- Executive Summary

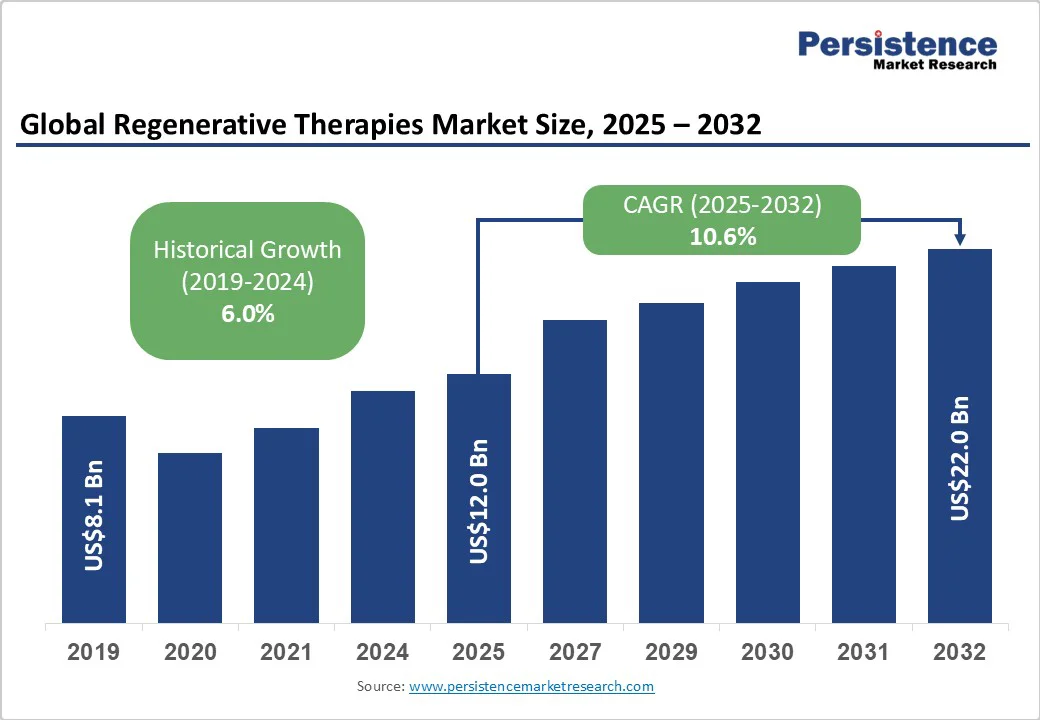

- Global Regenerative Therapies Market Snapshot, 2025 and 2032

- Market Opportunity Assessment, 2025 - 2032, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-economic Factors

- Global Sectoral Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Tool Adoption Analysis

- Regulatory Landscape

- Value Chain Analysis

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Analysis, 2024A

- Key Highlights

- Key Factors Impacting Deployment Costs

- Pricing Analysis, By Application

- Global Regenerative Therapies Market Outlook

- Key Highlights

- Market Volume (Units) Projections

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2019-2024

- Current Market Size (US$ Bn) Analysis and Forecast, 2025 - 2032

- Global Regenerative Therapies Market Outlook: Therapy Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Therapy Type, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Therapy Type, 2025 - 2032

