- Pharmaceuticals

- Androgenetic Alopecia Market

Androgenetic Alopecia Market Size, Share, and Growth Forecast 2026 - 2033

Androgenetic Alopecia Market by Gender (Male, Female), Treatment (Pharmaceuticals, Devices), by End-user (Dermatology Clinics, Homecare Settings), Sales Channel (Prescriptions, OTC), and Regional Analysis, 2026 - 2033

Androgenetic Alopecia Market Size and Trends Analysis

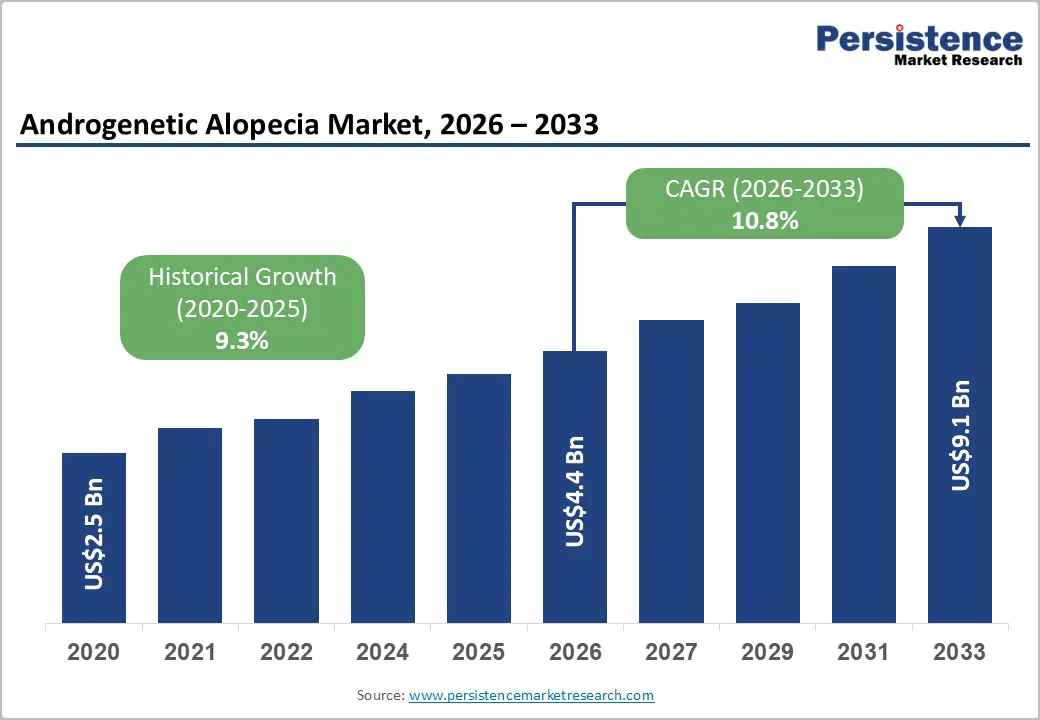

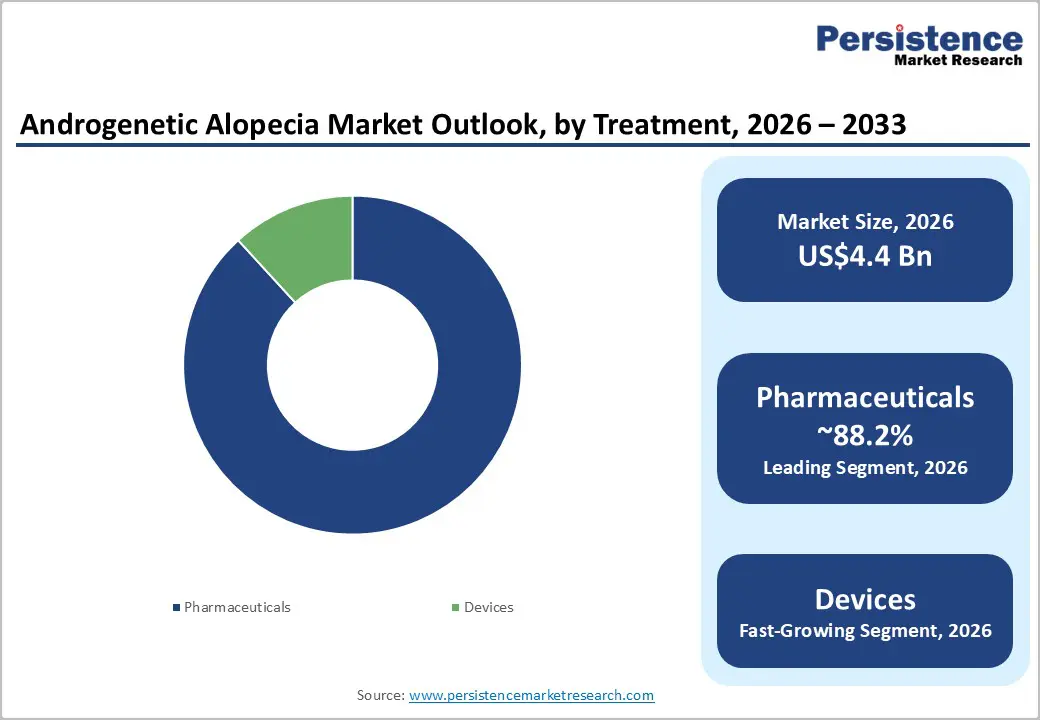

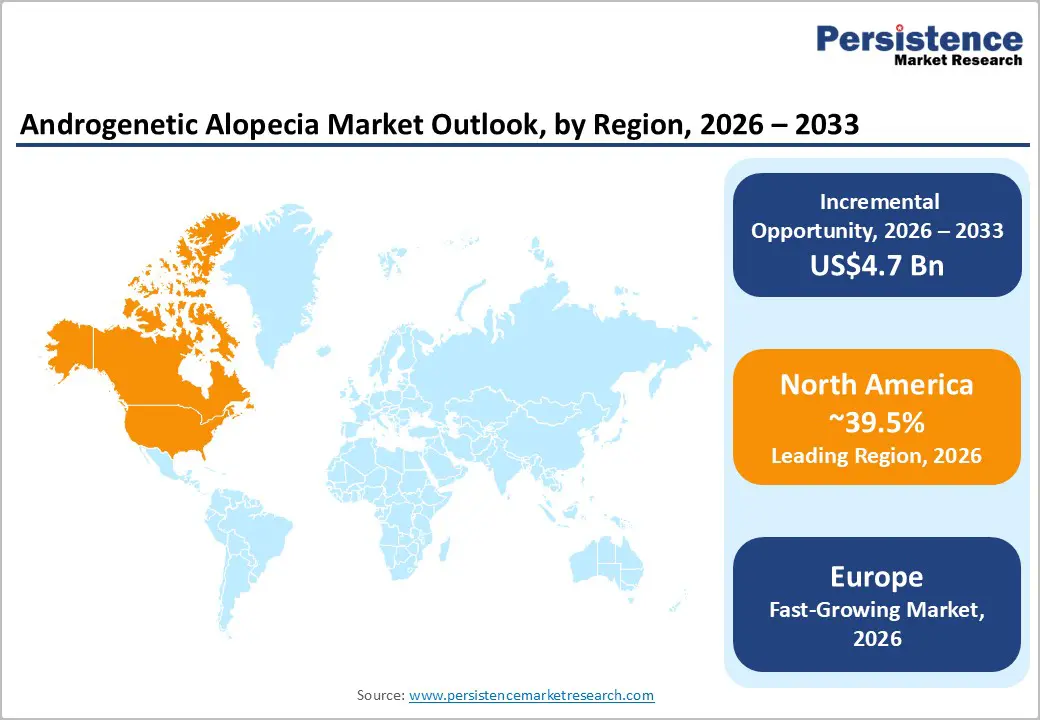

The global androgenetic alopecia market size is likely to be valued at US$4.4 billion in 2026 and is expected to reach US$9.1 billion by 2033, growing at a CAGR of 10.8% during the forecast period from 2026 to 2033, driven by rising early-onset hair loss linked to stress, hormonal imbalance, and lifestyle changes, which is increasing the treatment-seeking population. Expansion of tele-dermatology and direct-to-consumer prescription platforms is further improving access to clinically approved therapies.

Key Industry Highlights:

- Leading Treatment: Pharmaceuticals, approximately 88.2% share in 2026, as FDA-approved drugs such as minoxidil and finasteride remain the first-line treatments.

- Dominant End-user: Dermatology clinics, nearly 57.6% in 2026, as they provide accurate diagnosis and access to specialized treatments, including transplants.

- Leading Region: North America, with about 39.5% share in 2026, owing to early treatment adoption and the presence of key telehealth platforms.

- Fast-growing Region: Europe, backed by the rising use of combination therapies and increasing demand for non-invasive devices such as laser therapy.

- Clinical Trial: In December 2025, Cosmo Pharmaceuticals announced breakthrough Phase III topline results from its Scalp 1 and Scalp 2 trials for clascoterone 5% topical solution in male androgenetic alopecia, showing up to 539% relative improvement in target-area hair count versus placebo.

