- Pharmaceuticals

- Uterine Cancer Diagnostic Testing Market

Uterine Cancer Diagnostic Testing Market Size, Share, Growth, and Regional Forecast, 2025 to 2033

Uterine Cancer Diagnostic Testing Market by Cancer Type (Endometrial Carcinoma, Uterine Sarcoma), by Diagnostic Test (Ultrasound Scanning, Biopsy Procedures, Blood Tests), End-user, Regional Analysis, from 2026 to 2033

Uterine Cancer Diagnostic Testing Market Share and Trends Analysis

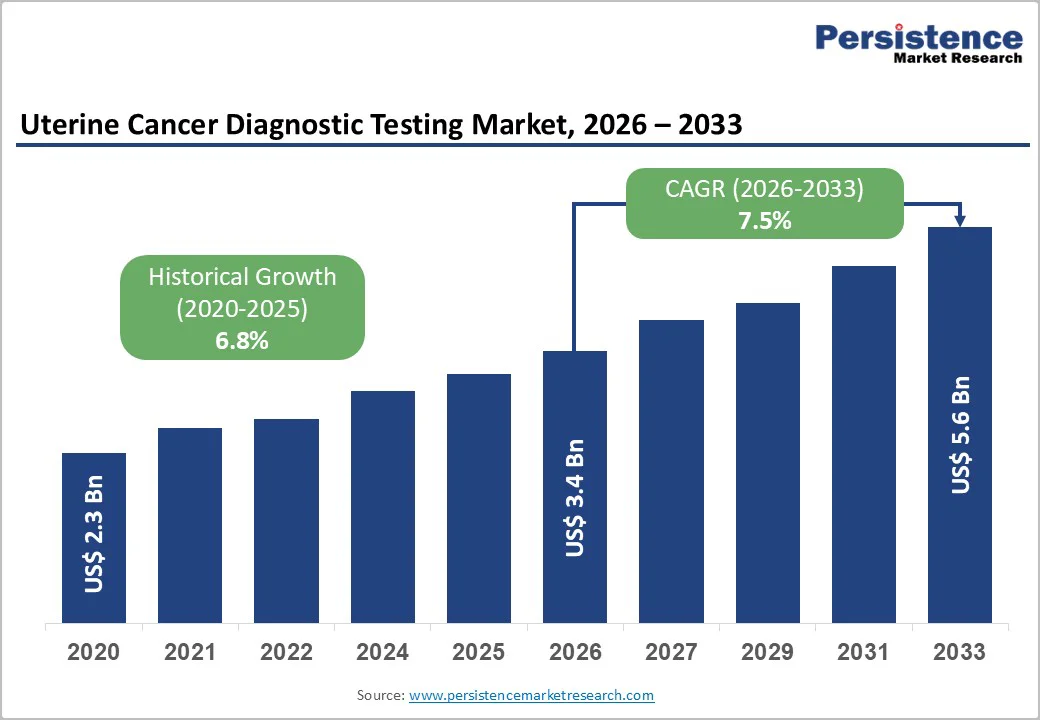

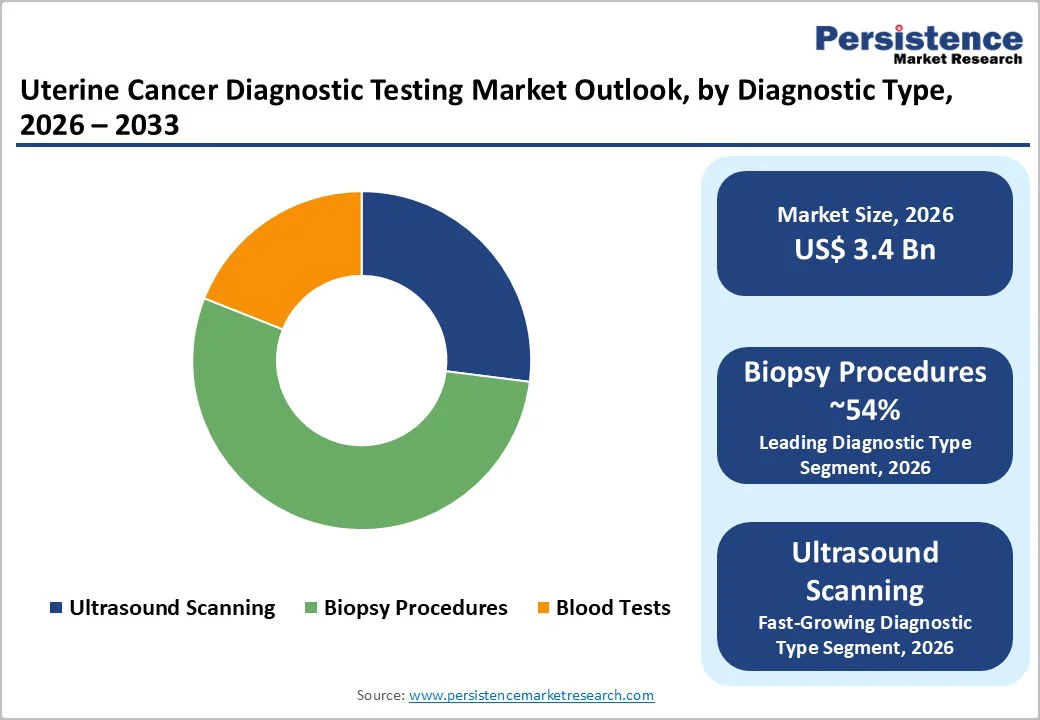

The global uterine cancer diagnostic testing market is estimated to grow from US$ 3.4 billion in 2026 to US$ 5.6 billion by 2033. The market is projected to record a CAGR of 7.5% during the forecast period from 2026 to 2033.

Uterus a female organ also referred to as the womb, is located in the lower abdomen. It supports fetal development until birth. Uterine cancer is the malignant growth of cells comprised of uterine tissues. Uterine cancer is of two types, namely endometrial carcinoma and uterine sarcoma. Endometrial carcinoma generally occurs in the lining of the uterus, called the endometrium. In contrast, uterine sarcoma develops in the supporting network of the uterus, including tissues, bones, and muscles associated with the uterus.

The risk associated with the development of uterine cancer includes hyperplasia, mostly in women who have never borne a child, obese women, and due to excessive intake of treatment drugs for breast cancer. Endometrial carcinoma is symptomatic in behavior, and the major symptoms include abnormal bleeding from the vagina, pelvic pain, or abrupt vaginal discharge. Unlike endometrial carcinoma, uterine sarcoma is asymptomatic in behavior and is diagnosed at later stages.