- Cell Therapy

- Gene Therapy

- Tissue Engineering

- Biomaterials

- Market Attractiveness Analysis: Therapy Type

- Global Regenerative Therapies Market Outlook: Application

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Application, 2019 - 2024

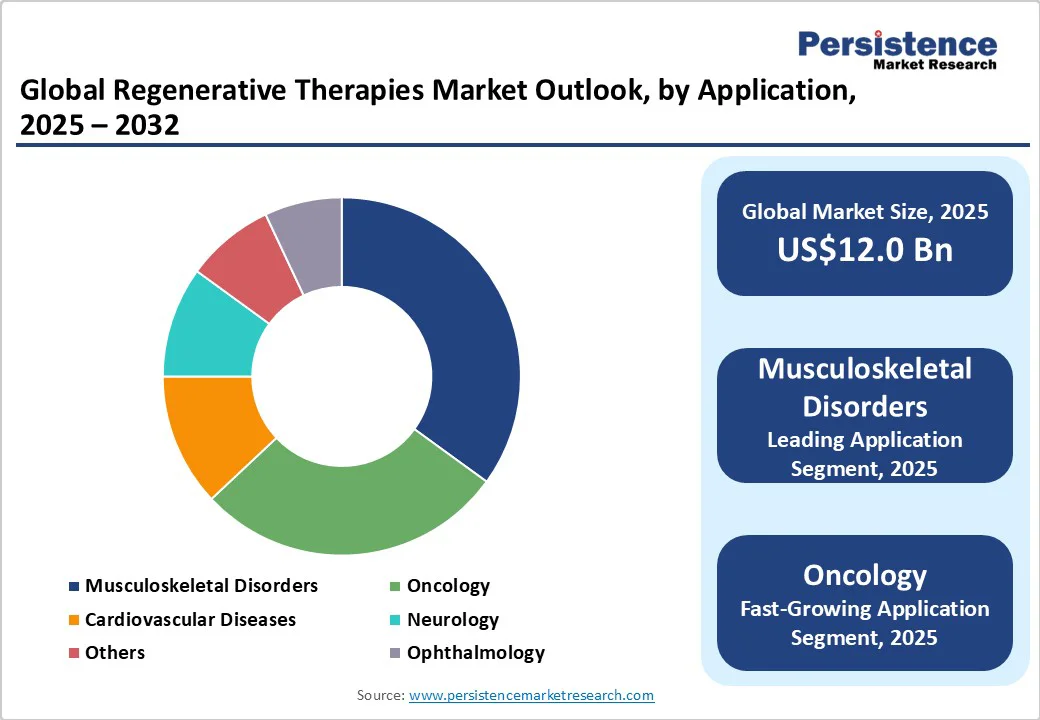

- Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2025 - 2032

- Musculoskeletal Disorders

- Oncology

- Cardiovascular Diseases

- Neurology

- Ophthalmology

- Others

- Market Attractiveness Analysis: Application

- Global Perlite Market Outlook: End-user

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By End-user, 2019 - 2024

- Current Market Size (US$ Bn) Analysis and Forecast, By End-user, 2025 - 2032

- Hospitals

- Specialty Clinics

- Academic & Research Institutes

- Commercial & Industrial Sectors

- Government Institutions

- Market Attractiveness Analysis: End-user

- Key Highlights

- Global Regenerative Therapies Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Region, 2019 - 2024

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Region, 2025 - 2032

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Regenerative Therapies Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2019 - 2024

- By Country

- By Therapy Type

- By Application

- By End-user

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2032

- U.S.

- Canada

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Therapy Type, 2025 - 2032

- Cell Therapy

- Gene Therapy

- Tissue Engineering

- Biomaterials

- Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2025 - 2032

- Musculoskeletal Disorders

- Oncology

- Cardiovascular Diseases

- Neurology

- Ophthalmology

- Others

- Current Market Size (US$ Bn) Analysis and Forecast, By End-user, 2025-2032

- Hospitals

- Specialty Clinics

- Academic & Research Institutes

- Commercial & Industrial Sectors

- Government Institutions

- Market Attractiveness Analysis

- Europe Regenerative Therapies Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2019 - 2024

- By Country

- By Therapy Type

- By Application

- End-user

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2032

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Therapy Type, 2025 - 2032

- Cell Therapy

- Gene Therapy

- Tissue Engineering

- Biomaterials

- Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2025 - 2032

- Musculoskeletal Disorders

- Oncology

- Cardiovascular Diseases

- Neurology

- Ophthalmology

- Others

- Current Market Size (US$ Bn) Analysis and Forecast, By End-user, 2025-2032

- Hospitals

- Specialty Clinics

- Academic & Research Institutes

- Commercial & Industrial Sectors

- Government Institutions

- Market Attractiveness Analysis

- East Asia Regenerative Therapies Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2019 - 2024

- By Country

- By Therapy Type

- By Application

- By End-user

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2032

- China

- Japan

- South Korea

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Therapy Type, 2025 - 2032

- Cell Therapy

- Gene Therapy

- Tissue Engineering

- Biomaterials

- Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2025 - 2032

- Musculoskeletal Disorders

- Oncology

- Cardiovascular Diseases

- Neurology

- Ophthalmology

- Others

- Current Market Size (US$ Bn) Analysis and Forecast, By End-user, 2025-2032

- Hospitals

- Specialty Clinics

- Academic & Research Institutes

- Commercial & Industrial Sectors

- Government Institutions

- Market Attractiveness Analysis

- South Asia & Oceania Regenerative Therapies Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2019 - 2024

