- Medical Devices

- U.S. Scalp Cooling Systems Market

U.S. Scalp Cooling Systems Market Size, Share, and Growth Forecast, 2026 - 2033

U.S. Scalp Cooling Systems Market by Product Type (Manual Cooling Systems/Cold Gel Caps, Automated Cooling Systems), Sales Type (Direct Sales, Rental Sales), End-user (Hospitals, Specialty Clinics, Others), and Zone Analysis for 2026 - 2033

U.S. Scalp Cooling Systems Market Size and Trends Analysis

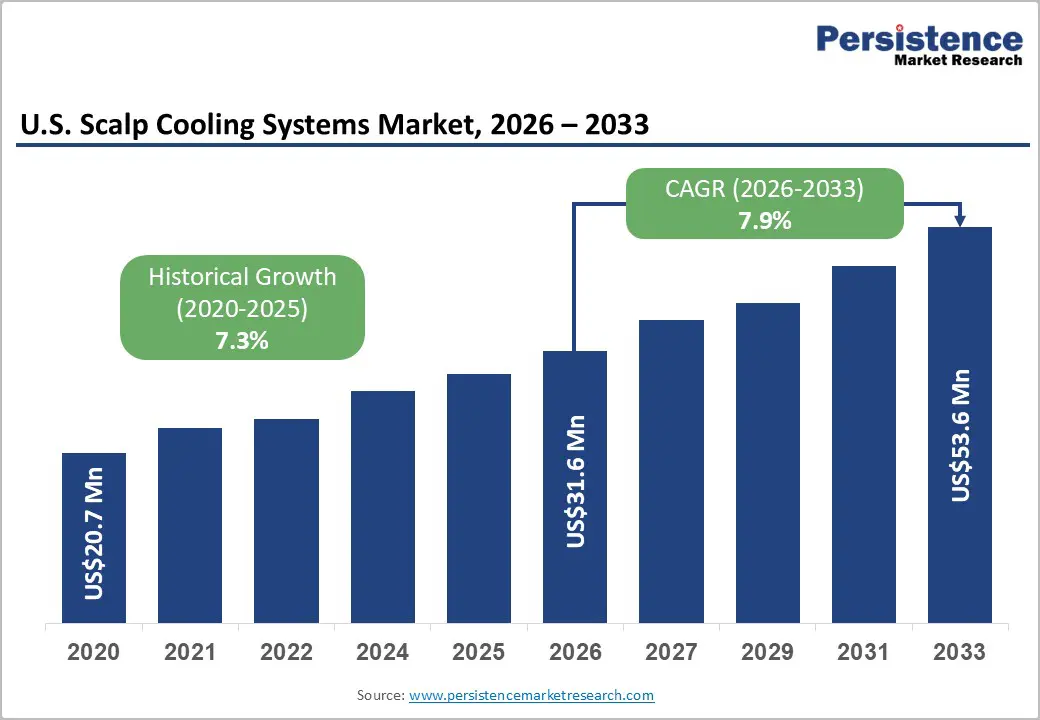

The U.S. scalp cooling systems market size is likely to be valued at US$31.6 million in 2026 and is expected to reach US$53.6 million by 2033, growing at a CAGR of 7.9% during the forecast period from 2026 to 2033, driven by rising adoption of supportive oncology care and increasing awareness regarding chemotherapy-induced alopecia (CIA).

According to the American Cancer Society, scalp cooling remains the only FDA-cleared approach to reduce chemotherapy-related hair loss, with automated and manual systems increasingly utilized across oncology centers. In 2025, a PubMed meta-analysis reported that CIA affects nearly 65% of chemotherapy patients, reinforcing demand for scalp cooling therapies. Manual cold cap systems continue to maintain strong demand because of affordability and accessibility, while automated systems are gaining traction due to improved temperature precision and clinical efficiency.

Key Industry Highlights:

- Leading Product Type: Manual cooling systems/cold gel caps are projected to represent the leading product type in 2026, accounting for 72% of the revenue share, driven by their affordability and wider accessibility.

- Leading Sales Type: Rental sales are anticipated to be the leading sales type, accounting for over 84% of the revenue share in 2026, owing to lower upfront costs and higher patient accessibility.

