- Executive Summary

- Global Pulmonary Embolism Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 – 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors – Relevance and Impact

- Value Added Insights

- Regulatory Landscape

- Product Adoption Analysis

- Value Chain Analysis

- Key Deals and Mergers

- PESTLE Analysis

- Porter’s Five Force Analysis

- Global Pulmonary Embolism Market Outlook:

- Key Highlights

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, 2026–2033

- Global Pulmonary Embolism Market Outlook: Treatment

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Treatment, 2020 – 2025

- Market Size (US$ Bn) Analysis and Forecast, By Treatment, 2026 – 2033

- Surgery

- Medications

- Mechanical Devices

- Others

- Market Attractiveness Analysis: Treatment

- Global Pulmonary Embolism Market Outlook: Diagnosis

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Diagnosis, 2020 – 2025

- Market Size (US$ Bn) Analysis and Forecast, By Diagnosis, 2026 – 2033

- MRI

- CT Scan

- ECG

- Chest X-Ray

- Pulmonary Angiography

- Venous Ultrasound

- Venography

- D-Dimer Test

- Others

- Market Attractiveness Analysis: Diagnosis

- Global Pulmonary Embolism Market Outlook: Symptom

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Symptom, 2020 – 2025

- Market Size (US$ Bn) Analysis and Forecast, By Symptom, 2026 – 2033

- Shortness of Breath

- Cough

- Chest Pain

- Fever

- Dizziness

- Cyanosis

- Irregular Heartbeat

- Others

- Market Attractiveness Analysis: Symptom

- Global Pulmonary Embolism Market Outlook: End User

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By End User, 2020 – 2025

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 – 2033

- Specialty Clinics

- Hospitals

- Homecare

- Others

- Market Attractiveness Analysis: End User

- Key Highlights

- Global Pulmonary Embolism Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Region, 2020 – 2025

- Market Size (US$ Bn) Analysis and Forecast, By Region, 2026 – 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Pulmonary Embolism Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Treatment

- By Diagnosis

- By Symptom

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- U.S.

- Canada

- Market Size (US$ Bn) Analysis and Forecast, By Treatment, 2026 – 2033

- Surgery

- Medications

- Mechanical Devices

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Diagnosis, 2026 – 2033

- MRI

- CT Scan

- ECG

- Chest X-Ray

- Pulmonary Angiography

- Venous Ultrasound

- Venography

- D-Dimer Test

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Symptom, 2026 – 2033

- Shortness of Breath

- Cough

- Chest Pain

- Fever

- Dizziness

- Cyanosis

- Irregular Heartbeat

- Others

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 – 2033

- Specialty Clinics

- Hospitals

- Homecare

- Others

- Market Attractiveness Analysis

- Europe Pulmonary Embolism Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Treatment

- By Diagnosis

- By Symptom

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Market Size (US$ Bn) Analysis and Forecast, By Treatment, 2026 – 2033

- Surgery

- Medications

- Mechanical Devices

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Diagnosis, 2026 – 2033

- MRI

- CT Scan

- ECG

- Chest X-Ray

- Pulmonary Angiography

- Venous Ultrasound

- Venography

- D-Dimer Test

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Symptom, 2026 – 2033

- Shortness of Breath

- Cough

- Chest Pain

- Fever

- Dizziness

- Cyanosis

- Irregular Heartbeat

- Others

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 – 2033

- Specialty Clinics

- Hospitals

- Homecare

- Others

- Market Attractiveness Analysis

- East Asia Pulmonary Embolism Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Treatment

- By Diagnosis

- By Symptom

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) Analysis and Forecast, By Treatment, 2026 – 2033

- Surgery

- Medications

- Mechanical Devices

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Diagnosis, 2026 – 2033

- MRI

- CT Scan

- ECG

- Chest X-Ray

- Pulmonary Angiography

- Venous Ultrasound

- Venography

- D-Dimer Test

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Symptom, 2026 – 2033

- Shortness of Breath

- Cough

- Chest Pain

- Fever

- Dizziness

- Cyanosis

- Irregular Heartbeat

- Others

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 – 2033

- Specialty Clinics

- Hospitals

- Homecare

- Others

- Market Attractiveness Analysis

- South Asia & Oceania Pulmonary Embolism Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Treatment