- By Country

- By Therapy Type

- By Application

- By End-user

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2032

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Therapy Type, 2025 - 2032

- Cell Therapy

- Gene Therapy

- Tissue Engineering

- Biomaterials

- Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2025 - 2032

- Musculoskeletal Disorders

- Oncology

- Cardiovascular Diseases

- Neurology

- Ophthalmology

- Others

- Current Market Size (US$ Bn) Analysis and Forecast, By End-user, 2025-2032

- Hospitals

- Specialty Clinics

- Academic & Research Institutes

- Commercial & Industrial Sectors

- Government Institutions

- Market Attractiveness Analysis

- Latin America Regenerative Therapies Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2019 - 2024

- By Country

- By Therapy Type

- By Application

- By End-user

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2032

- Brazil

- Mexico

- Rest of Latin America

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Therapy Type, 2025 - 2032

- Cell Therapy

- Gene Therapy

- Tissue Engineering

- Biomaterials

- Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2025 - 2032

- Musculoskeletal Disorders

- Oncology

- Cardiovascular Diseases

- Neurology

- Ophthalmology

- Others

- Current Market Size (US$ Bn) Analysis and Forecast, By End-user, 2025-2032

- Hospitals

- Specialty Clinics

- Academic & Research Institutes

- Commercial & Industrial Sectors

- Government Institutions

- Market Attractiveness Analysis

- Middle East & Africa Regenerative Therapies Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2019 - 2024

- By Country

- By Therapy Type

- By Application

- By End-user

- Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2032

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Therapy Type, 2025 - 2032

- Cell Therapy

- Gene Therapy

- Tissue Engineering

- Biomaterials

- Current Market Size (US$ Bn) Analysis and Forecast, By Application, 2025 - 2032

- Musculoskeletal Disorders

- Oncology

- Cardiovascular Diseases

- Neurology

- Ophthalmology

- Others

- Current Market Size (US$ Bn) Analysis and Forecast, By End-user, 2025-2032

- Hospitals

- Specialty Clinics

- Academic & Research Institutes

- Commercial & Industrial Sectors

- Government Institutions

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- Novartis AG

- Overview

- Segments and Deployments

- Key Financials

- Market Developments

- Market Strategy

- Pfizer Inc.

- BlueRock Therapeutics

- Athersys, Inc.

- Mesoblast

- Sangamo Therapeutics

- TiGenix

- Celyad Oncology

- Fate Therapeutics

- Orchard Therapeutics

- Regen Lab

- Cook Biotech

- Novartis AG

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Biotechnology

- Regenerative Therapies Market

Regenerative Therapies Market Trends, Size, Share, and Growth Forecast, 2025 - 2032

Regenerative Therapies Market by Therapy Type (Cell Therapy, Gene Therapy, Others), Application (Musculoskeletal Disorders, Oncology, Others), End-User (Hospitals, Specialty Clinics, Academic & Research Institutes, Others), and Regional Analysis for 2025 - 2032

Key Industry Highlights:

- Leading & Fastest-growing Therapy Types: Cell therapy holds a dominant market share of approximately 45.0%, while gene therapy is the fastest-growing segment with a CAGR of over 30%.

- Dominant Region & Fastest-growing Regional Market: At around 45.0%, North America leads the regional market share, while Asia Pacific is expected to be the fastest-growing region at an approximately 21% CAGR during 2025-2032.

- Leading End-user: Hospitals contribute over 55.0% of the market revenue share, but clinics are expanding rapidly at a 22% CAGR.

- Regulatory advances such as the U.S. RMAT designation and EMA harmonization have accelerated regenerative therapy commercialization.

- Strategic M&A activities and capacity expansions illustrate growing competitive dynamics among leading firms.

| Key Insights | Details |

|---|---|

|

Regenerative Therapies Market Size (2025E) |

US$12.0 Bn |

|

Market Value Forecast (2032F) |

US$22.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

10.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Prevalence of Chronic and Degenerative Diseases

The growing global burden of chronic diseases such as cardiovascular disorders, diabetes, neurodegenerative diseases, and cancer is the primary market driver. According to the World Health Organization (WHO), chronic diseases killed over 43 million people globally in 2021. These numbers bolster the demand for regenerative therapies that provide curative rather than symptomatic treatment. This trend accelerates clinical research and market adoption, with cancer-focused regenerative therapies constituting nearly 50% of current pipelines, fueling a rapidly expanding market segment.

