in 2026, reflecting its foundational clinical role, broadest evidence base across therapeutic indications, and universal deployment across all acupuncture practice settings globally.

- Dominant Application: Musculoskeletal conditions are anticipated to dominate, accounting for approximately 38% of market value in 2026, driven by the enormous global burden of chronic back pain, osteoarthritis, neck pain, and sports injuries, generating consistent high-volume treatment demand.

DRO Analysis

Driver - Global Integrative Medicine Movement and Expanding Regulatory Recognition

The global shift toward integrative and preventive healthcare, combining evidence-based conventional medicine with validated complementary therapies, including acupuncture, is driving structural market expansion across North America, Europe, and Asia Pacific. The WHO's Traditional Medicine Strategy 2025 explicitly advocates for the integration of traditional medicine, including acupuncture, into national health systems, a policy framework that has influenced regulatory recognition, insurance coverage expansion, and practitioner licensing developments across WHO member states.

In Europe, national health systems, including the German GKV statutory health insurance, which covers acupuncture for chronic low back pain and knee osteoarthritis, and NHS England's partial coverage through GP referral pathways, are creating reimbursement-supported demand that significantly expands acupuncture's addressable patient population beyond out-of-pocket self-pay markets.

Restraint - Inconsistent Regulatory Standards and Practitioner Licensing Frameworks

One of the most significant structural barriers constraining the acupuncture treatment market's growth potential is the pronounced inconsistency in practitioner licensing, scope-of-practice regulations, and quality assurance frameworks across different countries and sub-national jurisdictions. In the U.S., acupuncture licensing is regulated at the state level, with 47 states and the District of Columbia requiring licensure, but standards vary considerably in educational hours required, scope of practice boundaries, and continuing education mandates.

The lack of harmonized international standards for acupuncture practice creates barriers to cross-border practitioner mobility, complicates international clinical research collaboration, and impedes the development of consistent clinical quality metrics that third-party payers require to underpin reimbursement decisions.

Opportunity - Digital Health Integration and Teleacupuncture-Assisted Remote Services

The integration of digital health technologies with acupuncture practice is creating a strong market expansion opportunity by improving accessibility and convenience for patients. Telehealth consultation platforms, AI-powered acupoint identification applications, wearable electro-acupuncture devices, and remote patient monitoring tools are enabling acupuncture services to extend beyond traditional in-person clinic settings. The COVID-19 pandemic further accelerated global telehealth adoption, while temporary reimbursement support from agencies such as the Centers for Medicare & Medicaid Services encouraged both practitioners and patients to adopt remote healthcare delivery models.

Wearable electro-acupuncture devices, including consumer-grade transcutaneous electrical nerve stimulation (TENS) systems designed for acupoint therapy, are also expanding the market into the at-home wellness segment. Companies developing smartphone-connected stimulation devices are positioning themselves at the intersection of acupuncture and wearable health technology, attracting health-conscious consumers seeking convenient pain management and wellness solutions.

Category-wise Analysis

Service Type Insights

Needle acupuncture is projected to dominate the market, accounting for an estimated 48% share of the total revenue in 2026. Its market leadership reflects its foundational clinical role as the definitive acupuncture modality supported by the broadest body of randomized controlled trial evidence across musculoskeletal, neurological, and chronic pain indications and its universal deployment as the core service offering of licensed acupuncture practitioners across all practice settings globally. Kaiser Permanente incorporated needle acupuncture into its integrative pain management programs for chronic low back pain and musculoskeletal disorders.

Electro-acupuncture is likely to be the fastest-growing service type. Electro-acupuncture combines traditional needle insertion with controlled electrical stimulation to enhance therapeutic effectiveness, particularly for chronic pain, neurological disorders, and rehabilitation therapies. Its ability to deliver measurable and consistent treatment outcomes is driving growing adoption across hospitals, rehabilitation centers, and sports medicine clinics. ITO Physiotherapy & Rehabilitation developed the ES-160 electro-acupuncture system, which is widely used in rehabilitation and pain management settings for chronic pain, neurological disorders, and muscle recovery therapies

Application Insights

Musculoskeletal conditions are anticipated to dominate the application segment, accounting for an estimated 38% of the total revenue in 2026. The segment's leadership reflects the enormous global burden of chronic back pain, osteoarthritis, neck pain, shoulder disorders, and sports-related musculoskeletal injury conditions for which acupuncture has the most extensive clinical trial evidence base and the strongest third-party payer reimbursement coverage across major markets. Mayo Clinic uses acupuncture within its integrative medicine programs for managing chronic back pain, osteoarthritis, neck pain, and other musculoskeletal disorders.