- By Diagnosis

- By Symptom

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) Analysis and Forecast, By Treatment, 2026 – 2033

- Surgery

- Medications

- Mechanical Devices

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Diagnosis, 2026 – 2033

- MRI

- CT Scan

- ECG

- Chest X-Ray

- Pulmonary Angiography

- Venous Ultrasound

- Venography

- D-Dimer Test

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Symptom, 2026 – 2033

- Shortness of Breath

- Cough

- Chest Pain

- Fever

- Dizziness

- Cyanosis

- Irregular Heartbeat

- Others

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 – 2033

- Specialty Clinics

- Hospitals

- Homecare

- Others

- Market Attractiveness Analysis

- Latin America Pulmonary Embolism Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Treatment

- By Diagnosis

- By Symptom

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) Analysis and Forecast, By Treatment, 2026 – 2033

- Surgery

- Medications

- Mechanical Devices

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Diagnosis, 2026 – 2033

- MRI

- CT Scan

- ECG

- Chest X-Ray

- Pulmonary Angiography

- Venous Ultrasound

- Venography

- D-Dimer Test

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Symptom, 2026 – 2033

- Shortness of Breath

- Cough

- Chest Pain

- Fever

- Dizziness

- Cyanosis

- Irregular Heartbeat

- Others

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 – 2033

- Specialty Clinics

- Hospitals

- Homecare

- Others

- Market Attractiveness Analysis

- Middle East & Africa Pulmonary Embolism Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Treatment

- By Diagnosis

- By Symptom

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) Analysis and Forecast, By Treatment, 2026 – 2033

- Surgery

- Medications

- Mechanical Devices

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Diagnosis, 2026 – 2033

- MRI

- CT Scan

- ECG

- Chest X-Ray

- Pulmonary Angiography

- Venous Ultrasound

- Venography

- D-Dimer Test

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Symptom, 2026 – 2033

- Shortness of Breath

- Cough

- Chest Pain

- Fever

- Dizziness

- Cyanosis

- Irregular Heartbeat

- Others

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 – 2033

- Specialty Clinics

- Hospitals

- Homecare

- Others

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details – Overview, Financials, Strategy, Recent Developments)

- Bayer AG

- Overview

- Segments and Products

- Key Financials

- Market Developments

- Market Strategy

- Johnson & Johnson

- Boehringer Ingelheim

- Pfizer Inc.

- Bristol-Myers Squibb

- Amgen Inc.

- Astellas Pharma Inc.

- Daiichi Sankyo Co. Ltd.

- F. Hoffmann La Roche Ltd.

- Eli Lilly and Co.

- Gilead Sciences Inc., Medtronic Plc, Inari Medical Inc.

- Novartis AG

- Sanofi

- Viatris Inc.

- Takeda Pharmaceutical Co. Ltd.

- Others

- Bayer AG

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Pharmaceuticals

- Pulmonary Embolism Market

Pulmonary Embolism Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Pulmonary Embolism Market by Treatment (Surgery, Medications, Mechanical Devices, Others), Diagnosis (MRI, CT Scan, ECG, Chest X-Ray,Pulmonary Angiography, Venous Ultrasound, Venography, D-Dimer Test, Others), Symptom (Shortness of Breath, Cough, Chest Pain, Fever, Dizziness, Cyanosis, Irregular Heartbeat, Others), End User (Specialty Clinics, Hospitals, Homecare, Others), and Regional Analysis from 2026 to 2033

Key Industry Highlights

- Dominant Segment: Medications account 68.1% share of the pulmonary embolism market in 2025, driven by first-line use of anticoagulants and thrombolytics across low- and intermediate-risk PE cases. Their clinical efficacy, ease of administration, guideline support, and broad availability make drug therapy the backbone of PE management globally.