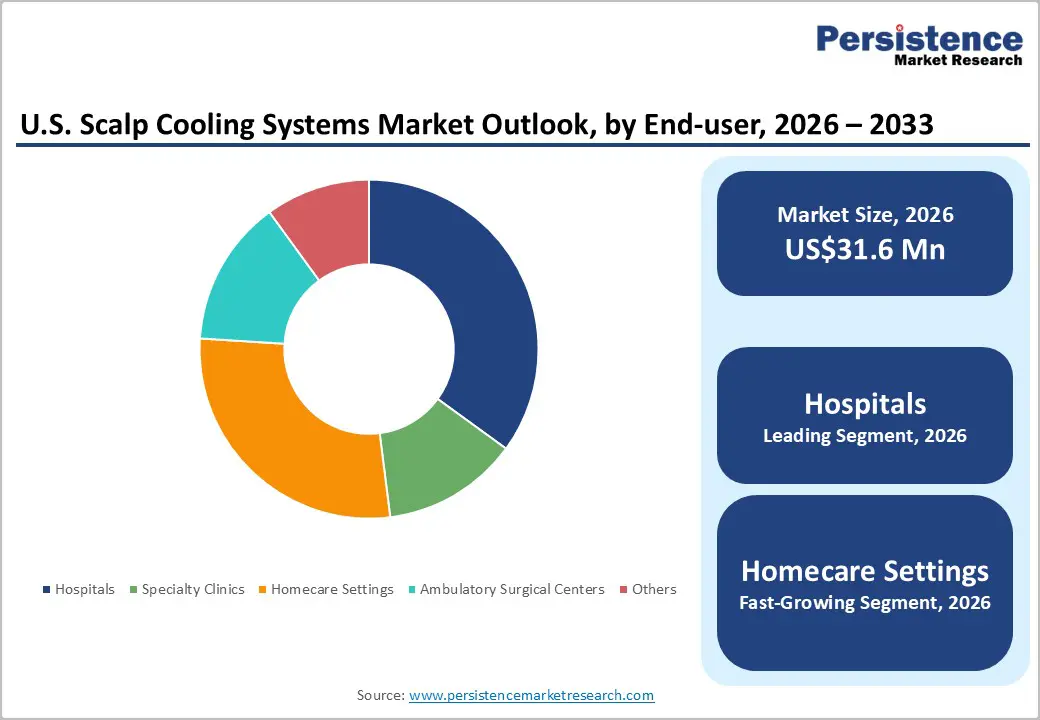

- Leading End- user: Hospitals are estimated to represent the leading end- user in 2026, accounting for 46% of the revenue share, as they remain the primary centers for chemotherapy treatment.

- Key Opportunity: Increasing integration of scalp cooling systems into mainstream oncology care, supported by expanding reimbursement policies and rising patient demand for quality-of-life preservation during chemotherapy, presents a significant growth opportunity for the U.S. scalp cooling systems market.

DRO Analysis

Driver - Rising Incidence of Cancer and Demand for Supportive Care

The increasing prevalence of cancer in the U.S. is significantly driving demand for scalp cooling systems across oncology care settings. According to the American Cancer Society, breast cancer remains one of the most diagnosed cancers among women, resulting in a growing number of chemotherapy procedures annually. Chemotherapy-induced alopecia continues to affect a substantial proportion of patients, creating strong demand for supportive treatments that improve emotional well-being and quality of life.

Hospitals and oncology clinics are increasingly integrating scalp cooling technologies into treatment programs to address patient concerns regarding hair loss. Growing awareness campaigns and patient advocacy initiatives are accelerating the adoption of scalp cooling therapies nationwide steadily. The market is also benefiting from the broader expansion of supportive oncology care services across the U.S. healthcare system.

Cancer treatment providers are increasingly emphasizing patient-centered care, including solutions that minimize treatment-related side effects and improve psychological confidence during chemotherapy. Automated scalp cooling systems are gaining traction because they provide consistent temperature control and improved treatment outcomes in busy oncology centers. Rising collaboration between device manufacturers, hospitals, and cancer foundations is improving product accessibility and awareness.

Restraint - Limited Clinical Awareness and Provider Training

Many oncology professionals continue to prioritize primary cancer treatment over supportive therapies, resulting in inconsistent recommendations for scalp cooling during chemotherapy sessions. In several community hospitals and smaller infusion centers, healthcare staff lack specialized training regarding device operation, patient eligibility, and scalp cooling protocols.