Fatigue & CNS conditions represent the fastest-growing application segment. Post-COVID fatigue syndrome (Long COVID), burnout, anxiety, insomnia, and stress-related cognitive dysfunction are driving a wave of patient demand for acupuncture as a non-pharmacological neurological and psychological health support modality.

Acupuncture practitioners with CNS and fatigue specialty expertise are experiencing significant demand growth in post-pandemic clinical environments across North America, Europe, and East Asia. Mount Sinai Health System incorporated acupuncture into its post-COVID care programs to help manage fatigue, anxiety, insomnia, and stress-related symptoms associated with Long COVID.

End-user Insights

Clinics are estimated to dominate the end-user segment of the acupuncture treatment market, capturing approximately 52% of the market share in 2026. Dedicated acupuncture clinics ranging from solo practitioner practices to multi-practitioner integrative medicine centers offer the highest treatment volume throughput, practitioner specialization depth, and treatment environment optimization of any end-user setting. Modern Acupuncture operates a large network of dedicated acupuncture clinics across the U.S., offering standardized acupuncture treatments focused on pain management, stress relief, and wellness care.

Wellness centers represent the fastest-growing end-user segment. The integration of acupuncture into premium wellness and spa facilities, including hotel wellness centers, corporate wellness facilities, and dedicated holistic health centers, is creating new service delivery channels that capture consumer wellness spending from populations who may not have engaged with acupuncture through traditional clinical pathways. Canyon Ranch, a leading wellness resort and integrative health company in the U.S., which provides acupuncture within personalized wellness and corporate health programs.

Regional Insights

North America Acupuncture Treatment Market Trends

North America is likely to be the fastest-growing major regional acupuncture treatment market in 2026. The U.S. market growth is driven by expanding insurance reimbursement mandates, surging chronic pain patient volumes amidst the opioid crisis, growing mainstream healthcare system integration of integrative medicine programs, and rising consumer health awareness among wellness-focused millennial and Gen Z demographics.

U.S. Acupuncture Treatment Market Insights

The U.S. acupuncture market is experiencing structural demand acceleration driven by multiple concurrent policy and clinical practice forces. The VA's Whole Health program, which integrates acupuncture as a core non-pharmacological pain management modality across VA healthcare networks serving approximately 9 million veteran patients, has created one of the world's largest institutionally mandated acupuncture service delivery programs.

Canada Acupuncture Treatment Market Insights

Canada demonstrates strong acupuncture market development, particularly in British Columbia, Ontario, and Alberta, supported by well-established regulatory frameworks for licensed acupuncture practitioners. The College of Traditional Chinese Medicine Practitioners and Acupuncturists of British Columbia (CTCMA) and equivalent Ontario regulatory bodies maintain structured practitioner licensing standards that support professional market development.

Europe Acupuncture Treatment Market Trends

Europe shows steady growth, driven by national health system integration programs, robust complementary medicine regulatory frameworks in Germany, the U.K., and the Netherlands, and strong consumer acceptance of complementary healthcare modalities across Western European societies.

Germany Acupuncture Treatment Market Trends

Germany is the leading European acupuncture market, driven by the GKV statutory health insurance system's coverage of acupuncture for chronic low back pain and knee osteoarthritis, two of the highest-prevalence musculoskeletal conditions generating acupuncture treatment demand in Germany's aging population. The German Medical Acupuncture Association (DAÄM) and the German Academy of Acupuncture maintain rigorous physician acupuncture training standards, supporting high-quality clinical service delivery across hospital, outpatient, and specialist practice settings.

