- Home Care & Utilities

- Textile Flooring Market

Textile Flooring Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Textile Flooring Market by Product Type (Rugs and Carpets), Material Type (Synthetic Textiles Animal Textiles, and Plant Textiles), Technology (Tufting, Woven, and Needlefelt), Application (Residential, Commercial, and Others (Industrial)), and Regional Analysis from 2026 to 2033

Textile Flooring Market Size and Share Analysis

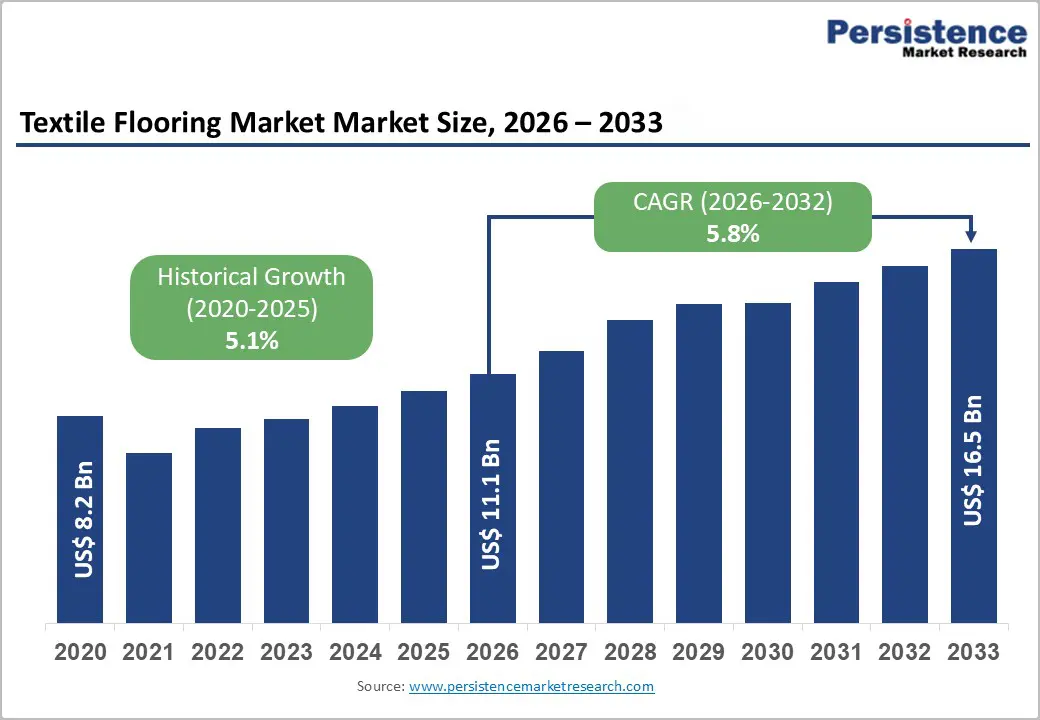

The global textile flooring market size is likely to be valued at US$ 11.1 billion in 2026 and is projected to reach US$ 16.5 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

The textile flooring market is experiencing robust growth driven primarily by the rise in consumer demand for sustainable and eco-friendly flooring options and the flourishing construction and real estate industries, particularly in developing economies experiencing rapid urbanization. Rising disposable incomes in emerging markets are enabling consumers to prioritize interior aesthetics and comfort, driving the adoption of premium textile flooring products.

