- Hardware & Software IT Services

- Gesture Recognition and Touchless Sensing Market

Gesture Recognition and Touchless Sensing Market Size, Share, and Growth Forecast 2026 - 2033

Gesture Recognition and Touchless Sensing Market by Product Type (Gesture-enabled consumer electronics, Touchless biometric equipment, Touchless sanitary equipment), Technology (Touch-based Gesture Recognition, Touchless Gesture Recognition), End-user (Consumer Electronics, Automotive, Healthcare, Retail & Hospitality, Others), and Regional Analysis, 2026 - 2033

Gesture Recognition and Touchless Sensing Market Size and Trend Analysis

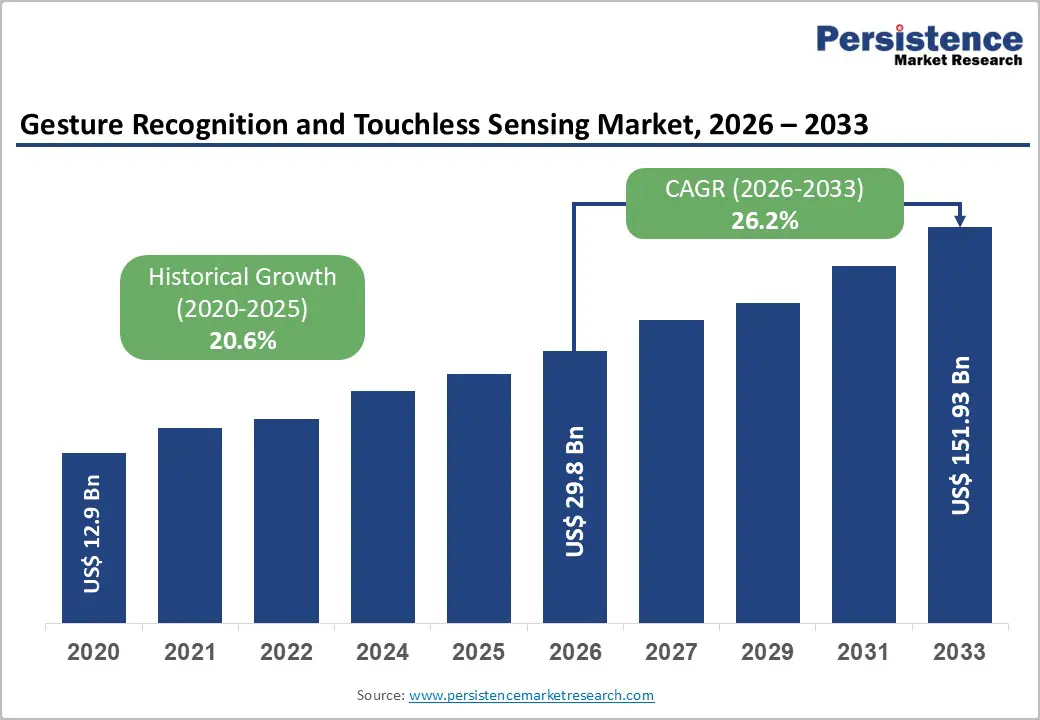

The global gesture recognition and touchless sensing market size is expected to be valued at US$ 29.80 billion in 2026 and is projected to reach US$ 151.93 billion by 2033, growing at a CAGR of 26.2% between 2026 and 2033.

This growth is driven by the accelerating adoption of human-machine interaction (HMI) technologies across consumer, industrial, and healthcare applications. In addition, post-pandemic hygiene imperatives and regulatory mandates favor touchless solutions in healthcare and food service sectors, creating sustained market demand beyond cyclical trends.

