ID: PMRREP18595| 181 Pages | 9 Dec 2025 | Format: PDF, Excel, PPT* | Automotive & Transportation

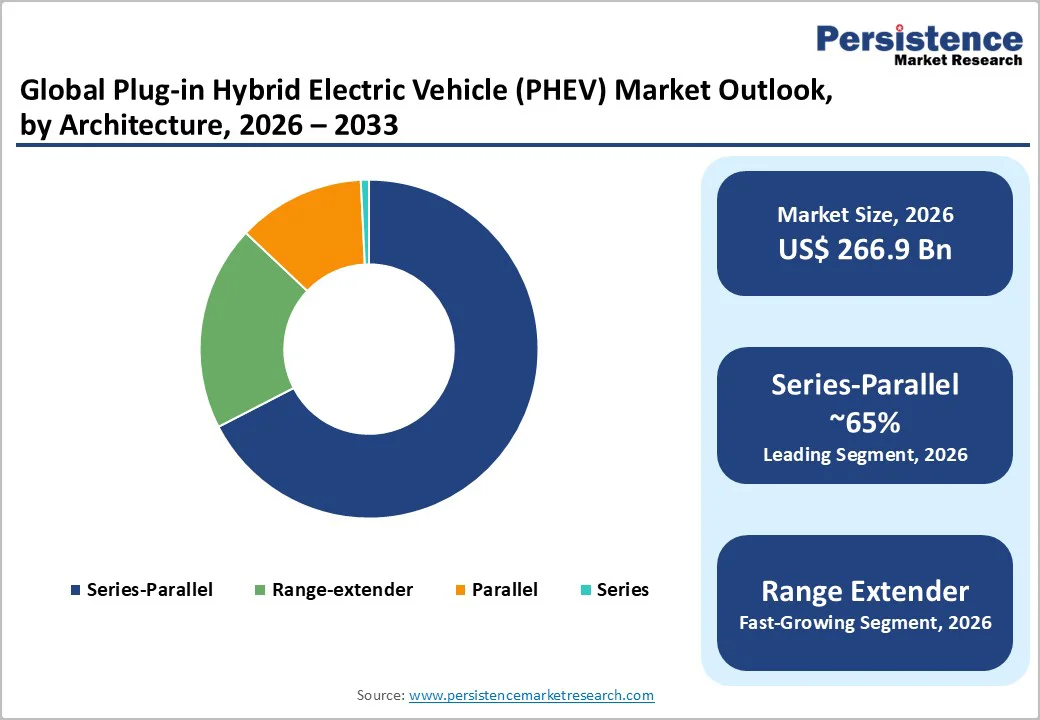

The global plug-in hybrid electric vehicle (PHEV) market size is likely to be valued at US$266.9 billion in 2026. It is expected to reach US$712.6 billion by 2033, growing at a CAGR of 15.1% during the forecast period from 2026 and 2033, driven by stringent regulations such as CO2 emission performance standards for new passenger cars and vans across major markets, rapid battery technology cost reductions, and increasing consumer adoption of electrified powertrains as a pragmatic bridge technology.

| Global Market Attribute | Key Insights |

|---|---|

| Plug-in Hybrid Electric Vehicle Market Size (2026E) | US$266.9 Bn |

| Market Value Forecast (2033F) | US$712.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 15.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 35.7% |

Stringent Regulatory Frameworks and CO2 Emission Standards

Regulatory mandates are the key driver accelerating global PHEV adoption. The European Union's CO2 emission targets (95 g/km by 2021 and 49.5 g/km by 2030) have compelled OEMs to accelerate the expansion of their electrified vehicle portfolios. China's dual-credit system, which combines fuel-consumption and new-energy-vehicle credits, penalizes manufacturers that rely solely on ICEs while incentivizing PHEV production.