- Dominant Region: North America leads the pulmonary embolism market with 38.0% share in 2025, supported by high disease awareness, advanced diagnostic imaging (CTPA), strong reimbursement, and early adoption of catheter-based interventions. Asia-Pacific is the fastest-growing region due to improving healthcare infrastructure, rising PE diagnosis rates, and expanding hospital and interventional capabilities.

- Market Drivers: Rising incidence of venous thromboembolism, aging population, increasing prevalence of obesity and cancer, improved diagnostic accuracy, wider use of DOACs, and growing adoption of minimally invasive PE treatment approaches are driving market growth.

- Market Opportunity: Key opportunities include growth of catheter-directed thrombectomy and thrombolysis, development of safer next-generation anticoagulants, expansion of PE response teams (PERT), improved risk-stratification tools, and increased adoption in emerging markets with improved emergency and cardiovascular care access.

| Global Market Attributes | Key Insights |

|---|---|

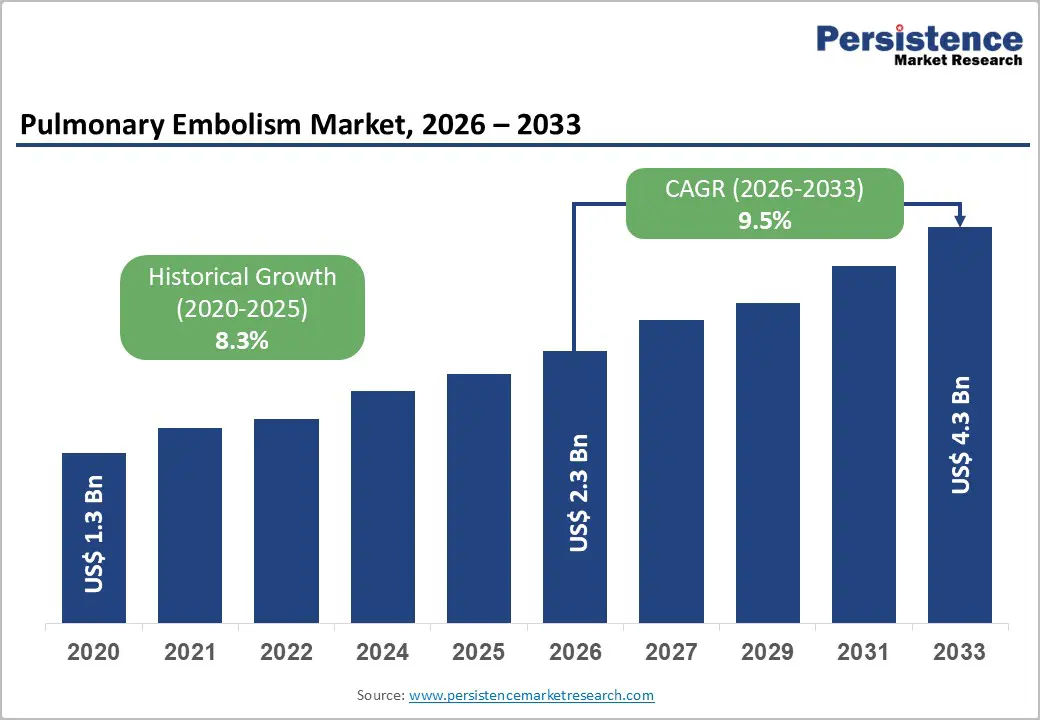

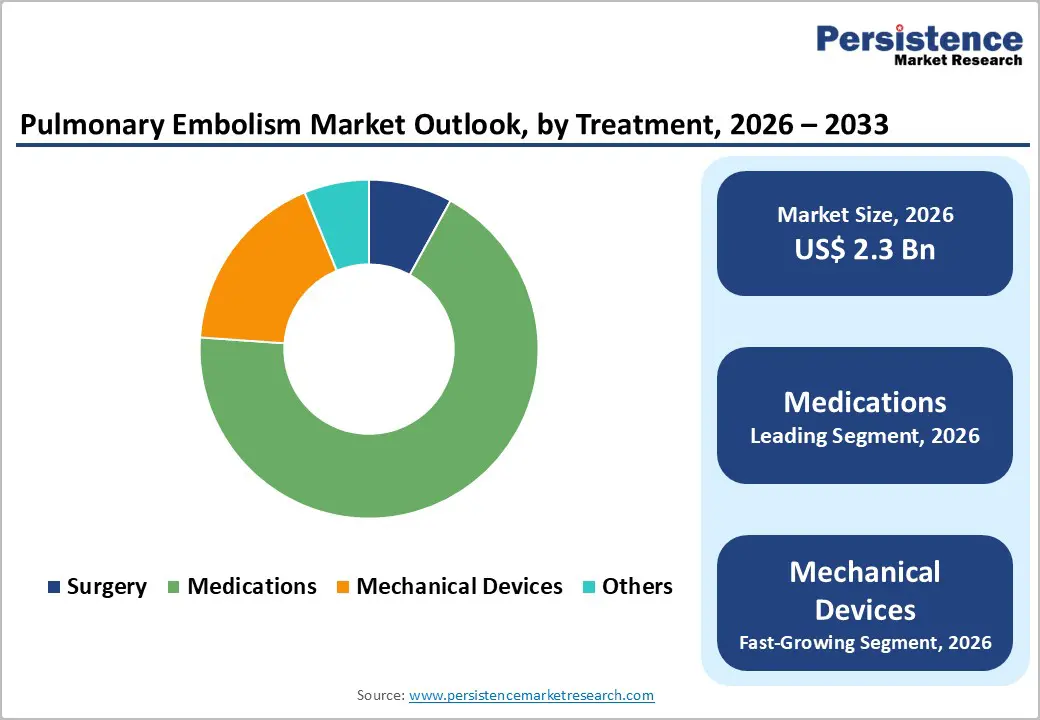

| Pulmonary Embolism Market Size (2026E) | US$ 2.3 Bn |

| Market Value Forecast (2033F) | US$ 4.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.3% |

Market Dynamics

Driver: Rising Incidence of Venous Thromboembolism and Aging Population

Pulmonary embolism (PE) is a major component of venous thromboembolism (VTE), which affects up to 900,000 people annually in the United States and is a leading cause of preventable hospital death. According to the CDC, VTE, including DVT and PE, results in an estimated 60,000–100,000 deaths each year in the U.S., and sudden death is the first symptom in about one-quarter of PE cases.

