- Processed Food

- Protein Snacks Market

Protein Snacks Market Size, Share, and Growth Forecast 2026 - 2033

Protein Snacks Market by Product Type (Protein Bars, Chips & Crisps, Cookies & Biscuits, Yogurt & Dairy Snacks, Nuts & Seeds, Jerky, Others), Distribution Channel (Online Retail, Specialty Stores, Convenience Stores), and Regional Analysis, 2026 - 2033

Protein Snacks Market Share and Trends Analysis

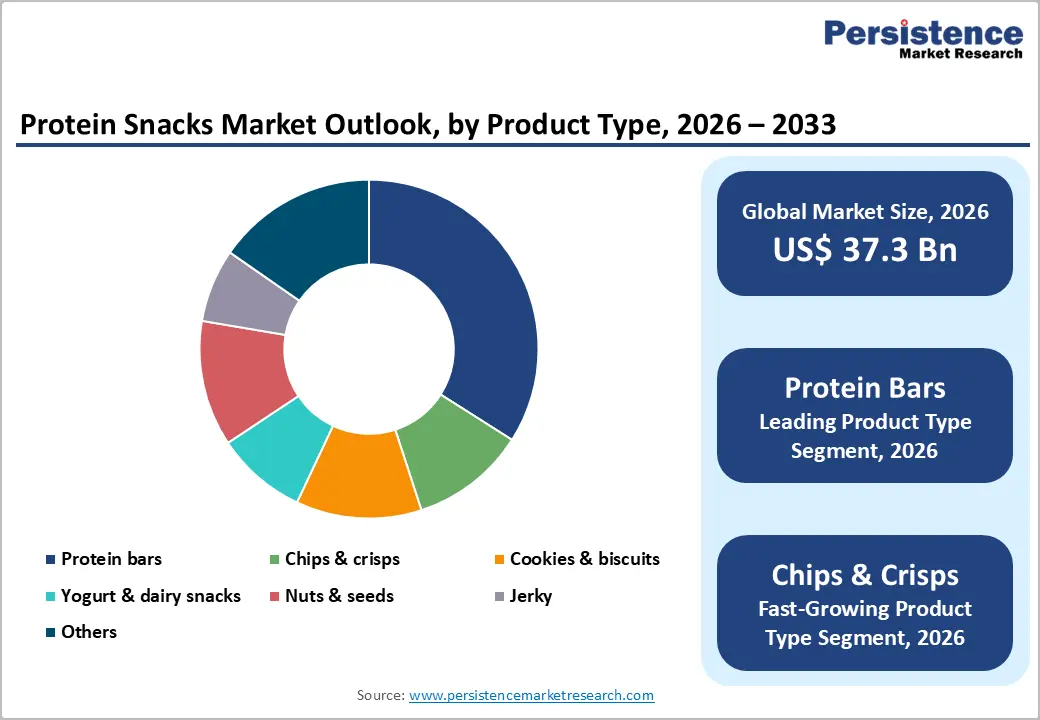

The global protein snacks market size is expected to be valued at US$ 37.3 billion in 2026 and projected to reach US$ 72.2 billion by 2033, growing at a CAGR of 9.9% between 2026 and 2033. This exceptional growth trajectory is driven by a structural, demographic-wide shift toward high-protein dietary patterns, accelerated by mainstream fitness culture adoption, sports nutrition democratization, and the rising consumer preference for snacks that deliver functional nutritional benefits alongside taste satisfaction.

According to the International Food Information Council (IFIC), protein is consistently the most sought-after functional nutrient by U.S. consumers, with over 60% actively trying to consume more protein in their diets. The convergence of the active lifestyle movement, aging population-driven muscle health awareness, and rising digital fitness engagement amplified by social media platforms and fitness apps is collectively expanding the protein snack consumer base far beyond traditional sports nutrition audiences into mainstream daily snacking occasions globally.

Key Industry Highlights:

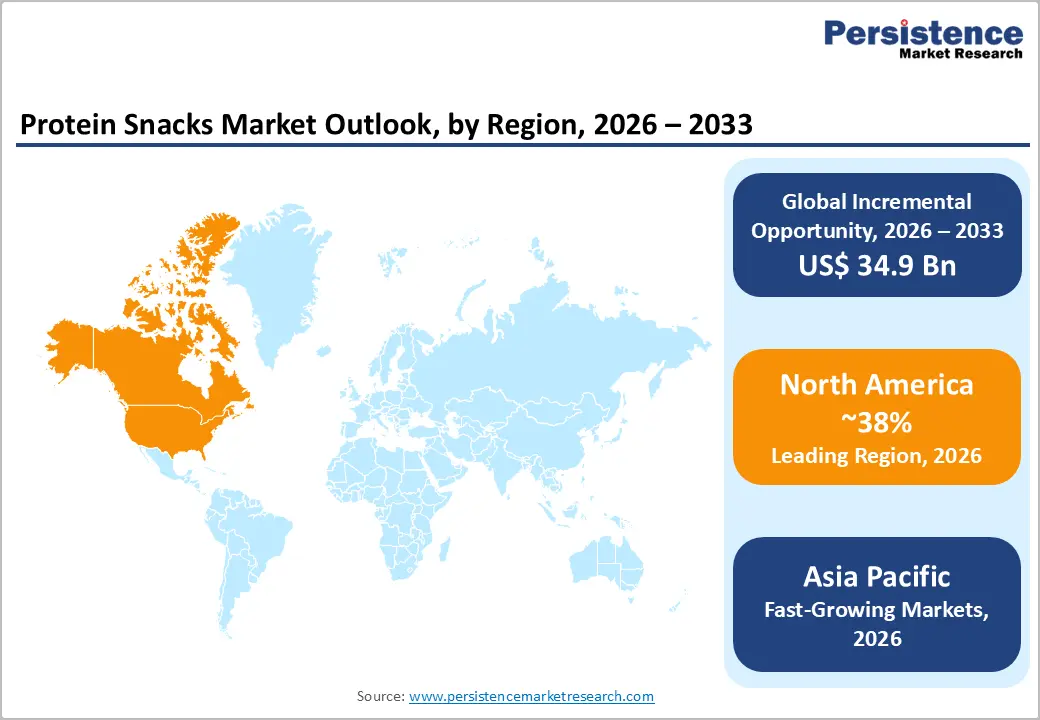

- Leading Region - North America held 38% of the global protein snacks market in 2025, anchored by the world's highest protein snack per-capita consumption, IFIC-documented 60%+ U.S. consumer protein prioritization, and the most competitive global protein snack brand ecosystem across online and specialty retail channels.

- Fastest Growing Region - Asia Pacific is the fastest-growing region (12.4% CAGR, 2026 - 2033), driven by China's explosive fitness culture expansion, India's 15-20% annual gym membership growth, and rapidly expanding e-commerce penetration, making premium protein snacks increasingly accessible to urban middle-class consumers.

- Dominant Product Segment - Protein Bars command 34% market share in 2025, reflecting their three-decade market leadership as the canonical protein snack format, with Quest, RXBAR, Clif Bar, and Kind collectively dominating global protein bar retail sales across specialty, grocery, and online channels.

- Fastest Growing Product - Chips & Crisps is the fastest-growing product type (2026 - 2033), driven by savory snacking innovation that pairs the world's most popular snack format with high-protein functionality, unlocking an enormous new consumer segment beyond traditional protein bar purchasers globally.

- Key Opportunity - Plant-Based Protein Snacks & Asia Pacific Penetration: Plant-based protein snack innovation and Asia Pacific market expansion, where fitness culture is growing at 12-20% annually and e-commerce channels are scaling rapidly, represent the highest-growth strategic opportunities for protein snack manufacturers through 2033, offering both premium pricing power and large new consumer pools.

Market Dynamics

Drivers - Sports Nutrition Democratization and Fitness Culture Driving Repeat Purchase Behavior

The global democratization of fitness culture and sports nutrition, driven by the rapid expansion of gym memberships, boutique fitness studios, digital workout platforms, and social media fitness influencers, has dramatically broadened the consumer base for protein snacks beyond competitive athletes into the mainstream active lifestyle segment. The International Health, Racquet & Sportsclub Association (IHRSA) reports that global gym membership has exceeded 184 million worldwide, and digital fitness platform subscriptions have grown exponentially post-pandemic.

Protein snacks have transitioned from post-workout specialist products to everyday consumption occasions consumed as breakfast replacements, mid-morning snacks, travel companions, and desk snacks by working professionals. According to Nielsen IQ, high-protein positioned food and beverage products have demonstrated consistent shelf velocity outperformance versus conventional alternatives across U.S. and European grocery channels, confirming the structural, repeat-purchase nature of protein snack demand across diverse shopper demographics.

Restraints - Ingredient Cost Volatility and Formulation Complexity for Clean-Label Protein Snacks

Manufacturing high-quality protein snacks to meet clean-label, natural ingredient, and non-GMO standards is technically complex and input cost-intensive. Key protein sources, including whey protein isolate, plant-based proteins (pea, soy, brown rice), and high-quality meat for jerky, are subject to commodity price volatility linked to agricultural cycles, supply chain disruptions, and competing demand from the broader food and supplement industries.

The USDA Agricultural Marketing Service data shows persistent volatility in dairy and soy commodity prices, which directly impacts formulation cost structures for protein bar and dairy snack manufacturers, creating margin pressure and potentially constraining product innovation investment for mid-size and emerging brand competitors.