The U.S. EPA standards, targeting 49 g/km by 2026, are also creating a similar market pressure. These regulatory mechanisms are expected to drive an estimated 40-45% of market volume growth between 2026 and 2033, particularly in North America and Europe. Compliance penalties for non-compliance exceed US$5,000 per non-compliant vehicle in major markets, creating urgent transformation imperatives for global OEMs.

Regulatory harmonization efforts across regions are standardizing PHEV technology requirements, reducing fragmentation, and enabling scaled manufacturing.

Battery Technology Cost Reduction and Performance Enhancement

Lithium-ion battery costs have declined from US$1,191/kWh (2010) to approximately US$132/kWh (2023), with projections reaching US$80-90/kWh by 2030. This 85%+ cost reduction directly improves PHEV affordability and battery range, addressing historically cited consumer concerns regarding purchase price premium and operational versatility.

Enhanced battery energy density (now 250+ Wh/kg) enables 50-80 km all-electric range in mass-market PHEVs, positioning vehicles as true dual-fuel alternatives rather than niche products. Fast-charging infrastructure (DC charging from 10-80% in 20-30 minutes) further accelerates adoption by reducing charging anxiety.

Battery durability improvements, with 8-10-year/160,000-km warranties now standard, enhance the total cost of ownership competitiveness versus pure ICE vehicles. This technological trajectory will continue to reduce the total cost of ownership for PHEVs relative to conventional cars, driving mainstream consumer adoption.

Macroeconomic Shift toward Sustainable Urban Mobility

Post-pandemic recovery has accelerated corporate sustainability commitments and Environmental, Social, Governance (ESG) investment mandates. Fleet operators and corporate buyers, accounting for 60-70% of PHEV purchases in Europe and 50-55% in North America, increasingly prioritize electrified powertrains to achieve carbon neutrality targets.

Urban congestion and air quality regulations in major metropolitan areas (London, Paris, Beijing, Mumbai) impose penalties on high-emission vehicles, with some cities planning ICE vehicle phase-outs by 2030 - 2035. This structural shift toward sustainable mobility is projected to unlock US$80-100 billion in incremental demand from fleet electrification initiatives alone between 2026 and 2033.

High Purchase Price Premium and Total Cost of Ownership Barriers

Despite battery cost reductions, PHEVs command 25-35% higher purchase prices compared to equivalent ICE vehicles. A mid-size PHEV SUV typically costs US$45,000-55,000, compared with US$32,000-38,000 for comparable ICE models. In price-sensitive markets, particularly India and Southeast Asia, this premium represents 8-12 months of average household income, significantly limiting addressable market scope.

Total cost of ownership (TCO) advantages, while mathematically favorable over 5-7 years in developed markets with high fuel costs and electricity tariffs, require consumer understanding of lifecycle economics, which is often lacking in developing regions. This affordability barrier is estimated to limit market penetration in price-sensitive Asia Pacific to 15-20% compound annual adoption rates, compared with 25-35% in mature markets.

Charging Infrastructure Fragmentation and Grid Capacity Constraints

While global charging infrastructure has expanded significantly, geographic disparities remain pronounced. North America and Europe have approximately 1 public charger per 100 EVs (including BEVs and PHEVs), whereas the Asia-Pacific ratio ranges from 1:200 (India) to 1:80 (China). Charging standardization challenges, exemplified by North America's NACS versus CCS debate and Asia's multiple connector standards, create interoperability inefficiencies.

Grid capacity constraints in developing regions pose operational barriers; India's power deficit (an 8-10% capacity shortfall during peak hours) complicates widespread adoption of PHEVs. These infrastructure gaps are projected to constrain volume growth in India and Southeast Asia by 30% annually through 2033, requiring parallel investments in grid modernization and charging networks.

Southeast Asia's Emerging PHEV Market with Government Support Mechanisms

Southeast Asia represents a high-growth opportunity driven by rising middle-class incomes, government electrification incentives, and OEM localization investments. Thailand's EV3.5 program provides tax incentives for vehicles with 70%+ local content, while Indonesia's tax breaks aim for a 13% EV sales share by 2030.