Key Market Highlights

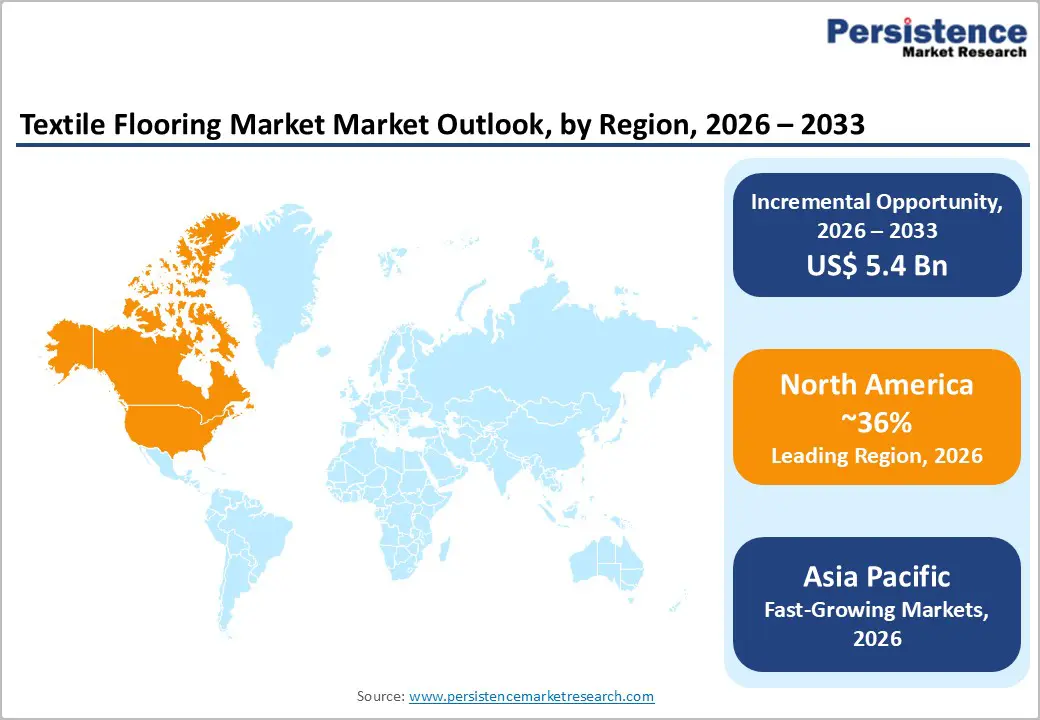

- Leading Region: North America, is poised for the largest market position, contributing approximately 36.9% of global market value through established manufacturing infrastructure, extensive distribution networks, and consumer preference for quality interior furnishings.

- Fastest Growing Region: Asia-Pacific emerges as the fastest-growing regional market, expanding at approximately 8.2% CAGR through 2030, driven by rapid urbanization, rising disposable incomes, government infrastructure investments, and manufacturing expansion.

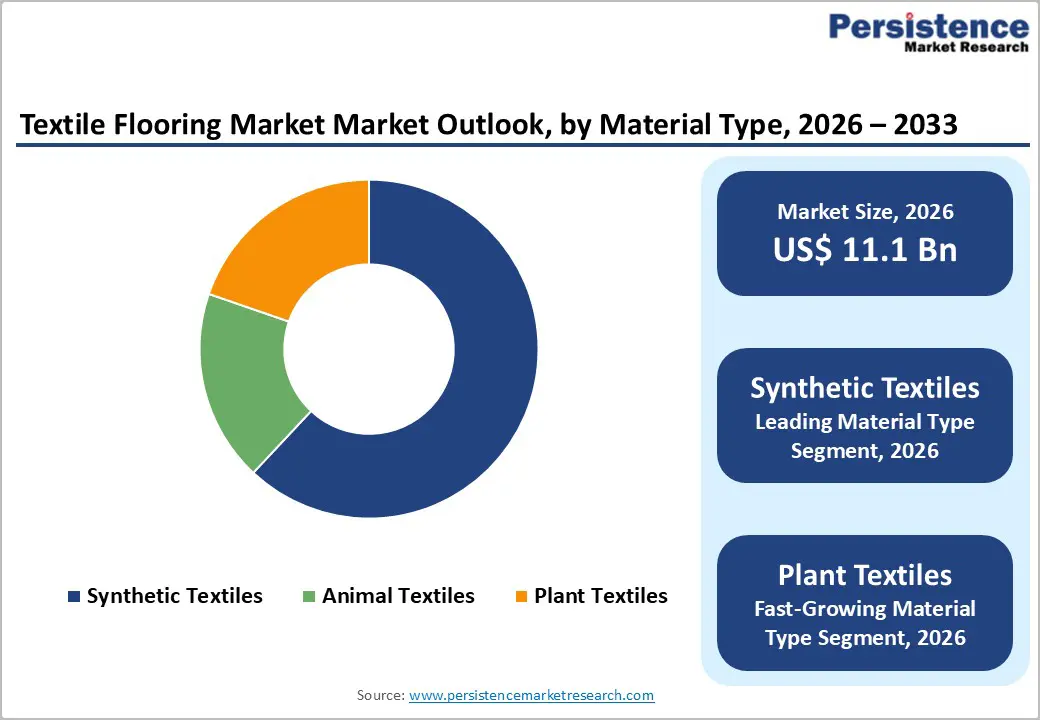

- Dominant Material Type: Synthetic textiles, including nylon, polyester, and polypropylene, command dominant market positioning with approximately 37.2% market share through superior durability, stain resistance, and cost-effectiveness.

