- Food Ingredients & Additives

- Aquafaba Market

Aquafaba Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Aquafaba Market by Product Type (Liquid Aquafaba, Powdered Aquafaba, Concentrated Aquafaba, and Flakes), Function (Foaming Agent, Emulsifier, Binding Agent, and Gelling Agent), Application (Bakery, Confectionery, Sauces & Dressings, Dairy Alternatives, Beverages & Cocktails, and Others) Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail, and Others), and Regional Analysis from 2026 - 2033

Aquafaba Market Share and Trend Analysis

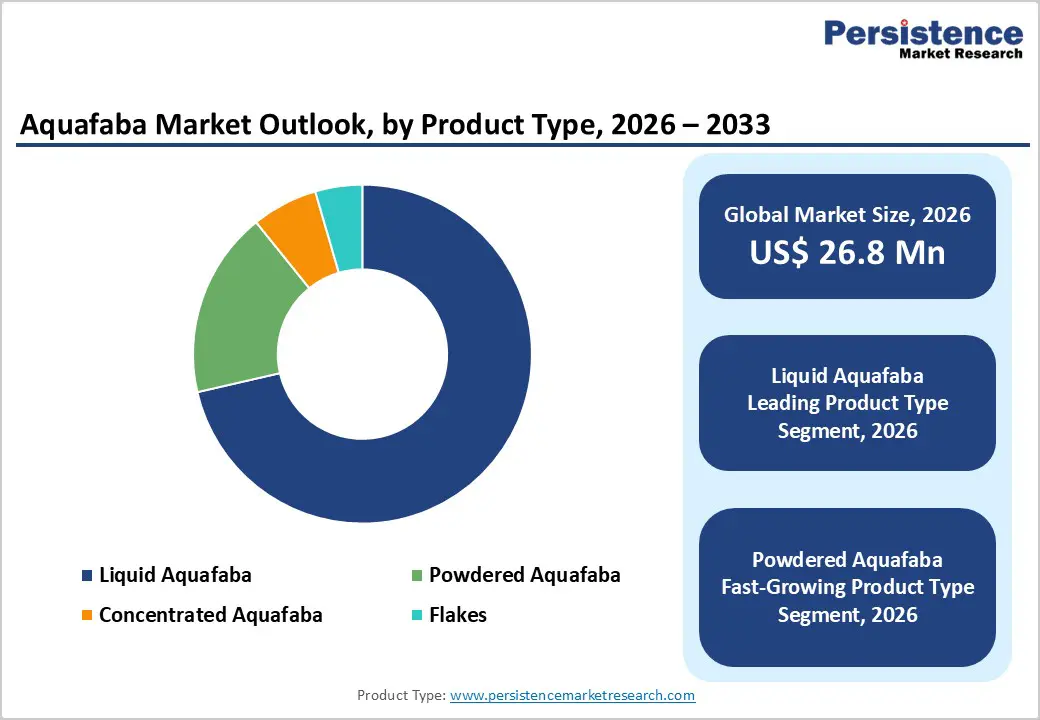

The global aquafaba market size is estimated to grow from US$ 26.8 million in 2026 to US$ 44.0 million by 2033 at a CAGR of 6.2% during the forecast period from 2026 to 2033. The increasing transition toward plant-based eating patterns, coupled with heightened demand for clean-label and allergen-free ingredients, is significantly supporting the adoption of aquafaba across global markets.

Derived as a byproduct of chickpea processing, aquafaba is gaining strong traction as a functional egg replacement due to its ability to deliver foaming, binding, and emulsification properties in a wide range of food applications. The growing availability of ready-to-use liquid formats and shelf-stable powdered variants, along with improved distribution through retail and online channels, is enhancing product accessibility and supporting broader market penetration.