DRO Analysis

Driver - Increasing Prevalence of Androgenetic Alopecia among Younger Demographics

Androgenetic alopecia (AGA) is no longer just a condition of middle age. A 2024 clinical study published in PubMed Central (PMC) found the average age of AGA onset to be just 23.9 years in men and 29.46 years in women. Lifestyle factors are a key reason behind this shift. A 2023 study in Nutrients found a direct link between consumption of sugar-sweetened beverages and male pattern hair loss in young men.

Compounding this, a September 2024 cross-sectional analysis using the National Institutes of Health’s (NIH) All of Us dataset confirmed that most male AGA cases present between ages 20 and 39, far earlier than previously documented. The convergence of dietary habits, chronic stress, and environmental triggers is pulling the onset window down, extending the patient population, and creating sustained demand for treatment.

Constant Normalization of Aesthetic Consciousness

The social conversation around hair loss has shifted dramatically. A 2024 study of 390 AGA patients found that 69.3% used social media platforms, primarily Google, Instagram, and TikTok, to seek information about hair loss and treatment options. This digital engagement is normalizing both the condition and the decision to treat it.

The American Hair Loss Association noted in its 2024 National Hair Loss Awareness Month statement that hair loss affects over 40% of women and two-thirds of men by age 35, reinforcing that it is a mainstream health concern. As more people openly discuss treatments such as minoxidil and hair transplants, the stigma is fading, further pushing several patients toward early consultations and active treatment.

Restraint - Side Effect Burden to Limit Long-Term Treatment Adherence

The two most prescribed AGA treatments carry well-documented side effects that deter continued use. A review published in Georgetown Medical Review found that some men using finasteride have reported persistent sexual side effects, including low libido, erectile dysfunction, and orgasmic dysfunction. These continue even after stopping the drug, a cluster of symptoms now referred to as Post-Finasteride Syndrome (PFS). This prompted the Food and Drug Administration (FDA) to update finasteride's label to include risks of depression and persistent sexual dysfunction.

On the topical side, a study in the Journal of Clinical and Aesthetic Dermatology found that around 21.2% of patients using over-the-counter minoxidil reported side effects, with scalp irritation being the most common. Only 44.7% adhered to the treatment long-term. Together, these tolerability issues significantly limit patient persistence and market growth.

Opportunity - Emergence of Oral Minoxidil as a New Standard of Care

Low-dose oral minoxidil is fast becoming a preferred alternative for patients who struggle with topical formulations. A 2024 randomized controlled trial published in the Journal of Cosmetic Dermatology found that 1 mg/day oral minoxidil was not significantly less effective than standard 5% topical minoxidil in both male and female AGA patients, with a much simpler application routine.

A 2024 literature review confirmed that even very low doses of 0.25 mg/day produced measurable hair growth effects, with the best results seen in the 1 to 5 mg/day range. ClinicalTrials.gov also lists an ongoing trial (NCT05888922) evaluating 1 mg oral minoxidil specifically in women with female AGA. This positions low-dose oral minoxidil as a broadly accessible treatment option, especially for patients unwilling or unable to maintain daily topical routines.

Surging Use of Bicalutamide to Treat Female Hair Loss

Bicalutamide is emerging as a viable antiandrogen option for women with AGA, particularly where other treatments fall short. A 2025 systematic review in JAAD Reviews, covering 494 female patients across nine studies, found that bicalutamide reduced hair loss severity by 17% to 28.9% in female pattern hair loss patients. It notably outperformed spironolactone in some analyses.

A 2024 comparative study in the Australasian Journal of Dermatology concluded that bicalutamide showed greater efficacy and a better safety profile than spironolactone for female pattern hair loss. Its peripheral selectivity means it blocks androgen receptors at the follicle level without the blood pressure fluctuations associated with spironolactone. With a rising number of women presenting with AGA alongside hyperandrogenic conditions such as PCOS, bicalutamide fills a meaningful clinical gap.

Category-wise Analysis

Treatment Insights

The pharmaceuticals segment is predicted to lead with a share of approximately 88.2% in 2026, as they are the only widely approved and clinically validated treatments for androgenetic alopecia. Drugs such as minoxidil and finasteride have decades of efficacy data. The U.S. Food and Drug Administration has approved both, which builds strong physician trust. Clinical studies published in journals such as the Journal of the American Academy of Dermatology show that finasteride can slow hair loss in around 80 to 90% of men. These drugs are also easy to prescribe and expand globally. Their low cost and availability in generic forms make them the first-line therapy in most countries.

