ID: PMRREP33879| 178 Pages | 26 Feb 2026 | Format: PDF, Excel, PPT* | Consumer Goods

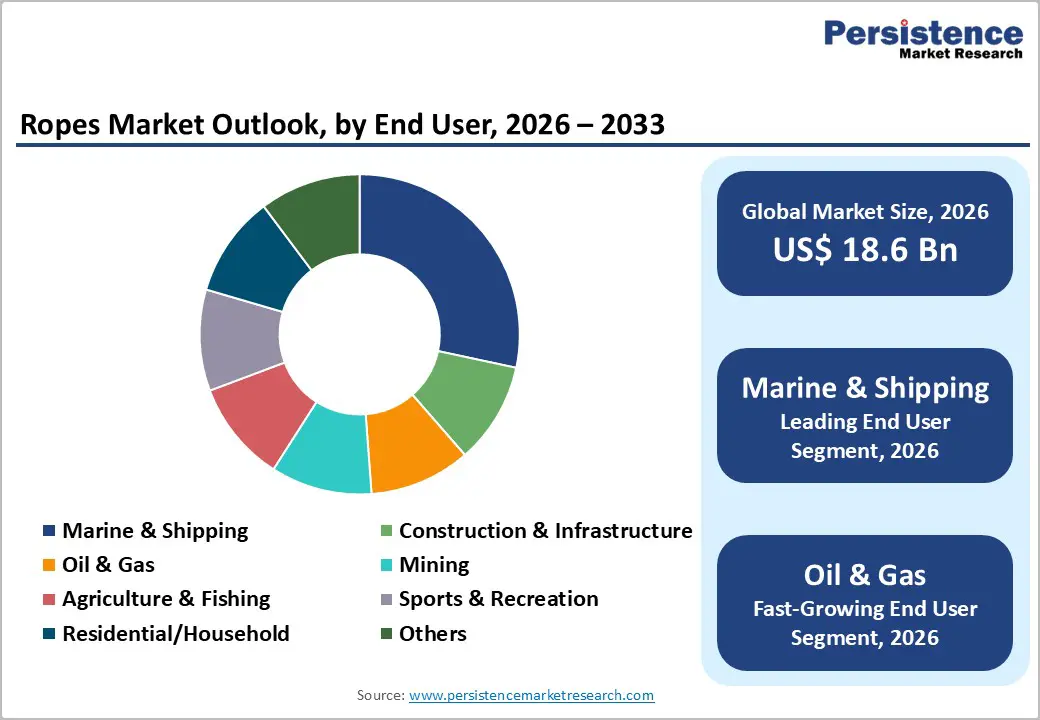

The global ropes market size is expected to be valued at US$ 18.6 billion in 2026 and projected to reach US$ 31.5 billion by 2033, growing at a CAGR of 7.8% between 2026 and 2033.

This robust growth is fundamentally underpinned by rising global demand across a wide spectrum of high-intensity industrial and marine end-use sectors, most critically, the accelerating expansion of offshore oil and gas exploration, surging global shipping and port infrastructure investment, and the rapid global build-out of offshore wind energy installations that require specialized high-performance mooring, lifting, and anchoring rope systems. The structural shift from conventional steel wire ropes to advanced high-modulus synthetic fiber ropes, including ultra-high-molecular-weight polyethylene (UHMWPE) and liquid crystal polymer (LCP) based products, is simultaneously expanding the addressable revenue base of the ropes market by enabling premium-priced, performance-differentiated product offerings that are gaining rapid acceptance in safety-critical industrial applications globally.

| Key Insights | Details |

|---|---|

| Ropes Market Size (2026E) | US$ 18.6 Billion |

| Market Value Forecast (2033F) | US$ 31.5 Billion |

| Projected Growth CAGR (2026 - 2033) | 7.8% |

| Historical Market Growth (2020 - 2025) | 6.9% |

The global offshore wind energy sector is emerging as one of the most consequential new demand drivers for the ropes market, creating structurally significant volume requirements for specialized synthetic fiber and steel wire rope products used in turbine mooring, anchor line systems, cable installation vessels, and dynamic positioning systems. The International Energy Agency (IEA) projects that global offshore wind capacity must reach approximately 2,000 GW by 2050 under net-zero emissions pathways, a trajectory requiring enormous ongoing capital investment in offshore installation and maintenance operations that depend on high-performance rope systems. The European Commission’s offshore renewable energy strategy targets 300 GW of offshore wind capacity in European waters by 2050, while the U.S. Bureau of Ocean Energy Management (BOEM) has auctioned offshore wind leases spanning hundreds of gigawatts of potential capacity along the U.S. coastline. Floating offshore wind platforms, which require dynamic synthetic fiber mooring systems using UHMWPE or polyester fiber ropes capable of withstanding millions of fatigue cycles in deepwater environments, are particularly demanding per-unit consumers of premium rope products, establishing offshore wind as a structurally durable growth vertical for rope manufacturers through the forecast period.