Key Industry Highlights:

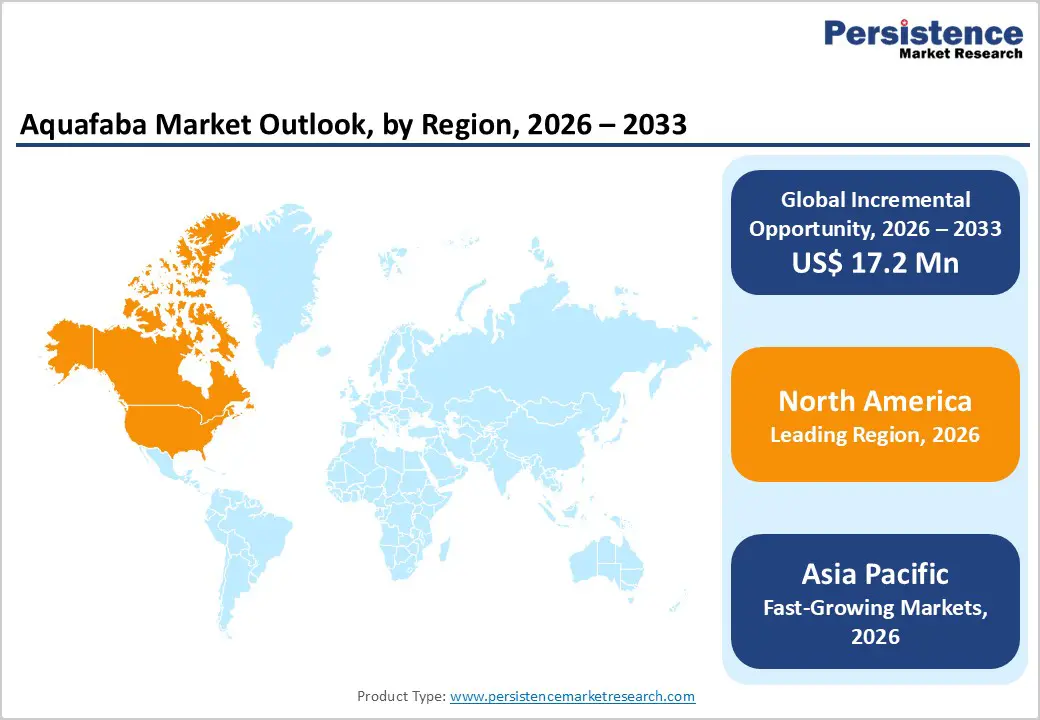

- Leading Region: North America accounts for 45.4%, supported by strong demand for plant-based alternatives, advanced retail ecosystems, and high consumer awareness regarding egg substitutes and clean-label ingredients.

- Fastest-Growing Region: Asia Pacific is emerging as the fastest-growing market, driven by abundant chickpea availability, rising urbanization, higher disposable incomes, and expanding plant-based food consumption.

- Leading Product Type Segment: Liquid aquafaba accounts for 71.4%, driven by its direct usability, functional efficiency in food preparation, and widespread adoption in household and foodservice applications.

- Leading Distribution Channel Segment: Supermarkets/Hypermarkets account for 46.2% and benefit from strong product visibility, diverse offerings, and established consumer trust in organized retail environments.

Market Dynamics

Drivers - Rising Adoption of Egg Alternatives and Clean-Label Ingredients Accelerating Demand

Growing consumer shift toward plant-based diets and allergen-free food formulations is significantly boosting demand for aquafaba as a natural egg substitute. Its multifunctional properties, particularly foaming, emulsifying, and binding, enable seamless replacement of egg whites in bakery, confectionery, and processed food applications without compromising texture or performance. This makes it highly attractive for vegan, cholesterol-free, and clean-label product development. The increasing incidence of egg allergies and dietary restrictions is further reinforcing its relevance across both household and industrial consumption.

Additionally, the surge in home baking trends and premium plant-based product launches is amplifying usage across retail and foodservice sectors. Aquafaba aligns well with sustainability goals, as it is derived from chickpea processing byproducts, supporting waste reduction and circular economy principles. Food manufacturers are actively incorporating it into ready-to-use mixes, sauces, and whipped formulations to meet evolving consumer preferences. Expanding distribution through supermarkets and online channels is improving accessibility, particularly in Western markets where plant-based innovation is accelerating. Combined with rising investments in alternative protein ecosystems and ingredient innovation, these factors continue to drive consistent growth and broaden application scope globally.