Misconceptions regarding effectiveness across different chemotherapy regimens continue to create hesitation among providers, limiting the broader implementation of scalp cooling systems across numerous healthcare facilities nationwide. Operational complexity and workflow challenges restrict widespread adoption among healthcare providers and treatment centers. Scalp cooling procedures require additional preparation time, monitoring, and coordination during chemotherapy administration, which may increase workload pressures for oncology staff.

Facilities without dedicated supportive care resources often face difficulties integrating scalp cooling systems into routine clinical operations efficiently. Some patients remain unaware of scalp cooling availability before beginning chemotherapy treatment, reducing utilization opportunities. The absence of standardized educational programs and limited exposure during oncology training also contribute to inconsistent adoption patterns.

Opportunity - Expansion of Insurance Mandates and Reimbursement

Increasing recognition of chemotherapy-induced alopecia as an important quality-of-life issue is encouraging insurers and policymakers to improve financial coverage for scalp cooling therapies. Several U.S. states have introduced legislation requiring insurance providers to include scalp cooling reimbursement within cancer treatment benefits. These policy developments can significantly reduce patient out-of-pocket costs while encouraging broader adoption of scalp cooling systems across healthcare facilities nationwide steadily.

Improved reimbursement pathways are also expected to encourage investments from hospitals, specialty clinics, and device manufacturers operating within the supportive oncology care segment. Healthcare providers are more likely to integrate scalp cooling technologies when reimbursement mechanisms support operational costs and patient affordability.

Expanding insurance coverage can increase access among middle-income and underserved patient populations previously unable to afford treatment. Manufacturers are strengthening partnerships with healthcare systems and advocacy organizations to expand awareness regarding reimbursement eligibility and treatment availability. These developments create strong long-term opportunities for market expansion, particularly as patient demand for supportive and personalized oncology care continues to rise.

Category-wise Analysis

Product Type Insights

Manual cooling systems/cold gel caps are expected to lead the U.S scalp cooling systems market, accounting for approximately 72% of revenue share in 2026, driven by their affordability, accessibility, and suitability for flexible treatment environments. These systems are widely preferred among patients seeking lower-cost supportive care solutions during chemotherapy treatment, especially in homecare settings and smaller oncology centers where advanced infrastructure is limited.

Their portability and ease of application make them practical for outpatient treatment programs and independent patient use. A notable example includes Penguin Cold Caps, which has expanded its presence among breast cancer patients by offering personalized manual scalp cooling support programs.

Automated cooling systems are likely to represent the fastest-growing segment in 2026, supported by increasing adoption across hospitals, infusion centers, and specialized oncology clinics. These systems are gaining strong acceptance because they provide precise temperature regulation, consistent scalp coverage, and improved treatment efficiency during chemotherapy sessions.

For example, Paxman, whose FDA-cleared automated scalp cooling technology has been adopted by multiple U.S. cancer treatment centers to improve supportive care services. Technological advancements such as user-friendly interfaces, improved patient comfort, and integrated monitoring systems are also supporting segment growth.

Sales Type Insights

Rental sales are projected to lead the market, capturing around 84% of the revenue share in 2026, supported by their cost-effective structure and wider accessibility for patients and healthcare providers. Rental-based models significantly reduce the financial burden associated with purchasing scalp cooling equipment outright, making supportive oncology care more attainable for a broader patient population.

For example, Dignitana AB has expanded its service-based business approach through scalable rental programs for oncology facilities. Increasing demand for affordable supportive cancer care solutions and flexible financing models continues to reinforce the dominance of the rental sales segment.

Direct sales are likely to be the fastest-growing sales type in 2026, driven by larger healthcare networks increasingly investing in permanent scalp cooling infrastructure. Growing confidence in scalp cooling efficacy, expanding patient demand, and improved reimbursement frameworks are encouraging hospitals and specialty oncology centers to purchase dedicated systems for long-term clinical use.

A notable example includes Paxman, which continues expanding partnerships with U.S. hospitals through direct installation of automated scalp cooling systems. Healthcare organizations are also prioritizing advanced supportive oncology services to strengthen patient satisfaction and competitive positioning within cancer care delivery.