Opportunities - Protein-Enriched Chips & Crisps: The Fastest-Growing Format Redefining Savory Snacking

Protein-enriched chips and crisps represent the fastest-growing product type within the global Protein Snacks market, capitalizing on the massive and deeply established consumer preference for savory, crunchy snack formats while delivering the functional protein benefits consumers actively seek. The convergence of traditional snack food appeal with high-protein positioning is unlocking an enormous new consumer segment, savory snackers who would not previously purchase protein bars or shakes but are receptive to familiar chip and crisp formats.

Brands including Quest Nutrition (Quest Chips), Wilde Protein Snacks, Chomps), and PotatoProtein-based formats are experiencing double-digit growth rates in U.S. and European convenience and online channels. According to the Snack Food Association (SFA), savory snacks represent over US$ 40 billion in annual U.S. retail sales, a base market of enormous scale that protein-enriched chip formats are beginning to penetrate meaningfully. Investment in extrusion technology, plant-based protein chip formulations, and clean-label savory protein formats positions manufacturers to capture the highest-growth revenue stream within the protein snacks category through 2033.

Category-wise Analysis

Product Type Insights

Protein Bars lead the product type category with a dominant 34% market share in 2025, reflecting their status as the canonical protein snack format offering the highest per-serving protein content, convenient portion-controlled packaging, and the broadest brand variety of any protein snack product type. Protein bars have benefited from over three decades of market development, creating deep brand loyalty among sports nutrition consumers and expanding into mainstream grocery, convenience, and e-commerce channels.

According to the Council for Responsible Nutrition (CRN), protein supplements and functional protein food consumption among U.S. adults have been growing consistently, with bars representing the most frequently purchased on-the-go format. Leading brands, including Quest Nutrition, RXBAR (Kellogg), Clif Bar, Kind (Mars Inc.), and The Simply Good Foods Company (Quest, Atkins) command the majority of bar segment share. Chips & Crisps represent the fastest-growing product type, driven by the savory snacking innovation wave that is making high-protein chip and crisp formats the fastest-emerging segment in the protein snacks category.

Distribution Channel Insights

Specialty stores lead the distribution channel category with approximately 38% share in 2025. Specialty health food retailers, including GNC, Vitamin Shoppe, Whole Foods Market, and Sprouts Farmers Market, serve as the primary discovery and trial channel for new protein snack brands, attracting health-conscious, label-reading consumers who prioritize ingredient quality, protein content, and dietary certifications.

Specialty stores provide premium shelf positioning and well-informed staff who support consumer education in the functional food segment. Online Retail is the fastest-growing distribution channel, driven by the scale of Amazon's supplement and health food marketplace, direct-to-consumer brand websites, and subscription snack box services. According to the U.S. Census Bureau, food and health product e-commerce has grown at over 15% annually since 2020, with protein snacks among the highest-velocity categories in health-positioned online food retail.

Regional Insights

North America leads the global Protein Snacks market with approximately 38% of total market share in 2025. Asia Pacific is the fastest-growing region, expanding at an estimated CAGR of approximately 12.4% through 2033, driven by China's fitness boom, India's rapidly growing urban health-conscious demographic, and expanding modern retail and e-commerce penetration across the region.

North America Protein Snacks Market Trends and Insights

North America is the most mature and commercially developed protein snacks market, characterized by the world's highest per-capita protein snack consumption, deep specialty and mass retail penetration, and the most competitive brand ecosystem globally. The U.S. leads regional demand, driven by pervasive fitness culture, the IFIC-documented protein nutrition priority of over 60% of Americans, and the continued premiumization of the snacking occasion toward functional, nutritionally meaningful products.

U.S. Protein Snacks Market Size

The U.S. accounts for approximately 85-87% of North American protein snack demand, with an estimated global market share of approximately 33% in 2025. The U.S. protein bar segment alone generates billions in annual retail sales across grocery, club, and specialty channels. The CRN's report that 74% of U.S. adults use dietary supplements reinforces the functional nutrition-oriented consumer base driving sustained protein snack market growth.

Europe Protein Snacks Market Trends and Insights

Europe is the second-largest regional market, with growing demand concentrated in the U.K., Germany, France, and Scandinavia. The region is experiencing accelerating protein snack adoption driven by gym culture expansion, rising health consciousness, and the rapid growth of plant-based and clean-label protein formats aligned with EU food labeling and health claim frameworks. The online retail channel is growing particularly strongly across European markets.

Germany Protein Snacks Market Size

Germany holds approximately 20-22% of European protein snack demand in 2025, supported by a large and growing fitness industry and strong consumer affinity for high-quality, clean-label functional foods. German consumers' premium quality orientation supports above-average spending on certified natural and organic protein snacks, with specialty health retail chains dm-drogerie markt and Rossmann serving as major protein snack distribution points.