The devices segment is estimated to be the fastest growing in the forecast period, as they provide non-drug options with few systemic side effects. Low-Level Laser Therapy (LLLT) devices, microneedling tools, and robotic transplant systems are gaining momentum. The National Institutes of Health has published studies showing LLLT improves hair density by increasing follicle activity. Companies are also launching FDA-cleared laser caps for home use. These devices are attractive to patients who avoid hormonal drugs. The shift toward combination therapy, such as microneedling with minoxidil, is also boosting device adoption.

End-user Insights

Dermatology clinics are anticipated to dominate with a share of nearly 57.6% in 2026, as diagnosis and treatment planning require medical expertise. Hair loss is often linked to hormones, genetics, or underlying conditions. Dermatologists use dermoscopy and scalp biopsy to confirm androgenetic alopecia. Clinics also provide novel procedures such as Platelet-Rich Plasma (PRP) and hair transplants. According to clinical guidance from the American Academy of Dermatology, patients benefit more when treatments are supervised by specialists. This keeps clinics at the center of the treatment cycle.

The homecare settings segment is expected to remain in the second position in 2026, fostered by convenience and the emergence of digital health platforms. Patients now prefer managing hair loss privately at home. Brands delivering subscription-based treatments have broadened access to oral and topical drugs. During and after COVID-19, tele-dermatology adoption increased sharply. The World Health Organization (WHO) found a global rise in telemedicine use, which supported remote treatment models. Home-use devices such as laser caps and microneedling rollers are also fueling this shift.

Regional Insights

North America Androgenetic Alopecia Market Trends

In 2026, North America will dominate with a share of around 39.5% in 2026, owing to high disease awareness and a well-established clinical infrastructure. In the U.S. and Canada, hair loss is treated early rather than delayed. This shifts demand toward long-term therapies instead of late-stage interventions. The National Institutes of Health estimates that androgenetic alopecia affects a large share of adults, with prevalence increasing sharply after age 40.

Another key factor is the quick rise of hybrid care models. Patients often start with teleconsultation and then move to in-clinic procedures such as PRP or transplants. This integrated approach is not yet as developed in many other regions. North America is also the first to adopt new formats such as topical finasteride sprays and compounded oral minoxidil, which are now widely prescribed through digital platforms.

U.S. Androgenetic Alopecia Market Trends

The U.S. is moving toward personalized and preventive treatment. Younger consumers are starting treatment in their 20s, which extends lifetime spending. Data from ClinicalTrials.gov shows a steady rise in trials focused on androgen receptor blockers and regenerative therapies. There is also a shift toward combination therapy as a standard approach. For example, dermatologists increasingly prescribe oral minoxidil along with finasteride and adjunct therapies such as microneedling. Another key driver is the subscription model. Companies are locking in long-term users through bundled offerings that include consultations, medication, and follow-ups. This creates recurring demand rather than one-time purchases.

Europe Androgenetic Alopecia Market Trends

Europe is anticipated to exhibit the fastest growth rate over the forecast period, backed by a blend of medical and aesthetic demand. Hair loss is no longer treated only as a medical issue. It is now closely associated with cosmetic outcomes. The European Academy of Dermatology and Venereology has reported a steady rise in dermatology visits related to hair thinning, especially among women. Southern and Eastern Europe are becoming key hubs for hair transplant tourism.

Countries such as Türkiye perform thousands of procedures each month, attracting patients from Western Europe. Another factor is regulatory consistency. The European Medicines Agency ensures standardized drug approvals, which support cross-border availability of treatments. Clinics are also early adopters of combination protocols, which improve treatment success rates.

U.K. Androgenetic Alopecia Market Trends

The U.K. market is expanding through private sector development. Since the National Health Service does not widely fund hair loss treatments, private clinics dominate. This has created a competitive environment where clinics differentiate through novel techniques. London has become a key center for high-density Follicular Unit Extraction (FUE) transplants and PRP-based therapies. Another trend is the rise of online prescription platforms. Patients can now access finasteride or minoxidil after a digital consultation, which reduces barriers to entry. Demand is also rising among women, especially for non-hormonal and low-dose therapies, which is boosting the market.

France Androgenetic Alopecia Market Trends

France stands out due to its superior clinical research base and high acceptance of dermatological care. The French National Authority for Health promotes strict clinical guidelines, which increases trust in approved treatments. Modern consumers are also more inclined toward preventive care. Several patients start treatment at the early stages of hair thinning. Another important factor is the presence of leading dermo-cosmetic brands that bridge the gap between pharmaceuticals and over-the-counter care. This creates a tiered market where prescription drugs, supplements, and topical solutions are used together. Pharmacies in France also play a key role in guiding patients, which increases product penetration.