End-user Insights

Hospitals are estimated to lead the U.S. scalp cooling systems market, accounting for approximately 46% of revenue in 2026, due to their role as primary chemotherapy treatment centers with advanced oncology infrastructure. Most cancer patients receive chemotherapy within hospital-based oncology departments, making hospitals the largest adopters of scalp cooling technologies across the country.

These facilities possess the trained healthcare professionals, infusion systems, and operational capacity necessary to integrate scalp cooling procedures into routine cancer treatment protocols effectively. For example, the Mayo Clinic has incorporated scalp cooling therapies into supportive cancer care services for chemotherapy patients. Increasing emphasis on supportive oncology care and patient quality of life is encouraging hospitals to expand scalp cooling services as part of comprehensive cancer treatment programs.

Homecare settings are likely to represent the fastest-growing segment, driven by rising patient preference for convenience, comfort, and personalized treatment support during chemotherapy. Increasing awareness regarding hair preservation therapies and the growing availability of portable manual cooling solutions are encouraging more patients to utilize scalp cooling outside traditional clinical environments.

For instance, Wishcaps which provides customized cold cap support services designed for patients managing chemotherapy treatment in home environments. Manual cold cap systems are particularly suitable for homecare settings because they do not require sophisticated infrastructure or continuous supervision. Expanding telehealth support and patient education initiatives are also contributing to higher adoption of homecare scalp cooling therapies nationwide.

Competitive Landscape

The U.S. scalp cooling systems market exhibits a moderately fragmented structure, driven by increasing demand for supportive oncology care, technological advancements in scalp cooling devices, and expanding adoption across hospitals and specialty cancer centers. The market is characterized by the presence of both automated scalp cooling system providers and manual cold cap solution companies competing to strengthen their clinical presence and patient support services. Growing awareness regarding chemotherapy-induced alopecia and improving reimbursement frameworks are encouraging companies to expand partnerships with oncology clinics and healthcare networks across the U.S.

With key leaders, including Paxman, Dignitana AB, Penguin Cold Caps, Wishcaps, and Cooler Heads Care, Inc., the competitive environment continues evolving through product innovation and strategic healthcare collaborations. These players compete through advanced cooling technologies, expansion of rental-based service models, wider distribution partnerships, and improved patient comfort solutions. Several manufacturers are also focusing on portable and easy-to-use systems suitable for both hospital and homecare settings.

Key Industry Developments:

- In March 2026, Paxman announced that 11 U.S. states were pursuing legislation to mandate insurance coverage for scalp cooling therapy, highlighting growing reimbursement support and expanding patient access to chemotherapy-induced hair loss prevention treatments across the country.

- In November 2025, Paxman announced that the U.S. Centers for Medicare & Medicaid Services finalized 2026 Medicare payment rates and new Category I CPT codes for mechanical scalp cooling, strengthening reimbursement support and expanding provider access to chemotherapy-induced hair loss prevention treatments in the United States.

- In July 2025, Cooler Heads Care, Inc. secured US$11 million in Series A funding to expand manufacturing and commercialization of its FDA-cleared Amma portable scalp cooling system designed to reduce chemotherapy-induced hair loss among cancer patients.

Companies Covered in U.S. Scalp Cooling Systems Market

- Paxman

- Dignitana AB

- Wishcaps

- Penguin Cold Caps

- Arctic Cold Caps LLC

- Chemotherapy Cold Caps, Inc.

- Warrior Caps

- Polar Cold Caps, LLC.

- Cooler Heads Care, Inc.

Frequently Asked Questions

The U.S. scalp cooling systems market is projected to reach US$31.6 million in 2026.

The U.S. scalp cooling systems market is driven by rising cancer incidence, growing awareness of chemotherapy-induced alopecia management, and increasing adoption of supportive oncology care solutions.

The U.S. scalp cooling systems market is expected to grow at a CAGR of 7.9% from 2026 to 2033.

Key opportunities lie in expanding insurance reimbursement coverage, increasing hospital adoption of automated scalp cooling systems, and growing demand for homecare-based supportive cancer therapies.

Paxman, Dignitana AB, Wishcaps, Penguin Cold Caps, Arctic Cold Caps LLC, and Chemotherapy Cold Caps, Inc., are the leading players.