- Semiconductor Materials & Components

- Secure Digital Memory Card Market

Secure Digital Memory Card Market Size, Share, and Growth Forecast 2025 - 2032

Secure Digital Memory Card Market by Card Type (SD, SDHC, SDXC, SDUC), Capacity Range (≤ 32 GB, 32-128 GB, 128-512 GB, 512 GB-1 TB, > 1 TB), End-user (Smartphones & Tablets, Digital Cameras, Action Cameras, Drones, Dashcams, Gaming Devices, Industrial & IoT Devices, PCs & Laptops, Professional Broadcasting & Cinematography), by Regional Analysis, 2025 - 2032

Secure Digital Memory Card Market Size and Trend Analysis

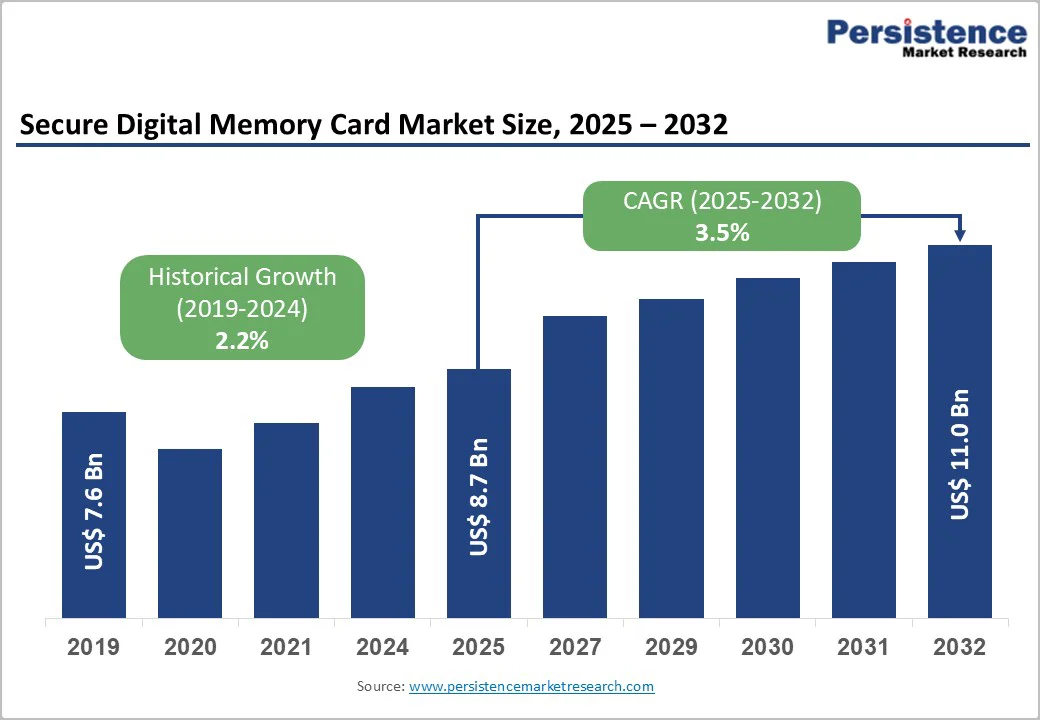

The global secure digital memory card market size is likely to be valued at US$ 8.7 billion in 2025 and is projected to reach US$ 11.1 billion by 2032, growing at a CAGR of 3.5% between 2025 and 2032.

This growth is driven by an increasing demand for high-capacity storage in consumer electronics and the development of new applications. The rise of 4K and 8K video recording in drones and cameras, along with the expansion of the Internet of Things (IoT), requires more robust memory solutions.