Asia Pacific Androgenetic Alopecia Market Trends

Asia Pacific is showing decent and diverse growth patterns. The region has a younger patient base compared to Western markets. Early-onset hair loss is rising due to stress, diet, and pollution. Countries such as India and South Korea are seeing high demand for both medical and surgical treatments. South Korea, in particular, is known for novel hair transplant techniques and high procedural volumes. Governments in countries such as Thailand and India are promoting medical tourism, which is boosting clinic revenues. Local brands are also launching affordable generic drugs, making treatment accessible to a wider population.

China Androgenetic Alopecia Market Trends

China is one of the fastest-evolving markets due to its expansion and digital infrastructure. The National Health Commission of China has reported that hair loss affects over 250 million people, with several cases appearing before age 30. This younger demographic is highly active online, which supports e-commerce-based sales of treatments. Platforms such as JD Health and Alibaba Health are enabling online consultations and direct drug delivery. Domestic pharmaceutical firms are also investing in new drug development, including topical anti-androgens. Social media platforms are further increasing awareness and reducing stigma, which is encouraging more people to seek treatment.

Japan Androgenetic Alopecia Market Trends

Japan’s growth is stable and pushed by quality-focused healthcare. The country has a well-regulated pharmaceutical market and high trust in medical treatments. The Ministry of Health, Labor and Welfare supports research into regenerative medicine, including stem-cell-based hair therapies. Local companies are focusing on developments in drug delivery systems, such as improved topical formulations. Another factor is the aging population. Hair thinning is more common in older adults, which sustains long-term demand. Younger consumers are also entering the market, especially with preventive treatments.

Competitive Landscape

The global androgenetic alopecia market is moderately fragmented. Competition is spread across pharmaceutical companies, hair restoration clinics, and direct-to-consumer telehealth brands. Established drug makers still hold a dominant position through products based on minoxidil and finasteride. New companies are gaining traction by providing combination therapies, oral formulations, AI-based diagnosis, subscription models, and regenerative treatments.

Another prominent competitive shift is the rise of digital-first brands such as Hims, Keeps, and Nutrafol. These companies are transforming the market by bundling prescription treatments, supplements, teleconsultations, and subscriptions into one interface. Instead of competing purely on clinical efficacy, they compete on convenience, affordability, and long-term customer retention. This strategy is helping them capture young consumers, especially millennials and Gen Z patients who are seeking early intervention.

Key Industry Developments:

- In March 2026, Xtressé announced that the U.S. FDA accepted its Investigational New Drug (IND) application for Xvie. It is described as the first and only extracellular vesicle injectable therapy for androgenetic alopecia.

- In December 2025, Kintor Pharmaceutical published Phase 2 trial results for GT20029, the world's first topical PROTAC compound for androgenetic alopecia, in a peer-reviewed journal. Unlike finasteride or minoxidil, GT20029 uses PROTAC technology to degrade androgen receptors directly at the scalp follicle level, targeting the root cause of hair loss without systemic hormonal interference.

- In October 2025, Pelage Pharmaceuticals announced the close of a US$120 million Series B financing round co-led by ARCH Venture Partners and GV (Google Ventures) to boost its lead program, PP405. It is a topical therapy designed to reactivate dormant hair follicle stem cells.

Companies Covered in Androgenetic Alopecia Market

- Johnson & Johnson Services, Inc.

- Cipla, Inc.

- Sun Pharmaceutical Industries Ltd.

- Merck & Co., Inc.

- Dr. Reddy’s Laboratories Ltd.

- Aurobindo Pharma

- Lexington Intl., LLC

- Freedom Laser Therapy, Inc. (iRESTORE Hair Growth System)

- Curallux, LLC

- Apira Science, Inc. (iGROW Laser)

- Theradome Inc.

- Others

Frequently Asked Questions

The global androgenetic alopecia market is projected to be valued at US$4.4 billion in 2026.

The market is expected to reach US$9.1 billion by 2033.

Key market trends include rising aesthetic awareness and increasing medical tourism for hair transplants.

Pharmaceuticals are expected to be the leading treatment with a share of nearly 88.2% in 2026, spurred by their affordability and easy availability in generic forms.

The market is expected to grow at a CAGR of 10.8% from 2026 to 2033.

Johnson & Johnson Services, Inc., Cipla, Inc., Sun Pharmaceutical Industries Ltd., and Merck & Co., Inc. are a few key market players.