Market volume growth in Southeast Asia is projected at over 25% CAGR between 2026 and 2033, with the addressable market expanding exponentially. Chinese OEMs (BYD, Cherry, and Wuling) are strategically expanding their regional presence, leveraging cost advantages and EV expertise.

OEM partnerships, including those with Mercedes-Benz and Volvo, signal confidence in long-term market maturation. Government investments in charging infrastructure and EV manufacturing incentives create a favorable regulatory environment that attracts OEM capital allocation.

Range-Extender Architecture Expansion and Application Diversification

Range-extender PHEVs, currently representing 15-20% of the PHEV market, are projected to reach 25%+ market share by 2033, particularly in the Asia Pacific. This architecture offers distinct advantages in regions with nascent charging infrastructure, enabling extended range through lightweight generator modules without substantial battery scaling.

The range-extender segment represents an estimated US$30-40 billion market opportunity by 2033, appealing to fleet operators managing long-haul logistics and regional delivery networks.

Technology partnerships between battery manufacturers (CATL, BYD) and powertrain specialists are accelerating development cycles. Application extension into commercial vehicle segments, light commercial vehicles, delivery vans, and regional transportation, unlocks underserved market niches with a distinct range and charging requirements.

Series-Parallel Architecture: Leading Segment

Series-parallel architecture maintains market dominance, with over 65% global market share in 2026, representing the optimal compromise between fuel-efficiency optimization and electric range maximization. This configuration enables independent operation of the electric motor and engine, optimizing powertrain efficiency across driving cycles. The architecture supports full regenerative braking recovery, enhancing electric-only range and reducing fuel consumption.

Sales of series-parallel PHEVs are expected to exceed 5.5 million units globally in 2026, with volumes projected to grow at a CAGR of 16% through 2033. OEM standardization around series-parallel platforms, exemplified by Volkswagen Group's MQB architecture and BMW's iPerformance modules, has reduced development costs and accelerated commercialization. Technical maturity and supplier ecosystem density position series- parallel as the primary architecture throughout the forecast period.

Range-Extender Architecture: Fastest Growing Segment

The range-extender architecture exhibits the highest growth trajectory, projected to grow at an 18% CAGR between 2026 and 2033. This configuration utilizes lightweight internal combustion engines (typically 1.0-1.5L displacement) primarily for power generation, reducing mechanical complexity and enabling independent optimization of electric motors.

The range-extender market value is projected to surpass US$50 billion by 2033, driven by strength in commercial vehicle applications and in infrastructure-constrained regions. Chinese manufacturers (BYD, Li Auto) have achieved commercial success with range-extender configurations, proving market viability beyond European and American markets. Fleet operators favor range-extender mechanics for logistics applications that require extended range without substantial battery investment.

Passenger Vehicle: Dominating Segment (98% Market Share)

Passenger vehicles hold overwhelming market dominance with around 98% market share in 2026, reflecting consumer preference alignment and OEM production capacity concentration. SUVs and crossovers represent the leading passenger vehicle category, commanding over 60% of passenger vehicle PHEV sales in 2026, driven by consumer preference for spacious, versatile vehicles.

The SUV segment's dominance reflects brand profitability dynamics; SUVs generate 25-40% higher margins than sedans, incentivizing OEM production prioritization. The hatchback and sedan categories account for 25-30% of the passenger vehicle market, appealing to price-conscious European consumers and to compact-focused Asian markets. Passenger vehicle segment value is estimated at US$260 billion in 2026, growing at a 15% CAGR through 2033.

Commercial Vehicles: Fast-Growing Segment

Commercial vehicle PHEVs represent a rapidly emerging segment, currently accounting for 1-2% of the market but projected to reach 5-8% by 2033. This segment encompasses light commercial vehicles (LCVs), delivery vans, and specialized commercial applications.

The commercial vehicle PHEV market is projected to grow at a 30% CAGR between 2026 and 2033, substantially exceeding passenger vehicle growth rates. Fleet electrification initiatives, driven by corporate carbon reduction commitments and total cost of ownership advantages, are accelerating commercial PHEV adoption.