Key Industry Highlights:

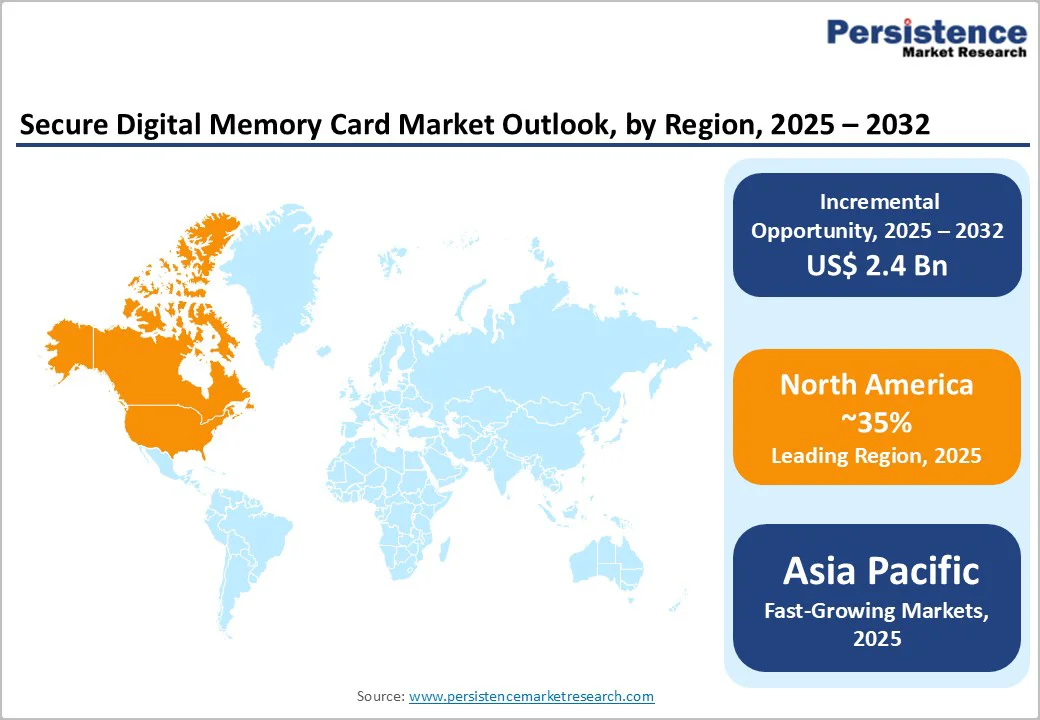

- Leading Region: North America leads as the dominant region, driven by U.S. innovation in gaming and IoT, capturing over 35% share through advanced adoption.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region at 5.3% CAGR, powered by manufacturing in China and India's digital surge.