- Fastest Growing Technology: Tufted carpets represent the fastest-growing technology segment, anticipated to expand at approximately 9.3% CAGR through 2034, driven by cost efficiency, rapid production capability, design versatility, and consumer preference.

- Key Market Opportunity Sustainable material adoption and smart flooring technology integration represent the highest-potential market opportunity, driven by environmental consciousness, occupancy optimization demands, and health and safety monitoring requirements.

| Key Insights | Details |

|---|---|

| Global Textile Flooring Market Size (2026E) | US 11.1 Bn |

| Market Value Forecast (2033F) | US$ 16.5 Bn |

| Projected Growth CAGR(2026 - 2033) | 5.8% |

| Historical Market Growth (2020 - 2025) | 5.1% |

Market Dynamics

Drivers - Rising Demand for Sustainable and Eco-Friendly Flooring Solutions

Environmental consciousness is fundamentally reshaping the textile flooring industry as consumers increasingly prioritize sustainable products that minimize environmental impact without compromising quality or aesthetics. Manufacturers are responding by developing flooring products from naturally durable and eco-friendly materials including organic cotton, coconut fibers, bamboo, wool, and silk. These materials require significantly less irrigation and chemical inputs during cultivation compared to conventional alternatives, resulting in reduced greenhouse gas emissions throughout the production lifecycle.

Natural fiber carpets, particularly wool and sisal-based options, are gaining substantial traction due to their longevity and renewable characteristics. Wool carpets can withstand decades of continuous foot traffic without significant degradation, enabling consumers to make one-time investments that reduce lifetime environmental impact and waste generation. The rise of green-building certifications such as LEED and BREEAM is motivating commercial buyers to increasingly specify low-VOC, recyclable, and bio-based flooring materials. Many manufacturers are also incorporating circular design principles, including take-back programs and recyclable backing systems, further strengthening the market shift toward fully sustainable textile flooring solutions.

Expanding Construction and Real Estate Sector Growth in Developing Economies

Rapid urbanization and construction activities in emerging markets, particularly across Asia-Pacific, India, and Africa, are creating substantial opportunities for textile flooring manufacturers. The construction industry in Asia Pacific is anticipated to witness significant expansion, with countries including China, India, Indonesia, and Vietnam leading infrastructure development initiatives. According to industry reports, China maintains dominance in flooring manufacturing with approximately 36.4% regional revenue share, while India is emerging as a critical hub for hand-knotted and tufted carpet production with operations concentrated in regions such as Rajasthan and Uttar Pradesh.

Rising income levels in these developing economies are allowing consumers to transition from conventional flooring materials to textile flooring options that offer superior aesthetic appeal and acoustic benefits. Government initiatives promoting affordable housing and smart city development are driving demand for economically viable textile flooring solutions that meet construction timelines and budget constraints.

Market Restraints

Stringent Environmental Regulations and Market Competition

Increasingly strict environmental regulations regarding synthetic material production, polymer processing, and chemical usage impose substantial compliance costs on textile flooring manufacturers. Governments across developed regions are implementing rigorous standards for volatile organic compound (VOC) emissions, chemical usage, and waste management, necessitating significant investments in manufacturing technology upgrades and process modifications. Simultaneously, the global textile flooring market faces intense competition among established multinational players, preventing manufacturers from substantially increasing prices even during commodity market upturns. This competitive pressure constrains profit margins and limits resources available for research and development initiatives, potentially slowing innovation and market expansion, particularly for smaller manufacturers lacking economies of scale.

Opportunity - Rapid Expansion of Modular Carpet Solutions and Flexible Workspace Concepts

The growing adoption of modular carpet tiles across commercial environments is a significant opportunity in the global textile flooring market. Organizations are increasingly shifting away from traditional broadloom carpets in favor of modular solutions that offer superior flexibility, easy maintenance, and reduced lifecycle costs. This presents strong growth potential for manufacturers that can provide versatile, high-quality tile formats tailored to the needs of offices, hospitality spaces, educational institutions, airports, and healthcare facilities. The ability to replace individual tiles, rather than entire floor sections, reduces operational disruptions and enhances long-term cost efficiency, making these products highly attractive for renovation-driven markets.