Expanding Global Shipping Fleet and Port Infrastructure Investment Sustaining Marine Rope Demand

Global maritime trade and the continuous expansion of the world’s commercial shipping fleet represent a foundational and structurally stable demand driver for the ropes market, particularly for the marine mooring, towing, and anchoring applications that account for the largest single end-use share within the sector. The United Nations Conference on Trade and Development (UNCTAD) reports that global seaborne trade volumes reached approximately 12 billion tons in 2023 and are projected to grow at approximately 2% annually through 2028, driving fleet expansion and replacement orders that generate recurring rope demand. Container shipping capacity expansions by major operators, including MSC (Mediterranean Shipping Company), Maersk, and CMA CGM, and the global buildout of deep-water port infrastructure across Southeast Asia, West Africa, and Latin America are contributing to sustained mooring rope consumption. The International Maritime Organization’s (IMO) progressively tightening safety regulations for mooring operations, including the implementation of the IMO Maritime Safety Committee’s guidelines on mooring equipment, are also driving specification upgrades toward higher-strength, longer-service-life rope products, supporting both volume and value growth in the marine segment.

The synthetic fiber rope segment, which accounts for the majority of total ropes market revenue, is acutely exposed to price volatility in its primary petrochemical-derived raw materials, including polypropylene (PP), polyester (PET), and high-density polyethylene (HDPE) resin feedstocks. These materials are closely linked to crude oil and natural gas price dynamics, and their costs have demonstrated significant volatility in recent years, with benchmark polypropylene spot prices fluctuating by more than 30-40% between 2021 and 2023 in response to energy price shocks and supply chain disruptions. For rope manufacturers operating in competitive, price-sensitive industrial procurement markets, these raw material cost swings create material margin compression risk, particularly when multi-year supply contracts prevent immediate pass-through of cost increases to end customers. This profitability volatility can defer capacity investment decisions and constrain R&D spending on next-generation fiber rope development among smaller market participants.

Increasing Competition from Alternative Load-Bearing Technologies in Select Applications

The ropes market faces incremental competitive pressure in select applications from alternative load-bearing and lifting technologies, including synthetic slings, textile webbing straps, rigid lifting chains, and advanced composite structural elements. In the construction and infrastructure sector, hydraulic and mechanical lifting systems increasingly substitute rope-based rigging arrangements in large-scale prefabrication and heavy lift operations, reducing per-project rope consumption intensity. The European Lifting Equipment Association (LEEA) has noted growing adoption of round slings and flat webbing slings in precision industrial lifting contexts where weight savings and ease of rigging are prioritized over the tensile strength advantages of wire rope. While these substitutes currently affect only a narrow range of applications, their progressive market penetration in mid-range construction and industrial lifting markets could limit volume growth for conventional wire and synthetic rope products in those specific segments over the forecast period.

The global oil and gas industry’s continuing shift toward deepwater and ultra-deepwater (UDW) exploration and production, driven by declining reserve replacement rates in mature onshore basins and the discovery of significant hydrocarbon accumulations in deepwater provinces including the Gulf of Mexico, Brazilian pre-salt, West African deep margins, and East Mediterranean, is creating a structurally compelling demand opportunity for high-performance synthetic fiber ropes. UDW mooring systems at depths exceeding 1,500 meters fundamentally cannot utilize conventional steel wire rope due to self-weight limitations, a constraint that makes UHMWPE and polyester fiber ropes the only technically viable mooring solution at these depths. Samson Rope Technologies and Cortland Limited have established themselves as specialized suppliers of deep-water mooring ropes to major offshore operators including Petrobras, TotalEnergies, and Shell. The IEA projects sustained deepwater capex investment through 2030 as operators prioritize high-flow-rate deepwater wells to maximize return on development spending, ensuring a durable premium demand opportunity for UDW-capable synthetic rope manufacturers offering engineered mooring system solutions.