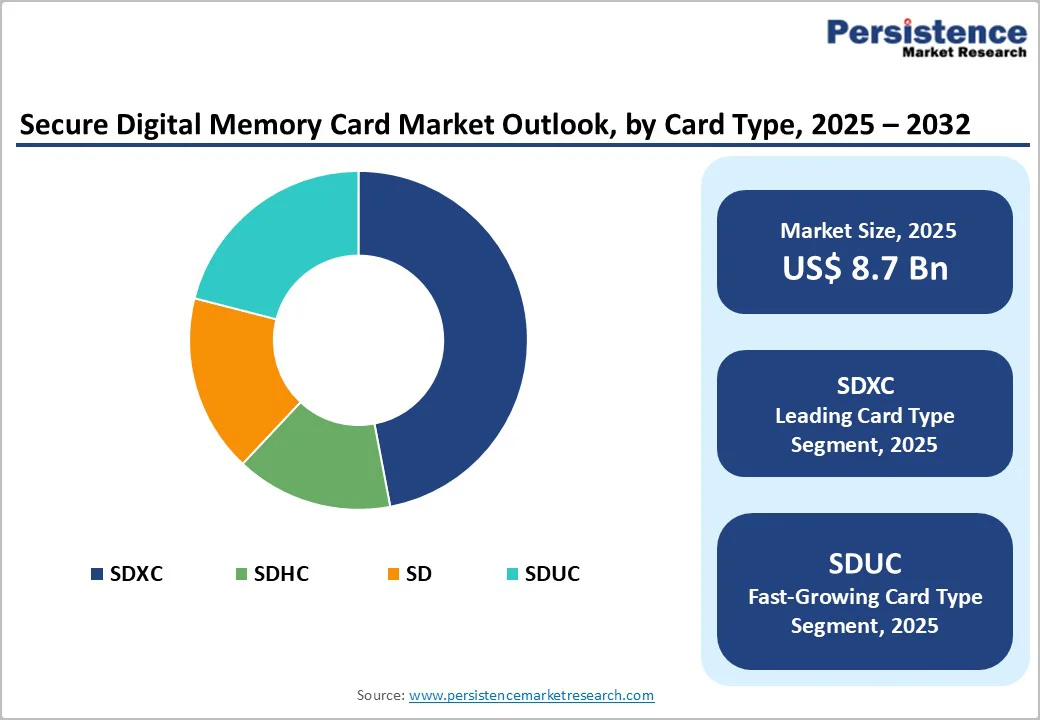

- Leading Segment: SDXC dominates Card Type with 47% share, ideal for 4K/8K in cameras and smartphones.

- Fastest-Growing Segment: 128-512 GB leads Capacity Range growth, holding 38% amid NAND capacity shifts for creators.

- Key Opportunity: SD Express in gaming/drones offers a key opportunity, promising high-speed expansion through 2032.

| Key Insights | Details |

|---|---|

| Secure Digital Memory Card Market Size (2025E) | US$ 8.7 Billion |

| Market Value Forecast (2032F) | US$ 11.0 Billion |

| Projected Growth CAGR (2025 - 2032) | 3.5% |

| Historical Market Growth (2019 - 2024) | 2.2% |

Market Dynamics

Drivers - Growing Demand for High-Capacity SD Cards Driven by 4K/8K Video and Surveillance Applications

The Secure Digital Memory Card Market is expanding strongly as users now need far higher storage capacity for modern applications such as 4K/8K video recording, drone imaging, automotive dashboards, home security systems, and edge-AI devices. These use cases generate extremely large video and data files, pushing consumers and professionals to prefer microSDXC cards with terabyte-level capacity and long-duration recording support.

The trend is also driven by the shift toward continuous surveillance and high-bitrate videography, where reliable storage expansion is essential. In 2024, SanDisk introduced its 1.5TB microSDXC card, designed specifically for videography and surveillance workloads. This launch demonstrated how manufacturers are increasing capacity to match real-world demand, reinforcing high-density storage as a core market growth driver.

Advanced High-Speed Standards such as SD Express Accelerate SD Card Upgrade and Replacement Demand

Performance upgrades are becoming a major driver of the Secure Digital Memory Card Market as devices now require much faster read/write speeds to support high-fps video, gaming consoles, professional photography, and portable computing. New technologies such as SD Express, which uses PCIe/NVMe interfaces, and improved UHS standards are enabling SD cards to deliver significantly higher throughput and lower latency.

This makes high-speed cards essential for users who need smooth data capture, quick file transfers, and reliable performance under heavy workloads. In 2024, Samsung began mass production of advanced terabyte-class microSD cards built with high-performance V-NAND to meet rising demand for speed and capacity.

Such developments clearly show how continuous improvements in performance standards are driving consumers and businesses to upgrade to next-generation SD cards.

Restraints - Heavy Competition and Falling Prices are Compressing SD Card Margins and Slowing Market Profitability

The market faces restraints mainly due to heavy competition and ongoing price erosion among SD card manufacturers. With many companies offering similar products, aggressive pricing strategies have led to shrinking profit margins across the industry. NAND flash memory prices continue to decline, which has caused average selling prices (ASPs) to drop consistently, limiting overall revenue potential for suppliers.

Increasing reliance on cloud storage reduces consumers’ dependence on physical cards, especially as smartphones now prioritize large internal storage capacities. Industry analyses highlight that device manufacturers shifting toward soldered memory solutions further constrain demand for expandable card slots.

Despite advancements in card capacity and speed, these structural market changes create strong downward pressure on volumes and profitability, challenging SD card makers to differentiate through premium performance and durability features.

Growing Reliance on Internal Storage and Cloud Services Reduces the Need for External SD Card Support in Modern Devices

Another major market restraint is the growing shift toward integrated storage and cloud-based services in consumer electronics. Smartphones increasingly eliminate expandable SD card slots, relying instead on built-in storage, which reduces the need for external memory cards. Although USB-C adapters provide some flexibility, native support is declining, limiting mainstream adoption.