Age is a predominant risk factor for VTE and PE. Population-based studies show that incidence increases sharply with age: older adults aged 65–69 have an annual PE incidence of ≈approximately 1.3 per 1,000, rising to ≈approximately 2.8 per 1,000 by age 85–89. Moreover, epidemiological evidence indicates VTE rates (and therefore PE) increase from less than 5 per 100,000 in young adults to over 500 per 100,000 in adults aged ≥80 years. This aging-related rise in PE risk drives greater clinical demand for early detection, treatment, and long-term management.

Restraints: High Bleeding Risk Associated with Anticoagulant and Thrombolytic Therapies

Anticoagulant therapy is the clinical backbone of PE treatment, but bleeding risk remains a major concern that restricts uptake and intensity of use. Common anticoagulants such as warfarin carry an annual bleeding incidence of 15–20%, with life-threatening bleeds occurring in 1–3% per year among treated patients. This risk escalates in older or renal-impaired patients, who represent a substantial proportion of the PE population, complicating clinical choices and sometimes leading to underdosing or avoidance of optimal therapy.

Thrombolytic therapy, used for high-risk or hemodynamically unstable PE, also increases hemorrhagic complications. Systemic thrombolysis has been associated with major bleeding rates up to 13–20% and a 2–3% risk of intracranial hemorrhage in some PE cohorts. These risks often limit clinicians' willingness to use powerful lytic regimens except in life-threatening situations and underscore the need for safer alternatives. This bleeding safety concern restrains market growth by reducing utilization of aggressive treatment modalities and expanding the market need for novel anticoagulants or targeted therapies with better safety profiles.