U.K. Acupuncture Treatment Market Trends

The U.K. acupuncture market is shaped by the British Acupuncture Council (BAcC), which represents approximately 3,000 professionally qualified acupuncturists, and the integration of acupuncture within NHS pain management and oncology support service pathways at select NHS trusts. NICE guidance acknowledges acupuncture for chronic primary pain and some headache conditions, providing an NHS commissioning foundation that sustains structured referral demand beyond purely private-pay market dynamics.

Asia Pacific Acupuncture Treatment Market Trends

Asia Pacific is projected to dominate, holding approximately 45% of total revenue in 2026. The region benefits from deep cultural integration of acupuncture within traditional medicine systems across China, Japan, South Korea, and Vietnam, combined with government-mandated TCM service provision in several major economies and the world's highest practitioner density, creating both the highest absolute treatment volumes and the most institutionally embedded demand structures in the global acupuncture market.

China Acupuncture Treatment Market Trends

China is projected to dominate the Asia Pacific market and remain the largest national acupuncture treatment market globally. Growth is supported by the Chinese government’s strong promotion of Traditional Chinese Medicine (TCM) through policies such as the Traditional Chinese Medicine Law (2017) and the Healthy China 2030 Initiative, which encourage the integration and availability of TCM services, including acupuncture, across tertiary hospitals, community health centers, and rural healthcare facilities throughout the country.

India Acupuncture Treatment Market Trends

India represents one of the highest-growth acupuncture treatment markets in Asia Pacific, driven by growing consumer acceptance of evidence-based alternative therapies, the Central Council for Research in Yoga and Naturopathy (CCRYN) and Ministry of AYUSH frameworks that include acupuncture within India's complementary and integrative medicine regulatory landscape, and the country's large chronic musculoskeletal pain patient population.

Competitive Landscape

The global acupuncture treatment market features a highly fragmented competitive landscape reflecting the professional services nature of acupuncture practice, which distributes market participation across hundreds of thousands of individual practitioners, single-location clinics, and multi-location integrative medicine groups rather than concentrating it among a small number of large corporate entities as in medical device or pharmaceutical markets.

TCM Australia operates as one of the largest organized TCM and acupuncture practitioner networks in the Asia Pacific region outside mainland China, offering training, professional membership, and clinical practice support infrastructure to licensed acupuncture practitioners across Australian states and territories.

PRTCM (Professional Register of Traditional Chinese Medicine, Ireland), NZCMAS (New Zealand Chinese Medicine and Acupuncture Society), and ETCMA (European Traditional Chinese Medicine Association, U.K.) represent the professional association model, which shapes market standards, practitioner credentialing, public awareness, and policy advocacy in their respective markets without directly operating patient-facing clinical services.

Key Industry Developments:

- In March 2024, TCM Australia launched a national corporate wellness acupuncture program, partnering with three major Australian employers in the mining, financial services, and logistics sectors to deliver on-site workplace acupuncture services targeting musculoskeletal injury prevention and stress management for approximately 12,000 combined employees.

Companies Covered in Acupuncture Treatment Market

- TCM Australia

- Jingshen TMC Clinic, U.K.

- ACTCM, U.S.

- PRTCM, Ireland

- NZCMAS, New Zealand

- ChinaMed Charlottesville

- ATCM, U.K.

- Beijing Acupuncture and Herbal Clinic

- ETCMA, U.K.

- Flow Acupuncture & Osteopathy

Frequently Asked Questions

The global acupuncture treatment market is projected to reach US$56.1 billion in 2026.

The increasing prevalence of chronic pain, stress-related disorders, and musculoskeletal conditions is driving demand for acupuncture as a non-pharmacological treatment option.

The acupuncture treatment market is poised to witness a CAGR of 12.6% from 2026 to 2033.

The integration of digital health technologies, including telehealth platforms and wearable electro-acupuncture devices, is creating significant market expansion opportunities.

Key players include TCM Australia, Jingshen TMC Clinic, ACTCM, PRTCM, NZCMAS, ChinaMed Charlottesville, ATCM, Beijing Acupuncture and Herbal Clinic, ETCMA, and Flow Acupuncture & Osteopathy.