Mining Sector Modernization and Hoist System Upgrades Driving High-Value Wire Rope Replacement Cycle

The global mining sector represents a significant and increasingly high-value growth opportunity for wire rope manufacturers, driven by the combination of accelerating mining equipment modernization programs, growing mineral demand from the energy transition, and the industry’s progressive adoption of deeper, higher-capacity shaft mining systems that require larger-diameter, higher-strength hoisting ropes with superior fatigue endurance characteristics. The World Mining Congress and International Council on Mining & Metals (ICMM) have both highlighted the escalating capital investment cycle in mining operations globally, particularly in copper, nickel, lithium, and cobalt mining that underpins battery supply chains, with deeper ore body development driving demand for advanced steel wire hoisting and guide rope systems capable of operating reliably at depths exceeding 2,000-3,000 meters. Bridon-Bekaert and WireCo WorldGroup, the world’s two largest wire rope manufacturers, are investing in high-tensile, rotation-resistant rope designs with enhanced fatigue life that address the specific requirements of ultra-deep shaft hoisting systems. As global critical mineral mining investment accelerates under energy transition policy frameworks including the U.S. Critical Minerals Strategy and the EU Critical Raw Materials Act, the mining wire rope replacement cycle represents a high-margin, sustained growth opportunity through 2033.

Wire Ropes dominated the global Ropes Market by product type, accounting for approximately 52% of total market share in 2025. This leadership is underpinned by wire ropes’ superior load-bearing capacity, abrasion resistance, dimensional stability, and proven reliability in heavy-duty lifting, hoisting, and structural tensioning applications. Their entrenched use in mining hoists, tower cranes, elevators, oil & gas drilling rigs, and infrastructure construction continues to generate large-volume, recurring replacement demand. Steel wire ropes, including galvanized and stainless-steel variants, remain the industry standard in high-load and high-temperature environments where mechanical robustness and safety compliance are paramount.

Braided Ropes led the global Ropes Market by rope design, accounting for approximately 44% of total market share in 2025. Braided rope architecture, encompassing double-braid, single-braid (hollow braid), and 8-strand braid constructions, has become the dominant design platform across a wide range of demanding end-use applications, owing to its superior torque-balanced construction, excellent handling characteristics, and consistently higher tensile strength-to-weight performance compared to traditional laid or twisted rope constructions of equivalent diameter. In marine applications, from yacht halyards and sheets to large-vessel mooring lines, braided ropes are the industry-standard specification, driven by their non-kinking behavior, round cross-section that seats cleanly in rope clutches and winch drums, and superior resistance to abrasion over the service life of the product. Leading rope manufacturers including Marlow Ropes, Samson Rope Technologies, and English Braids Limited have built their premium product lines around advanced braiding technology platforms. Laid/Twisted ropes represent the fastest-growing design segment, supported by ongoing demand from agriculture, fishing, and general-purpose industrial applications across high-growth developing markets.

Marine & Shipping dominated the global ropes market by end user, representing approximately 28% of total market share in 2025. The marine and shipping sector’s commanding leadership position reflects the fundamental and recurring nature of rope consumption across all aspects of maritime operations, from port mooring and towing operations that require heavy-duty synthetic fiber mooring lines on every commercial vessel, to offshore oil and gas platform mooring systems, fishing vessel rigging, yacht and leisure marine halyards and sheets, and the rigging equipment of specialized marine construction vessels operating in the rapidly expanding offshore wind installation sector. The global commercial shipping fleet, comprising over 100,000 vessels as reported by Lloyd’s Register, requires periodic mooring rope replacement driven by wear, fatigue, and mandatory safety inspection standards under SOLAS and port state control inspection regimes, creating a large and structurally recurring baseline demand. The offshore wind installation and maintenance market is the fastest-growing end-user segment within the marine category, while the broader Oil & Gas end-user segment is the fastest-growing category-level segment, driven by deepwater exploration and production investment across global offshore basins.