The rise of agile workplaces and hybrid office layouts is driving demand for flooring systems that can adapt to evolving spatial configurations, enabling suppliers of modular carpet tiles to tap into new design and layout trends. With many commercial buyers prioritizing sustainability, manufacturers offering recyclable tiles, low-VOC backings, and circular material options can further strengthen their competitive position. As modular tiles also support rapid installation and creative design possibilities, they represent a substantial opportunity for companies to capture market share in the expanding commercial flooring segment.

Integration of Smart & Functional Textile Flooring

The integration of smart and functional technologies into textile flooring presents a high-value opportunity for manufacturers aiming to differentiate in a competitive market. Advancements in materials science and embedded sensor technologies now enable carpets and textile floorings to offer capabilities far beyond traditional aesthetics and comfort. Smart flooring solutions equipped with pressure or motion sensors can support space utilization analytics, patient monitoring in healthcare facilities, fall detection for elderly care, and interactive customer experiences in retail environments.

Functional enhancements such as antimicrobial treatments, stain-resistant coatings, enhanced thermal insulation, and advanced acoustic-dampening layers are increasingly sought after in commercial buildings, schools, hotels, and residential properties. As demand for healthier indoor environments grows, opportunities are expanding for textile flooring that contributes to air quality improvement through low-VOC materials and dust-capturing fiber structures. Manufacturers that invest in developing intelligent, high-performance flooring systems, integrating IoT compatibility, sustainability, and easy maintenance, can unlock new revenue streams and gain strong traction in specialized applications such as smart buildings, healthcare infrastructure, and premium residential projects.

Category-wise Analysis

Product Type Insights

Carpets represent the dominant product type in the textile flooring market, which hold approximately 60.7% market share due to their heir widespread adoption across both residential and commercial environments. Their popularity stems from several advantages, including superior comfort, acoustic insulation, and broad design versatility. In commercial spaces, such as offices, hotels, retail centers, educational institutions, and healthcare facilities, carpets are preferred for their ability to reduce noise, enhance safety, and create cohesive interior aesthetics. The availability of modular carpet tiles has further strengthened the dominance of carpets by offering easy installation, simplified maintenance, and the flexibility to replace localized sections without disrupting entire areas.

Material Type Insights

The synthetic textiles maintaining dominant market positioning, holding approximately 37.2% market share in 2026 due to their hardwearing performance characteristics well-suited for high-traffic applications. Synthetic fibers including nylon, polyester, and polypropylene are engineered to withstand extensive foot traffic, frequent vacuuming, and intensive cleaning protocols while resisting matting and crushing better than natural alternatives.

Nylon represents the largest synthetic material segment with approximately 41.7% share of the material category, valued for its exceptional resilience, superior stain resistance through solution-dyed processes, and longevity in demanding commercial environments. Polypropylene offers cost-effective performance characteristics with excellent stain resistance and color fastness through solution-dyeing, without water consumption during processing. Among animal textiles, wool maintains approximately 30.88% market share in 2026 valued for premium applications requiring superior durability, comfort, and aesthetic appeal.

Application Insights

The residential application holds approximately 55% of total textile flooring demand, driven by rising home improvement investments, interior design consciousness, and homeowner preference for comfort and aesthetics. Residential consumers increasingly invest in high-quality carpet and rug products to enhance living space appeal and comfort, with premium segments experiencing accelerating growth as disposable incomes rise globally.

Commercial applications account for approximately 45% of market demand, encompassing office spaces, hospitality environments, retail establishments, healthcare facilities, educational institutions, and industrial settings. Commercial buyers prioritize durable, easy-to-maintain, and quickly replaceable flooring solutions, driving adoption of modular carpet tiles and commercial-grade synthetic carpets.

Regional Insights

North America Textile Flooring Market Trends

North America maintains a substantial market position with approximately 36.9% global market share in 2026, supported by well-established distribution channels, strong industrial flooring manufacturing infrastructure, and major fiber producer headquarters concentration in the region. North American manufacturers including Mohawk Industries, Shaw Industries, Tarkett, and Beaulieu International Group benefit from tight supply chain management, economies of scale, and proximity to keydistribution networks enabling cost-effective delivery.

Consumer awareness regarding environmentally-friendly flooring alternatives continues expanding, with growing demand for products meeting LEED certification standards and demonstrating sustainable sourcing practices. Substantial spending on interior design and home renovation projects, though moderated by mortgage rate pressures, continues supporting market expansion across residential and commercial applications.