SD Express cards, while extremely fast, have thermal management issues in compact devices, as their high-speed operations can generate excess heat during continuous data transfers. This thermal challenge makes implementation difficult in thin smartphones and tablets.

The broader preference for cloud syncing of images, apps, and videos also weakens the role of removable storage. These factors collectively pose barriers to SD card penetration, particularly in high-volume mobile markets where internal storage solutions dominate.

Opportunity - Growing Adoption of SDUC Cards to Support the Rising Demand for 8K/12K Professional Content Storage

The introduction of SDUC (Secure Digital Ultra Capacity) cards creates a major new opportunity for SD memory manufacturers to serve the rapidly growing professional content market. With cameras, drones, and editing devices now capturing 8K and even 12K video, creators need extremely large and reliable removable storage. SDUC cards support capacities far beyond the 2TB SDXC limit, enabling smooth handling of massive video files without frequent card swaps.

This opens strong demand from filmmakers, broadcasters, drone operators, and high-end laptop users who rely on portable, high-capacity media. In 2024, Western Digital’s 4TB SanDisk SDUC UHS-I card was showcased at NAB 2024, specifically designed for professional video creators requiring huge storage volumes. This confirms that SDUC is becoming commercially viable, giving manufacturers a chance to lead in premium, ultra-high-capacity SD solutions.

Increasing Need for Ultra-Capacity SD Cards for Surveillance, AI Edge Systems, and Industrial Data Logging

Fast-emerging opportunities have surfaced for ultra-capacity SD cards, especially 4TB to 8TB SDUC models, in industries that generate continuous high-volume data. Video surveillance, industrial sensors, telematics, AI edge systems, and automated machinery increasingly require long-duration storage that is compact, power-efficient, and removable. Ultra-capacity SD cards allow these systems to store data locally for weeks or months without relying on cloud connectivity, reducing operational costs and improving reliability.

In 2024, Western Digital’s announcement of the world’s first 8TB SanDisk SDUC UHS-I card demonstrates the accelerating shift toward extremely large SD storage for professional and industrial use. This trend enables SD card manufacturers to target enterprise customers with high-margin, durable, high-density products that support 24/7 recording, long-term retention, and rugged field operations.

Category-wise Analysis

Card Type Insights

SDXC leads the Card Type segment with around 47% market share because its wide capacity range of 32GB to 2TB is ideal for 4K video recording, gaming, and professional photography. It supports high-speed UHS-II standards, preventing frame drops in high-performance cameras and smartphones.

Its strong adoption in DSLRs, drones, and action cameras reinforces its market leadership. The shift of more than 50% of consumers toward 64GB and above storage also aligns with SDXC’s advantages, making it the preferred choice across both consumer and professional devices.

Capacity Range Insights

The 128-512GB segment holds approximately 38% market share as it offers the best balance between price and performance for mid-to-high-end devices. The 256GB and 512GB cards account for a large share of camera and smartphone purchases because they support 8K video recording and large files without frequent card changes.

Advances in NAND technology have made these capacities more affordable and faster, making them especially popular among gamers, photographers, and content creators who require reliable, high-volume storage for everyday use.

End-user Insights

Smartphones and Tablets remain the dominant End-user category, contributing over 60% of SD card demand globally. This growth is driven by strong smartphone adoption in emerging markets and the continued use of USB-C adapters for expandable storage.

Around 65% of mobile-related storage use comes from photography, apps, social media, and video consumption. With increasing everyday content creation and the need for higher storage capacities, this segment continues to lead the market and remains a key driver of microSD card sales worldwide.

Regional Insights

North America Secure Digital Memory Card Market Trends

The Secure Digital (SD) Memory Card Market in North America is expanding steadily due to strong demand from consumer electronics, professional content creation, gaming, and cloud-connected surveillance systems.

The region benefits from high spending on premium electronics such as action cameras, drones, DSLR and mirrorless cameras, and gaming handhelds, all of which rely on high-speed SDXC and microSDXC cards. Retailers and e-commerce platforms have widened product accessibility, while enterprises and city authorities continue upgrading to high-endurance SD cards for large-scale security deployments.