Restraints - Stability Limitations and Processing Challenges Restricting Wider Industrial Adoption

Despite its functional advantages, aquafaba faces notable limitations related to stability, standardization, and shelf life, which constrain its large-scale commercial adoption. Liquid aquafaba, in particular, is highly perishable and requires controlled storage conditions to maintain its functional integrity, increasing logistical complexity and cost. Variability in composition across chickpea sources, cooking methods, and concentration levels creates inconsistent performance, posing challenges for food manufacturers seeking uniformity in large-scale production.

Moreover, converting aquafaba into powdered or concentrated forms requires advanced drying technologies, such as spray drying or freeze drying, which can be capital-intensive and may compromise functional efficiency if not optimized. Limited consumer awareness in certain regions also restricts adoption, as aquafaba is still perceived as a niche or specialty ingredient rather than a mainstream alternative. In addition, competition from established egg replacers such as starch blends, soy proteins, and commercial emulsifiers intensifies market pressure. Supply chain inefficiencies in sourcing and processing chickpea byproducts further add to cost constraints. These combined factors continue to hinder scalability, particularly in price-sensitive and emerging markets.

Opportunities - Expansion of Functional Plant-Based Formulations and Shelf-Stable Formats Creating New Growth Avenues

The increasing demand for innovative plant-based ingredients is opening significant growth opportunities for aquafaba, particularly in value-added and industrial applications. Its ability to replicate egg functionality positions it as a key component in next-generation vegan formulations across bakery, dairy alternatives, and ready-to-eat categories. Manufacturers are focusing on developing shelf-stable powdered and concentrated variants to enhance usability, extend shelf life, and improve logistics, thereby expanding its commercial viability in global supply chains.

Growth in e-commerce and direct-to-consumer platforms is enabling niche brands to scale rapidly while educating consumers about their versatility. Emerging markets offer untapped opportunities driven by urbanization, evolving dietary habits, and growing interest in plant-based alternatives. Technological advancements in drying and stabilization processes are improving product consistency and performance, making it more suitable for industrial-scale applications. Strategic collaborations between ingredient manufacturers and food brands, along with continuous product innovation, are expected to unlock long-term growth and differentiation in the competitive landscape.

Category-wise Analysis

By Product Type, Liquid Aquafaba Leads Owing to High Usability and Strong Adoption in Direct Food Applications

Liquid aquafaba is projected to command 71.4% of the global market share in 2026, primarily due to its immediate applicability and minimal processing requirements. Its ability to function as a direct egg white substitute in recipes such as meringues, mousses, and baked goods makes it highly attractive for both household and foodservice usage. Unlike powdered variants, liquid aquafaba preserves functional integrity without requiring rehydration, ensuring ease of use and consistent performance. The growing popularity of vegan cooking and home baking trends is further accelerating demand.

Additionally, widespread availability through canned chickpeas and ready-to-use packaged formats supports accessibility and affordability. Foodservice operators and artisanal bakeries prefer liquid formats for maintaining texture and taste authenticity. Despite limitations in shelf life, its strong alignment with clean-label preferences and culinary familiarity continues to reinforce its dominant position in the global aquafaba market.

By Application, Bakery Segment Maintains Dominance Driven by Core Egg Replacement Functionality

The bakery segment is expected to account for 54.8% of total market revenue in 2026, securing its leading position due to aquafaba’s critical role as an egg substitute in baking formulations. Its unique foaming and binding capabilities enable the preparation of products such as cakes, macarons, and whipped toppings without compromising texture or stability. Increasing consumer inclination toward plant-based, allergen-free, and cholesterol-free baked goods is significantly boosting their adoption across both industrial and artisanal baking segments.

Moreover, the surge in vegan product launches and reformulation of traditional recipes is expanding its usage scope. Food manufacturers are leveraging aquafaba to develop clean-label bakery products that meet evolving dietary preferences. The ingredient’s compatibility across a wide range of baked goods, combined with growing retail availability and innovation in ready mixes, continues to strengthen its leadership within the application landscape.