Key Industry Highlights:

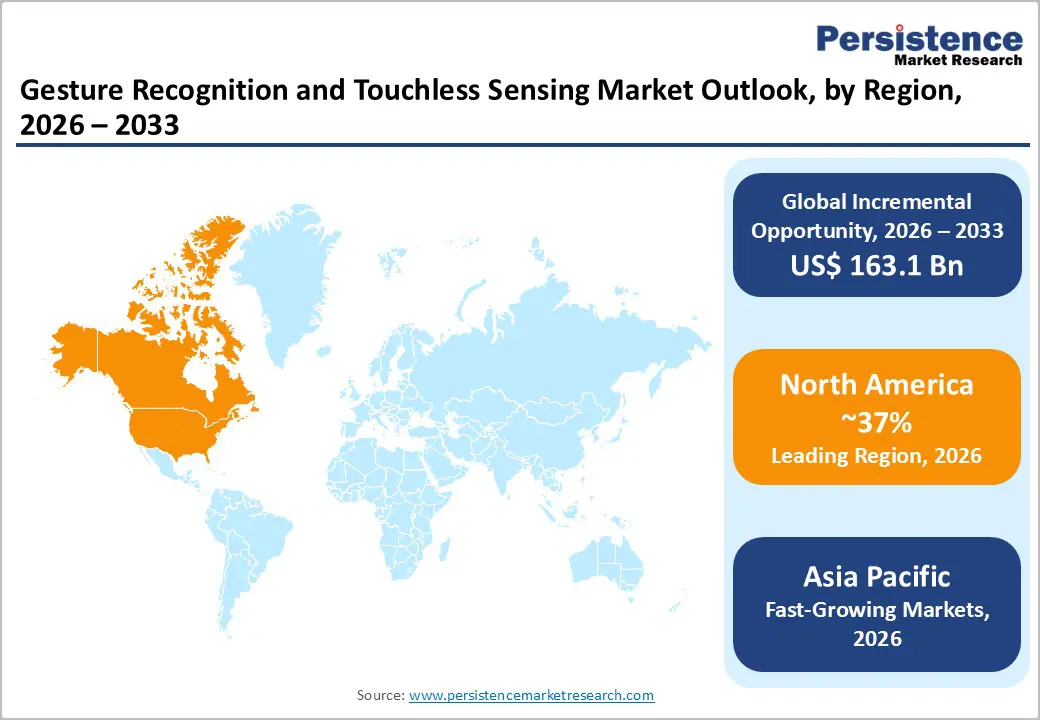

- Leading Region: North America is likely to lead the global market with a 37.0% share in 2026, driven by AI and semiconductor innovation, early enterprise technology adoption culture, and substantial federal investment in touchless biometric infrastructure across security, healthcare, and transportation verticals.

- Fast-Growing Market: Asia Pacific is the fast-growing regional market, expanding at a positive CAGR with acceleration driven by China's AI hardware investment ambitions.

- Leading Technology Segment: The touch-based gesture recognition technology segment dominates with a 59.0% share in 2026, reflecting decades of manufacturing maturity and supply chain integration across the consumer electronics and automotive sectors.

- Fast-Growing Technology Segment: Touchless gesture recognition represents the fast- growing technology segment with growth catalyzed by post-pandemic contactless user experience mandates, rapidly declining time-of-flight and radar sensor costs, and the maturation of AI computer vision platforms that are closing the accuracy gap with established touch-based systems.

- Key Opportunity: The healthcare vertical represents the most actionable opportunity for vendors entering the Gesture Recognition and Touchless Sensing Market between 2026 and 2033, as infection-control mandates shift touchless clinical interface procurement from discretionary to capital-expenditure status, and FDA and EU MDR certification pathways create durable competitive barriers to non-specialist technology entrants.

Market Dynamics

Drivers - Surging Demand for AI-Powered Human-Machine Interaction Across Consumer Electronics

The accelerating integration of AI and machine learning into motion detection algorithms embedded within consumer electronics applications. Manufacturers across the smartphone, smart television, and gaming segments now treat gesture recognition technology as a baseline feature rather than a premium differentiator, compressing time-to-integration and expanding the installed base at speed.

Global shipments of AI-enabled consumer devices crossed 1.5 billion units annually by the mid-2020s, each representing a potential endpoint for gesture and touchless sensing capabilities. This volume effect generates a self-reinforcing cycle: larger installed bases attract developer investment in gesture-based software ecosystems, which in turn increase the perceived utility of gesture-enabled hardware and drive further adoption.