Key Industry Highlights

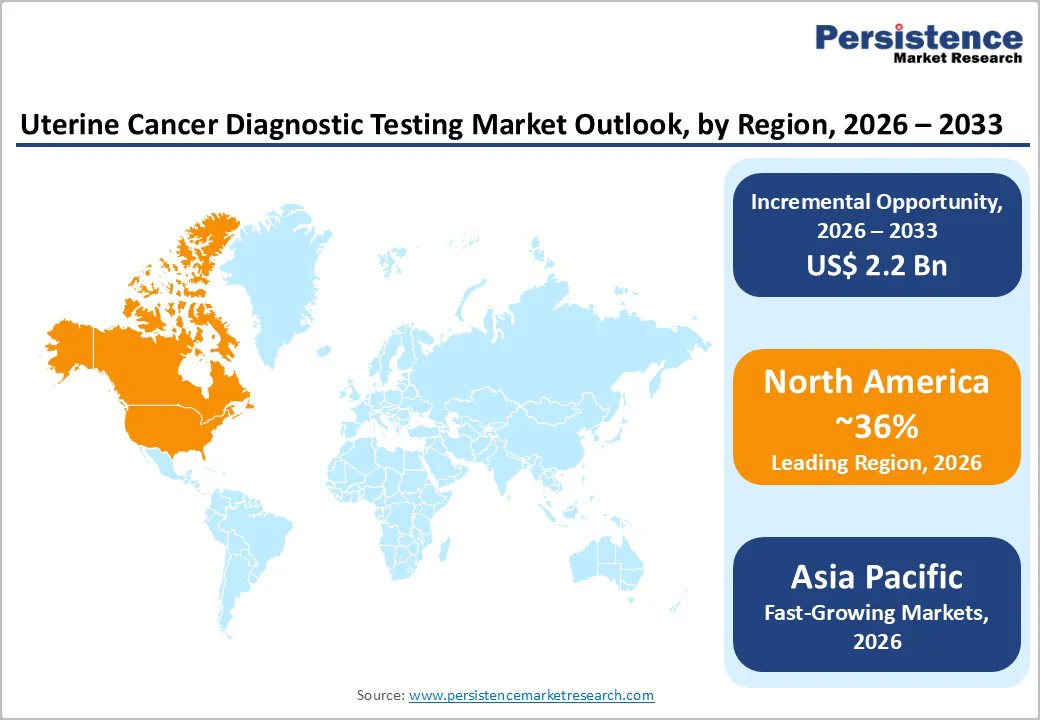

- Leading Region: North America leads the global market with approximately 36% share in 2025, supported by high endometrial carcinoma prevalence, advanced diagnostic infrastructure, and strong reimbursement systems.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by rising awareness of women’s health, improved healthcare infrastructure, and increased

- adoption of minimally invasive diagnostic procedures.

- Dominant Segment: Endometrial Carcinoma remains the dominant segment due to its high prevalence, guideline-directed diagnostic protocols, and widespread use of transvaginal ultrasound and biopsy procedures.

- Fastest-Growing Segment: Uterine sarcoma is the fastest-growing segment, driven

- by increasing the adoption of advanced imaging, molecular profiling, and specialized pathology for aggressive subtypes.

| Key Insights | Details |

|---|---|

| Uterine Cancer Diagnostic Testing Market Size (2026E) | US$ 3.4 Bn |

| Market Value Forecast (2033F) | US$ 5.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.8% |

Market Dynamics

Driver - Standardized Diagnostic Pathways Driving Uterine Cancer Testing Demand

The growth of the uterine cancer diagnostic testing market is strongly supported by the increasing clinical reliance on structured diagnostic pathways, in which ultrasound scanning serves as the initial assessment tool. Both abdominal and transvaginal ultrasound procedures enable non-invasive visualization of the uterus and ovaries, helping clinicians detect abnormal endometrial thickening or other suspicious lesions. Ultrasound scanning is widely adopted owing to its lower cost, easy accessibility in hospital settings, and ability to guide next-level confirmatory tests. Its continued use as a standard first-line assessment, particularly in symptomatic women with post-menopausal bleeding, is a significant factor fueling testing demand globally.

Market growth is also driven by increasing utilization of confirmatory diagnostic procedures such as endometrial biopsy, hysteroscopy, and dilation & curettage. These procedures remain essential for establishing definitive evidence of malignancy and guiding treatment decisions. Combined biopsy-based approaches are used to retrieve malignant tissue samples for histopathological evaluation, making them indispensable in clinical workflows. Additionally, blood-based diagnostic tests, such as a complete blood count and CA125 tumor marker evaluation, further support early screening, monitoring progression, and treatment follow-up. As adoption of these tests rises across oncology centers, women's health clinics, and specialty diagnostic laboratories, demand for uterine cancer testing solutions is expected to increase, reinforcing market expansion.

Restraints - Ambiguous Early-Stage Symptoms and Infrastructure-Based Diagnostic Gaps

Early-stage uterine cancer often presents with nonspecific symptoms such as irregular bleeding, abdominal discomfort, or pelvic pressure, which resemble benign gynecological conditions like fibroids or hormonal imbalance. As there is no routine screening test for asymptomatic women, disease onset frequently goes unnoticed, delaying testing and diagnosis until symptoms worsen. Early diagnostic pathways also face reliability challenges, as certain imaging modalities or biopsies may misinterpret borderline abnormalities, leading to false positives or false negatives. This reduces diagnostic confidence and often necessitates repeat testing, increasing cost and care delays.