Technological Advancements and Innovation

Breakthroughs in stem cell research, CRISPR gene editing, tissue engineering, and biomaterial science have enabled the development of novel regenerative products with enhanced efficacy and safety profiles. The U.S. FDA’s approval of pluripotent stem cell-derived therapies, such as BlueRock Therapeutics’ DA01, exemplifies regulatory validation of these innovations. Coupled with advances in manufacturing automation, these developments lower production costs and improve scalability, driving accelerated commercialization globally.

Supportive Regulatory Environment and Funding

Governments worldwide, especially in North America and Asia Pacific, have instituted expedited regulatory pathways and increased funding to support regenerative medicine R&D. For example, the U.S. has implemented the Regenerative Medicine Advanced Therapy (RMAT) designation to fast-track clinical trials. Public-private partnerships and venture capital investment surged to US$22.7 Billion in 2021, according to the Alliance for Regenerative Medicine, enabling accelerated development and broader market access.

Barrier Analysis - High Treatment and Manufacturing Costs

The intricate manufacturing processes and the need for personalized treatments make regenerative therapies costly. High prices limit broad adoption, particularly in emerging markets. The evolving reimbursement landscape also presents uncertainties, contributing to a barrier that could slow market penetration by approximately 10-15% until cost-efficient solutions mature.

Regulatory and Ethical Challenges

Despite positive regulatory movements, inconsistencies across regions, particularly in Asia Pacific and Europe, create approval delays and complicate global commercialization strategies. Additionally, ethical concerns related to stem cell sourcing and genetic modification pose ongoing risks, mandating rigorous compliance that can slow clinical trial progression by 6-12 months on average, impacting market timelines.

Opportunity Analysis - Expansion in Emerging Markets

Asian economies, led by China, Japan, and India, represent lucrative growth frontiers driven by expanding healthcare infrastructure and growing patient populations. China regenerative medicine market is growing at over 20.0% CAGR, propelled by increasing government funding and rapid adoption of advanced therapies, potentially contributing an additional US$10 Billion to global revenues by 2030.

Convergence of Technologies and Unaddressed Clinical Needs & Niche Indications

Integrating AI, machine learning, and 3D bioprinting with regenerative medicine unlocks new avenues for precise therapy development and customized treatments. The advent of AI-enabled drug discovery could reduce R&D timelines by up to 30%, enhancing pipeline efficiency and supporting faster time-to-market. Moreover, therapies targeting rare diseases and complex indications such as spinal cord injuries and autoimmune conditions remain underserved, presenting niches that could generate an incremental market size of US$5-7 Billion by 2032. Focused investment in these areas promises early mover advantages as competitors develop scalable solutions.

Category-wise Analysis

Therapy Type Insights

Cell therapy is set to continue to dominate the regenerative therapies market with an approximate 45.0% share in 2025, driven by its widespread clinical use, particularly in oncology and musculoskeletal disorder treatments. Stem cell therapies maintain leadership due to their proven clinical efficacy and extensive presence in the development pipeline, supported by a growing number of Phase II and III trials.

Gene therapy is emerging rapidly, forecasted to outpace other segments with a CAGR exceeding 30.0% through 2032. This acceleration is largely attributable to advancements in precision gene-editing technologies such as CRISPR-Cas systems and expanding regulatory frameworks that expedite approval processes. The transition from predominantly ex vivo approaches toward in vivo gene therapies is broadening therapeutic indications beyond cancers to include rare genetic diseases, cardiovascular disorders, and metabolic conditions. This expansion not only opens new treatment possibilities but also attracts significant investor and commercial interest, marking gene therapy as a pivotal driver of future market growth.

Application Insights

Musculoskeletal disorders are expected to hold the largest share, constituting nearly 35.0% of the regenerative therapies application market in 2025. This prominence stems from demographic shifts such as global population aging and increased prevalence of degenerative conditions such as osteoarthritis and spinal injuries. Osteoarthritis prevalence peaks in populations aged above 55 years, accounting for approximately 73.0% of cases worldwide, necessitating regenerative interventions focused on cartilage regeneration and bone repair. The urgent unmet needs among chronic musculoskeletal patients have catalyzed increased R&D investments, leading to innovative therapies targeting tissue regeneration and pain management.

Oncology is the fastest-growing application segment, with a projected CAGR exceeding 28.0%, propelled by breakthroughs in CAR-T cell therapies and other immuno-oncology modalities that are revolutionizing treatment paradigms. The rising global cancer incidence is intensifying the demand for personalized, curative interventions, with CAR-T therapies demonstrating substantial success in hematologic malignancies. This has triggered an influx of clinical trials and upper-level regulatory approvals in major markets, including the U.S. and Europe, driving significant commercial potential.