Logistics operators benefit from silent electric-only urban delivery operations, reducing noise pollution and improving driver comfort. The commercial vehicle PHEV market value is projected to exceed US$20 billion by 2033, representing a high-growth opportunity for OEM investment.

North America represents a mature PHEV market with nuanced regulatory dynamics and evolving consumer preferences. The U.S. accounts for approximately 95% of regional volume.

The U.S. plug-in hybrid electric vehicle (PHEV) market is valued at US$20 billion in 2026 and is projected to exceed US$40 billion by 2033, growing at a 9.4% CAGR during this period. This moderate growth trajectory reflects market saturation in early-adopter segments and increasing competition from battery electric vehicles (BEVs).

Architecture and Vehicle Type Dynamics: SUVs and crossovers account for over 85% of the U.S. PHEV market, reflecting consumer preferences for larger vehicles and the appeal of higher battery capacity, which helps ease range anxiety.

The parallel architecture currently holds the highest share; however, the series-parallel configuration is projected to account for over 60% of PHEV sales by 2033 as efficiency-focused OEMs optimize powertrains for stricter EPA standards. This architectural transition indicates OEM recognition of efficiency optimization as a competitive differentiator in mature markets.

Regulatory Environment: The Biden administration's target of 50% EV sales share (including BEVs and PHEVs combined) by 2030 drives regulatory pressure, though PHEV-specific incentives have eased compared to previous administrations.

Federal tax credits of US$7,500 apply to qualifying PHEVs, influencing purchase decisions in mid-market segments. State-level initiatives, particularly in California, Massachusetts, and New York, impose stricter emission standards and ZEV (Zero Emission Vehicle) mandates, creating regional compliance differentiation.

Competitive Landscape and Investment Trends: The North American PHEV market is dominated by traditional OEMs (Ford, General Motors, Jeep) supplemented by luxury manufacturers (BMW, Mercedes-Benz, Porsche).

Chinese EV manufacturers have a limited presence in North America due to regulatory barriers, thereby preserving market share concentration among established players. OEM investment in dedicated PHEV platforms is slowing in favor of BEV-focused strategies, indicating potential pressure on PHEV market share as BEVs achieve lower total cost of ownership.

Europe represents the second-largest global PHEV market with pronounced regulatory influence and geographic concentration. The European PHEV market was valued at approximately US$80 billion in 2026 and is projected to surpass US$135 billion by 2033, growing at an 8% CAGR. Regional market dynamics reflect stringent CO2 emission regulations and policy-driven incentive structures supporting electrified powertrains.

Geographic Concentration: Germany holds market leadership with over 20% regional share, followed by the U.K. (16%) and Spain (9%). Germany's dominance reflects a strong OEM presence (Volkswagen Group, BMW, Daimler-Benz, and Audi) and affluent consumer demographics that support premium PHEV purchases.

The Benelux countries and Scandinavia exhibit disproportionately high PHEV adoption rates relative to population, driven by government tax incentives and investments in charging infrastructure. Regional variations in incentive structures, ranging from purchase price subsidies (Germany, Spain) to tax exemptions (Norway, Denmark), create market differentiation and investment opportunities.

Architecture and Vehicle Preferences: SUVs and crossovers dominate sales, accounting for more than 65% of the PHEV market share, while the Hatchback and Sedan categories account for 30-35% of the market. Series-parallel architecture continues dominance, accounting for over 60% of projected 2033 sales. This architectural consistency reflects European OEM expertise concentration and regulatory predictability, enabling long-cycle platform investments.

Regulatory Environment and Electrification Leadership: The EU's CO2 standards (49.5 g/km by 2030) mandate comprehensive electrification across OEM portfolios. Super-credit mechanisms, assigning electric vehicles two to four times their value for compliance, have historically supported PHEV market growth.