North America held approximately 24% of the global Ropes Market share in 2025, with the United States serving as the dominant national market driven by the convergence of an expansive commercial maritime sector, large-scale offshore oil and gas operations in the Gulf of Mexico, rapidly growing offshore wind development along the Atlantic and Pacific coasts, and significant military and defense rope procurement through the U.S. Department of Defense (DoD). The U.S. Bureau of Safety and Environmental Enforcement (BSEE) regulates mooring system safety standards for offshore platforms operating in U.S. federal waters, driving specification of certified high-performance rope systems by operators including Chevron, ExxonMobil, and BP. Samson Rope Technologies (headquartered in Ferndale, Washington) and Cortland Limited are leading domestic suppliers serving the region’s offshore energy and marine markets.

The North American offshore wind sector, still in its early buildout phase relative to Europe, is rapidly accelerating, with BOEM having issued leases for over 20 GW of potential offshore wind capacity as of 2024 and multiple utility-scale projects under active development off the coasts of New York, Massachusetts, New Jersey, and Virginia. Each offshore wind installation vessel and floating wind platform represents substantial rope consumption for anchor handling, cable laying, and mooring operations. North American rope manufacturers are investing in specialty fiber rope production capabilities, particularly UHMWPE-based products, to capture the premium mooring and lifting rope opportunities associated with this offshore energy expansion wave.

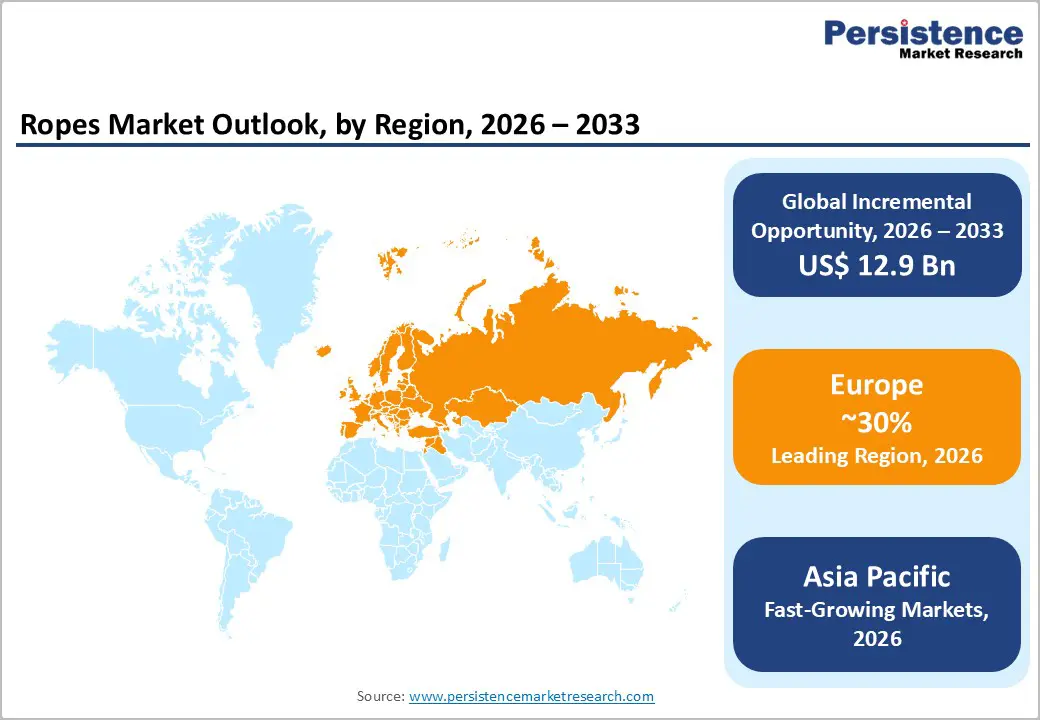

Europe is the leading regional market for ropes globally, accounting for approximately 30% of total market share in 2025, underpinned by the world’s most advanced offshore wind manufacturing and installation ecosystem, a deep maritime heritage with significant commercial shipping and port infrastructure, major fishing industry rope demand, and a sophisticated regulatory environment that sets global standards for rope safety performance. Germany, the United Kingdom, France, and Spain collectively form the backbone of European rope demand, with the offshore wind sector, centered on the North Sea, Celtic Sea, and Baltic Sea, as the fastest-growing application domain. The UK’s ambitious target of 50 GW of offshore wind capacity by 2030 and Germany’s accelerated offshore wind expansion plan are creating sustained, multi-year demand for floating and fixed-bottom turbine installation ropes, dynamic power cable installation systems, and maintenance access rope systems.