Diagnostic restraints are further aggravated by uneven healthcare infrastructure across regions. Access to advanced modalities such as transvaginal ultrasound, hysteroscopy-guided biopsy, and CA125-based testing varies significantly between urban and rural facilities. Limited specialist availability restricts timely evaluation, particularly in developing markets where diagnostic wait times are longer. Financial constraints and low awareness further discourage early testing. Combined, these challenges slow patient flow into diagnostic programs, restraining market penetration and adoption of advanced testing platforms.

Opportunity - Liquid Biopsy and AI-Integrated Imaging Expansion

Advancements in liquid biopsy technologies are enabling the detection of circulating tumor DNA, circulating tumor cells, and tumor-specific methylation patterns in blood samples. These approaches provide non-invasive alternatives to conventional biopsy, making them suitable for mass screening and longitudinal monitoring. Validation studies demonstrating strong sensitivity for early-stage endometrial malignancies are reinforcing adoption pathways across cancer research centers, ambulatory surgery units, and diagnostic labs. At the same time, clinical guidelines increasingly emphasize molecular profiling to support treatment planning, encouraging laboratories to invest in assays aligned with subtype classification. This shift is expanding demand for companion diagnostics and high-accuracy blood-based screening kits.

AI-supported imaging platforms are emerging as an additional driver, particularly for ultrasound and MRI interpretation. Automated identification of suspicious tissue patterns reduces variability in manual reporting and enhances clinical decision-making. Hospitals seeking faster turnaround times and standardized readings are integrating AI-enabled systems into diagnostic workflows. The Asia-Pacific region presents a strategic growth channel, as local manufacturing ecosystems in India and China enable the production of affordable testing systems. Scalable deployment of low-cost platforms, combined with rising awareness of early-onset uterine cancer, is expected to accelerate market uptake.

Category-wise Analysis

By Cancer Type Insights

Endometrial carcinoma dominates the cancer type segment of the uterine cancer diagnostic testing market, capturing an 83% share in 2025. Epidemiological data show that it accounts for most uterine malignancies, with SEER reporting an age-adjusted incidence of 26-28 cases per 100,000 women, far exceeding the prevalence of uterine sarcoma, which represents less than 10% of cases. Endometrial carcinoma is primarily of endometrioid histology (79-87%) and typically presents with abnormal uterine bleeding, prompting early evaluation via transvaginal ultrasound and biopsy. Diagnostic protocols from ESGO, ESTRO, and ESP recommend molecular classification for the majority of endometrioid tumors, thereby reinforcing the demand for laboratory testing. Although uterine sarcoma remains rare, it is projected to be the fastest-growing segment due to increased adoption of advanced imaging and molecular profiling for aggressive subtypes, creating opportunities for specialized diagnostic platforms and companion tests in tertiary care centers and research institutions.

By Diagnostic Test Insights

Biopsy procedures dominate the diagnostic test segment, holding approximately 54% share in 2025, as they provide definitive histopathological confirmation of uterine cancer. ACOG and NCCN widely recommend endometrial biopsy and dilation and curettage following abnormal findings on ultrasound, with office-based sampling sufficient in over 90% of cases. Hysteroscopy is advised for focal lesions, especially for atypical hyperplasia, delivering a higher diagnostic yield with sensitivity exceeding 95%. The procedural reliance on biopsy, combined with rising incidence rates (around 1.74% annually), ensures sustained demand over imaging or blood tests, which are often less specific for confirmatory diagnosis. The growth of minimally invasive biopsy techniques and integration with molecular testing further strengthens adoption, supporting both early detection and precise tumor characterization. Imaging and blood-based modalities complement biopsies but remain secondary due to limited specificity in confirming uterine malignancies.

Region-wise Insights

North America Uterine Cancer Diagnostic Testing Market Trends

North America, led by the U.S., represents the largest regional market for uterine cancer diagnostic testing, driven by high disease prevalence, advanced healthcare infrastructure, and strong reimbursement systems. SEER data indicate endometrial carcinoma incidence rates of 26-28 cases per 100,000 women, contributing to a substantial patient pool requiring timely screening and confirmatory testing. The region benefits from the widespread adoption of first-line diagnostic tools, such as transvaginal ultrasound and blood-based tumor markers, complemented by biopsy procedures, including endometrial sampling, hysteroscopy, and dilation & curettage.