The presence of major brands, including SanDisk, Lexar, PNY, and Samsung’s U.S. distribution network, further strengthens supply capabilities. In 2024 when SanDisk announced expanded availability of its 1.5TB microSDXC cards for North American videographers and surveillance users, it reflected rising demand for ultra-high-capacity storage. As the region continues adopting 4K/8K imaging and AI-enabled devices, high-performance SD cards remain essential.

Europe Secure Digital Memory Card Market Trends

Europe represents a mature yet innovation-driven SD Memory Card Market, supported by strong professional imaging, media production, and cross-border e-commerce channels.

The region has a large base of photographers, broadcasters, creative agencies, and rental studios that rely on high-speed SDXC and SD Express cards to handle 4K, 6K, and 8K workflows. European buyers prioritize reliability, regulatory compliance, and environmental standards such as RoHS, which encourages manufacturers to supply durable and sustainable memory solutions.

Countries such as Germany, the UK, France, and the Netherlands serve as key distribution hubs, supported by specialized retail chains and professional equipment suppliers. In 2024, Lexar highlighted Europe as a major rollout region during IFA Berlin, showcasing its new professional SD card range designed for high-speed capture and robust field performance.

This continued product activity demonstrates Europe’s ongoing shift toward faster, high-capacity cards aligned with professional-grade requirements.

Asia Pacific Secure Digital Memory Card Market Trends

Asia Pacific is the fastest-growing region in the Secure Digital (SD) Memory Card Market, driven by massive smartphone usage, large-scale electronics manufacturing, rising demand for surveillance systems, and the rapid growth of digital content creators.

Countries such as China, India, Japan, South Korea, and Vietnam account for a large share of global microSD consumption due to widespread use of Android smartphones, action cameras, dashcams, and home monitoring devices.

The region also benefits from strong manufacturing ecosystems, enabling faster production cycles and competitive pricing across capacity tiers from 128GB to 1.5TB. In 2025, Samsung expanded SD and memory-related production capabilities in Vietnam, reinforcing the region’s strategic role in the global storage supply chain.

Growing e-commerce penetration, increasing adoption of 4K mobile video content, and broader digitalization across enterprises continue to boost demand for high-speed, high-endurance SD cards throughout Asia Pacific.

Competitive Landscape

The global secure digital memory card market exhibits a consolidated structure, led by top players controlling innovation via NAND advancements and SD Express. Strategies focus on R&D for high-capacity cards, partnerships with OEMs like Nintendo, and expansion into industrial segments. Key differentiators include durability and speed, with emerging models emphasizing AI-integrated encryption.

Key Market Developments:

- In January 2024, SanDisk introduced a breakthrough 1.5TB microSDXC card designed for professional videography and surveillance systems requiring extreme capacity and reliability. The product supports continuous 4K/8K recording, strengthening SanDisk’s leadership in high-density flash storage.

- In March 2024, Samsung expanded its Vietnam manufacturing plant by 35% to increase production of high-speed SD and microSD cards. This expansion supports rising global demand for premium storage used in smartphones, cameras, and IoT devices.

- In October 2025, Silicon Motion accelerated SD Express technology adoption through advanced PCIe controller integration, enabling faster portable storage with near-NVMe performance. This innovation enhances next-generation memory cards for gaming, cameras, and AI workloads.

Companies Covered in Secure Digital Memory Card Market

- SanDisk Corporation

- Transcend

- ADATA Technologies Co. Ltd.

- Panasonic Corporation

- Kingston Technology Corporation

- Micron Technology, Inc.

- Sony Corporation

- Samsung Electronics Co. Ltd.

- Toshiba Corporation

- PNY Technologies, Inc.

- Silicon Motion

- Other

Frequently Asked Questions

The market is projected to reach US$ 11.1 billion by 2032, growing at 3.5% CAGR from US$ 8.7 billion in 2025.

High-resolution 4K/8K content creation in drones and cameras drives demand, with over 50% cards now 64GB+.

SDXC leads with 57% share, due to 32GB-2TB capacities for professional video and gaming.

North America dominates, led by U.S. innovation in IoT and gaming ecosystems.

SD Express adoption in gaming and drones offers high-speed growth potential through 2032.

Leading players include SanDisk, Samsung, Kingston, and Sony, focusing on capacity innovations.