By Distribution Channel, Supermarkets Dominate Due to Strong Retail Presence and Consumer Accessibility

Supermarkets and hypermarkets are expected to capture 46.2% of global aquafaba market revenue in 2026, making them the primary distribution channel. Their dominance is driven by extensive product visibility, a wide assortment of plant-based ingredients, and established consumer trust in organized retail formats. These outlets offer multiple aquafaba formats, including liquid and powdered variants, enabling easy product comparison and informed purchasing decisions. Efficient supply chain networks and strong vendor relationships ensure consistent stock availability, particularly in urban markets. In-store promotions, product placement strategies, and increased shelf space for vegan and specialty ingredients further drive sales growth.

Additionally, supermarkets serve as key platforms for introducing new product innovations and private-label offerings. While online retail is witnessing faster growth, the immediacy of purchase, tactile evaluation, and reliability associated with physical stores continue to sustain their leading position in the market.

Regional Insights

North America Aquafaba Market Trends

North America is projected to account for 45.4% of the global aquafaba market value in 2026, driven by strong demand for plant-based, allergen-free, and clean-label food ingredients. Increasing vegan adoption, rising egg replacement demand in bakery applications, and product innovation are key growth drivers. The region benefits from advanced retail infrastructure and strong penetration of packaged and ready-to-use formats. The U.S. dominates with 78.2% share, while Canada holds 21.8%, supported by growing organic and specialty food demand. Expansion of e-commerce and private-label product offerings further strengthens market penetration across both countries.

U.S. Aquafaba Market Trends

The U.S. accounts for approximately 78.2% of the North American market and is expected to reach a CAGR of 6.8% by 2033. The increasing demand for plant-based egg substitutes in bakery and processed foods. Strong presence of vegan brands, product innovation, and wide availability across supermarkets and online platforms are accelerating adoption in both household and foodservice sectors.

Canada Aquafaba Market Trends

Canada accounted for around 21.8% of the regional market in 2025 and is projected to reach a CAGR of 6.0%. Rising consumer preference for organic, clean-label, and sustainable food products is driving demand. Expansion of specialty retail stores, coupled with increasing online grocery penetration and growing vegan population, is improving accessibility and supporting steady market growth.

Europe Aquafaba Market Trends

Europe accounted for approximately 27.6% of the global aquafaba market in 2025, characterized by strong regulatory frameworks and high demand for sustainable, plant-based ingredients. Growth is supported by increasing consumer preference for vegan and allergen-free formulations, particularly in bakery and confectionery applications.

Germany leads with 31.5% share, followed by the UK at 24.3%, reflecting strong adoption across retail and foodservice sectors. Companies are focusing on traceability, clean-label positioning, and sustainable sourcing. Innovation in powdered aquafaba and functional blends is further expanding industrial applications across the region.

Germany Aquafaba Market Trends

Germany holds approximately 31.5% of the European market and is expected to grow at a CAGR of 5.6%–6.2%. Demand is driven by a strong preference for organic and sustainably sourced food ingredients. Well-developed retail infrastructure and an increasing vegan population are supporting adoption, particularly in bakery and ready-to-cook applications.

UK Aquafaba Market Trends

The UK accounts for nearly 24.3% of the regional market and is projected to grow at a CAGR of 6.0%–6.7%. Growth is fueled by rising demand for plant-based convenience foods and increasing vegan adoption. Expansion of online grocery platforms, coupled with frequent product launches, is strengthening market penetration across retail and foodservice channels.

Asia Pacific Aquafaba Market Trends

Asia Pacific is the fastest-growing region, expected to expand at a CAGR of 16.7% from 2026 to 2033, accounting for approximately 19.8% of global market share in 2026. Growth is driven by abundant availability of raw materials (chickpeas and legumes), increasing awareness of plant-based foods, and rising urbanization. China leads with 36.4% share, followed by India at 28.7%, supported by strong domestic consumption and expanding food processing industries. Improving supply chain infrastructure and export potential are further accelerating growth across the region.