Recent policy shifts prioritizing pure electric vehicles, along with potential ICE phase-out timelines such as the EU’s 2035 proposal, are creating strategic uncertainty for PHEVs and may temper long-term investment commitments.

Norway leads global electrification with a 93% adoption rate of electric powertrains (BEVs and PHEVs combined), while Denmark follows with over 85%, demonstrating market maturation in the Nordic region.

Competitive Dynamics: The European PHEV market is highly competitive, with 25-30 active OEMs competing across segments. Luxury and premium segments show stronger competition than mass-market segments, driven by battery cost premiums, justifying PHEV investments only in higher price points. OEM profitability compression from CO2 compliance costs has intensified competitive pricing pressures, particularly in volume segments.

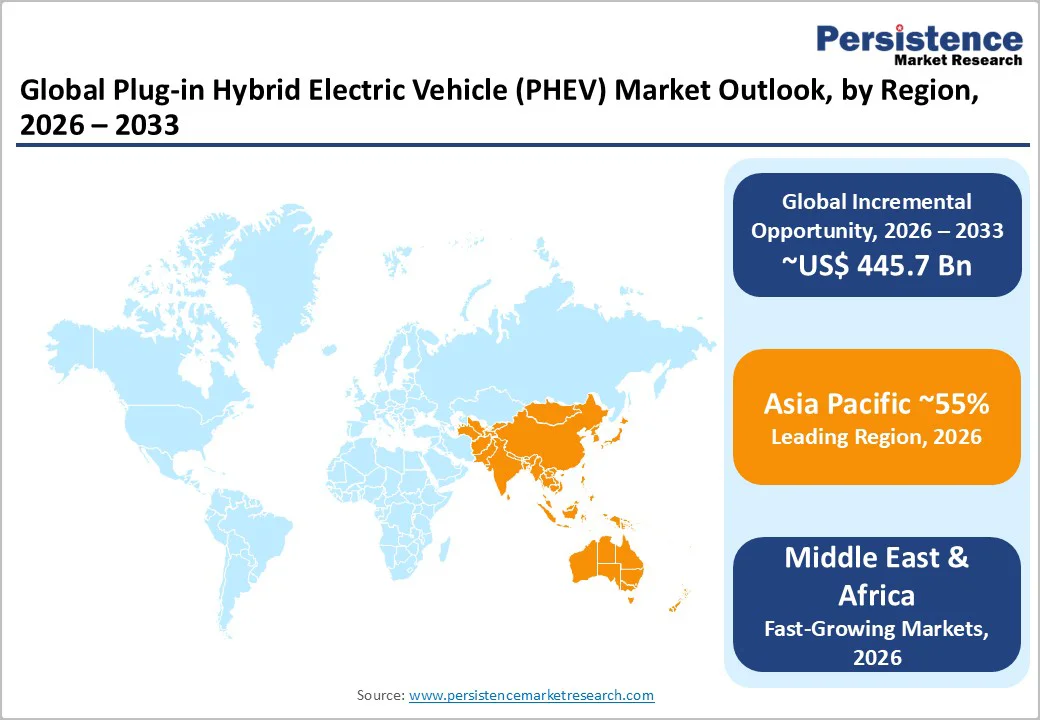

Asia Pacific is the dominant global PHEV region, accounting for 55% of value market share and 75% of volume market share in 2026. This region encompasses diverse market maturity levels and regulatory frameworks, creating heterogeneous growth dynamics requiring nuanced regional analysis.

China: Market Dominance and Technological Leadership

China's PHEV market is valued at US$150 billion in 2026, representing 58% of global market value despite representing 70% of global volume. This value-to-volume disparity reflects an average selling price differential, with Chinese PHEVs predominantly concentrated in mid-market segments (US$20,000-40,000) compared with premium-focused developed markets.

SUVs and crossovers dominate Chinese sales, holding more than 60% of the market share, while small cars represent around 25% of the market, reflecting urban congestion patterns and family vehicle preferences.