U.K. Protein Snacks Market Size

The U.K. accounts for approximately 23-25% of European market share, the region's largest, driven by a highly developed sports nutrition industry, one of Europe's most active gym membership bases, and a mature protein bar retail ecosystem. Holland & Barrett and major supermarket chains, including Tesco, Sainsbury's, and Asda maintain extensive protein snack ranges, contributing to high consumer trial and repeat purchase rates.

Asia Pacific Protein Snacks Market Trends and Insights

Asia Pacific is the fastest-growing regional market, driven by China's fitness boom, where gym membership has grown exponentially in major cities and India's rapidly expanding urban health-conscious consumer base. China accounts for approximately 40-42% of Asia Pacific protein snack demand in 2025, with domestic e-commerce platforms JD.com and Tmall serving as major protein snack distribution channels for both domestic and imported brands. Japan and South Korea represent sophisticated, high-value sub-markets for premium protein formats.

India Protein Snacks Market Size

India accounts for approximately 10-12% of the Asia Pacific protein snack demand in 2025, with one of the region's fastest growth rates. India's urban fitness market is growing at 15-20% annually per industry estimates, creating an expanding consumer base for protein-enriched snacks. Domestic brands, including RiteBite Max Protein and Yoga Bar (ITC) are expanding rapidly alongside global entries from Nestlé and PepsiCo India.

Competitive Landscape

The protein snacks market is highly competitive and fragmented, characterized by the presence of multinational food manufacturers, specialized nutrition brands, and emerging startups. Competition is driven by continuous product innovation, including new flavors, clean-label formulations, and plant-based alternatives to meet evolving consumer preferences. Companies are focusing on high-protein, low-sugar, and functional positioning to differentiate their offerings. Strong distribution networks across supermarkets, convenience stores, and e-commerce platforms play a critical role in market penetration.

Key Developments

- In December 2025, Chipotle introduced its first-ever high-protein snack offering, launching a grab-and-go meat cup containing approximately four ounces of chicken or steak. The product was developed to tap into rising consumer demand for convenient, protein-rich snacking options and evolving dietary preferences.

- In March 2026, PepsiCo launched a protein-enhanced version of its Doritos chips as part of its expansion into the functional snacking segment. The product offered around 10 grams of protein per serving, contained no artificial colors or flavors, and was introduced in popular flavors such as Nacho Cheese and BBQ.

- In April 2026, Avvatar launched a limited-edition Matcha Protein Wafer Bar to reinforce its leadership in the protein snacks category and tap into evolving consumer preferences. The product featured 10g of whey protein isolate in a light wafer format combined with a globally trending matcha flavor, offering a convenient and premium snacking option.

Protein Snacks Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 22.6 Billion |

| Current Market Value (2026) | US$ 37.3 Billion |

| Projected Market Value (2033) | US$ 72.2 Billion |

| CAGR (2026 - 2033) | 9.9% |

| Leading Region | North America, 38% market share (2025) |

| Dominant Category - Product Type | Protein Bars, 34% market share (2025) |

| Top-ranking Category - Distribution Channel | Specialty Stores, 40% market share (2025) |

| Incremental Opportunity | US$ 34.9 Billion (2026 - 2033) |

Companies Covered in Protein Snacks Market

- Nestlé S.A.

- PepsiCo, Inc.

- General Mills, Inc.

- Kellogg Company

- Mondelez International, Inc.

- Mars, Incorporated

- The Hershey Company

- Hormel Foods Corporation

- Tyson Foods, Inc.

- Unilever PLC

- Abbott Laboratories

- Quest Nutrition LLC

- The Simply Good Foods Company

- Clif Bar & Company

Frequently Asked Questions

The global Protein Snacks market is estimated to be valued at US$ 37.3 billion in 2026.

The primary demand drivers are the mainstream adoption of high-protein diets, with IFIC data showing over 60% of U.S. adults actively increasing protein intake, supported by USDA/HHS Dietary Guidelines 2020-2025 and the global democratization of fitness culture, with IHRSA-reported global gym memberships exceeding 184 million.

North America leads the global Protein Snacks market with approximately 38% of market share in 2025, anchored by the U.S. as both the world's largest and most innovation-intensive protein snack market.

The most significant opportunities are Protein Chips & Crisps, the fastest-growing product type combining savory snacking format popularity with functional protein positioning, and the Asia Pacific regional expansion opportunity, where fitness culture is growing at 12-20% annually and expanding e-commerce reach are creating large and rapidly growing new consumer bases for global and regional protein snack brands through 2033.

The leading companies include Nestlé S.A., PepsiCo Inc., Kellogg Company (RXBAR), General Mills, Mondelez International, Mars Inc. (Kind), The Simply Good Foods Company (Quest, Atkins), Clif Bar & Company, Abbott Laboratories, Hormel Foods Corporation, Tyson Foods Inc., and The Hershey Company, etc.