Europe Textile Flooring Market Trends

Europe represents a significant market region with growing emphasis on sustainable flooring solutions and stringent environmental regulatory compliance driving product innovation and manufacturing practices. Germany is anticipated to dominate the European flooring market and emerge as the fastest-growing country, supported by robust construction industry fundamentals, strong presence of established flooring manufacturers, and intense consumer demand for high-quality, sustainably-produced building materials.

European consumers demonstrate particularly strong preference for eco-certified products and formaldehyde-free, low-VOC flooring solutions, compelling manufacturers to invest substantially in sustainable production processes and material sourcing. Government sustainability initiatives promoting renewable and recyclable materials, combined with development of toxin-free adhesives and water-based finishing processes, continue driving market innovation and adoption of eco-friendly textile flooring alternatives.

Asia Pacific Textile Flooring Market Trends

Asia Pacific has emerged as the fastest-growing regional market for textile flooring, expanding at approximately 8.2% CAGR through 2033 and representing the most dynamic growth opportunity for global manufacturers. China maintains market leadership with approximately 36% of regional share in 2026, driven by massive residential and commercial construction activities, strong government policies supporting flooring manufacturing, and availability of skilled labor and raw materials at competitive costs.

China's textile flooring industry benefits from complete product value chain integration from fiber production through finished goods distribution, enabling manufacturers to achieve economies of scale and cost competitiveness. The country accounts for over 50% of global textile flooring manufacturing and functions as a critical sourcing hub for international brands seeking cost-effective production capabilities.

Competitive Landscape

The global textile flooring market exhibits moderately consolidated competitive structure with Mohawk Industries leading companies collectively control approximately 18% of global market value. The remainder of the market remains fragmented across numerous regional manufacturers, specialty producers, and emerging market competitors. Market concentration reflects significant barriers to entry including substantial capital requirements for manufacturing facilities, distribution infrastructure development, technical expertise requirements, and brand establishment.

Market leaders pursue expansion through strategic acquisitions, manufacturing facility expansion and modernization, geographic market penetration, product portfolio diversification, and research and development investments targeting sustainable and smart flooring innovations. Emerging business model trends include subscription-based flooring leasing arrangements enabling customer access without ownership, direct-to-consumer digital platforms bypassing traditional distribution channels, customization services leveraging digital design tools, and circular economy initiatives emphasizing product recyclability and material reuse.

Key Market Developments:

- In November 2025, Beaulieu International Group announced acquisition of Congoleum Flooring, a historic American vinyl flooring manufacturer founded in 1886, strengthening its North American market presence and residential resilient flooring capabilities.

- In October 2024, Tarkett Group introduced EverGen, a premium wood plastic composite (WPC) flooring collection combining unparalleled realism with exceptional durability through 8 mm thickness and 1.5 mm irradiated cross-linked polyethylene (IXPE) padding.

- In April 2024, Interface Inc. launched two innovative flooring collections featuring industry-leading low carbon footprint carpet tile technology, combining style and performance for commercial interior applications while advancing sustainability commitments through absolute emission reduction versus offset strategies.

Companies Covered in Textile Flooring Market

- Mohawk Industries, Inc.

- Interface Inc.

- Beaulieu International Group N.V

- Tarkett SA

- Balta Group

- Shaw Industries Group Inc.

- Forbo Holding AG

- Mannington Mills, Inc.

- J+J Flooring Group

- Vorwerk and Co. KG

- Bentley Mills Inc.

- Dixie Group

- Oriental Weavers Group

- Suminoe Textile Co., Ltd.

- Victoria PLC

Frequently Asked Questions

The global textile flooring market was valued at US$ 11.1 Bn in 2025 and is projected to grow at a CAGR of 5.8% through 2032, reaching US$ 16.5 Bn by the forecast end year.

Rising consumer demand for sustainable and eco-friendly flooring solutions is the primary growth driver, with consumers prioritizing environmentally conscious products that minimize carbon footprints.

Synthetic textiles including nylon, polyester, and polypropylene dominate with approximately 37.2% global market share in 2026.

North America holds the largest regional market position with approximately 36.9% global market share, supported by established manufacturing infrastructure, and consumer investment in interior design and home renovation projects across both residential and commercial sectors.

The integration of smart flooring technologies with IoT-enabled sensor systems represents the highest-growth opportunity, driven by occupancy optimization, safety monitoring, and facility management requirements across commercial, healthcare, and hospitality applications.

Mohawk Industries, Shaw Industries Group, Tarkett SA, Interface Inc., and Beaulieu International Group represent the leading market competitors, collectively commanding approximately 18% global market share.