Accelerating Touchless Technology Deployment in Automotive Infotainment Systems

Automotive infotainment systems represent one of the most structurally committed end-use vectors for the gesture recognition and touchless sensing market, as original equipment manufacturers (OEMs) embed touchless sensing systems as standard across mid-range and premium vehicle platforms. Regulatory pressure in key markets, including evolving distracted-driving standards across North America and the European Union, is actively incentivizing OEMs to replace physical controls with gesture and voice-activated interfaces, treating driver safety compliance as a purchasing mandate rather than a feature aspiration. Based on authenticated market intelligence, the number of vehicles shipped globally with integrated gesture control systems grew at a compound rate exceeding 22% between 2020 and 2025. Industry participants that secure early design-win positions with Tier-1 automotive suppliers will enjoy multi-year contractual lock-in, making this driver both immediate and strategically durable.

Restraints - High Development and Integration Costs Limiting Mid-Market Penetration

The elevated cost of developing low-latency gesture recognition technology into production-ready hardware and software stacks. Capacitive sensing arrays, time-of-flight (ToF) cameras, and the specialized motion detection algorithms required to achieve commercial-grade accuracy demand substantial upfront engineering investment, often placing robust gesture interfaces out of reach for mid-tier device manufacturers in cost-sensitive markets. This cost barrier preserves a bifurcated competitive structure in which high-end consumer electronics and premium automotive platforms advance rapidly, while budget and mass-market segments lag, thereby slowing overall addressable market expansion.

Privacy Concerns and Regulatory Ambiguity Around Biometric Data Collection

The collection and processing of gesture-related biometric data, particularly through touchless biometric equipment and camera-based computer vision systems, exposes market participants to an expanding and geographically inconsistent regulatory environment. Jurisdictions including the European Union (under the General Data Protection Regulation, GDPR, and the emerging EU AI Act), California (under the California Consumer Privacy Act, CCPA), and multiple Asia-Pacific markets are tightening requirements regarding biometric data storage, consent mechanisms, and cross-border data transfer.

This regulatory fragmentation forces global vendors to maintain multiple compliance architectures, increasing operational cost and extending product certification timelines. Beyond regulatory compliance costs, persistent consumer concern about surveillance and identity data misuse continues to slow enterprise adoption of touchless biometric solutions in public-facing retail and hospitality environments.

Opportunities - Healthcare Touchless Interface Deployment at Scale

The healthcare sector presents a near-term opportunity within the gesture recognition and touchless sensing market, and vendors with existing relationships in medical device manufacturing should treat this vertical as a priority growth channel by 2033. Infection control requirements in clinical environments, reinforced by post-pandemic hospital protocols, are converting previously discretionary touchless sensing investments into capital expenditure mandates across surgical suites, diagnostic imaging rooms, and patient-facing kiosks.

Based on authenticated market intelligence, healthcare IT spending as a share of total hospital operating budgets increased by more than 20% between 2020 and 2025 in developed markets, with procurement of touchless interfaces among the fastest-growing line items. Vendors that invest in medical-grade certification pathways, including FDA 510(k) clearance in the United States and CE marking under the EU Medical Device Regulation (MDR), will secure defensible moats against general-purpose consumer technology competitors entering the vertical. The combination of regulatory protection, sticky customer relationships, and recurring software revenue streams makes healthcare the highest-value addressable opportunity within this period of the gesture recognition and touchless sensing industry report.

Smart Retail and Hospitality Integration Driven by Contactless Customer Experience Mandates

The Retail & Hospitality segment offers a scalable and rapidly monetizable opportunity for gesture recognition and touchless sensing market participants willing to build vertically integrated solution stacks that combine touchless sensing hardware with customer analytics software. Global retailers are under measurable pressure to reduce friction in the purchase journey. Contactless checkout and self-service kiosk deployments increased by approximately 35% globally between 2021 and 2024, and gesture-based interaction represents the next evolutionary step beyond near-field communication (NFC) and QR-code-based touchless systems.

The hospitality sector's parallel investment in smart room controls, touchless check-in systems, and AI-powered concierge interfaces creates a complementary demand pool that shares underlying technology components with retail deployments. Vendors that develop modular, software-defined gesture-sensing platforms capable of serving both retail point-of-sale and hotel room-control use cases from a common hardware base will achieve superior unit economics and faster sales cycles. This opportunity is particularly time-sensitive because early-deploying retail chains are establishing platform allegiances now, and the switching costs of proprietary gesture ecosystems are meaningfully high once infrastructure investment is committed.