End-user Analysis

Hospitals currently dominate, accounting for about 55.0% of the revenue share in 2025. This leadership is underpinned by their comprehensive clinical infrastructure, high patient throughput, and capabilities to perform complex regenerative procedures such as CAR-T cell infusions and autologous stem cell transplantation. The multidisciplinary care teams and availability of specialized technological equipment allow hospitals to efficiently manage therapy administration and post-procedural monitoring.

Conversely, specialty clinics are emerging as the fastest-growing end-user segment, expanding at about 22.0% CAGR. Their growth reflects advantages such as lower operational overhead, improved patient convenience, and the increasing adoption of minimally invasive regenerative treatments and aesthetic procedures suitable for outpatient settings. These clinics capitalize on technological advancements, enabling simplified therapeutic delivery and facilitating access to regenerative treatments outside traditional hospital environments. This evolving landscape signals diversification of care delivery channels and expanding market access options.

Regional Insights

North America Regenerative Therapies Market Trends

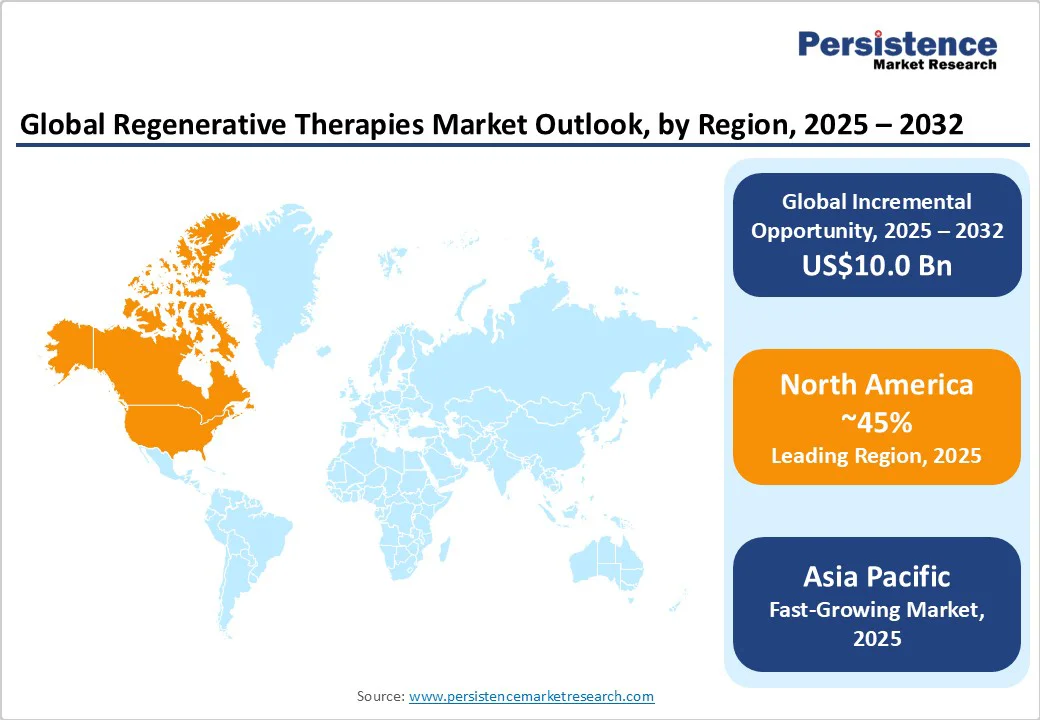

North America is the undisputed leader in the regenerative therapies market, commanding a 45.0% share valued at around US$19.1 Billion in 2025. The United States spearheads regional growth supported by forward-looking regulatory policies such as the FDA's Regenerative Medicine Advanced Therapy (RMAT) designation, designed to accelerate development and market entry of breakthrough therapies.

The U.S. invests over USD8 Billion annually in research and development, resulting in a dynamic innovation ecosystem characterized by frequent product launches, strategic partnerships, and a rich therapeutic pipeline comprising cell, gene, and tissue engineering modalities. Venture capital deployment remains high, nurturing startups with niche regenerative platforms and expediting commercialization efforts. Additionally, a rising incidence of chronic diseases, including cancer, diabetes, and neurodegenerative conditions, sustains demand, positioning North America as an innovation and market expansion hub.