Opportunity: Rapid Growth of Catheter-Directed Thrombectomy and Thrombolysis

Mechanical and catheter-based therapies for PE are emerging as a significant opportunity due to their potential to reduce clot burden while mitigating bleeding risk. Catheter-directed thrombolysis (CDT) and aspiration thrombectomy techniques have been adopted increasingly for intermediate- and high-risk PE where systemic thrombolysis poses excessive hemorrhagic risk. Meta-analyses and registry data indicate that CDT and mechanical thrombectomy are associated with lower mortality and favorable hemodynamic improvements while maintaining acceptable safety profiles compared with systemic thrombolysis or anticoagulation alone.

Specific data indicate that procedural complication rates (including major bleeding) with catheter-based interventions can be substantially lower (e.g., ~1.4–6.7% in some settings) than historical estimates for systemic thrombolysis. Additionally, emerging large-bore mechanical thrombectomy registries report favorable outcomes, with lower rates of clinical deterioration and readmission than CDT alone. These trends underscore a market opportunity: as catheter-directed approaches mature with better outcomes and guideline integration, adoption is increasing across interventional cardiology and radiology, expanding the PE treatment market beyond traditional anticoagulant therapy.

Category-wise Analysis

By Treatment, Medications Dominates the Pulmonary Embolism Market

Medications occupies 68.1% share of the global market in 2025, because they directly address the underlying pathophysiology: clot propagation and recurrence. The CDC reports that anticoagulant therapy remains the standard of care for most PE patients, reducing mortality and recurrent VTE (venous thromboembolism). Direct oral anticoagulants (DOACs) such as apixaban and rivaroxaban have demonstrated similar efficacy with lower major bleeding risk compared with traditional therapies (warfarin) in large, randomized trials, leading to widespread guideline adoption. A seasonally adjusted study showed that >80% of non-massive PE patients are managed primarily with anticoagulants, because these drugs can be administered safely in both inpatient and outpatient settings (CDC; AHA/ASA guidelines). Their ease of use, predictable pharmacokinetics, and avoidance of routine monitoring underpin their clinical dominance in PE management.

By Diagnosis, CT Scan dominates due to rapid, accurate imaging and widespread emergency adoption

Computed Tomography Pulmonary Angiography (CTPA) dominates PE diagnosis because it provides rapid, high-resolution visualization of the pulmonary vasculature and is widely accepted as the “gold standard” imaging modality. According to the American Thoracic Society, CTPA has >95% sensitivity and specificity for detecting central and segmental emboli, significantly outperforming older modalities such as ventilation/perfusion scans. The Centers for Medicare & Medicaid Services (CMS) data indicate that increased availability of multi-detector CT scanners has led to a steady rise in CTPA utilization in emergency settings, making it the first-line test in suspected PE. CTPA’s ability to concurrently assess alternative diagnoses (e.g., pneumonia, aortic dissection) enhances clinical decision-making and reduces diagnostic delay. Its rapid acquisition time and broad hospital accessibility ensure that the majority of suspected PE cases are confirmed or excluded with CT scans, solidifying its dominant role in the diagnostic algorithm.

Regional Insights

North America Pulmonary Embolism Market Trends

North America dominates the pulmonary embolism market with 38.0% share in 2025, due to a high disease burden and advanced healthcare infrastructure. In the United States alone, an estimated up to 900,000 people are affected by venous thromboembolism (VTE) annually, of which a substantial portion are pulmonary embolism cases making PE a significant clinical concern. The region benefits from widespread availability of advanced diagnosis and treatment technologies, including CT pulmonary angiography and direct oral anticoagulants, and a dense network of hospitals and specialty clinics equipped for rapid PE management. Strong reimbursement systems and substantial public health resources further support early detection and treatment. Collectively, these factors ensure North America retains the largest market share and clinical adoption rates globally.