Category-wise Analysis

Product Type Insights

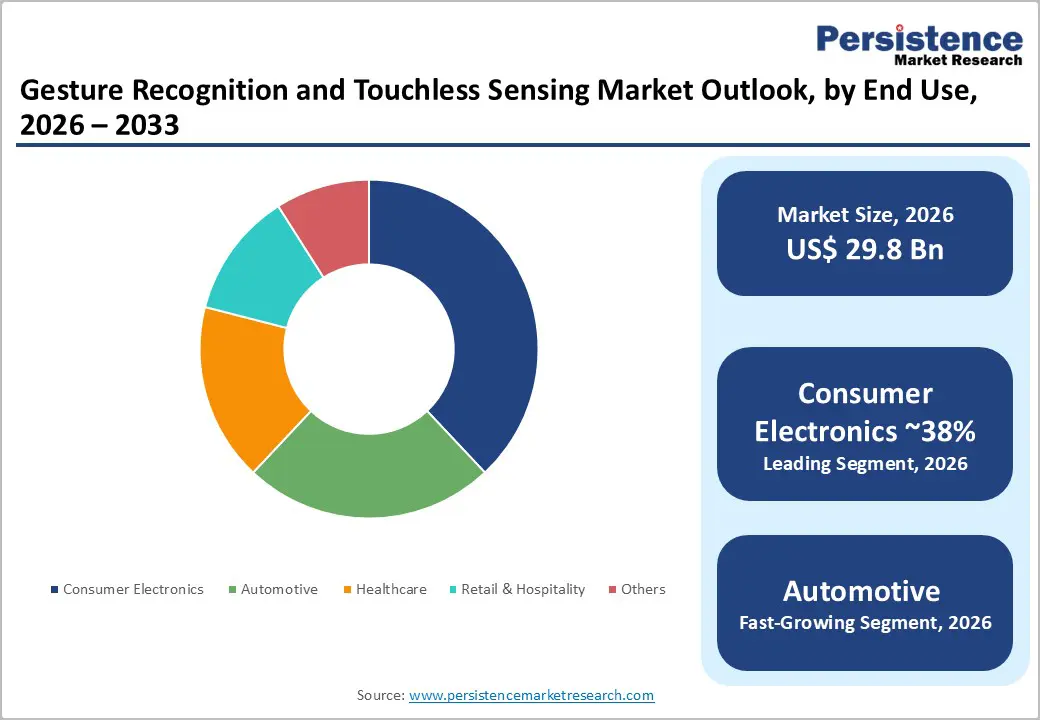

The gesture-enabled consumer electronics segment is likely to account for 38% of the gesture recognition and touchless sensing market in 2026 as the leading product category. This dominates because consumer electronics manufacturers, including smartphone OEMs, smart TV providers, gaming console makers, and wearable device companies, adopt gesture recognition at scale, driving significantly higher volumes than biometric or sanitation-related applications.

Industry data indicates that global shipments of devices with gesture or touchless features exceeded 800 million units in 2025, highlighting the segment’s broad reach. It is also the fastest-growing product segment, supported by advances in AI-based motion detection, smaller infrared sensors, and declining component costs, which are enabling adoption in mid-range devices. This leadership is expected to remain stable through 2033 as smart devices continue to expand. Companies should focus more on AI-driven software differentiation rather than competing only on hardware pricing.

Technology Insights

Touch-based gesture recognition holds 59% of the global gesture recognition and touchless sensing market in 2026, valued at US$ 17.58 billion, making it the dominant technology segment. Its leadership comes from well-established capacitive and resistive sensing technologies, supported by mature manufacturing processes, strong supply chains, and compatibility with existing consumer electronics and automotive systems.

Over 70% of gesture-enabled devices currently use touch-based interfaces, reinforcing their strong market presence. However, touchless gesture recognition is the fastest-growing segment, driven by rising demand for contactless interaction and improvements in AI-powered sensing technologies such as time-of-flight, infrared, ultrasonic, and radar systems. As hardware costs decline and accuracy improves, the gap between touch and touchless solutions is narrowing. Companies focused on touch-based systems should begin investing in touchless technologies or consider strategic partnerships to stay competitive.