Teufelberger Holding AG (Austria), Lanex AS (Czech Republic), and Marlow Ropes (United Kingdom) are among the region’s leading rope manufacturers investing in advanced braiding technology, UHMWPE rope development, and specialty marine rope product lines. The European Maritime Safety Agency (EMSA) and SOLAS Convention requirements provide a well-defined regulatory framework that enforces rope safety standards across European-flagged vessels and port operations, supporting specification of premium-grade certified rope products. Spain’s fishing industry and France’s maritime and naval rope consumption add meaningful volume to the regional market. The EU’s Green Deal industrial investment framework and national offshore energy strategies are providing visibility into long-term project pipelines that allow European rope manufacturers to plan capacity expansion and product development investments with greater confidence.

Asia Pacific is the fastest-growing regional market for ropes, expected to register a CAGR of approximately 9.5-10% between 2026 and 2033, significantly above the global average, driven by the region’s dominant global shipbuilding industry, vast and expanding fishing fleet, rapidly growing offshore energy sector, and large-scale construction and mining activity across major economies. China is the world’s largest shipbuilder, accounting for approximately 50% of global ship deliveries by gross tonnage according to Lloyd’s Register, generating enormous volumes of wire rope and synthetic fiber rope demand for vessel outfitting, mooring equipment, and anchor chain systems. China is also advancing rapidly in offshore wind development, with the National Energy Administration (NEA) reporting cumulative offshore wind capacity exceeding 37 GW by end-2023, the world’s largest, and ambitious further expansion targets driving growing demand for specialized mooring and installation ropes.

Japan is a technologically advanced rope market, with specialized manufacturers including Dong Yang Rope Mfg. Co., Ltd. and domestic Japanese suppliers serving the country’s precision marine, fishing, and industrial sectors. India is an important high-growth market, with the country’s massive fishing industry, one of the world’s largest with approximately 3.5 million active fishermen according to the Ministry of Fisheries, Animal Husbandry and Dairying, generating substantial natural and synthetic fiber rope demand, while accelerating construction and port infrastructure investment under the National Infrastructure Pipeline (NIP) is driving wire rope and synthetic rope consumption in lifting and rigging applications. Axiom Cordages Ltd. is among India’s leading domestic rope producers serving both national and export markets. Across ASEAN, particularly in Indonesia, Vietnam, Thailand, and the Philippines, growing fishing, aquaculture, and maritime logistics sectors are generating incremental rope demand that is expected to contribute materially to Asia Pacific’s regional market leadership through 2033.

The global ropes market is moderately fragmented, comprising a mix of large vertically integrated manufacturers and numerous regional and application-focused producers. Market concentration is higher in the wire rope segment, where established players benefit from scale economies, standardized specifications, and entrenched relationships with mining, construction, and energy customers. In contrast, synthetic and specialty rope segments remain more differentiated, driven by engineering customization and performance-based specifications.

Competitive strategy centers on product reliability, certification compliance, and technical support capabilities, particularly for offshore, marine, and heavy-lifting applications where safety standards are stringent. Companies are investing in high-performance fiber technologies, advanced braiding and construction techniques, and expanded inspection and lifecycle service networks to secure recurring replacement demand. Increasing emphasis is also placed on integrated solutions, including rope health monitoring systems with embedded sensors for predictive maintenance in offshore energy operations. Strategic partnerships across the fiber supply chain and targeted expansion into deepwater energy and defense applications are shaping long-term competitive positioning.

The ropes market is projected to reach US$ 18.6 billion in 2026, driven by maritime trade growth, offshore wind expansion, and rising adoption of synthetic fiber ropes.

Demand is fueled by offshore wind installations, expanding global shipping activity, and recurring mooring and replacement needs across commercial fleets.

Europe leads with around 30% share, supported by a strong offshore wind industry and advanced maritime operations.

Major opportunities include floating offshore wind mooring systems and deep mining hoisting applications.

Key players include Bridon-Bekaert, WireCo, Samson Rope, Teufelberger, Marlow Ropes, Cortland, Yale Cordage, and others.

| Report Attribute | Details |

|---|---|

| Historical Data/Actuals | 2020 - 2025 |

| Forecast Period | 2026 - 2033 |

| Market Analysis Units | Value: US$ Mn/Bn, Volume: As Applicable |

| Geographical Coverage |

|

| Segmental Coverage |

|

| Competitive Analysis |

|

| Report Highlights |

|

By Product Type

By Rope Design

By End User

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author