Europe Pulmonary Embolism Market Trends

Europe constitutes a major portion of the pulmonary embolism market because of its large population base, extensive healthcare systems, and coordinated clinical guidelines for VTE and PE. Across more than 30 countries, over 2.8 million PE cases are reported annually, supported by widespread use of diagnostic imaging like CT pulmonary angiography and Doppler ultrasound. Integration of standardized treatment protocols by bodies such as the European Society of Cardiology enhances consistent clinical practices across the region. Public and private healthcare sectors maintain a large network of hospitals and imaging centers that facilitate early diagnosis and intervention. Europe’s aging demographics and rising cardiovascular risk factors also contribute to substantial demand for both PE diagnostics and therapeutics, making it a key regional market globally.

Asia-Pacific Pulmonary Embolism Market Trends

The Asia-Pacific region is the fastest-growing pulmonary embolism market due to expanding healthcare infrastructure, rising disease awareness, and increasing access to diagnostics and treatments. Countries such as China, India, Japan, and South Korea account for a large share of the region’s >2.2 million annual PE cases, driven by population size and rising cardiovascular disease prevalence. Rapid improvements in hospital capacity, adoption of CT pulmonary angiography, and increasing physician awareness contribute to higher diagnosis rates. Growth of interventional labs and adoption of catheter-directed therapies further fuel market expansion. Government healthcare reforms and increased healthcare spending are accelerating access to advanced PE care across urban and rural settings, positioning Asia-Pacific as a dynamic and fast-expanding regional market.

Market Competitive Landscape

The pulmonary embolism market is moderately competitive, led by pharmaceutical companies offering anticoagulants and thrombolytics, alongside device manufacturers providing catheter-directed thrombectomy systems. Competition is driven by clinical efficacy, safety profiles, technological innovation, and growing adoption of minimally invasive interventions across hospitals and emergency care settings.

Key Industry Developments:

- In February 2026, Bristol Myers Squibb and Johnson & Johnson launched a clinician-focused educational initiative titled “Change the Target. Change What’s Possible” to address unmet needs in cardiovascular and thromboembolic care. The program was developed to educate healthcare providers on thromboembolic conditions and the potential of targeting factor XIa (FXIa) to prevent dangerous clots while preserving normal clotting. It highlighted that many patients with atrial fibrillation remained undertreated and a significant portion of strokes were recurrent despite existing therapies.

- In January 2025, Bayer’s investigational antibody BAY-3018250 was developed to target alpha-2 antiplasmin (α2AP) for thrombotic cardiovascular conditions, including pulmonary embolism and deep vein thrombosis, and entered Phase II clinical testing. The candidate acted by enhancing clot breakdown, a novel mechanism compared with traditional anticoagulants.

Companies Covered in Pulmonary Embolism Market

- Bayer AG

- Johnson & Johnson

- Boehringer Ingelheim

- Pfizer Inc.

- Bristol-Myers Squibb

- Amgen Inc.

- Astellas Pharma Inc.

- Daiichi Sankyo Co. Ltd.

- F. Hoffmann La Roche Ltd.

- Eli Lilly and Co.

- Gilead Sciences Inc., Medtronic Plc, Inari Medical Inc.

- Novartis AG

- Sanofi

- Viatris Inc.

- Takeda Pharmaceutical Co. Ltd.

- Others

Frequently Asked Questions

The global pulmonary embolism market is projected to be valued at US$ 2.3 Bn in 2026.

Rising venous thromboembolism incidence, aging population, improved diagnostics, and expanding adoption of anticoagulants and minimally invasive therapies.

The global pulmonary embolism market is poised to witness a CAGR of 9.5% between 2026 and 2033.

Growth of catheter-based therapies, safer anticoagulants, AI-driven diagnostics, PE response teams, and emerging markets.

Bayer AG, Johnson & Johnson, Boehringer Ingelheim, Pfizer Inc., Bristol-Myers Squibb, Amgen Inc.