China Aquafaba Market Trends

China holds around 36.4% of the Asia Pacific market and is projected to grow at a CAGR of 7.8%–8.6% through 2033. Growth is supported by increasing demand for plant-based food products and the expansion of the food processing sector. Rising health awareness and focus on functional ingredients are further boosting adoption.

India Aquafaba Market Trends

India accounts for approximately 28.7% of the regional market and is expected to grow at a CAGR of 8.5%–9.3%. Growth is driven by abundant chickpea availability and rising demand for plant-based and clean-label ingredients. Increasing awareness, along with the expansion of retail and foodservice channels, has accelerated market penetration.

Competitive Landscape

The global aquafaba market is highly competitive, with strong participation from Symrise AG, Alternative Foods London Ltd, Casa Amella Bio Food, S.L.U., EURO S.P.I.D. srl, and Maicerías Españolas S.L. These companies leverage integrated supply chains, strong sourcing networks, and advanced processing capabilities to enhance product consistency and functionality.

Rising demand for plant-based ingredients, egg substitutes, and clean-label formulations is accelerating innovation across applications. Market players are expanding product portfolios, strengthening global distribution channels, forming strategic partnerships, and increasing investments to develop convenient, shelf-stable, and functional aquafaba solutions aligned with evolving consumer and industrial food processing requirements.

Key Industry Developments:

- In April 2026, Pasta Premium, in collaboration with EggField, introduced a new line of cook-stable, plant-based pasta under the ERNST brand. Made using durum wheat semolina and aquafaba, the formulation replaces egg functionality while maintaining structure and cooking performance. Designed for foodservice and catering, the product offers a stable, resource-efficient alternative amid fluctuating egg supply.

- In November 2025, The VERY Food Co. introduced an industrial-grade aquafaba powder designed as a scalable alternative to eggs in commercial food production. The product offers strong foaming, emulsifying, and binding functionality, making it suitable for applications such as bakery, confectionery, and ready-to-eat formulations. With improved shelf stability and ease of handling compared to liquid formats, the powder is tailored for large-scale manufacturing. This launch supports the growing demand for plant-based, allergen-free, and clean-label ingredients across the global food industry.

- In October 2023, Symrise launched diana food chickpea and aquafaba flakes, expanding its plant-based ingredient portfolio. The chickpea flakes provide high protein and fiber, enhancing texture and moisture in applications such as snacks, falafel, and dips. The aquafaba flakes function as a vegan egg alternative, offering emulsification and water-binding properties, making them suitable for products such as mayonnaise and salad dressings.

Global Aquafaba Market Report – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 20.3 Mn |

|

Current Market Value (2026) |

US$ 26.8 Mn |

|

Projected Market Value (2033) |

US$ 44.0 Mn |

|

CAGR (2026-2033) |

6.2% |

|

Leading Region |

North America, 45.4% share |

|

Dominant Function |

Foaming Agent, 38.6% share |

|

Top-ranking Product Type |

Liquid Aquafaba, 71.4% |

|

Incremental Opportunity |

US$ 17.2 Mn |

Companies Covered in Aquafaba Market

- Symrise AG

- Alternative Foods London Ltd

- Casa Amella Bio Food, S.L.U.

- EURO S.P.I.D. srl

- Maicerías Españolas S.L.

- Haden's Aquafaba

- SESAJAL S.A. de C.V.

- The Very Food Co.

- Chickplease

- Ingredion Incorporated

- Vor Food

- Vör Foods

- Sabatino North America LLC

- The Plant Based Egg

- Ernst Böcker GmbH & Co. KG

- Others

Frequently Asked Questions

The global aquafaba market is projected to be valued at US$ 26.8 billion in 2026.

Rising demand for vegan, allergen-free egg substitutes in bakery and processed foods is a key driver of the global aquafaba market.

The global aquafaba market is poised to witness a CAGR of 6.2% between 2026 and 2033.

Growing industrial adoption of powdered aquafaba in clean-label, plant-based formulations presents significant market expansion opportunities.

Symrise AG, Alternative Foods London Ltd, Casa Amella Bio Food, S.L.U., EURO S.P.I.D. srl, and Maicerías Españolas S.L are some of the key players in the aquafaba market.