Advanced molecular diagnostics, guided by ESGO, ESTRO, and ESP protocols, are increasingly implemented for tumor subtyping, enhancing precision in treatment planning. The presence of leading diagnostic and biotechnology companies, such as Abbott Laboratories, Roche, Siemens Healthineers, and Becton Dickinson, supports the rapid deployment of both conventional and innovative diagnostic solutions. Continuous investment in research and clinical trials, coupled with growing awareness of early detection, is further reinforcing market growth. Additionally, integration of AI-assisted imaging and liquid biopsy platforms is accelerating adoption, improving diagnostic accuracy and workflow efficiency across hospitals, outpatient clinics, and specialized laboratories.

Asia Pacific Uterine Cancer Diagnostic Testing Market Trends

Asia Pacific uterine cancer diagnostic testing market is expanding rapidly due to the rising incidence of endometrial carcinoma, improving healthcare infrastructure, and increasing awareness of women’s health issues. Countries such as China, India, Japan, South Korea, and Australia are witnessing growing adoption of ultrasound scanning, biopsy procedures, and blood-based tumor marker tests for early detection and confirmatory diagnosis. Limited access to advanced diagnostic technologies in rural and semi-urban areas has historically restrained market growth. Still, investments in modern diagnostic labs, telemedicine, and mobile health units are improving coverage. The prevalence of early-onset uterine cancer among women under 50 is driving demand for molecular subtyping and minimally invasive procedures. Government initiatives and private hospital expansion are enabling wider access to cost-effective diagnostic solutions.

Additionally, regional manufacturing hubs in China and India are supporting scalable deployment of ultrasound equipment, reagents, and biopsy kits at lower costs, increasing affordability. Rising awareness campaigns, educational programs, and growing insurance penetration are further accelerating the adoption of comprehensive diagnostic testing, positioning the Asia Pacific as one of the fastest-growing markets globally.

Market Competitive Landscape

The market features consolidated leadership by diagnostics giants like Roche Holdings AG, Siemens AG, Abbott Laboratories, and Danaher, amid fragmented pathology providers. Leaders pursue R&D in AI-imaging and NGS panels, partnering for ESGO-aligned trials; differentiators include integrated platforms for biopsy-to-molecular workflows. Expansion targets the Asia Pacific via local manufacturing.

Key Industry Developments:

- In November 2025, Promega received FDA approval for its microsatellite instability testing technology as a companion diagnostic for Merck and Eisai’s Keytruda-Lenvima therapy in advanced endometrial carcinoma patients.

- In July 2025, Gnosis launched EdenDx in the U.S., the first commercially available non-invasive, liquid-based cytology test for early-stage endometrial cancer detection.

- In April 2022, the U.S. FDA granted approval to Roche Holding AG’s VENTANA MMR RxDx Panel for endometrial cancer diagnostics.

Companies Covered in Uterine Cancer Diagnostic Testing Market

- Abbott Laboratories

- Roche Holdings AG

- Siemens AG

- Danaher

- BioMerieux SA

- Sanofi

- Becton, Dickinson & Co.

- GlaxoSmithKline Plc

- Merck & Co., Inc.

- Novartis AG

- Others

Frequently Asked Questions

The global uterine cancer diagnostic testing market is projected to be valued at US$ 3.4 Bn in 2026.

Rising endometrial cancer cases, adoption of molecular diagnostics, early detection focus, improved reimbursement, and technological advancements accelerating diagnosis accuracy.

The global market is poised to witness a CAGR of 7.5% between 2026 and 2033.

Growing demand for minimally invasive tests, biomarker-based assays, liquid biopsies, digital pathology expansion, and diagnostics adoption in emerging regional healthcare systems.

Major players include Abbott Laboratories, Roche Holdings AG, Siemens AG, Danaher, BioMerieux SA, Becton Dickinson & Co., Merck & Co., Inc., Novartis AG, Hologic Inc., GE HealthCare.