Series-parallel architecture is projected to hold around 70% market share by 2033, while range-extender architecture is expected to grow rapidly, reaching around 27% share by 2033. This architectural diversity reflects the Chinese OEMs' focus on innovation and the variability of domestic charging infrastructure, encouraging range-extender adoption in infrastructure-constrained regions.

Southeast Asia: High-Growth Emerging Market

Southeast Asia represents the fastest-growing regional PHEV market, with volume growth projected at over 25% CAGR between 2026 and 2033, substantially exceeding developed market growth rates. The current market size is estimated at US$8 billion and is projected to exceed US$30 billion by 2033. Thailand and Indonesia lead regional adoption, driven by government electrification incentives and strategic OEM localization investments.

Thailand's EV3.5 program and Indonesia's tax breaks create purchase-price incentives that offset affordability barriers. SUVs are the preferred vehicle category, reflecting Indian Ocean climate considerations and variations in infrastructure quality that require robust vehicle platforms.

Chinese OEM market presence, particularly BYD's aggressive regional expansion through partnership models and direct manufacturing investments, is creating market competition advantages based on cost structure and EV expertise.

Mercedes-Benz, Volvo, and other Western OEMs have announced Southeast Asia localization initiatives aimed at tariff reduction and improved affordability. Government investments in charging infrastructure, though nascent, are improving gradually. Regional market maturation is expected to accelerate post-2028 as charging networks approach critical mass thresholds (1 charger per 100-150 vehicles).

India and Japan: Contrasting Market Dynamics

India is a price-sensitive emerging market with nascent PHEV adoption, currently representing <1% of the Asia-Pacific PHEV market. Affordability barriers, power infrastructure limitations, and consumer preference for ICE vehicles in this price-sensitive market constrain market growth.

Regulatory support through production-linked incentive (PLI) schemes targeting EV manufacturing is expected to accelerate gradual adoption. Still, widespread PHEV market penetration requires either a substantial reduction in purchase prices through localization or significant income growth among addressable consumer segments.

Japan and South Korea represent mature markets with PHEV adoption concentrated among affluent consumers. Home-charging orientation and domestic OEM strength (Toyota, Honda, and Nissan) support stable but moderate market growth. South Korea exhibits similar maturity characteristics, with BEV preference trends gradually displacing PHEV market share.

The global plug-in hybrid electric vehicle (PHEV) market exhibits moderate consolidation with BYD, Cherry, Geely-Volvo, Volkswagen Group (including Audi, Porsche, Skoda), and BMW Group collectively accounting for approximately 50% of the global market share in 2026.

Chinese manufacturers, led by BYD (15-18% market share), have rapidly expanded their presence through volume production and competitive pricing. The market structure is characterized by oligopolistic competition with 10-12 major OEMs controlling over 80% of volume, while 40-50 secondary manufacturers compete in niche or emerging market segments.

Growth in the global PHEV market is fueled by tightening CO₂ regulations, declining battery costs, and increasing demand for cleaner, versatile mobility solutions, reinforced by supportive government incentives.

The plug-in hybrid electric vehicle (PHEV) market is forecast to grow from US$266.9 billion in 2026 to US$712.6 billion by 2033, at a CAGR of 15.1%.

Passenger vehicles dominate with over 98% share, led by SUVs and crossovers, while commercial PHEVs remain smaller but the fastest-growing segment.

Asia Pacific leads in volume and value, driven by China and fast-growing Southeast Asia, while Europe and North America remain key regulated, high-value markets.

High upfront prices versus ICE vehicles and uneven charging infrastructure, especially in emerging markets, remain the primary barriers to broader PHEV adoption.

| Report Attribute | Details |

|---|---|

| Historical Data/Actuals | 2020 - 2025 |

| Forecast Period | 2026 - 2033 |

| Market Analysis | Value: US$ Bn |

| Geographical Coverage |

|

| Segmental Coverage |

|

| Competitive Analysis |

|

| Report Highlights |

|

By Architecture

By Vehicle Type

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author