End Use Analysis

The consumer electronics segment represents 38.0% of the global Gesture Recognition and Touchless Sensing Market in 2026, equal to US$ 11.32 billion, making it the largest end-use category. This dominance is driven by high-volume products such as smartphones, smart TVs, gaming devices, and wearables, all of which widely incorporate gesture and touchless features. Industry estimates suggest that over 2.3 billion smart consumer devices with gesture capabilities will be in use globally by 2025, creating a strong and recurring revenue base.

The automotive sector is the fastest-growing end-use segment, fueled by the increasing integration of gesture controls into infotainment systems, touchless cabin features, and driver-monitoring solutions powered by AI and computer vision. Although the automotive and healthcare sectors are expanding, consumer electronics will retain its lead due to its massive scale. Companies should view emerging sectors as growth opportunities rather than direct competition.

Regional Insights

North America Gesture Recognition and Touchless Sensing Market Trends and Insights

North America holds 37.0% of the global market in 2026, driven by early adoption, strong AI and computer vision R&D, and supportive regulations. US-based firms lead innovation. Growth will be fueled by automotive OEM integration and smart building deployments, where touchless interfaces are becoming core infrastructure.

- United States Gesture Recognition and Touchless Sensing Market Size

The US accounts for 82% of North America’s market, with the market reaching about US$9.04B in 2026. Growth is driven by strong performance in the consumer electronics and semiconductor sectors, adoption of automotive infotainment, and federal investment in biometric security. Expansion of AI-powered smart home ecosystems will sustain dominance through 2033.

Europe Gesture Recognition and Touchless Sensing Market Trends and Insights

Europe holds 22.0% of the global market in 2026. Demand is shaped by automotive strength and by strict regulations such as GDPR and the EU AI Act. Healthcare adoption is rising post-pandemic. Growth will remain steady, supported by smart building initiatives and the shift to software-defined vehicles.

- Germany Gesture Recognition and Touchless Sensing Market Size

Germany accounts for 28% of Europe’s market, driven by automotive leadership and industrial automation. Demand centers on gesture-enabled infotainment and industrial HMI systems. Growth will be supported by Industry 4.0 investments, positioning touchless sensing as a key interface in advanced manufacturing environments.

- United Kingdom Gesture Recognition and Touchless Sensing Market Size

The UK accounts for 18% of Europe’s market, driven by retail and NHS digitalization. Gesture-based payments and kiosks are expanding. While post-Brexit regulations add complexity, a more flexible framework may accelerate adoption and attract global vendors to the UK’s active innovation ecosystem.

- France Gesture Recognition and Touchless Sensing Market Size

France represents 15% of Europe’s market, driven by the luxury retail, hospitality, and automotive sectors. Adoption focuses on premium touchless experiences. Aerospace and defense add demand. Growth will exceed the regional average as public sector digitalization expands across healthcare and government services.

Asia Pacific Gesture Recognition and Touchless Sensing Market Trends and Insights

Asia Pacific accounts for 30.0% of the global market and is the fastest-growing region (CAGR of 29.8%). Growth is driven by China’s AI push, India’s electronics demand, and Japan’s innovation. Smart city projects across the region are accelerating large-scale adoption, challenging North America’s dominance.

- China Gesture Recognition and Touchless Sensing Market Size

China leads Asia Pacific with 48% share, supported by strong electronics manufacturing, AI investment, and smart city expansion. Domestic firms are advancing competitive solutions. Growth will strengthen as local semiconductor capacity expands, reducing reliance on imports and boosting self-sufficiency.

- India Gesture Recognition and Touchless Sensing Market Size

India holds 17% of the Asia Pacific’s market, driven by rapid smartphone adoption and Digital India initiatives. Touchless biometrics are expanding across banking and public services. Growing automotive integration and affordable hardware will accelerate adoption, making India one of the fastest-growing markets globally.