Europe Regenerative Therapies Market Trends

Europe is anticipated to account for approximately 25.0% of the regenerative therapies market share, propelled by key contributors such as Germany, the U.K., France, and Spain. Regulatory harmonization under the European Medicines Agency (EMA) facilitates streamlined market access across member states, although approval timelines generally lag behind U.S. benchmarks, moderating growth rates to an estimated 18.0% CAGR through 2032.

Strong collaborations between academia and industry bolster translational research, particularly in orthopedics and cardiovascular applications, supported by increasing healthcare expenditure. Robust public-private partnerships and targeted funding initiatives also drive steady market expansion by supporting clinical trial activities and commercialization. Europe's focus on integrated healthcare delivery models and diverse patient populations ensures sustained demand for regenerative therapies in both urban and rural settings.

Asia Pacific Regenerative Therapies Market Trends

Asia Pacific emerges as the fastest-growing regional market with a leading CAGR through 2032. Growth is powered by expansive government support mechanisms, major investments in healthcare infrastructure, and cost efficiencies in biotechnology manufacturing and clinical trials relative to Western counterparts.

China leads the region, with the regenerative medicine market anticipated to exceed US$15 Billion by 2030, driven by proactive regulatory reforms and significant private sector involvement. Other countries in the region, including India and ASEAN members, are progressively aligning regulatory standards with global best practices, facilitating smoother market entry and international collaborations. The competitive landscape reflects a mix of established multinational corporations and local biotech firms, intensifying R&D activities and market penetration efforts. Furthermore, increasing middle-class population, rising prevalence of chronic diseases, and enhanced public healthcare awareness collectively contribute to sustained demand growth.

Competitive Landscape

The global regenerative therapies market landscape is moderately consolidated, with the top 10 players commanding approximately 65% of revenue. Leading firms include Novartis, Pfizer, and BlueRock Therapeutics. Market concentration has intensified in cell and gene therapy segments, while tissue engineering remains more fragmented. Competitive positioning centers on innovation, leadership, and partnership-driven growth. Market leaders are prioritizing innovation through R&D, extensive collaborations, and geographic expansion. Cost leadership is less prevalent due to the high-value nature of therapies, while personalized medicine business models gain traction.

Strategic Developments

- In September 2025, researchers at the University of Zurich used neural stem cell transplants derived from human induced pluripotent stem cells in mice one week after stroke. The treatment restored motor function, regenerated neurons, reduced inflammation, improved blood-brain barrier integrity, and promoted new blood vessel growth. Transplanted cells survived up to five weeks, integrated with existing brain cells, and delaying treatment by a week enhanced graft survival.

- In September 2025, an international team led by CAMH and the University of Aberdeen received £500,000 (US$610,000) to advance a novel multiple sclerosis (MS) treatment that halts disease progression and repairs nerve damage. Targeting excitotoxicity, a process that kills neurons in MS, the therapy promotes remyelination and functional recovery. In animal studies, it restored motor function even when administered after symptom onset. The project is in the final preclinical stages, with industry partners sought for clinical trials.

- In August 2025, KK Care Hospital in Pune, India, partnered with ORTHOReNEW (powered by Regenexx USA) to introduce advanced non-surgical orthopedic and regenerative medicine treatments, offering alternatives to surgery for conditions such as soft-tissue injuries, early degenerative bone issues, ligament & tendon damage. The procedures involve the patient’s own biological materials (such as super-concentrated platelets and mesenchymal cells), processed and reinjected under guidance, aiming for pain relief and functional recovery.

Companies Covered in Regenerative Therapies Market

- Novartis AG

- Pfizer Inc.

- BlueRock Therapeutics

- Athersys, Inc.

- Mesoblast

- Sangamo Therapeutics

- TiGenix

- Celyad Oncology

- Fate Therapeutics

- Orchard Therapeutics

- Regen Lab

- Cook Biotech

Frequently Asked Questions

The regenerative therapies market is projected to reach US$12.0 Billion in 2025.

Key drivers include the rising prevalence of chronic diseases, ongoing technological advances, and evolving regulatory support.

The regenerative therapies market is poised to witness a CAGR of 10.6% from 2025 to 2032.

Innovations in stem cell therapies, gene editing, and tissue engineering, supported by rising investments and expanding clinical applications, are the key market opportunities.

Novartis, Pfizer, and BlueRock Therapeutics are some of the key market players.