- Japan Gesture Recognition and Touchless Sensing Market Size

Japan accounts for 16% of Asia Pacific’s market, supported by robotics, automotive innovation, and precision sensing technologies. Demand is rising in healthcare due to ageing demographics. Touchless interfaces are increasingly used for accessibility and infection control, strengthening long-term growth prospects.

Competitive Landscape

The Gesture Recognition and Touchless Sensing Market exhibits a moderately fragmented competitive structure characterized by a small cohort of large-scale technology platform leaders, commanding dominant share in software ecosystems, AI processing, and proprietary sensing hardware, and a larger population of specialized component vendors and application-layer integrators competing on vertical expertise. Differentiation pivots primarily on three axes: the accuracy and latency performance of embedded AI motion detection algorithms; the breadth of sensing modality support spanning capacitive sensing, infrared sensors, ultrasonic sensing, radar, and computer vision; and the depth of end-use vertical integration, particularly in automotive, healthcare, and smart retail.

Strategic M&A activity is intensifying as platform leaders seek to acquire specialized capabilities in touchless biometric authentication and radar-based gesture sensing that would otherwise require multi-year in-house development cycles. Ecosystem lock-in strategies, built around proprietary software development kits (SDKs), developer communities, and certified integration partnerships, are emerging as the dominant competitive moat, making early ecosystem positioning decisions more strategically consequential than component-level price competition.

Key Market Developments

- January, 2025: Qualcomm Incorporated announced an expanded gesture recognition processing capability within its Snapdragon 8 Elite mobile platform, integrating on-device AI-powered motion detection algorithms that enable sub-10ms touchless gesture response latency for next-generation smartphone and extended reality (XR) applications, reinforcing its leadership in the mobile gesture sensing silicon segment.

- March, 2025: Infineon Technologies AG launched its next-generation XENSIV radar sensing portfolio targeting automotive cabin gesture control and touchless sanitary equipment applications, offering a single-chip radar solution that reduces system integration complexity for Tier-1 automotive suppliers by an estimated 40% compared with prior multi-chip architectures.

- October, 2024: Elliptic Labs ASA secured a major design-win agreement with a leading Asia Pacific smartphone OEM to deploy its AI-powered ultrasonic sensing software across a flagship device series, marking a significant validation of software-defined touchless sensing as a commercially competitive alternative to hardware-based gesture recognition modules.

Companies Covered in Gesture Recognition and Touchless Sensing Market

- Apple Inc.

- Microsoft Corporation

- Google LLC

- Intel Corporation

- Qualcomm Incorporated

- Sony Corporation

- Samsung Electronics Co., Ltd.

- Infineon Technologies AG

- Microchip Technology Inc.

- STMicroelectronics N.V.

- Texas Instruments Incorporated

- Synaptics Incorporated

- Omron Corporation

- GestureTek Inc.

- Elliptic Labs ASA

- Cognitec Systems GmbH

- Eyesight Technologies Ltd.

- Ultraleap Limited

- Jabil Inc.

- IrisGuard Inc.

Frequently Asked Questions

The market is valued at US$ 29.80 billion in 2026 and projected to reach US$ 151.93 billion by 2033, growing at a CAGR of 26.2%, driven by AI integration.

Growth is driven by widespread AI-powered gesture integration in consumer devices and regulatory mandates for touchless automotive interfaces, accelerating adoption across industries and reinforcing demand through increased user familiarity.

Consumer Electronics leads with 38.0% share in 2026, driven by high-volume devices like smartphones, TVs, gaming systems, and wearables, where gesture recognition is now a standard interface feature.

North America leads with 37.0% share due to strong AI, semiconductor, and tech company presence, along with high investment in touchless systems across healthcare, security, and financial services sectors.

Key opportunities include healthcare touchless systems requiring regulatory certification and rapid adoption in retail and hospitality through contactless kiosks, creating early-mover advantages and long-term high-margin contracts.

The leading companies in the Gesture Recognition and Touchless Sensing Market include Apple Inc., Microsoft Corporation, Google LLC, Intel Corporation, Qualcomm Incorporated, Samsung Electronics Co., Ltd., Infineon Technologies AG, STMicroelectronics N.V., Synaptics Incorporated, and Elliptic Labs ASA, among other specialised players.